Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

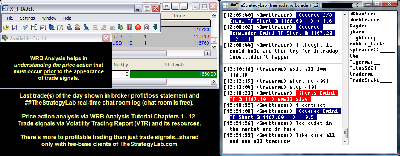

Attachment:

090814-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1660.00.png [ 175.03 KiB | Viewed 323 times ]

090814-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1660.00.png [ 175.03 KiB | Viewed 323 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,660.00 dollars or +16.60 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,660.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1882 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

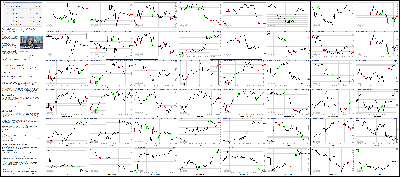

Attachment:

090814-Key-Price-Action-Markets.png [ 1.35 MiB | Viewed 336 times ]

090814-Key-Price-Action-Markets.png [ 1.35 MiB | Viewed 336 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:15 pm: [BRIEFING.COM] The stock market started the first full week of September on a cautious note. The S&P 500 lost 0.3%, but the relative strength of small cap stocks helped the Russell 2000 (+0.2%) and Nasdaq Composite (+0.2%) finish ahead of the benchmark index.

Equity indices struggled from the get-go with the overall risk sentiment dampened by continued dollar strength that sent the US Dollar Index (+0.54, 84.28) near its best level of the year. The greenback surged on the back of yen weakness following a downward revision to Japan's Q2 GDP (to -7.1% from -6.8%), while also drawing strength from weakness in the British pound. The pound fell to 1.6110 from 1.6330 against the greenback after a weekend YouGov poll revealed majority support for Scottish independence with the referendum coming up on September 18.

Conversely, the dollar strength weighed on commodities with gold futures falling 0.9% to $1255.80/ozt. Similarly, crude oil also retreated, testing its 2014 low, before narrowing its loss to 0.7% by the pit close. The energy component settled at $92.64/bbl, but continued its rebound in electronic trading.

The early weakness in crude contributed to a defensive start for the energy sector (-1.6%), which ended near its worst level of the session. Dow components Chevron (CVX 126.21, -1.19) and ExxonMobil (XOM 97.77, -1.49) posted respective losses of 0.9% and 1.5% as the stronger dollar and cheaper oil weighed on earnings prospects of the two multinational giants.

Energy notwithstanding, other sectors ended much closer to their flat lines. The consumer discretionary sector (-0.5%) weighed amid weakness in the shares of Ford (F 16.80, -0.34) and General Motors (GM 33.24, -1.04) after Morgan Stanley downgraded the U.S. auto sector.

Elsewhere, the consumer staples sector (-0.6%) was pressured by Campbell Soup (CPB 43.39, -1.15), which fell 2.6% in reaction to an in-line report and disappointing guidance. Manufacturers of cosmetics also lagged after the CEO of L'Oreal (LRLCY 32.60, -0.73) made cautious comments about the industry. Peers Avon Products (AVP 13.66, -0.18) and Estee Lauder (EL 75.59, -1.19) lost 1.3% and 1.6%, respectively.

On the upside, the technology sector (+0.2%) outperformed throughout the session, which underpinned the Nasdaq. Top-weighted components like Google (GOOGL 601.63, +3.85), Microsoft (MSFT 46.47, +0.56), and Intel (INTC 35.33, +0.33) posted gains between 0.6% and 1.2%, while the top index member by weight-Apple (AAPL 98.35, -0.62)-lost 0.6%.

High-beta Nasdaq components also provided a measure of support with the PHLX Semiconductor Index adding 0.2% and the iShares Nasdaq Biotechnology ETF (IBB 273.06, +2.46) climbing 0.9%. Meanwhile, the broader health care sector (+0.1%) ended just above its flat line.

Treasuries rallied overnight, but spend the day in a steady retreat. The 10-yr note shed four ticks to boost its yield to 2.47%.

Participation remained light with fewer than 590 million shares changing hands at the NYSE floor.

Economic data was limited to the Consumer Credit report for July, which pointed to a $26.00 billion increase from an upwardly revised $18.80 billion (from $17.30 billion) in June, while the Briefing.com consensus expected an increase of $17.40 billion.

Tomorrow's data will be limited to the Job Openings and Labor Turnover Survey, which will be released at 10:00 ET.

Nasdaq Composite +10.0% YTD

S&P 500 +8.3% YTD

Dow Jones Industrial Average +3.2% YTD

Russell 2000 +0.7% YTD

3:35 pm: [BRIEFING.COM]

The dollar index continued to weigh on precious metals today

Gold and silver sold off in early trade and basically remained there for the rest of the session

Dec gold finished $12.90 lower at $1254.30/oz, while Dec silver ended $0.20 lower at $18.97/oz.

Crude oil sold off from its overnight high of $93.56/barrel and fell as low as $91.80.

However, crude began to recover and closed $0.68 lower at $92.64/barrel. Oct crude is now at $92.94/barrel in electronic trading.

Natural gas futures rallied today and held it gains.

Oct nat gas rose as high as $3.89/MMBtu and finished out the day up $0.09 higher (or +2.4%) at $3.88/MMBtu.

Dec copper rallied this morning, but sold off later in the day to $3.17 from around $3.21/lb, erasing earlier gains. Dec copper ended the day unchanged at $3.17/lb.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.4% with one hour remaining in the session.

The Consumer Credit report for July was just released by the Federal Reserve and it showed that consumer credit increased by $26.00 billion. That was higher than the Briefing.com consensus estimate of $17.40 billion. The prior month's credit growth was revised to $18.80 billion.

2:30 pm: [BRIEFING.COM] Equity indices remain pressured with all ten sectors holding losses. Interestingly, small caps are holding up better than the S&P 500 (-0.5%) with the Russell 2000 lower by 0.2%.

Furthermore, today's retreat has pressured biotechnology and chipmakers from their highs, but the iShares Nasdaq Biotechnology ETF (IBB 271.50, +0.90) continues holding a slim gain. Meanwhile, the PHLX Semiconductor Index hovers right below its flat line.

On a separate note, the Consumer Credit report for July will cross the wires at 15:00 ET (Briefing.com consensus $17.40 billion).

2:00 pm: [BRIEFING.COM] The major averages have dropped to new lows with the S&P 500 widening its loss to 0.6%. All ten sectors now trade in the red with the weakest performer-energy-down 2.0%.

Elsewhere, the technology sector (-0.2%) has dipped into the red, also taking the Nasdaq Composite (-0.2%) with it. Notably, the top-weighted Nasdaq component-Apple (AAPL 98.19, -0.78)-has shown relative weakness throughout the session and now trades lower by 0.8%.

Also of note, Treasuries have continued their retreat with the 10-yr note now down four ticks with its yield up two basis points at 2.48%.

1:25 pm: [BRIEFING.COM] Currency issues are in the mix today as an overhang for the stock market. They emanate from the weakness in the British pound, which followed reports noting the possibility of Scotland voting for its independence from the UK in a September 18 referendum.

The pressure on the stock market isn't related so much to that possibility as it is to the recognition that the uncertainty is driving strength in the US Dollar Index (84.09, +0.36), which is also benefiting from the yen slipping to a six-year low against the greenback.

Throw in further losses in the euro and suddenly concerns about a stronger dollar weighing on the earnings prospects of US multinationals begin to round into focus along with assumptions that currency wars could soon be brewing.

The upshot of the stronger dollar is that it often drives dollar-denominated commodities lower. Sure enough, crude futures are down 1.2% to $92.17/bbl. That is helpful for consumers, but not so much for the major oil companies, which are pacing a 1.8% decline in the energy sector.

1:00 pm: [BRIEFING.COM] Equity indices are mixed at midday with the Nasdaq Composite (+0.1%) holding a slim gain, while the S&P 500 (-0.2%) hovers in the red.

The benchmark index has spent the entire first half of the session below its flat line with the early pressure coming from the energy sector (-1.6%). The growth-sensitive group slumped out of the gate amid weakness in the price of crude oil (-1.1% at $92.26/bbl), which hovers near its lowest level of the year. Meanwhile, top components Chevron (CVX 126.12, -1.28) and Exxon Mobil (XOM 98.00, -1.26) hold respective losses of 1.0% and 1.3%.

Elsewhere, the two consumer sectors are the only other laggards of note. The discretionary sector (-0.5%) has been pressured by the likes of Ford (F 16.76, -0.38) and General Motors (GM 33.39, -0.89) after Morgan Stanley downgraded the U.S. auto sector. For its part, the consumer staples space (-0.5%) has had to contend with a 2.2% decline in Campbell Soup (CPB 43.59, -0.95) after the company reported in-line results, but guided lower.

On the upside, the Nasdaq has been able to stay out of the red thanks to the outperformance of the technology sector (+0.2%). The top-weighted group sits in the lead with help from some blue chip components and high-beta chipmakers. Microsoft (MSFT 46.53, +0.62) and Intel (INTC 35.29, +0.29) hold respective gains of 1.4% and 0.9%, while the PHLX Semiconductor Index has added 0.3%.

Biotechnology has also given a booster shot to the Nasdaq with the iShares Nasdaq Biotechnology ETF (IBB 271.57, +0.97) trading higher by 0.4%. The broader health care sector (unch) outperforms, but has struggled to stay out of the red.

Interestingly, Treasuries have erased their overnight gains even though equities have been on shaky footing. The 10-yr note is unchanged with its yield at 2.46%.

Also of note, the U.S. Dollar Index (+0.4% at 84.09) has spiked at the expense of the British pound after a weekend YouGov poll indicated majority support for Scottish independence with the referendum coming up on September 18. The pound has climbed off its low, but still trades well below its rate on Friday. The pound/dollar pair is near 1.6140 after ending last week at 1.6330.

There was no economic data reported this morning, but the Consumer Credit report for July will cross the wires at 15:00 ET (Briefing.com consensus $17.40 billion).

12:25 pm: [BRIEFING.COM] The S&P 500 (-0.3%) has returned to its session low after a failed attempt at climbing past its opening level. The index has been trading inside a seven-point range, but that could change soon since the S&P 500 is currently probing the lower end of that range.

For its part, the tech heavy Nasdaq has spent the bulk of the day in the green, but broad weakness has caused the index to return to its flat line. Chipmakers and biotechnology continue showing relative strength with the PHLX Semiconductor Index higher by 0.3% and the iShares Nasdaq Biotechnology ETF (IBB 271.05, +0.45) holding a modest gain of 0.2%.

12:00 pm: [BRIEFING.COM] Equity indices remain little changed with the S&P 500 taking a couple steps back from its recent level. The benchmark index slumped out of the gate, but has been trying to work its way back to the flat line.

That battle has gotten a bit more difficult considering the technology sector has narrowed its gain to just 0.1%. Fittingly, the Nasdaq has returned to its flat line after showing a modest advance in the early going.

Interestingly, the weakness among equities has not led to gains in Treasuries. The 10-yr note has returned to its flat line, bringing the benchmark yield back to 2.46%.

11:30 am: [BRIEFING.COM] The S&P 500 (-0.1%) has climbed off its low and now trades near its opening level. Four sectors hold gains between 0.1% and 0.3%, while six groups remain in the red.

The energy sector (-1.3%) tumbled out of the gate and has not moved away from its low, while crude oil has inched up from its worst level of the session. The energy component remains down 1.1% at $92.23/bbl after marking a low under the $91.90 level.

On the upside, the technology sector (+0.3%) remains in the lead, while health care (+0.1%) has climbed out of the red.

10:55 am: [BRIEFING.COM] Recent action saw the S&P 500 (-0.3%) widen its loss, while the Nasdaq (+0.2%) has been able to stay out of the red.

The Nasdaq remains supported by influential components of the technology sector (+0.3%), while biotechnology has also played a part. The iShares Nasdaq Biotechnology ETF (IBB 271.93, +1.33) is higher by 0.5% after losing 2.2% last week. The industry group has helped the health care sector climb off its low, but the top-weighted countercyclical sector (-0.1%) remains in the red.

Meanwhile, the remaining three countercyclical sectors-consumer staples (-0.6%), telecom services (-0.8%), and utilities (-0.6%)-trail the broader market.

10:35 am: [BRIEFING.COM]

The dollar index, which touched 84.00 for the first time since July 2013, is weighing on commodities again today as well as the broader market

Gold, silver and crude oil sold off this morning. Gold and silver hit new lows on the day a few minutes ago. All three remains near the lows for the day.

The dollar index, copper and natural gas futures, on the other hand, are all sitting near current highs for the day.

Copper rallied overnight and are currently +0.9% at $3.20/lb

Natural gas put in small rally earlier this morning and are now

Dec gold is currently 0.7% at $1258.20/oz, while Dec silver is -0.5% at $19.07/oz

Oct crude oil is currently -1.4% at $91.97/barrel

10:00 am: [BRIEFING.COM] Equity indices remain mixed with the Dow (-0.1%) and S&P 500 (-0.1%) in the red, while the Nasdaq Composite (+0.3%) has climbed to a new high.

Fittingly, the technology sector (+0.4%) has also made some headway with help from influential components like Google (GOOGL 602.28, +4.50), Microsoft (MSFT 46.72, +0.81), and Intel (INTC 35.43, +0.43). The three names hold gains between 0.8% and 1.7%, while the top-weighted sector member-Apple (AAPL 98.86, -0.10) hovers in the red.

Chipmakers also outperform with the PHLX Semiconductor Index up 0.6%.

9:40 am: [BRIEFING.COM] Equity indices began the session with slim losses, but the Nasdaq (+0.1%) was quick to regain its flat line. Meanwhile, the S&P 500 (-0.1%) remains in the red with six sectors showing losses.

The energy sector (-1.2%) is an early laggard amid weakness in crude oil prices. The energy component trades lower by 1.5% at $91.90/bbl. Elsewhere, the remaining sectors hover closer to their flat lines.

On the upside, financials (+0.2%) have climbed into the lead with Bank of America (BAC 16.27, +0.25) contributing to the strength. The stock has added 1.7% in reaction to a Goldman Sachs upgrade.

Treasuries continue hovering near their highs with the 10-yr yield down two basis points at 2.42%.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: -3.30. Nasdaq futures vs fair value: -5.50. The stock market is on track for a modestly lower start as futures on the S&P 500 trade three points below fair value. Index futures spent the entire night in negative territory and notched their lows during the past 15 minutes.

Overnight, markets in Asia ended on a mixed note, while their European counterparts trade lower across the board. Most notably, Great Britain's FTSE is lower by 0.8% after a weekend YouGov poll indicated the majority now supports Scottish independence with the referendum coming up on September 18. The pound has also been on the defensive, falling to 1.6150 from 1.6330.

On the corporate front, Ford (F 16.75, -0.39) is indicated to open lower by 2.2% after Morgan Stanley downgraded the U.S. auto sector to 'Cautious,' while also downgrading the automaker. Separately, Campbell Soup (CPB 43.09, -1.45) holds a pre-market loss of 3.3% after reporting in-line earnings and guiding lower.

Treasuries hold gains with the 10-yr yield down three basis points at 2.43%.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: -3.70. Nasdaq futures vs fair value: -7.50. The S&P 500 futures trade four points below fair value.

Asian markets finished the session on a mixed note, while China's Shanghai Composite was closed for Mid-Autumn Festival.

In economic data:

China's trade surplus expanded to $49.83 billion from $47.30 billion (expected surplus of $40.00 billion) as imports fell 2.4% (expected 1.7%; prior -1.6%) and exports rose 9.4% (consensus 8.0%; last 14.5%)

Japan's GDP was revised down to an in-line -1.8% quarter-over-quarter, while the year-over-year reading fell 7.1% (consensus 7.0%; prior -6.8%). Separately, the Current Account surplus narrowed to JPY100 billion from JPY130 billion (expected surplus of JPY180 billion). Also of note, Economy Watchers Current Index fell to 47.4 from 51.3 (expected 52.4)

------

Japan's Nikkei added 0.2%, finishing at its best level in almost eight months. Heavyweight Softbank provided support, up 1.2%, after a regulatory filing by its holding, Alibaba, showed the company may raise more than $21 billion in its U.S. IPO.

Hong Kong's Hang Seng shed 0.2%, easing off its best levels in six years. Heavyweight Tencent Holdings sank 1.7% in response to the filing by its competitor, Alibaba.

China's Shanghai Composite was closed.

Major European indices trade lower across the board with Great Britain's FTSE (-0.9%) showing relative weakness after a weekend YouGov poll indicated the majority now supports Scottish independence with the referendum coming up on September 18. The pound has also been on the defensive, falling to 1.6130 from 1.6330.

Economic data was limited:

Eurozone Sentix Investor Confidence fell to -9.8 from 2.7 (expected 2.0)

Germany's trade surplus widened to EUR22.20 billion from EUR16.40 billion (expected surplus of EUR16.80 billion)

Great Britain's Halifax House Price Index ticked up 0.1% month-over-month (expected 0.2%; prior 1.2%), while the year-over-year reading rose 9.7% (consensus 9.9%; last 10.2%)

Swiss CPI was unchanged month-over-month (expected -0.1%; last -0.4%), while Retail Sales fell 0.6% year-over-year (expected 2.6%; prior 3.3%)

------

Germany's DAX is lower by 0.2% with Adidas leading the retreat. The stock holds a loss of 1.2%. Health care names outperform with Fresenius SE and Fresenius Medical Care up 0.9% and 0.5%, respectively.

In France, the CAC holds a loss of 0.4%. Oil services company Technip is the worst performer, down 2.4% amid continued weakness in crude oil. Steelmaker ArcelorMittal outperforms with a gain of 1.8%.

Great Britain's FTSE trades down 0.9% amid broad weakness. Lloyds Banking and Royal Bank of Scotland are both down near 3.0%. Randgold Resources has held up well and leads with an increase of 0.7%.

8:29 am: [BRIEFING.COM] S&P futures vs fair value: -3.30. Nasdaq futures vs fair value: -6.30. U.S. equity futures continue drifting near their pre-market lows. Index futures have maintained a narrow range throughout the night with futures on the benchmark index bounded by the 2,002 level and 2,004.50.

Range-bound was the theme for the better part of last week as three sessions ended within four points of their starting levels, while Friday's affair bucked the trend with the S&P 500 climbing almost ten points. All in all, the S&P 500 has been a bit tentative since registering its first close above the 2,000 level on August 26.

7:58 am: [BRIEFING.COM] S&P futures vs fair value: -2.80. Nasdaq futures vs fair value: -5.80. U.S. equity futures trade modestly lower amid cautious action overseas. The S&P 500 futures hover three points below fair value following last week's slim advance of 0.1%. With a light week of data ahead and no market-moving earnings on the schedule, participants are likely to keep an eye on geopolitical developments. On that note, Great Britain's FTSE (-1.0%) has slumped in reaction to growing support for Scottish independence ahead of the September 18 vote.

Economic data will be limited to the Consumer Credit report for July, which will cross the wires at 15:00 ET (Briefing.com consensus $17.40 billion).

Treasuries hold slim gains with the 10-yr yield down two basis points at 2.44%.

In U.S. corporate news of note:

Bank of America (BAC 16.18, +0.16): +1.0% after Goldman Sachs upgraded the stock to 'Buy' from 'Neutral.'

Campbell's Soup (CPB 43.71, -0.83): -1.9% after its earnings matched the Capital IQ consensus estimate on light revenue.

Ford (F 16.79, -0.35): -2.0% after Morgan Stanley downgraded the stock to 'Underweight' with a $16 target.

Reviewing overnight developments:

Asian markets ended mixed. Japan's Nikkei +0.2%, Hong Kong's Hang Seng -0.2%, and China's Shanghai Composite was closed for Mid-Autumn Festival

In economic data:

China's trade surplus expanded to $49.83 billion from $47.30 billion (expected surplus of $40.00 billion) as imports fell 2.4% (expected 1.7%; prior -1.6%) and exports rose 9.4% (consensus 8.0%; last 14.5%)

Japan's GDP was revised down to an in-line -1.8% quarter-over-quarter, while the year-over-year reading fell 7.1% (consensus 7.0%; prior -6.8%). Separately, the Current Account surplus narrowed to JPY100 billion from JPY130 billion (expected surplus of JPY180 billion). Also of note, Economy Watchers Current Index fell to 47.4 from 51.3 (expected 52.4)

In news:

Even though China's headline trade data surpassed expectations, participants showed some concern over a slowdown in shipments to the European Union and the United States.

Major European indices trade lower across the board. Germany's DAX -0.1%, France's CAC -0.3%, and Great Britain's FTSE -1.0%. Elsewhere, Italy's MIB -0.3% and Spain's IBEX -0.6%

Economic data was limited:

Eurozone Sentix Investor Confidence fell to -9.8 from 2.7 (expected 2.0)

Germany's trade surplus widened to EUR22.20 billion from EUR16.40 billion (expected surplus of EUR16.80 billion)

Great Britain's Halifax House Price Index ticked up 0.1% month-over-month (expected 0.2%; prior 1.2%), while the year-over-year reading rose 9.7% (consensus 9.9%; last 10.2%)

Swiss CPI was unchanged month-over-month (expected -0.1%; last -0.4%), while Retail Sales fell 0.6% year-over-year (expected 2.6%; prior 3.3%)

Among news of note:

The British pound weakened notably after a weekend YouGov poll indicated the majority now supports Scottish independence with the referendum coming up on September 18. The pound trades near 1.6140 versus the dollar after ending Friday at 1.6330.

6:38 am: [BRIEFING.COM] S&P futures vs fair value: -2.50. Nasdaq futures vs fair value: -7.50.

6:38 am: [BRIEFING.COM] Nikkei...15,705.11...+36.40...+0.20%. Hang Seng...25,190.45...-49.70...-0.20%.

6:38 am: [BRIEFING.COM] FTSE...6,796.68...-58.10...-0.80%. DAX...9,739.54...-7.60...-0.10%.

Dollar Rises to 6-Year High Versus Yen on Fed Policy Bets By Mariko Ishikawa Sep 8, 2014 11:14 PM ET

The dollar rose to the strongest in almost six years versus the yen after Treasury yields climbed on speculation economic reports this week will back the case for the Federal Reserve to raise interest rates next year.

A gauge of the greenback touched a 14-month high before the U.S. data forecast to show jobless claims decreased and retail sales improved. Fed policy makers will next meet Sept. 16-17. Low volatility across financial markets may signal traders are underestimating rate increases, according to San Francisco Fed researchers. The pound fell to the lowest since November, extending yesterday’s biggest decline in 14 months, before a vote on Scottish independence next week.

“The dollar is likely to test new highs against the yen ahead of the Fed meeting next week,” said Kengo Suzuki, the chief currency strategist at Mizuho Securities Co. in Tokyo. “The dollar broke out of the range as investors gained confidence in the U.S. economy and as the Fed deepens the debate about the policy after tapering ends.” The yen could test 110 per dollar this year, according to Suzuki.

The U.S. currency gained 0.2 percent to 106.21 yen at 11:57 a.m. in Tokyo, after reaching 106.28, the highest since October 2008. The greenback strengthened 0.1 percent to $1.2881 per euro, after earlier touching $1.2877, the strongest since July 2013. The shared currency added 0.1 percent to 136.82 yen.

The Bloomberg Dollar Spot Index, which tracks the greenback against a basket of 10 leading currencies, rose 0.2 percent to 1,047.11, after touching 1,047.18, the highest since July 2013.

The pound slid 0.1 percent to $1.6082 from the New York close, after earlier reaching $1.6077, the weakest since Nov. 21.

Positive DataFirst-time applications for U.S. unemployment benefits fell by 2,000 to 300,000 in the week ended Sept. 6, according to the median estimate of economists surveyed by Bloomberg News before the Labor Department report on Sept. 11.

Economists in a separate Bloomberg survey forecast a Commerce Department report due Sept. 12 will show U.S. retail sales increased 0.6 percent in August from the previous month.

“Surveys, market expectations, and model estimates show that the public seems to expect a more accommodative policy than Federal Open Market Committee participants,” San Francisco Fed Senior Economist Jens Christensen and Vice President of Financial Research Simon Kwan wrote in a report yesterday.

The 10-year U.S. Treasury yield touched 2.50 percent today, the highest since Aug. 5.

‘Further Upside’“Higher U.S. yields are fueling U.S. dollar buying,” said Naohiro Nomoto, an associate for foreign-exchange trading at Bank of Tokyo-Mitsubishi UFJ Ltd. in New York. “There looks to be further upside in U.S. yields, especially on the long end. There is speculation that the Fed will revise its forward guidance at next week’s meeting.”

Fed policy makers are on track to end a bond-buying stimulus program in October. Futures trading showed a 56 percent chance they will raise the benchmark interest-rate target to at least 0.5 percent by July 2015. The likelihood was 52 percent at the end of August. The Fed has held the rate in a range of zero to 0.25 percent since 2008 to support the economy.

The euro slid to a 14-month low after the European Central Bank on Sept. 4 unexpectedly cut all three of its main interest rates.

The ECB’s record stimulus will continue to spur investments in higher-yielding currencies funded in euros, according to FPG Securities Co. The greenback, the Australian and New Zealand dollars, as well as some emerging market would benefit, said Koji Fukaya, chief executive officer of FPG Securities, which provides over-the-counter currency derivative products for companies.

Scottish VoteA poll by YouGov Plc showed the Scottish independence campaign gained a lead for the first time this year before the referendum next week. A “yes” vote would raise the prospect of a more cautious approach from the Bank of England, which this month kept its key interest rate at a record low.

Sterling slumped 2.1 percent in the past month, the worst performer among a basket of 10 developed-nation currencies tracked by Bloomberg Correlation-Weighted Indexes. The euro sank 1.8 percent, and the yen fell 1.8 percent. The dollar rose 2.6 percent.

“The dollar was bought across the board as the euro declined on expectations of additional easing by the ECB and the pound weakened amid the risk of a breakup of the U.K.,” said Mizuho’s Suzuki.

To contact the reporter on this story: Mariko Ishikawa in Tokyo at

mishikawa9@bloomberg.netTo contact the editors responsible for this story: Garfield Reynolds at

greynolds1@bloomberg.net Jonathan Annells, Naoto Hosoda

U.S. Stocks Fall From Record as Energy Overshadows Yahoo By Elena Popina Sep 8, 2014 4:36 PM ET

The Standard & Poor’s 500 Index fell, after a five-week rally sent the gauge to a record, as declines in energy companies along with oil prices overshadowed a rally by Yahoo! Inc.

Exxon Mobil Corp. and Chevron Corp. dropped at least 0.9 percent to pace declines in the Dow Jones Industrial Average as oil prices tumbled. Ford Motor Co. slipped 2 percent after Morgan Stanley downgraded the shares of the automaker. Yahoo climbed 5.6 percent to the highest level since 2006 after Alibaba Group Holding Ltd. said it plans to raise as much as $21.1 billion in an initial public offering.

The S&P 500 (SPX) retreated 0.3 percent to 2,001.54 at 4 p.m. in New York. The Dow lost 25.94 points, or 0.2 percent, to 17,111.42. The Nasdaq 100 Index added 0.1 percent, led by Yahoo. About 5.2 billion shares changed hands today, 6 percent below the three-month average.

“You have five weeks of S&P growth, we may be in the overbought territory,” Bruce Bittles, chief investment strategist at Milwaukee-based RW Baird & Co., which oversees $110 billion, said in a phone interview. “You generally don’t continue to grow forever.”

The S&P 500 climbed 0.2 percent last week, completing its longest streak of weekly gains this year, as investors speculated weaker jobs growth will keep the Federal Reserve from raising interest rates. Bets on continued Fed support got a boost on Sept. 5 as data showed the economy added fewer jobs than estimated in August and the unemployment rate fell to 6.1 percent.

Fed StimulusThe Fed is gauging the strength of the labor market as it winds down a bond-buying program and considers the timing of raising interest rates. Policy officials next meet Sept. 16-17.

Low volatility across financial markets may signal investors are underestimating how quickly the Fed will raise interest rates, according to researchers at the San Francisco Fed.

“Surveys, market expectations, and model estimates show that the public seems to expect a more accommodative policy than Federal Open Market Committee participants,” Jens Christensen, a senior economist, and Simon Kwan, a vice president of financial research, said in a report today. Data also suggest that the public is “less uncertain about their projections.”

Morgan Stanley chief U.S. equity strategist Adam Parker announced today an increase in the firm’s 12-month S&P 500 forecast to 2,125, while Goldman Sachs Group Inc. raised its three-month rating on stocks to the equivalent of buy, after the European Central Bank reduced its main interest rates and implement an asset-buying plan. The move reversed a July 26 call, when the firm cut its three-month rating on stocks to neutral amid expectations government bond yields would increase.

Equity ValuationThe S&P 500 trades at 18 times the reported earnings of its members, near the highest level in four years. The gauge hasn’t posted a four-day streak of losses in all of 2014 and the last time it fell more than 10 percent was three years ago.

While markets are calm for now, the trajectory of the U.S. stock market is about to get bumpier, according to one measure in the options market.

Investors are bidding up contracts that protect against losses in the S&P 500 in the next three months, driving the price to near the highest level in 19 months compared with contracts expiring in a month. The difference in implied volatility shows traders are hedging for risks that may be months away while expressing less concern over the present.

Ukraine, EbolaU.S. equities climbed last week after Ukraine agreed on a cease-fire with pro-Russian separatists to stem months of bloodshed. The S&P 500 extended declines in afternoon trading today after an NBC affiliate in Florida reported a possible Ebola case at an area hospital, citing the U.S. Centers for Disease Control and Prevention. Shares recouped some of the losses after the patient tested negative, according to a report from the Washington Post.

The Chicago Board Options Exchange Volatility Index, a gauge of investor concern derived from options prices, climbed 4.7 percent to 12.66 today. The index plummeted 29 percent in August, the biggest monthly drop since October 2011.

Eight of 10 main industries in the S&P 500 fell today, with energy shares dropping 1.6 percent to lead declines. Brent crude briefly fell below $100 for the first time since June 2013 as Chinese imports slipped in August, bolstering concern there’s a global oil surplus.

Oil PricesEnergy companies also had the worst performance last week, with a loss of 1.5 percent. Brent has tumbled 13 percent since June 19 as economies from Europe to Asia show signs of slowing while oil output climbs. Oil markets in the U.S. and Europe face a glut amid constrained consumption and the recovery of supplies from Libya, the International Energy Agency, the Paris-based adviser to 29 nations, said last month.

Marathon Oil Corp. dropped 1.7 percent to $40.21 and Newfield Exploration Co. lost 4.7 percent, the most in the S&P 500, to $40. Exxon Mobil retreated 1.5 percent to $97.77, while Chevron dropped 0.9 percent to $126.21.

Ford declined 2 percent to $16.80 after Morgan Stanley downgraded the shares to underweight, similar to sell, from overweight, similar to buy. The brokerage cited a high exposure to the U.S. market, where it said sales in the last five years were driven by pent-up demand.

Campbell Soup Co. slid 2.6 percent to $43.39 as its 2015 profit forecast was less than analysts had estimated. The company has struggled to rekindle Americans’ appetite for soup, with sales of ready-to-serve varieties decreasing 8 percent in the quarter ended Aug. 3.

Apple PresentationApple Inc. slipped 0.6 percent to $98.36. The company will unveil the latest iPhones and a wearable gadget at an event tomorrow near its headquarters. The iPhones will include software that lets the handset act as a mobile wallet, while the watch-like wearable device is expected to include features for tracking health and fitness activity, people familiar with the plans have said.

Technology shares had the best performance among the S&P 500 groups, climbing 0.2 percent.

Yahoo, which owns more than 22 percent of e-commerce company Alibaba, rallied 5.6 percent to $41.81 for the biggest advance in the S&P. Alibaba plans to list on the New York Stock Exchange this month, according to a regulatory filing on Sept. 5. Yahoo will sell 121.7 million of its Alibaba shares, potentially reaping as much as $8.03 billion.

Facebook Inc. added 0.8 percent to $77.89 as its market value exceeded $200 billion, making it the 22nd-largest company in the world, as investors bet on the company to capitalize on the future of mobile advertising.

Rackspace RalliesRackspace Hosting Inc. rallied 6.9 percent to $39.79 after people familiar with the situation said CenturyLink Inc. has discussed the idea of acquisition with the San Antonio, Texas-based company. The cloud-computing provider said last month it is conducting an internal review of its strategic options. A spokeswoman for Rackspace and a representative for CenturyLink at Joele Frank Wilkinson Brimmer Katcher declined to comment.

Multimedia Games Holding Co. jumped 30 percent to $36.15 in its biggest advance since February 2012 as Global Cash Access Holdings Inc., a provider of cash solutions to the gaming industry, said it will buy the company for about $1.2 billion to expand its access to casino floors.

Boeing Co. (BA) rose 2.6 percent to $127.98 after Ryanair Holdings Plc agreed to buy as many as 200 high-density Boeing 737 jets in a deal worth a potential $22 billion at list prices.

To contact the reporter on this story: Elena Popina in New York at

epopina@bloomberg.netTo contact the editors responsible for this story: Lynn Thomasson at

lthomasson@bloomberg.net Jeff Sutherland

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage