Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

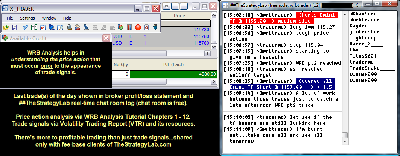

Attachment:

090914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4980.00.png [ 176.15 KiB | Viewed 341 times ]

090914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4980.00.png [ 176.15 KiB | Viewed 341 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$4,980.00 dollars or +49.80 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $4,980.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1883 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

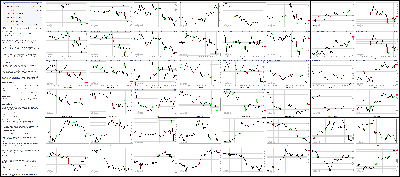

Attachment:

090914-Key-Price-Action-Markets.png [ 1.29 MiB | Viewed 327 times ]

090914-Key-Price-Action-Markets.png [ 1.29 MiB | Viewed 327 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:10 pm: [BRIEFING.COM] The major averages ended the Tuesday session on their lows with the S&P 500 sliding 0.7%. Small-cap stocks outperformed yesterday, but the Russell 2000 erased Monday's uptick with a 1.2% decline.

Equity indices spent the entire session in the red with the early pressure coming from the financial sector (-1.0%). The second-largest group by market cap slumped out of the gate amid broad weakness in top-weighted components. Bank of America (BAC 16.14, -0.21), Citigroup (C 51.27, -0.78), and JPMorgan Chase (JPM 59.06, -0.83) lost between 1.3% and 1.5%, while the sector acted as a drag on the market throughout the session.

Meanwhile, the consumer discretionary space (-1.0%) also weighed with the SPDR S&P Retail ETF (XRT 88.06, -0.86) falling 1.0%. The quick-service restaurant space did not fare much better as McDonald's (MCD 91.09, -1.41) fell 1.5% after reporting a 3.7% decline in comparable store sales during August. The decline was paced by a 14.5% slump in Asia following the recent food safety scandal.

Elsewhere, the top-weighted sector-technology (-0.6%)-endured a choppy session before settling on its low. Shares of Apple (AAPL 97.99, -0.37) were responsible for the volatile action, with the stock surging on the announcement that near field communication capabilities will be included in the upcoming version of the iPhone. Despite the spike, Apple slumped from highs to lows after revealing the long-rumored "Apple Watch," which will be available next year.

Combined with the underperformance of the aforementioned sectors, the afternoon retreat in Apple pressured the market to fresh lows.

Despite the weakness in three top-weighted sectors, another influential group-health care (-0.3%)-kept the market from extending its loss. Insurers and managed care names outperformed, while biotechnology slumped. Tenet Healthcare (THC 60.97, +1.98) jumped 3.4% after Deutsche Bank added the stock to its short-term buy list, while the iShares Nasdaq Biotechnology ETF (IBB 269.60, -3.46) fell 1.3%.

Similar to health care, the consumer staples sector (-0.3%) outperformed, while telecom services (-1.2%) and utilities (-1.2%) lagged.

Economic data was limited to the Job Openings and Labor Turnover Survey for July, which indicated job opening decreased to 4.673 million from 4.675 million.

Tomorrow, the weekly MBA Mortgage Index will be released at 7:00 ET, while the Wholesale Inventories report for July (Briefing.com consensus 0.5%) will cross the wires at 10:00 ET.

Nasdaq Composite +9.0% YTD

S&P 500 +7.6% YTD

Dow Jones Industrial Average +2.6% YTD

Russell 2000 -0.4% YTD

3:30 pm: [BRIEFING.COM]

Dec gold extended yesterday's losses as a slightly stronger dollar index weighed on prices. The yellow metal brushed a session high of $1258.10 per ounce in early morning pit trade but slipped into the red as the session progressed.

It traded as low as $1248.10 per ounce, its lowest level since June, and settled with a 0.5% loss at $1248.60 per ounce.

Dec silver also retreated into negative territory after touching a session high of $19.08 per ounce in morning action. It eventually settled at $18.92 per ounce, or 0.3% lower.

Oct crude oil touched a session high of$93.68 per barrel as floor trade opened but pulled back as the session progressed. It brushed a session low of $92.52 per barrel and settled at $92.73 per barrel, or 0.1% higher.

Oct natural gas extended yesterday's gains as it rose from a session low of $3.93 per MMBtu. It traded as high as $4.02 per MMBtu and settled with a 2.6% gain at $3.98 per MMBtu.

3:05 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.5% with one hour remaining in the session. The benchmark index finds itself right back on its low following a volatile afternoon. Shares of Apple (AAPL 99.16, +0.80) have contributed to the whipsaw trade, and like the S&P 500, the top-weighted tech stock sits on its low going into the last hour of action.

Elsewhere, small caps remain weak with the Russell 2000 now lower by 1.0%. Similarly, biotechnology names lag with the iShares Nasdaq Biotechnology ETF (IBB 270.50, -2.56) down 0.9%.

2:30 pm: [BRIEFING.COM] Equity indices have returned to their lows following a brief spike that was aided by a rally in the shares of Apple (AAPL 99.66, +1.30). Similar to the broader market, the top-weighted tech stock has slid from its best level of the day after the company revealed a digital watch, which had been expected. Meanwhile, the technology sector (-0.1%) has dipped back below its flat line.

Elsewhere, Treasuries continue respecting narrow ranges with the 10-yr note lower by seven ticks (2.50%).

2:00 pm: [BRIEFING.COM] The S&P 500 (-0.1%) has climbed to its best level since the opening print, while shares of Apple (AAPL 102.76, +4.40) have extended to a new high after the company revealed NFC technology in its iPhone devices and announced the "Apple Watch."

The strength in Apple has bolstered the technology sector, which now trades higher by 0.7%. Outside of technology, energy (+0.1%), industrials (+0.1%), and health care (+0.1%) also hover in the green at this juncture.

On the downside, consumer discretionary (-0.4%) and financials (-0.6%) continue showing relative weakness.

1:25 pm: [BRIEFING.COM] With Apple's (AAPL 99.32, +0.96) "special event" now underway, the remainder of the afternoon session will assuredly produce a lot of talk/debate about what Apple's new product launches mean for the company and its earnings prospects.

The lead headline thus far is that Apple has unveiled iPhone 6 and iPhone 6 Plus. The former will have a 4.7 inch screen size and the latter will have a 5.5 inch screen size, as expected.

Apple, which has a history of selling off after new product announcements (because it runs in anticipation of the announcement), has faded from its earlier highs, producing a slight downtick in the broader market since our last update..

Separately, the Treasury conducted a $27 bln 3-yr note auction that was deemed to be mixed in terms of the response. The 3-yr drew a high yield of 1.066% on a 3.17 bid-to-cover ratio. The latter was below the prior 12-auction average of 3.32. Indirect bidders, however, took 33.1% of the supply versus a 12-auction average of just 18.8%. The 10-yr note (-8/32, 2.50%) is probing its lows for the day following the auction.

1:00 pm: [BRIEFING.COM] Equity indices trade lower across the board at midday with the S&P 500 down 0.4%. Small caps displayed relative strength yesterday, but they are giving back those gains today with the Russell 2000 trading lower by 0.9%.

The S&P 500 slipped out of the gate amid weakness in all ten sectors with financials (-0.8%) leading the market lower. The influential group has ticked up off its low since then, but continues showing relative weakness with Citigroup (C 51.45, -0.60), Goldman Sachs (GS 178.30, -1.81), and JPMorgan Chase (JPM 59.00, -0.89) down between 1.0% and 1.5%.

The benchmark index was able to halt its slide near the 1,990 level before reclaiming roughly a half of its loss. Although all ten sectors remain in the red, energy (-0.2%), industrials (-0.2%), technology (unch), and health care (-0.1%) have approached their respective flat lines.

Of the four groups, the tech sector has received support from Apple (AAPL 100.03, +1.68), which has added 1.7% ahead of its product refresh event set to begin at 13:00 ET. In the past, shares of Apple have sold off in reaction to product announcements. If that pattern continues today, investors should not be surprised to see additional losses in the S&P 500, which has been lifted off the lows by Apple's strength.

Elsewhere, the health care sector trades a bit ahead of the market amid strength in hospital and insurer names. Tenet Healthcare (THC 61.56, +2.57) trades up 4.4% after Deutsche Bank added the stock to its short-term buy list, while Humana (HUM 130.27, +0.72) and UnitedHealth Group (UNH 88.25, +0.34) are both up near 0.5%. Biotech names have not been as fortunate with the iShares Nasdaq Biotechnology ETF (IBB 271.05, -2.01) trading lower by 0.7%.

Treasuries have maintained a narrow range near their lows with the 10-yr yield up four basis points at 2.50%.

Economic data was limited to the Job Openings and Labor Turnover Survey for July, which indicated job opening decreased to 4.673 million from 4.675 million.

12:25 pm: [BRIEFING.COM] The major averages continue drifting along their recent levels. Although the S&P 500 (-0.3%) has climbed off its low, it still has some work left ahead of it with all ten sectors trading in the red.

Overall, cyclical sectors continue trading in mixed fashion with respect to the broader market. Consumer discretionary (-0.6%), financials (-0.7%), and materials (-0.5%) underperform, while energy (unch), industrials (-0.1%), and technology (+0.1%) display relative strength.

Notably, the tech sector has received significant support from shares of Apple (AAPL 100.24, +1.88) with the company's product refresh event scheduled for the top of the hour. In the past, Apple has sold off after revealing updated products and a continuation of that pattern would leave the market vulnerable to additional downside.

12:00 pm: [BRIEFING.COM] Equity indices remain near their recent levels with the S&P 500 (-0.3%) trading right in the middle of today's range.

The energy sector (+0.3%) has built on its early strength, but despite today's outperformance, the growth-sensitive group is the weakest performer so far in the third quarter. The sector has surrendered 4.5% since the start of July, while the second-weakest performer-utilities-has given up 3.5% in Q3.

Meanwhile, the other commodity-related sector-materials (-0.6%)-underperforms with Mosaic (MOS 46.14,-1.00) lower by 2.1% after RBC Capital Markets downgraded the stock to 'Sector Perform' from 'Outperform.'

11:30 am: [BRIEFING.COM] The S&P 500 (-0.3%) has inched up from its session low, but nine sectors continue trading in the red. To be fair, health care, industrials, and technology hover within 0.1% of their respective flat lines.

Interestingly, the health care sector posted a slim gain of 0.1% yesterday with biotechnology overshadowing the relative weakness among hospital and managed health care names. Today, the tables have turned and biotechnology lags with the iShares Nasdaq Biotechnology ETF (IBB 271.83, -1.23) down 0.5%, while insurers and hospital stocks outperform.

Tenet Healthcare (THC 61.82, +2.83) has added 4.8% after Deutsche Bank added the stock to its short-term buy list. Elsewhere, Humana (HUM 130.80, +1.25) and UnitedHealth Group (UNH 88.42, +0.51) are up 1.0% and 0.6%, respectively.

11:00 am: [BRIEFING.COM] Equity indices remain pressured with the S&P 500 (-0.4%) trading near its worst level of the session. Meanwhile, small-cap stocks are showing relative weakness as evidenced by a 0.8% decline for the Russell 2000. Yesterday, the index posted a slim gain of 0.2%, while the S&P 500 ended in the red. Today, however, the Russell is struggling to keep up with the broader market.

At the start of today's session we pointed out the underperformance of the financial sector. Since then, the second-largest sector by weight has extended its loss to 1.0%. Top-weighted components haven't fared much better with Bank of America (BAC 16.17, -0.18), Citigroup (C 51.32, -0.73), and JPMorgan Chase (JPM 58.93, -0.96) down between 1.1% and 1.6%.

On the upside, the energy sector (+0.2%) is the lone advancer at this juncture, while crude oil is higher by 0.6% at $93.19/bbl.

10:30 am: [BRIEFING.COM]

The dollar index pulled back from its overnight high and is now, which has provided some relief for select commodities

However, its now back up 0.1% at 84.31

Natural gas surged higher this morning, rising over $4/MMBtu.

Oct NG is now +2.3% at $3.97/MMBtu

Dec copper tanked this morning to a LoD at $3.10/lb. Copper is now -2.2% at $3.10/lb

Oct crude oil has pulled back off its HoD of $93.94/barrel and is now +0.5% at $93.11/barrel

Dec gold is +0.1% at $1255.70/oz, Sept silver is +0.02% at $18.97/oz

10:05 am: [BRIEFING.COM] The S&P 500 (-0.5%) has continued its retreat, but the energy sector (unch), which plunged 1.6% yesterday has returned to its flat line. Technology (-0.1%) follows not far behind, while consumer discretionary (-0.6%), financials (-0.9%), and health care (-0.5%) continue showing relative weakness.

Just released, the Job Openings and Labor Turnover Survey for July indicated job opening decreased to 4.673 million from 4.675 million.

9:40 am: [BRIEFING.COM] Equity indices slipped out of the gate with all ten sectors showing early losses. The S&P 500 trades down 0.3% with the financial sector (-0.7%) displaying the largest decline.

Elsewhere, the utilities sector (-0.7%) sports a comparable loss, while the remaining sectors trade closer to their flat lines. Furthermore, the consumer discretionary sector (-0.4%) and health care (-0.4%) deserve close attention as the two influential groups appear among the early laggards.

Treasuries remain near their lows with the 10-yr yield at 2.49%.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: -3.30. Nasdaq futures vs fair value: -4.80. The stock market is on track for a lower start as futures on the S&P 500 hover three points below fair value. Futures hovered near their highs about three hours ago, but have since returned to overnight lows. Overseas action has been fairly subdued with markets in Asia ending little changed. Meanwhile, European indices have dropped to fresh lows with Spain's IBEX (-0.9%) leading the slide amid broad weakness.

Notably, outgoing European Council President Herman Van Rompuy said the EU has adopted new sanctions against Russia, but will delay implementation due to 'pending developments.' It is believed Mr. Van Rompuy was referring to the current cease-fire agreement in Eastern Ukraine and that sanctions may target Russia's main energy companies.

Domestically, investors have been responding to a modest dose of corporate news. On the M&A front, Annie's (BNNY 45.99, +12.47) holds a pre-market gain of 37.2% after agreeing to be acquired by General Mills (GIS 53.18, -0.33). Also of note, Apple (AAPL 99.00, +0.64) is indicated to start higher by 0.7% with its product refresh event scheduled to begin at 13:00 ET.

Treasuries are near their lows with the 10-yr yield up three basis points at 2.50%.

The Job Openings and Labor Turnover Survey will be released at 10:00 ET.

9:01 am: [BRIEFING.COM] S&P futures vs fair value: -0.40. Nasdaq futures vs fair value: -0.50. The S&P 500 futures trade just below fair value.

Markets in Asia ended the session on a mixed note. The latest Bank of Japan minutes indicated the economic recovery remains moderate and inflation expectations are on the rise.

In economic data:

Japan's Tertiary Industry Activity Index was unchanged month-over-month (expected 0.3%; prior 0.0%), while Household Confidence slipped to 41.2 from 41.5 (consensus 42.3)

Australia's Home Loans rose 0.3% month-over-month (expected 1.0%; prior 0.1%), while NAB Business Confidence slipped to 8 from 10 and NAB Business Survey fell to 4 from 8

------

Japan's Nikkei added 0.3%, posting its best close since late January. The weaker yen supported exporters with Honda Motor up 1.2% and Advantest higher by 2.5%.

Hong Kong's Hang Seng was closed for the day after Mid-Autumn Festival.

China's Shanghai Composite ended flat, holding at its best levels since March 2013. Financials lagged as Bank of Beijing eased 2.5%.

Major European indices hover near their flat lines, while Spain's IBEX (-0.8%) underperforms. Of note, Bank of Italy is expected to broaden its definition of collateral in order to facilitate borrowing from the ECB under the TLTRO program. Elsewhere, outgoing European Council President Herman Van Rompuy said the EU has adopted new sanctions against Russia, but will delay implementation due to 'pending developments.' It is believed Mr. Van Rompuy was referring to the current cease-fire agreement in Eastern Ukraine and that sanctions may target Russia's main energy companies.

Economic data was limited:

Great Britain's trade deficit widened to GBP10.19 billion from GBP9.41 billion (expected deficit of GBP9.10 billion). Separately, Industrial Production rose 0.5% month-over-month (expected 0.2%; prior 0.3%), while Manufacturing Production increased 0.3%, as expected

French government budget deficit widened to EUR84.10 billion from EUR59.40 billion, while trade deficit narrowed to EUR5.50 billion from EUR5.60 billion (expected deficit of EUR5.00 billion)

------

Great Britain's FTSE is flat. Homebuilders outperform with Barratt Developments and Persimmon up 1.5% and 2.4%, respectively. Energy names are on the defensive with BP and Royal Dutch Shell both down in excess of 1.0%.

In France, the CAC is lower by 0.2%. Renault is the weakest performer, down 2.1% after announcing plans to develop an electric car with Bollore. Pernod Ricard leads with a gain of 1.7%.

Germany's DAX holds a loss of 0.3%. Exporters lag with BMW and Volkswagen down 0.6% and 0.9%, respectively. Producers of basic materials outperform with Lanxess higher by 1.8% and K+S up 0.9%.

Spain's IBEX trades down 0.8% amid broad weakness. Banco Popular has surrendered 1.1% and Bankia is down 0.7%.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: flat. Nasdaq futures vs fair value: +0.70. U.S. equity futures have slipped from their best levels of the morning, but they remain near fair value. Generally speaking, pre-market action has been subdued with futures respecting relatively narrow ranges.

The dollar rallied against other major currencies yesterday and saw overnight strength, which has since faded. The Dollar Index hovers near 84.30 after marking an overnight high north of 84.50. Also of note, the British pound ended yesterday at 1.6107 yesterday, rallied to 1.6158 overnight, but has since returned to where it finished yesterday. For its part, the dollar/yen pair is modestly higher at 106.15.

8:01 am: [BRIEFING.COM] S&P futures vs fair value: +1.50. Nasdaq futures vs fair value: +3.00. U.S. equity futures trade little changed amid cautious action overseas. The S&P 500 futures hover two points above fair value after climbing off their overnight low. Market participants received a handful of quarterly earnings since yesterday's close, but the bunch did not include any market-moving surprises. On a separate note, shares of Apple (AAPL 99.13, +0.77) will be in focus with the company scheduled to present a refreshed line of products at a press event scheduled to begin at 12:00 ET.

On the economic front, the Job Openings and Labor Turnover Survey will be released at 10:00 ET.

In U.S. corporate news of note:

Annie's (BNNY 46.00, +12.49): +37.3% after agreeing to be acquired by General Mills (GIS 53.73, +0.22) for $46 per share

Avon Products (AVP 13.00, -0.66): -4.8% after CFO Kimberly Ross left the company for Baker Hughes (BHI 67.25, 0.00)

Reviewing overnight developments:

Asian markets ended little changed. Japan's Nikkei +0.3%, while China's Shanghai Composite settled flat. Hong Kong's Hang Seng was closed in observance of the day following the Chinese Mid-Autumn Festival.

In economic data:

Japan's Tertiary Industry Activity Index was unchanged month-over-month (expected 0.3%; prior 0.0%), while Household Confidence slipped to 41.2 from 41.5 (consensus 42.3)

Australia's Home Loans rose 0.3% month-over-month (expected 1.0%; prior 0.1%), while NAB Business Confidence slipped to 8 from 10 and NAB Business Survey fell to 4 from 8

In news:

Japan's Finance Minister Taro Aso said the Q2 GDP revision did not change the view that the Japanese economy is recovering moderately. Mr. Aso added there are no plans to increase the budget this autumn.

Major European indices hover near their flat lines. Germany's DAX -0.1%, Great Britain's FTSE -0.1%, and France's CAC -0.1%. Elsewhere, Italy's MIB +0.2% and Spain's IBEX -0.6%

Economic data was limited:

Great Britain's trade deficit widened to GBP10.19 billion from GBP9.41 billion (expected deficit of GBP9.10 billion). Separately, Industrial Production rose 0.5% month-over-month (expected 0.2%; prior 0.3%), while Manufacturing Production increased 0.3%, as expected

French government budget deficit widened to EUR84.10 billion from EUR59.40 billion, while trade deficit narrowed to EUR5.50 billion from EUR5.60 billion (expected deficit of EUR5.00 billion)

Among news of note:

Bank of Italy is expected to broaden its definition of collateral in order to facilitate borrowing from the ECB under the TLTRO program

Outgoing European Council President Herman Van Rompuy said the EU has adopted new sanctions against Russia, but will delay implementation due to 'pending developments.' It is believed Mr. Van Rompuy was referring to the current cease-fire agreement in Eastern Ukraine and that sanctions may target Russia's main energy companies.

6:39 am: [BRIEFING.COM] S&P futures vs fair value: flat. Nasdaq futures vs fair value: -0.50.

6:39 am: [BRIEFING.COM] Nikkei...15,749.15...+44.00...+0.30%. Hang Seng...Holiday.........

6:39 am: [BRIEFING.COM] FTSE...6,824.87...-9.90...-0.10%. DAX...4,469.06...-5.90...-0.10%.

WTI Gains a Second Day Before U.S. Stockpile Data; Brent Climbs By Ben Sharples Sep 9, 2014 9:46 PM ET

West Texas Intermediate advanced for a second day before government stockpile data that will signal the strength of fuel demand in the U.S., the world’s biggest oil consumer. Brent rose in London.

Futures gained as much as 0.5 percent in New York. Crude inventories probably shrank by 1.5 million barrels last week to 358.1 million, according to a Bloomberg News survey before a report from the Energy Information Administration today. Brent closed below $100 a barrel yesterday for the first time since May 2013 amid easing geopolitical unrest.

“The market is still looking for further draws, even though we’ve seen a slight tick down of refinery utilization,” Michael McCarthy, a chief strategist at CMC Markets in Sydney, said by phone. “Threats in Ukraine and the Middle East appear to be abating, so we’re seeing a removal of risk premium.”

WTI for October delivery climbed as much as 47 cents to $93.22 a barrel in electronic trading on the New York Mercantile Exchange, and was at $92.95 at 11:31 a.m. Sydney time. The contract gained 9 cents to $92.75 yesterday. The volume of all futures traded was about 30 percent above the 100-day average. Prices have decreased 5.6 percent this year.

Brent for October settlement rose 23 cents, or 0.2 percent, to $99.39 on the London-based ICE Futures Europe exchange. The European benchmark crude was at a premium of $6.42 to WTI. It closed at $6.41 yesterday.

Fuel SuppliesU.S. gasoline stockpiles were probably unchanged at 209.9 million barrels during the week ended Aug. 5, according to the median estimate of nine analysts surveyed by Bloomberg before the EIA data. Supplies of distillates, which includes diesel and heating oil, increased by 1 million, the survey shows.

Crude supplies fell by 1.9 million barrels last week, the industry-funded American Petroleum Institute said yesterday, according to Bain Energy. The API collects information on a voluntary basis from operators of refineries, bulk terminals and pipelines, while the government requires that reports be filed with the EIA, the Energy Department’s statistical arm.

Oil prices are poised to drop next year as U.S. crude production reaches a 45-year high, the EIA said yesterday. WTI will average $94.67 a barrel in 2015 versus the August projection of $96.08, the government forecaster said in its monthly Short-Term Energy Outlook. It trimmed its Brent crude estimate for next year to $103 from $105.

Ukraine TruceUkraine and pro-Russian separatists agreed to a Sept. 5 truce, raising the prospect of ending a conflict that has soured Russia’s ties with former Cold War foes. European Union governments are meeting to consider tougher Russian sanctions after this week delaying a package of economic penalties.

The conflict in Iraq, the second-biggest producer in the Organization of Petroleum Exporting Countries, has spared oil facilities in the south, home to about three-quarters of its crude output. The nation pumped 3.09 million barrels a day last month, a Bloomberg survey of producers and analysts shows.

In Libya, output from the OPEC producer increased to 747,000 barrels a day, Mohamed Elharari, a spokesman for National Oil Corp., said yesterday.

To contact the reporter on this story: Ben Sharples in Melbourne at

bsharples@bloomberg.netTo contact the editors responsible for this story: Pratish Narayanan at

pnarayanan9@bloomberg.net Mike Anderson

U.S. Stocks Decline as Rate Concerns Grow, Apple Fades By Elena Popina and Lu Wang Sep 9, 2014 4:54 PM ET

U.S. stocks fell, with the Standard & Poor’s 500 Index declining the most in a month, as concerns grew that the Federal Reserve may raise interest rates sooner than anticipated and a rally in Apple Inc. (AAPL) disappeared.

Apple wiped out a rally of as much as 4.8 percent after unveiling new products including larger-screen iPhones. Garmin Ltd. (GRMN) and Amazon.com Inc. dropped at least 3.5 percent, pacing declines int the technology-heavy Nasdaq 100 Index. McDonald’s Corp. retreated 1.5 percent as its monthly sales missed estimates. Home Depot Inc. lost 2.1 percent after confirming that hackers attacked its computer systems.

The S&P 500 fell 0.7 percent to 1,988.44 at 4 p.m. in New York, for its largest retreat since Aug. 5. The Dow Jones Industrial Average lost 97.55 points, or 0.6 percent, to 17,013.87. The Nasdaq 100 slumped 0.8 percent, and the Russell 2000 Index of smaller companies tumbled 1.2 percent, its biggest drop since July 31. About 5.8 billion shares changed hands on U.S. exchanges, 3.5 percent above the three-month average.

“There are still a number of people who fear the Fed will raise rates too soon, but I don’t think there’s anything to be gained by being early in raising interest rates,” John Manley, who helps oversee about $233 billion as chief equity strategist for Wells Fargo Funds Management in New York, said in a phone interview. “If the Fed tightens too soon, it will drag the U.S. and the world into another recession.”

Fed StimulusThe Fed is gauging the strength of the economy as it winds down a bond-buying program and considers the timing of raising rates. Policy officials next meet Sept. 16-17.

Assessments of the strength of the economy are mixed, after gross domestic product expanded more than previously forecast in the second quarter, while a report on Sept. 5 showed the economy added fewer jobs than anticipated in August. Data this week will likely show a decline in weekly jobless claims and stronger retail sales, according to economists’ forecasts.

Rick Rieder, BlackRock Inc.’s chief investment officer of fundamental fixed income in New York, said in a report that an improving labor market and signs of inflation argue for the Fed to boost borrowing costs. Meanwhile, former Fed Chairman Alan Greenspan said the U.S. economic rebound has been hindered by a slump in the construction industry as wage growth remains slow and credit conditions tight.

Strategist TargetsWall Street strategists have been raising their targets for the S&P 500. Gina Martin Adams at Wells Fargo & Co. and Tony Dwyer, a strategist at Canaccord Genuity Securities LLC, were the latest today to lift their forecasts for the S&P. They follow increased projections from Morgan Stanley and Deutsche Bank AG and a bullish rating on global stocks from Goldman Sachs Group Inc.’s portfolio strategy team.

The S&P 500 retreated 0.3 percent yesterday after a five-week rally, its longest winning streak this year. The benchmark is trading at 16.6 times the projected earnings of its members, near the 16.8 multiple reached on Sept. 5 that was the highest valuation since the end of 2009, according to data compiled by Bloomberg.

The S&P 500 had not posted a move of more than 0.5 percent in either direction for 14 straight days until today, the longest streak since 1995, data compiled by Bloomberg show. The last time the index fell more than 10 percent was three years ago.

Volatility IndexThe Chicago Board Options Exchange Volatility Index, the gauge known as the VIX, climbed 6.6 percent to 13.50 today, the most in more than a month. The gauge lost 29 percent last month, the biggest drop in almost three years.

All 10 groups in the S&P 500 dropped today, with financial companies, utilities and phone shares losing more than 1 percent. Technology shares dropped 0.6 percent, reversing an earlier rally of 0.7 percent.

Apple fell 0.4 percent to $97.99, after climbing to within one point of its intraday record of $103.74 reached last week. The shares have typically fallen at other events where it debuted new products. Apple is up 22 percent so far this year, exceeding the 7.6 percent gain for the S&P 500.

The company announced a smartwatch, mobile-payments system, health applications and bigger-screen iPhones that all work together -- in the biggest new lineup so far under Chief Executive Officer Tim Cook.

Garmin Ltd. dropped 3.5 percent to $51.71. The maker of navigation services tumbled as much as 6.1 percent after Apple introduced the Apple Watch, which will include apps for maps.

Technology SharesAmazon.com Inc. retreated 3.7 percent, the most since July, to $329.75. The company yesterday cut the price of its Fire smartphone to 99 cents to boost adoption of the device.

Other technology companies also slumped. Yahoo Inc. dropped 2.5 percent, EBay Inc. lost 2.8 percent, and Intel Corp. slid 1.2 percent.

Morgan Stanley dropped 2.7 percent to $33.91 and Goldman Sachs Group Inc. lost 1.5 percent to $177.40. The Fed is planning risk-based capital standards for banks that are tougher than those developed by their international counterparts, Fed Governor Daniel Tarullo told lawmakers today.

McDonald’s retreated 1.5 percent to $91.09. The world’s largest restaurant chain said sales at stores open at least 13 months fell 3.7 percent in August as its U.S. slump continued for the fourth straight month.

Home Depot lost 2.1 percent to $88.93 after it confirmed that hackers attacked its computer systems at stores in the U.S. and Canada. The company, which didn’t disclose how many customers may have been affected, said the continuing investigation is focused on purchases made since April.

Avon RetreatsPinnacle Foods Inc. (PF) declined 4.7 percent to $31.99. Shareholders affiliated to Blackstone Group LP will sell 15 million shares in the company, according to a statement late yesterday. Blackstone held a 51 percent stake in Pinnacle as of June 30, according to data compiled by Bloomberg.

Avon Products Inc. retreated 3.6 percent to $13.17. The company said yesterday that Kimberly Ross resigned as chief financial officer, effective Oct. 2. The cosmetics company has dropped 24 percent this year.

Annie’s Inc. rallied 38 percent to $46.10. General Mills Inc., the maker of Cheerios, Bisquick and Yoplait, will buy the company for about $820 million, gaining a popular lineup of natural and organic foods. General Mills dropped 0.6 percent to $53.32.

To contact the reporters on this story: Elena Popina in New York at

epopina@bloomberg.net; Lu Wang in New York at

lwang8@bloomberg.netTo contact the editors responsible for this story: Lynn Thomasson at

lthomasson@bloomberg.net Jeff Sutherland

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage