Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

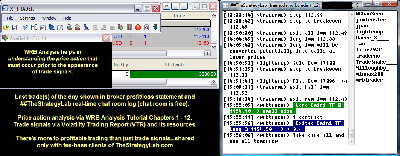

Attachment:

092214-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3380.00.png [ 176.16 KiB | Viewed 295 times ]

092214-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3380.00.png [ 176.16 KiB | Viewed 295 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,380.00 dollars or +33.80 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,380.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1892 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

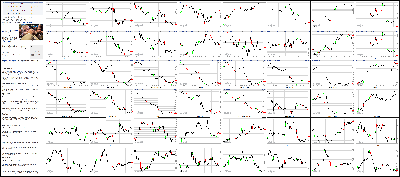

Attachment:

092214-Key-Price-Action-Markets.png [ 1.58 MiB | Viewed 333 times ]

092214-Key-Price-Action-Markets.png [ 1.58 MiB | Viewed 333 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:10 pm: [BRIEFING.COM] The stock market began the new trading week on the defensive note with small-cap stocks pacing the retreat. The Russell 2000 (-1.4%) and Nasdaq Composite (-1.1%) displayed relative weakness, while the S&P 500 lost 0.8% with all ten sectors ending in the red.

Global equities began showing some cracks overnight after China's Finance Minister Lou Jiwei poured cold water on hopes for new stimulus measures. Specifically, Mr. Lou said the government has no plans to change policies despite the recent string of disappointing data. A somewhat similar hawkish tone was conveyed by comments from Japan's Economy Minister Akira Amari, who said his country's government remains on track to implement another consumption tax hike.

The macroeconomic concerns have led to weakness in equities, while also weighing on growth-sensitive commodities like copper (-1.6% to $3.04/lb) and crude oil (-0.9% to $90.80/bbl). Unlike last week, the losses were not driven by a stronger dollar as the Dollar Index ended flat after wiping out its overnight decline.

Meanwhile, the weakness in crude prices spilled over to the energy sector (-1.4%), which slumped out of the gate and spent the entire day among the laggards. The sector widened its September loss to 5.6% and is now down 7.2% during the third quarter.

Similar to energy, the consumer discretionary sector (-1.5%) lagged from the start with high-beta names like Amazon.com (AMZN 324.50, -6.82), Netflix (NFLX 442.78, -14.74), Priceline.com (PCLN 1165.79, -20.33) exerting notable pressure. The three lost between 1.7% and 3.2%. Homebuilders also weighed on the sector following today's disappointing Existing Home Sales report. The iShares Dow Jones US Home Construction ETF (ITB 23.24, -0.50) lost 2.1%.

Elsewhere among cyclical groups, the financial sector (-0.7%) displayed relative strength in the morning, but settled just ahead of the broader market. The technology sector (-0.8%) also finished near the broader market, while industrials (-1.1%) were pressured by transports. The Dow Jones Transportation Average fell 1.4%.

Also of note, the materials sector (-0.1%) spent the bulk of the session in the green, but was pressured into negative territory by the close. The relative strength stemmed from a 33.2% surge in Sigma-Aldrich (SIAL 136.40, +34.03) after the company agreed to be acquired by Merck KGaA (MKGAF 93.70, +4.20) for $140.00/share, which represents a 37.0% premium to Friday's closing price.

On the countercyclical side, consumer staples (-0.2%) and telecom services (-0.1%) displayed relative strength, while utilities (-0.7%) ended near the S&P 500. For its part, the health care sector (-0.6%) outperformed even as biotechnology struggled. The iShares Nasdaq Biotechnology ETF (IBB 272.55, -2.68) lost 1.0%.

Treasuries ended near their highs after spending the day in the green. The 10-yr yield slipped one basis point to 2.56%.

Participation was in line with recent averages as more than 680 million shares changed hands at the NYSE.

Economic data was limited to the Existing Home Sales for August, which fell 1.8% to 5.05 million SAAR from a slightly downwardly revised 5.14 million SAAR (from 5.15 million SAAR) in July, while the Briefing.com consensus expected an increase to 5.20 million. The report revealed the first monthly drop in sales since March and overall sales are still down 5.3% year-over-year.

Tomorrow, the July FHFA Housing Price Index will be released at 9:00 ET.

Nasdaq Composite +8.4% YTD

S&P 500 +7.9% YTD

Dow Jones Industrial Average +3.6% YTD

Russell 2000 -2.8% YTD

3:25 pm: [BRIEFING.COM] The commodity complex was pressured by global macroeconomic concerns, while the Dollar Index was able to erase its overnight loss.

Dec gold spent the bulk of the overnight session in the red, but jumped from lows to highs in the $1220.00/ozt area after the release of today's disappointing Existing Home Sales report. The yellow metal then retreated from its high, ending with a slim gain of 0.1% at $1218.20/ozt.

Dec silver started with a sharp overnight loss that placed the metal at $17.50/ozt; however, a steady recovery off that low, put the metal at $17.77/ozt, representing a decline of 0.4%.

Nov crude oil traded little changed in the morning, but spent the bulk of the day in a slide from the early high. The energy component marked a low in the $90.43/bbl area before settling lower by 0.9% at $90.80/bbl.

Oct natural gas spent some time on each side of its flat line, peaking at $3.88/MMBtu before sliding to a low near $3.81/MMBtu. A subsequent recovery placed natural gas at $3.85/MMBtu by the close for one-cent loss.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.8% with one hour remaining in the first session of the week. This morning was very quiet on the economic front with participants receiving just one report-August Existing Home Sales. Tomorrow's session will be equally as quiet with economic data limited to the FHFA Housing Price Index for July.

The remainder of the week will feature August Durable Orders (Briefing.com consensus -16.3%) and the third revision of Q2 GDP with the latter set to be released on Friday morning. The Briefing.com consensus expects the reading to be revised up to 4.6% from 4.2%.

2:25 pm: [BRIEFING.COM] Not much change in the major averages as they continue hovering near their lowest levels of the day. The S&P 500 (-0.8%) notched its session low around 12:00 ET and has maintained a seven-point range since then. Meanwhile, the price-weighted Dow Jones Industrial Average (-0.5%) continues trading a little ahead of the benchmark index.

Six Dow components remain in the green, but the leading performer, DuPont (DD 71.75, +0.50), is the only stock showing an increase larger than 0.4%. On the downside, six index members are lower by 1.0% or more with Nike (NKE 80.59, -1.22) sporting the largest decline. The apparel retailer has given up 1.5%.

2:00 pm: [BRIEFING.COM] Equity indices remain near their lows with the S&P 500 trading down 0.8%. The consumer discretionary sector (-1.5%) slumped to the bottom of the leaderboard at the start and the growth-sensitive sector remains behind the other nine groups at this juncture.

High-beta names like Amazon.com (AMZN 321.92, -9.40), Netflix (NFLX 439.80, -17.72), and Priceline.com (PCLN 1157.78, -28.34) have contributed to the underperformance with losses ranging from 2.4% to 2.9%. Meanwhile, retailers also lag with the SPDR S&P Retail ETF (XRT 87.24, -1.30) down 1.5%.

Elsewhere, Treasuries have returned into the middle of their trading range. The 10-yr yield is down one basis point at 2.57%.

1:30 pm: [BRIEFING.COM] The major indices continue to struggle under the weight of profit taking that has hit far and wide.

Not surprisingly, after a big run in the market, valuation concerns are being discussed in the foreground as concerns in the background about growth rates in China and the EU, as well as the US following the weaker than expected existing home sales report for August, have kept buyers at bay.

Continued weakness in the small-cap Russell 2000 (-1.5%) is also weighing on sentiment. Most companies domiciled there have a domestic orientation, so the underperformance may be raising concerns that the US economy isn't faring as well as some pundits are suggesting and/or won't be insulated from a slowdown in China and the EU should conditions there continue to deteriorate.

Weakness in commodities, which can't be attributed to a big move in the greenback today, has contributed to the narrative today that growth concerns are pulling stock prices lower. The CRB Index is down 0.8%.

12:55 pm: [BRIEFING.COM] Equity indices sit near their lows at midday with small caps leading the retreat. The Russell 2000 (-1.4%) and Nasdaq Composite (-1.2%) trail the S&P 500 (-0.7%), while the Dow Jones Industrial Average (-0.4%) has resisted some of the selling pressure.

The stock market has been pressured since the get go after overnight comments from China's Finance Minister Lou Jiwei poured cold water on hopes for new stimulus measures. Specifically, Mr. Lou said the government has no plans to change policies following the recent string of disappointing data.

A somewhat similar hawkish tone stemmed from comments made by Japan's Economy Minister Akira Amari, who said Japan's government remains on track to implement another consumption tax hike.

Overall, the concerns have translated into broad weakness for equities and growth-sensitive commodities like copper (-1.6% at $3.04/lb) and crude oil (-1.1% at $90.68/bbl). Furthermore, the Dollar Index holds a slim gain (+0.1%) after wiping out its overnight loss.

The noteworthy decline in crude oil has weighed on the energy sector (-1.2%), which is the second-weakest performer of the day. Meanwhile, the biggest laggard-consumer discretionary (-1.5%)-has been pressured by losses among high-beta names like Netflix (NFLX 440.56, -16.96) and Priceline.com (PCLN 1155.09, -31.03). Homebuilders haven't fared much better with the iShares Dow Jones US Home Construction ETF (ITB 23.30, -0.44) down 1.8%.

Elsewhere, the top-weighted sector-technology (-0.8%)-trails the broader market, while the materials space (+0.1%) has been able to stay in the green thanks a boost from Sigma-Aldrich (SIAL 136.53, +34.16), which has surged 33.4% after agreeing to be acquired by Merck KGaA (MKGAF 89.50, 0.00) for $140.00/share, representing a 37.0% premium to Friday's closing price.

The countercyclical side has fared a bit better with consumer staples (-0.1%), telecom services (-0.5%), and utilities (-0.5%) trading ahead of the broader market, while health care (-0.7%) lags amid weakness in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 271.14, -4.09) is lower by 1.5%.

Treasuries are near their highs with the 10-yr yield down two basis points at 2.56%.

Economic data was limited to the Existing Home Sales for August, which fell 1.8% to 5.05 million SAAR from a slightly downwardly revised 5.14 million SAAR (from 5.15 million SAAR) in July, while the Briefing.com consensus expected an increase to 5.20 million. The report revealed the first monthly drop in sales since March and overall sales are still down 5.3% year-over-year.

12:30 pm: [BRIEFING.COM] After spending the first two hours of the trading day in a steady slide, the S&P 500 has maintained a four-point range over the past 60 minutes.

The materials sector (+0.1%) has been able to stay out of the red, but its slim gain is now in jeopardy following an orderly decline from the opening high. Steelmakers have factored into the retreat as evidenced by a 2.9% decline in the Market Vectors Steel ETF (SLX 47.23, -1.40). Miners haven't done much to turn the tide with the Market Vectors Gold Miners ETF (GDX 22.23, -0.43) trading down 1.9%.

With stocks on their lows, participants have shown increased demand for volatility protection. The CBOE Volatility Index (VIX 13.89, +1.78) has approached the 14.00% mark.

12:00 pm: [BRIEFING.COM] Recent action saw the key indices inch to fresh lows for the session. Including today's decline of 0.8%, the S&P 500 is lower by 0.5% so far in September. Despite the loss for the month, the benchmark index has fared a bit better than its higher-beta peers. On that note, the Nasdaq has given up 1.3% so far this month, while the Russell 2000 is down 3.7% for the month. Elsewhere, the price-weighted Dow (-0.5%) trades ahead of the broader market today and is up 0.6% for the month.

Also of note, Treasuries slumped in the morning, but the broad-based weakness in equities has caused a rebound to a fresh high. The 10-yr note is higher by seven ticks with its yield down three basis points at 2.55%.

11:25 am: [BRIEFING.COM] The major averages remain pressured with the S&P 500 trading lower by 0.7%. Two cyclical sectors-consumer discretionary (-1.4%) and energy (-1.2%)-began the session well behind the broader market and the pair remains at the bottom of the leaderboard at this time.

Meanwhile, other growth-sensitive groups are a bit mixed. Financials (-0.3%) and materials (+0.2%) outperform, while industrials (-0.8%) and technology (-0.8%) trade just behind the broader market.

The countercyclical side looks a bit better with consumer staples (-0.2%), telecom services (-0.1%), and utilities (-0.2%) trading ahead of the S&P 500, while health care (-0.6%) has been pressured by biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 271.74, -3.50) is lower by 1.3%.

10:55 am: [BRIEFING.COM] Equity indices have continued their retreat with small-cap stocks leading the slide. As a result, the Russell 2000 (-1.5%) trades near the Nasdaq Composite (-1.2%), while the S&P 500 (-0.7%) hovers a bit ahead of the other indices.

The relative weakness of small caps has carried over into high-beta areas like biotechnology and chipmakers. The iShares Nasdaq Biotechnology ETF (IBB 270.84, -4.39) is lower by 1.6%, while the PHLX Semiconductor Index trades down 1.1%.

Elsewhere, the Dow (-0.4%) has held up relatively well with 10 of its 30 components holding gains at this juncture. On the downside, Caterpillar (CAT 101.14, -1.37) is the weakest performer with a 1.3% decline.

10:30 am: [BRIEFING.COM] Precious metals are trading lower this morning. Dec gold brushed a session low of $1212.50 in recent action and is now down 0.2% at $1214.60. Dec silver traded as low as $17.57 but has been inching higher in recent trade. It is currently at $17.71, or 0.8% lower.

Nov crude oil pulled back from its session high of $91.82 set at pit trade open and is slipping deeper into negative territory. It touched a LoD of $90.77 and is currently down 0.9% at $90.86.

Oct natural gas, on the other hand, is trading higher in a tight range between $3.85 and $3.88. It is now up 0.4% at $3.85.

10:00 am: [BRIEFING.COM] The S&P 500 trades lower by 0.4%, while the Russell 2000 (-0.9%) underperforms.

Just reported, existing home sales hit an annualized rate of 5.05 million units in August, while the Briefing.com consensus expected a reading of 5.20 million. The pace for August was up from the prior month's revised rate of 5.14 million units (from 5.15 million).

9:45 am: [BRIEFING.COM] Equity indices began the session on the defensive amid broad-based weakness. The S&P 500 trades lower by 0.4% with nine sectors holding opening losses. Most notably, heavily-weighted consumer discretionary (-0.7%) and energy (-0.7%) sectors have pressured the broader market, while the materials sector (+0.4%) outperforms amid relative strength in paper manufacturers.

Despite its relative strength, the materials sector only represents 3.5% of the entire market. Meanwhile, another cyclical sector, financials, also trades ahead of the broader market with a slim loss of 0.1%.

Treasuries have slid to lows over the past 30 minutes, sending the 10-yr yield back to unchanged for the day (2.57%).

The Existing Home Sales report for August will be released at 10:00 ET (Briefing.com consensus 5.20 million)

9:16 am: [BRIEFING.COM] S&P futures vs fair value: -5.80. Nasdaq futures vs fair value: -12.00. The stock market is on track for a cautious start to the week as futures on the S&P 500 hover six points below fair value. Index futures dropped overnight, but have recovered nearly half of their original losses.

The initial weakness took place after China's Finance Minister Lou Jiwei played down expectations for additional easing measures from the government. A similar tone emanated from the European Central Bank with Governing Council member Ignazio Visco saying recent easing measures have worked as planned. Also of note, Japan's Economy Minsiter Akira Amari played up expectations of a consumption tax hike going forward.

The hawkish undertone to commentary from three major economies has translated into defensive action in futures. Conversely, Treasuries have been in demand with the 10-yr note sitting near its high with the benchmark yield at 2.56%.

On the corporate front, Yahoo! (YHOO 40.01, -0.91) is indicated to open lower by 2.2% on heavy volume after being downgraded at Bank of America/Merrill Lynch and Bernstein.

Elsewhere, Dresser-Rand (DRC 82.10, +2.19) has agreed to be acquired by Siemens (SIEGY 124.00, 0.00) for $83.00/share, representing a 37.4% premium to DRC price on July 16, 2014 when merger speculation first took place. Separately, Sigma-Aldrich (SIAL 137.78, +35.41) will be acquired by Merck KGaA (MKGAF 89.50, 0.00) for $140.00/share, which represents a 37.0% premium to Friday's closing price.

Treasuries are near their highs with the 10-yr yield down two basis points at 2.56%.

8:58 am: [BRIEFING.COM] S&P futures vs fair value: -6.10. Nasdaq futures vs fair value: -12.80. The S&P 500 futures trade six points below fair value.

Markets ended lower across most of Asia. Notably, Chinese Finance Minister Lou Jiwei suggested Beijing has no plans to adjust its current policy path despite the recent slowdown.

Economic data was limited:

New Zealand's Westpac Consumer Sentiment dropped to 116.7 from 121.2

Hong Kong's CPI slowed to 3.9% year-over-year (expected 4.0%; prior 4.0%) and the current account deficit widened to HKD8.94 billion from HKD4.43 billion, while the unemployment rate slipped to 3.9% from 4.0%.

------

Japan's Nikkei lost 0.7%, sliding off seven-year highs. Heavyweight Softbank tumbled 6.1% as traders sold the news of the Alibaba IPO after shares saw a big run up into the event.

Hong Kong's Hang Seng lost 1.4%, slumping to its lowest level in two months. Traders booked profits in shares of internet gaming giant Tencent Holdings, pushing the stock down 3.3%.

China's Shanghai Composite fell 1.7% to a two-week low. Financials led to the downside with China Pacific Insurance shedding 3.8%.

India's Sensex added 0.4%, finishing just shy of all-time highs. Automaker Tata Motors reversed its recent weakness, adding 3.9%.

Major European indices trade in the red with Great Britain's FTSE (-0.7%) and Italy's MIB (-0.9%) trailing the region. After the close on Friday, Moody's affirmed France at Aa1 with a 'Negative' outlook. Separately, European Central Bank Governing Council member Ignazio Visco discussed policy, saying the recent easing steps have pressured the euro, suggesting additional easing will remain on hold for the time being.

Economic data included just one report: o Italy's Industrial New Orders fell 1.5% month-over-month (expected 1.1%; previous -2.1%), while the year-over-year reading fell 0.7% (prior -2.5%)

------

Germany's DAX is lower by 0.2% with exporters on the defensive. BMW and Daimler hold respective losses of 2.6% and 1.4%. Merck KGaA outperforms with an increase of 6.5% after agreeing to acquire Sigma-Aldrich.

France's CAC trades down 0.2% amid weakness in consumer names. Accor, Danone, Kering, and LVMH Moet Hennessy are down between 0.8% and 1.2%. Steelmaker Vinci leads with an increase of 1.0%.

Great Britain's FTSE holds a loss of 0.7%. Miners lag with Anglo American, Antofagasta, Glencore, and Rio Tinto down between 2.1% and 3.1%. Also of note, Tesco has tumbled 8.5% in reaction to its profit warning.

Italy's MIB has given up 0.9% amid weakness in financials. Banco Popolare, BMPS, and Banca Pop Emilia Romagna are down between 1.8% and 2.7%.

8:28 am: [BRIEFING.COM] S&P futures vs fair value: -5.50. Nasdaq futures vs fair value: -11.80. U.S. equity futures continue holding modest losses with the S&P 500 futures down six points below fair value.

The Dollar Index began the night in the red after gaining 0.6% last week, but a steady rally off the lows has placed the index back near its flat line for the session. The dollar is currently little changed versus the yen (109.05), while the euro (1.2844) and the pound (1.6330) continue holding slim gains against the greenback.

On the commodity side, both crude oil ($91.63/bbl) and gold futures ($1217.20/ozt) are little changed, while copper futures have tumbled 1.6% to $3.042/lb amid growth concerns in China.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -5.80. Nasdaq futures vs fair value: -12.80. U.S. equity futures trade modestly lower amid cautious action overseas. The S&P 500 futures hover six points below fair value after climbing off their overnight lows reached during the Asian session. The night has been very quiet on the economic front with several central bank and government officials playing down expectations of additional stimulus. On that note, China's Finance Minister Lou Jiwei said the government has not changed policies following the recent string of disappointing data, while Japan's Economy Minsiter Akira Amari played up expectations of a consumption tax hike going forward.

Treasuries hold slim gains with the 10-yr yield at 2.56%.

In U.S. corporate news of note:

AutoZone (AZO 525.00, -1.44): -0.3% despite beating bottom-line estimates on light revenue.

Dresser-Rand (DRC 81.60, +1.69): +2.1% after agreeing to be acquired by Siemens (SIEGY 124.00, 0.00) for $83.00/share, representing a 37.4% premium to DRC price on July 16, 2014 when merger speculation first took place.

Sigma-Aldrich (SIAL 137.45, +35.08): +34.3% after agreeing to be acquired by Merck KGaA (MKGAF 89.50, 0.00) for $140.00/share, representing a 37.0% premium to Friday's closing price.

Reviewing overnight developments:

Asian markets ended on a lower note. China's Shanghai Composite -1.7%, Hong Kong's Hang Seng -1.4%, and Japan's Nikkei -0.7%

Economic data was limited:

New Zealand's Westpac Consumer Sentiment dropped to 116.7 from 121.2

Hong Kong's CPI slowed to 3.9% year-over-year (expected 4.0%; prior 4.0%)

In news:

China's Finance Minister Lou Jiwei said the country's government does not plan to change its economic policies despite disappointing data received in August

Japan's Economy Minister Akira Amari hinted at an increased likelihood that a consumption tax hike will go into effect

Major European indices trade in mixed fashion. Germany's DAX +0.1%, Great Britain's FTSE -0.7%, and France's CAC is flat. Elsewhere, Italy's MIB -0.8% and Spain's IBEX -0.1%

In economic data:

Italy's Industrial New Orders fell 1.5% month-over-month (expected 1.1%; previous -2.1%), while the year-over-year reading fell 0.7% (prior -2.5%)

Among news of note:

European Central Bank Governing Council member Ignazio Visco discussed policy, saying the recent easing steps have pressured the euro, suggesting additional easing will remain on hold for the time being

After the close on Friday, Moody's affirmed France at Aa1 with a 'Negative' outlook

6:18 am: [BRIEFING.COM] S&P futures vs fair value: -8.00. Nasdaq futures vs fair value: -19.00.

6:18 am: [BRIEFING.COM] Nikkei...16,205.90...-115.30...-0.70%. Hang Seng...23,955.49...-350.70...-1.70%.

6:18 am: [BRIEFING.COM] FTSE...9,776.10...-35.50...-0.50%. DAX...9,776.10...-23.80...-0.20%.

Treasuries Gain a Third Day as Dudley Asks for Patience By Cordell Eddings Sep 22, 2014 5:07 PM ET

Treasuries gained for a third day, the longest rally this month, after Federal Reserve Bank of New York President William Dudley argued for “patience” on interest-rate increases.

Benchmark 10-year note yields fell to the lowest in a week as billionaire Julian Robertson said there’s a bubble in bonds that will end “in a very bad way.” Treasury market inflation bets dropped to a 14-month low and a decrease in investor purchases prompted an unexpected decline in sales of U.S. existing homes in August.

“It’s been a risk-off day with Dudley talking down the Fed’s projections,” said Larry Milstein, managing director in New York of government-debt trading at R.W. Pressprich & Co. “The data hasn’t borne them out yet. And often the Fed is inaccurate in their economic-growth expectations.”

Benchmark Treasury 10-year yields fell one basis point, or 0.01 percentage point, to 2.56 percent as of 5 p.m. New York time after touching 2.55 percent, the least since Sept. 12, according to Bloomberg Bond Trader prices. The price of the 2.375 percent note maturing in August 2024 rose 3/32, or 94 cents per $1,000 face value, to 98 11/32. The last three-day rally ended Aug. 25.

The yield has traded between 2.55 percent and 2.65 percent since Sept. 15.

“‘Buy the dip’ should be the mentality at this point, as we get closer to 2.60 percent,” said Milstein.

Global RallyThe Treasury will auction $29 billion of two-year notes tomorrow, $35 billion of five-year debt on Sept. 24, and $29 billion of seven-year securities on Sept. 25. It will also sell $13 billion of two-year floating-rate notes on Sept. 24.

“We are seeing a risk-off trade that is supporting a rally in global bonds, and by extension the Treasury market, despite the incoming supply,” said Adrian Miller, director of fixed-income strategies at GMP Securities LLC in New York. “The 10-year note is fairly valued at this level, given inflation expectations.”

Inflation running below the Fed’s 2 percent target argues for “patience” on interest-rate increases and may require letting the economy run “a little hot,” Dudley said today at the Bloomberg Markets Most Influential Summit in New York.

“We really need the economy to run a little hot, at least for some period of time,” Dudley said.

Fed policy makers announced last week an increase in their median estimate for the fed funds rate at the end of 2015 to 1.375 percent, compared with 1.125 percent in June. The rate has been held at zero to 0.25 percent since 2008.

Robertson’s View“Bonds are at ridiculous levels,” Robertson, the founder of Tiger Management LLC, said at the Bloomberg summit. “It’s a worldwide phenomenon that governments are buying bonds to keep their countries moving along economically.”

Robertson was joined on stage by Carlyle Group LP co-founder William Conway, who said he didn’t see a catalyst that would cause the bond market collapse. Interest rates will stay low and asset prices remain elevated, he said.

Treasuries rose earlier after existing-home sales last month were 5.05 million, versus an estimate of 5.2 million, according to the National Association of Realtors. July’s sale were 5.14 million, revised from 5.15 million.

U.S. economic activity fell in August, according to the Fed Bank of Chicago. Its national index, which draws on 85 economic indicators, was minus 0.21 in August. A reading below zero indicates below-trend-growth in the national economy and a sign of easing pressures on future inflation.

‘Considerable Time’Getting in the way of the Fed tightening monetary policy “is the question of how the Fed is going to achieve this without the support of a lot of growth and an inflation trigger,” Kevin Giddis, head of fixed income capital markets in Memphis at Raymond James & Associates Inc. wrote in a note to clients. “The market still has it right and that rates will remain low for even more of a ‘considerable time’ than people may want to believe.”

The Fed’s preferred price index rose 1.6 percent in July from the year before, based on the latest Commerce Department data, and it has been less than the central bank’s 2 percent target for more than two years.

The implied yield on 30-day federal funds futures contracts expiring in September 2015 was 0.5 percent, indicating traders expect the Fed to increase its target rate from the current range of zero to 0.25 percent by then.

Gains in longer-dated bonds, the securities that benefit most from low inflation, narrowed the yield difference between 10- and 30-year Treasuries to a five-year low of 70 basis points.

The yield difference between 10-year notes and similar-maturity Treasury Inflation Protected Securities, a gauge of expectations for consumer prices over the life of the debt, narrowed to 1.99 percentage points, the least since July 2013.

To contact the reporter on this story: Cordell Eddings in New York at

ceddings@bloomberg.netTo contact the editors responsible for this story: Dave Liedtka at

dliedtka@bloomberg.net Kenneth Pringle

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage