Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

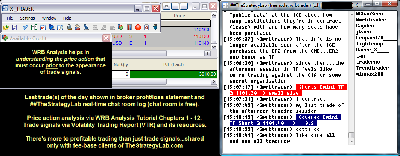

Attachment:

093014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3010.00.png [ 175.08 KiB | Viewed 511 times ]

093014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3010.00.png [ 175.08 KiB | Viewed 511 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,010.00 dollars or +30.10 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,010.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1900 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

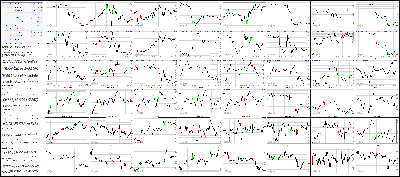

Attachment:

093014-Key-Price-Action-Markets.png [ 1.3 MiB | Viewed 504 times ]

093014-Key-Price-Action-Markets.png [ 1.3 MiB | Viewed 504 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market finished the third quarter on a cautious note with small caps leading the retreat. The S&P 500 shed 0.3% to narrow its Q3 gain to 0.6%, while the Russell 2000 (-1.5%) widened its quarterly loss to 7.9%.

Equity indices endured another volatile affair after the S&P 500 alternated between gains and losses during the past five trading days. Today's retreat represented the second consecutive decline for the benchmark index, which registered a September loss of 1.6%.

The benchmark index displayed modest strength in the early going with help from influential sectors like technology (+0.2%), financials (-0.2%), and industrials (-0.1%). The three cyclical groups helped the S&P 500 climb to a late morning high at 1985.18, but the index spent the next two hours in a steady retreat.

The slide from highs took place amid significant weakness in the two commodity-related sectors. Most notably, the energy space (-1.2%) widened its Q3 loss to 9.2% and was pressured by a 3.6% decline in crude oil. The energy component finished the pit session at $91.16/bbl, which represented a 13.6% loss for the quarter.

Similarly, the materials sector (-1.2%) stumbled in reaction to sliding prices of metals. Silver plunged 2.9% to $16.85/ozt, while gold (-0.6% to $1211.40/ozt) and copper (-1.6% to $3.01/lb) held up a bit better.

Also weighing on commodities was the continued strength of the Dollar Index, which added 0.4% to book a 3.9% gain for the month and an even more impressive 7.8% surge for the third quarter.

On the upside, the technology sector (+0.2%) finished ahead of the remaining cyclical groups and helped the S&P 500 trim its loss into the close. Large cap components displayed strength with Apple (AAPL 100.75, +0.64), Cisco Systems (CSCO 25.17, +0.24), and Visa (V 213.37, +2.44) climbing between 0.6% and 1.2%. Meanwhile, chipmakers traded alongside small-cap stocks as evidenced by a 0.9% decline in the PHLX Semiconductor Index.

Likewise, the high-beta biotechnology group underperformed, causing the health care sector (-0.6%) to finish behind the other three countercyclical sectors. The iShares Nasdaq Biotechnology ETF (IBB 273.63, -2.43) lost 0.9%.

Treasuries registered losses after spending the entire session in the red. The 10-yr note fell seven ticks to send its yield higher by three basis points to 2.50%.

Today's participation was ahead of average with more than 910 million shares changing hands at the NYSE floor.

Economic data included Chicago PMI, Consumer Confidence, and the Case-Shiller 20-City Index:

The Chicago PMI fell to 60.5 in September from 64.3 in August, while the Briefing.com consensus expected a decline to 61.5

Even though the PMI dropped more than expected, the current reading is far from a disappointment. Levels have remained above 60 for five of the past six months, and readings above 60 are generally considered too strong for long-term stability

The Conference Board's Consumer Confidence Index dropped to 86.0 in September from an upwardly revised 93.4 (from 92.4), while the Briefing.com consensus expected a fall to 92.0

This was the lowest reading in the Consumer Confidence Index since May

The Case-Shiller 20-city Home Price Index for July rose 8.1%, while a 7.4% increase had been expected by the Briefing.com consensus

The reading followed June's increase of 8.1%

Tomorrow, the weekly MBA Mortgage Index will be reported at 7:00 ET, while ADP Employment Change for September (Briefing.com consensus 202K) will be released at 8:15 ET. The day's data will be topped off with the 10:00 ET release of the ISM Index for September (consensus 58.5) and the Construction Spending report for August (consensus 0.4%).

Nasdaq Composite +7.6% YTD

S&P 500 +6.7% YTD

Dow Jones Industrial Average +2.8% YTD

Russell 2000 -5.3% YTD

3:30 pm: [BRIEFING.COM] The commodities space was mostly weaker today as the dollar index traded higher and the quarter came to an end.

Dec gold touched a session high of $1220.70 per ounce in morning action but quickly retreated back into negative territory. Earlier in overnight trade, the yellow metal fell as low as $1204.30 per ounce, its lowest level since early January. It managed to erase some of the losses as it headed into the close and settled 0.6% lower at $1211.40 per ounce, booking a loss of 8.4% for the quarter.

Dec silver slid to $16.85 per ounce in early afternoon pit trade, its lowest level since February 2010. It recovered back above $17 per ounce later in the session and settled with a 2.9% loss at $17.07 per ounce, declining 19.1% over the quarter.

Nov crude oil fell below the $91 per barrel level today after pulling back from a session high of $94.85 per barrel set moments after pit trade opened. The energy component traded as low as $90.86 per barrel while the dollar index held gains. Unable to find buying support, it settled 3.6% lower at $91.16 per barrel, booking a loss of 11.5% for the quarter.

Nov natural gas also retreated into negative territory after touching a session high of $4.17 per MMBtu in early morning action. It settled 0.5% lower at $4.12 per MMBtu, bringing losses for the quarter to 7.6%.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.2% with one hour remaining in the final session of the quarter. If the benchmark index holds its ground into the close, it will register a third-quarter gain of 0.7%, which compares favorably with the Russell 2000. The small-cap index enters the final hour with a quarter-to-date loss of 7.2%.

Today's weakest sector-energy (-1.1%)-will round out a disappointing quarter that saw the group surrender 9.0% since the end of the second quarter.

On the upside, the health care sector is on track to register a quarterly advance of 0.5%.

2:30 pm: [BRIEFING.COM] The S&P 500 (-0.4%) remains near its session low with dip buyers reluctant to step into the fold amid weakness in commodity-related sectors and high-growth areas like biotechnology (IBB -1.2%) and chipmakers (PHLX Semiconductor Index -0.9%).

The technology sector has recently surrendered its slim advance, leaving the telecom services sector (+0.2%) as the lone group trading in the green. As for the remaining countercyclical sectors, health care (-0.6%) lags, while consumer staples and utilities hover near their flat lines.

Elsewhere, Treasuries have not moved much since climbing off their lows in the morning. The 10-yr note remains lower by three ticks with its yield up one basis point at 2.49%.

2:00 pm: [BRIEFING.COM] During the past hour, the S&P 500 (-0.4%) tried to return above its flat line, but that attempt was rejected, resulting in fresh session lows for the benchmark index.

The two commodity-related sectors-energy and materials-remain at the bottom of the leaderboard with respective losses of 1.4% and 1.2%. On the upside, the technology sector (+0.1%) continues holding a slim gain, while the telecom services sector (+0.3%) remains in the lead.

The continued weakness in equities has caused participants to increase their demand for volatility protection. The CBOE Volatility Index (VIX 16.32, +0.34) hovers near the middle of yesterday's range, which represents the highest level since early August.

1:25 pm: [BRIEFING.COM] The stock market is mixed and little changed on this final day of the third quarter. Thus far, the trading action has been indecisive.

The real action is coming outside the stock market. Specifically, the commodity pits are a hotbed of activity, most of it on the sell side.

Oil (91.31, -3.26) in particular is getting clobbered along with silver ($16.97, -0.60) and gasoline ($2.43, -0.08) futures. The significant losses are without specific explanation. That is engendering some concern that the selling might be forced, but not to be overlooked is the continued strength in the US Dollar Index (85.96, +0.37). A stronger dollar weighs on dollar-denominated commodities.

Crude oil futures began trading down in a near straight line around 9:10 a.m. ET and are just now starting to stabilize. The weakness there is pressuring the energy stocks, which comprise the stock market's worst-performing sector (-1.2%) today.

1:00 pm: [BRIEFING.COM] The major averages are little changed at midday after enduring a volatile start to the trading day. The Dow, Nasdaq, and S&P 500 hover near their respective flat lines, while small caps underperform with the Russell 2000 down 0.8%.

Equity indices slipped out of the gate amid continued weakness in the energy sector (-1.1%), which has widened its September loss to 7.5%. Despite the early retreat, the indices were able to return into the green thanks to relative strength among influential sectors like technology (+0.4%), financials (unch), and industrials (+0.2%). However, the rebound did not involve small-cap stocks, and their continued weakness, combined with new lows in the energy sector, caused the broader market to return near its opening low. Furthermore, the Russell 2000 has widened its month-to-date loss to 5.5%.

Staying among high-beta names, chipmakers have been unable to stage a rally despite the relative strength of the tech sector. The PHLX Semiconductor Index is lower by 0.7%, which puts the industry group on track to register a September loss of 0.9%.

Similarly, the biotech space lags with the iShares Nasdaq Biotechnology ETF (IBB 273.93, -2.13) trading lower by 0.8%. Meanwhile, the health care sector (-0.3%) is the weakest countercyclical group at this juncture.

The remaining countercyclical sectors have fared better with telecom services (+0.5%) and utilities (+0.3%) holding modest gains, while the consumer staples sector trades flat.

Treasuries hold slim losses with the 10-yr yield up one basis point at 2.49%.

Economic data included Chicago PMI, Consumer Confidence, and the Case-Shiller 20-City Index:

The Chicago PMI fell to 60.5 in September from 64.3 in August, while the Briefing.com consensus expected a decline to 61.5

Even though the PMI dropped more than expected, the current reading is far from a disappointment. Levels have remained above 60 for five of the past six months, and readings above 60 are generally considered too strong for long-term stability

The Conference Board's Consumer Confidence Index dropped to 86.0 in September from an upwardly revised 93.4 (from 92.4), while the Briefing.com consensus expected a fall to 92.0

This was the lowest reading in the Consumer Confidence Index since May

The Case-Shiller 20-city Home Price Index for July rose 8.1%, while a 7.4% increase had been expected by the Briefing.com consensus

The reading followed June's increase of 8.1%

12:30 pm: [BRIEFING.COM] The S&P 500 has returned to its flat line while the Dow Jones Industrial Average (+0.1%) outperforms with 21 of its 30 trading in the green.

Despite the relative strength, only two index components hold gains in excess of 1.0%. Fittingly, both leaders-Cisco Systems (CSCO 25.24, +0.31) and Visa (V 213.823, +2.90)-fall under the umbrella of the technology sector (+0.4%), which trades ahead of the remaining cyclical groups.

On the countercyclical side, telecom services (+0.6%) and utilities (+0.8%) hover near their highs, while consumer staples and health care are flat.

12:00 pm: [BRIEFING.COM] Recent action saw the S&P 500 (+0.2%) take a step back from its session high. Meanwhile, small caps remain weak with the Russell 2000 down 0.5%.

Although the S&P 500 has respected a narrow range since turning positive, the commodity space has shown some significant volatility. Crude oil has been caught up in a sharp downtrend and now trades lower by 3.3% at $91.43/bbl. Metals have not fared much better with silver down 3.1% at $17.02/ozt and gold lower by 0.9% at $1208.30/ozt.

The weakness among commodities has sent energy (-0.7%) and materials (-0.5%) to lows.

11:30 am: [BRIEFING.COM] The S&P 500 (+0.3%) hovers at a fresh session high after having erased its entire decline from yesterday. Influential sectors continue driving the action with financials (+0.4%), industrials (+0.6%), and technology (+0.7%) trading ahead of the broader market.

The leading sector-technology-has drawn considerable strength from a handful of large cap names. Apple (AAPL 101.47, +1.36) and Cisco Systems (CSCO 25.17, +0.24) are both up near 1.0%, while eBay (EBAY 56.38, +3.72) has surged 7.1% after announcing plans to separate eBay and PayPal into independent companies.

The relative strength of the sector has had little effect on chipmakers as evidenced by a 0.3% decline in the PHLX Semiconductor Index. The high-beta group is on course to register a September loss of 0.4%.

10:55 am: [BRIEFING.COM] The Dow (+0.2%), Nasdaq (+0.2%), and S&P 500 (+0.2%) have clawed their way back into the green, while the Russell 2000 (-0.4%) remains pressured.

The underperformance of the small-cap index is fitting, considering the Russell 2000 has been the weakest index this month. Including the current loss, the index is on track to end the month lower by 5.0% versus a 1.1% decline for the S&P 500.

For the most part, the rebound has been fueled by influential sectors like financials (+0.3%), industrials (+0.3%), and technology (+0.5%), while energy (-0.2%) remains behind the other nine groups. Meanwhile, crude oil has continued its retreat and now trades lower by 1.3% at $93.33/bbl.

10:30 am: [BRIEFING.COM] Commodities are mostly lower this morning while the dollar index trades higher.

Dec gold touched a floor session high of $1220.70 in recent action after trading as low as $10204.30 in overnight trade but has since retreated back into negative territory. The precious metal is currently 0.2% lower at $1216.40.

Dec silver traded as low as $17.08 in overnight action, its lowest level since May 2010, but has since erased some of the loss. It is now at $17.27, or 1.7% lower.

Nov crude oil pulled back from its session high of $94.85 set moments after floor trade opened and slipped into negative territory. It has been trending lower and is currently down 1.2% at $93.47.

Nov crude oil is also chopping around in the red after pulling back from a session high of $4.18. It is now trading 0.5% lower at $4.13.

10:00 am: [BRIEFING.COM] The S&P 500 trades lower by 0.3% with nine sectors showing losses.

Just released, the consumer confidence reading for September came in at 86.0, while economists polled by Briefing.com expected the survey to come in at 92.0. This followed the prior month's revised reading of 93.4 (from 92.4).

9:45 am: [BRIEFING.COM] Equity indices began the session with slim gains before slipping to their lows. The S&P 500 trades lower by 0.2% with three sectors showing gains.

The technology space (+0.2%) has displayed opening strength, while other advancers include utilities (+0.3%) and telecom services (+0.1%). On the flip side, the weakest sector of the month-energy (-0.7%)-has extended its September loss to 7.1%.

Just released, the Chicago PMI for September fell to 60.5 from 64.3, while the Briefing.com consensus expected a decrease to 61.5.

Treasuries remain pressured with the 10-yr yield up two basis points at 2.50%.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: +2.00. Nasdaq futures vs fair value: +13.50. The stock market is on track for a slightly higher start to the final session of the third quarter. The S&P 500 futures trade two points above fair value, which should put the benchmark index on track to narrow its September loss of 1.3%. As for the quarter, the index has added 0.9% since the end of June. However, it is worth mentioning that index futures have slid from their highs over the past 30 minutes on no news.

Overnight, equities in Hong Kong remained pressured amid continued student protests, while markets in Europe (except for UK's FTSE) have been able to rebound from yesterday's weakness. Notably, Catalonia's President Artur Mas said he will suspend the campaign for Catalan independence after the Constitutional Court said it will block the vote.

Domestically, participants have been responding to stock-specific developments, including news that eBay (EBAY 56.80, +4.15) plans to spin-off PayPal during the second half of 2015. On the earnings front, Walgreen (WAG 59.70, +0.10) trades up 0.2% after reporting in-line results.

Treasuries hover in the red with the 10-yr yield up almost three basis points at 2.51%.

The Chicago PMI report for September (Briefing.com consensus 61.5) will be released at 8:45 ET and the Consumer Confidence report for September (expected 92.0) will cross the wires at 10:00 ET.

9:02 am: [BRIEFING.COM] S&P futures vs fair value: +4.10. Nasdaq futures vs fair value: +16.50. The S&P 500 futures trade four points above fair value.

The Case-Shiller 20-city Home Price Index for July rose 6.7%, while a 7.4% increase had been expected by the Briefing.com consensus. This follows the previous month's increase of 8.1%.

8:33 am: [BRIEFING.COM] S&P futures vs fair value: +5.80. Nasdaq futures vs fair value: +18.50. The S&P 500 futures trade six points above fair value.

Markets across Asia settled on a mixed note. The 'Occupy Central' protests for democracy continue in Hong Kong. Elsewhere, the Reserve Bank of India kept its benchmark interest rate unchanged at 8.00%, as expected.

In economic data:

China's HSBC Manufacturing PMI ticked down to 50.2 from 50.5 (expected 50.5)

Japan's Household Spending fell 4.7% year-over-year (expected -3.8%; previous -5.9%), but Retail Sales rose 1.2% year-over-year (expected 0.3%; prior 0.5%). The Unemployment Rate ticked down to 3.5% from 3.8% (consensus 3.8%) and Industrial Production fell 1.5% month-over-month (expected 0.2%; last 0.4%). Separately, Average Cash Earnings rose 1.4% year-over-year (expected 1.1%; prior 2.6%) and Housing Starts fell 12.5% year-over-year (expected -14.2%; previous -14.1%)

South Korea's Retail Sales rose 2.7% month-over-month (consensus 0.5%; prior 0.3%)

Australia's Private Sector Credit expanded 0.4% month-over-month, as expected

New Zealand's ANZ Business Confidence eased to 13.4% from 24.4%

------

Japan's Nikkei lost 0.8%, falling from seven-year highs. Trading giant Sumitomo tumbled 12.0% after cutting its annual profit forecast 96% due to lower prices in the commodity space.

Hong Kong's Hang Seng fell 1.3% to a three-month low as sellers remained in control for the sixth time in seven sessions. Casino stocks remained weak as Galaxy Entertainment and Sands China shed 2.7% and 2.4%, respectively.

China's Shanghai Composite added 0.3% to finish at a 19-month high ahead of Golden Week. Coal names posted solid gains as Datong Coal Industry jumped 3.5% to lead the sector higher.

India's Sensex ticked up 0.1% to hold its 50-day average. Financials ended mixed as HDFC Bank gained 0.9% and ICICI Bank lost 1.7%.

Major European indices trade mostly higher with Italy's MIB (+1.2%) in the lead. Also of note, Spain's El Pais has reported Artur Mas will stop campaigning for Catalan independence after the Constitutional Court announced it will block the vote.

Economic data was plentiful:

Eurozone CPI ticked up 0.3% year-over-year, as expected, while core CPI rose 0.7% (consensus 0.9%; prior 0.9%. Separately, the Unemployment Rate held steady at 11.5%, as expected

Germany's Claimant Count rose by 13,000 (expected -2,000; previous 3,000), but the Unemployment Rate remained unchanged at 6.7%, as expected

Great Britain's GDP rose 0.9% quarter-over-quarter (expected 0.8%; previous 0.7%), while the current account deficit widened to GBP23.10 billion from GBP20.50 billion (expected deficit of GBP17.00 billion). Separately, Nationwide HPI rose 9.4% year-over-year (expected 10.4%; previous 11.0%)

French Consumer Spending rose 0.7% month-over-month (expected -0.2%; previous 0.8%), while PPI ticked down 0.3% month-over-month (consensus 0.0%; last -0.3%)

Spain's Business Confidence ticked down to -6.9 from -6.7 (expected -6.8)

Italy's CPI ticked down 0.3% month-over-month, as expected. Also of note, PPI fell 1.7% year-over-year (expected -1.6%; previous -1.6%)

------

Great Britain's FTSE is lower by 0.2% with consumer names on the defensive after Next issued a cautious forecast. The stock has tumbled 5.0%, while Marks & Spencer Group and Sports Direct International hold respective losses of 2.5% and 1.7%.

Germany's DAX has added 0.4% with help from utilities. E.On and RWE are both up near 1.5%. On the downside, Infineon Technologies is lower by 3.0%.

In France, the CAC trades up 1.2% with energy names providing support. Technip and Total hold respective gains of 3.2% and 1.9%. Renault has given up 2.6% after Ford issued a cautious sales forecast for Europe.

Italy's MIB is higher by 1.2% amid broad strength. Banco Popolare, BMPS, UBI Banca, and Unicredit are up between 1.8% and 2.8%.

8:01 am: [BRIEFING.COM] S&P futures vs fair value: +6.50. Nasdaq futures vs fair value: +21.20. U.S. equity futures trade near their pre-market highs amid upbeat action overseas. The S&P 500 futures hover seven points above fair value after inching up over the course of the night. Given the current indication, the benchmark index will get an early boost in an attempt to narrow its September loss of 1.3%. Furthermore, the S&P 500 will enter the day with a quarter-to-date gain of 0.9%.

Market participants will receive three economic reports to round out the month with the Case-Shiller 20-city Index for July (Briefing.com consensus 7.4%) set to be released at 9:00 ET, while the Chicago PMI for September (consensus 61.5) will cross the wires at 9:45 ET. The day's data will be topped off with the 10:00 ET release of the Consumer Confidence report for September (expected 92.0).

Treasuries sit near their lows with the 10-yr yield up three basis points at 2.51%.

In U.S. corporate news of note:

Alcoa (AA 16.15, +0.22): +1.4% after Bank of America/Merrill Lynch upgraded the stock to 'Buy' from 'Neutral.'

eBay (EBAY 58.58, +5.94): +11.3% after announcing plans to spinoff PayPal during the second half of next year.

Walgreen (WAG 61.00, +1.40): +2.4% in reaction to in-line earnings and revenue.

Reviewing overnight developments:

Asian markets ended mixed. Japan's Nikkei -0.8%, Hong Kong's Hang Seng -1.3%, and China's Shanghai Composite +0.3%

In economic data:

China's HSBC Manufacturing PMI ticked down to 50.2 from 50.5 (expected 50.5)

Japan's Household Spending fell 4.7% year-over-year (expected -3.8%; previous -5.9%), but Retail Sales rose 1.2% year-over-year (expected 0.3%; prior 0.5%). The Unemployment Rate ticked down to 3.5% from 3.8% (consensus 3.8%) and Industrial Production fell 1.5% month-over-month (expected 0.2%; last 0.4%). Separately, Average Cash Earnings rose 1.4% year-over-year (expected 1.1%; prior 2.6%) and Housing Starts fell 12.5% year-over-year (expected -14.2%; previous -14.1%)

South Korea's Retail Sales rose 2.7% month-over-month (consensus 0.5%; prior 0.3%)

Australia's Private Sector Credit expanded 0.4% month-over-month, as expected

New Zealand's ANZ Business Confidence eased to 13.4% from 24.4%

In news:

Japan's Finance Minister Taro Aso welcomed the improvement in the Unemployment Rate, but cautioned that poor weather is likely to impact economic data from the third quarter

Major European indices trade mostly higher. Great Britain's FTSE -0.1%, Germany's DAX +0.5%, and France's CAC +1.2%. Elsewhere, Spain's IBEX +1.1% and Italy's MIB +1.3%

Economic data was plentiful:

Eurozone CPI ticked up 0.3% year-over-year, as expected, while core CPI rose 0.7% (consensus 0.9%; prior 0.9%. Separately, the Unemployment Rate held steady at 11.5%, as expected

Germany's Claimant Count rose by 13,000 (expected -2,000; previous 3,000), but the Unemployment Rate remained unchanged at 6.7%, as expected

Great Britain's GDP rose 0.9% quarter-over-quarter (expected 0.8%; previous 0.7%), while the current account deficit widened to GBP23.10 billion from GBP20.50 billion (expected deficit of GBP17.00 billion). Separately, Nationwide HPI rose 9.4% year-over-year (expected 10.4%; previous 11.0%)

French Consumer Spending rose 0.7% month-over-month (expected -0.2%; previous 0.8%), while PPI ticked down 0.3% month-over-month (consensus 0.0%; last -0.3%)

Spain's Business Confidence ticked down to -6.9 from -6.7 (expected -6.8)

Italy's CPI ticked down 0.3% month-over-month, as expected. Also of note, PPI fell 1.7% year-over-year (expected -1.6%; previous -1.6%)

Among news of note:

Spain's El Pais has reported Artur Mas will stop campaigning for Catalan independence after the Constitutional Court announced it will block the vote

6:27 am: [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +14.50.

6:26 am: [BRIEFING.COM] Nikkei...16,173.52...-137.10...-0.80%. Hang Seng...22,932.98...-296.20...-1.30%.

6:26 am: [BRIEFING.COM] FTSE...6645.09...-1.60...0.00. DAX...9476.38...+53.70...+0.60%.

U.S. Crude Futures Slide Most in 22 Months; Brent Falls By Moming Zhou and Mark Shenk Sep 30, 2014 5:08 PM ET

West Texas Intermediate crude slid the most in 22 months and Brent reached a two-year low as ample supply shielded the market from the risk of disruption due to the conflict in the Middle East.

Futures slumped 3.6 percent in New York and 2.6 percent in London. OPEC oil production increased in September, led by a rebound in Libyan output to the highest level in more than a year, a Bloomberg survey showed today. Both benchmarks capped their biggest quarterly declines in more than two years. WTI may approach $90.63 after breaking below $91.50, according to Bloomberg First Word oil strategist Eric D. Pradas.

“We are going to continue to see lower prices as we go forward,” said Tariq Zahir, a New York-based commodity fund manager at Tyche Capital Advisors. “Fundamentally we are just very well supplied. The dollar continues to get stronger and it’s adding pressure to oil.”

WTI for November delivery fell $3.41 to end at $91.16 a barrel on the New York Mercantile Exchange, the lowest settlement since May 1, 2013. It was the biggest one-day loss since November 2012. Prices have lost 13 percent this quarter, the most since June 2012. The volume of all futures was 70 percent above the 100-day average.

Brent for November settlement slid $2.53 to $94.67 a barrel on the London-based ICE Futures Europe exchange, the lowest close since June 28, 2012. Volume was 22 percent above the 100-day average. Prices have decreased 16 percent this quarter. WTI was at a discount of $3.51 to Brent on ICE, compared with $2.63 yesterday, which was the narrowest since August 2013.

Third MonthWTI was little changed after the American Petroleum Institute said inventories slid 460,000 barrels last week, according to Bain Energy. Stockpiles at Cushing, Oklahoma, the delivery point for WTI crude, rose 355,000 barrels.

Oil dropped for a third straight month as supply gains offset the U.S.-led military campaign against Islamic State. Brent is down 8.3 percent in September, compared with a 5 percent retreat for WTI.

“It’s the quarter end and a lot of hedge funds are pulling money out of the market,” said Carl Larry, president of Oil Outlooks & Opinions LLC in Houston.

Reformulated RBOB gasoline futures slid 4.1 percent to $2.5869 a gallon on the Nymex, for a quarterly drop of 16 percent. The October contract expired today.

“The weakness in the expiring RBOB contract is the primary driver today,” Stephen Schork, president of Schork Group Inc. in Villanova, Pennsylvania, said by phone. “The secondary driver is the end of the quarter, which leads to book squaring. A tertiary reason is the strength of the dollar, which always weighs on commodity markets.”

Reduced PositionsSpeculators reduced their net long positions on WTI by 4.8 percent in the week ended Sept. 26 to 193,965 futures and options combined, according to the Commodity Futures Trading Commission.

Oil also followed declines in other commodities as the Bloomberg Dollar Index climbed to 1,073.81, the highest since 2010. The Bloomberg Commodity Index fell 1.4 percent. A stronger dollar reduces commodities’ investment appeal.

U.S. crude stockpiles probably expanded by 1.5 million barrels last week, a Bloomberg News survey showed before an Energy Information Administration report tomorrow.

U.S. crude stockpiles may have climbed last week as refineries started conducting seasonal maintenance. Plants typically schedule planned work for September and October, when they move from maximizing gasoline output to producing winter fuels.

‘Continuous Decline’“What we are seeing is a continuous decline since the highs in June,” said Harry Tchilinguirian, BNP Paribas SA’s London-based head of commodity markets strategy. “We have not only financial deleveraging, but also physical surplus in the market. The dollar is going to be dominating.”

U.S. domestic production rose to 8.87 million barrels a day in the week ended Sept. 19, the most since March 1986, according to EIA estimates. A combination of horizontal drilling and hydraulic fracturing, or fracking, has unlocked supplies from shale formations in the central U.S.

U.S. output gains are pushing out imports. Crude oil shipments to the U.S. fell 1.24 million barrels a day to 6.87 million in the week ended Sept. 19, the lowest level since May.

“Our reduction of imports is the same as an increase of supply to the world,” said James Williams, an economist at WTRG Economics, an energy-research firm in London, Arkansas. “The supply-demand fundamentals favor lower oil prices. A lot of speculators are getting out of long positions.”

Libyan OutputThe International Energy Agency said earlier this month that higher exports from Libya and booming U.S. production “deepened the overhang in crude markets and overshadowed any lingering worries of potential output disruptions in Iraq.”

Libya’s oil production was at 900,000 barrels a day, unchanged from yesterday, according to National Oil Corp. The country is working to restore crude output after a year of unrest reduced it to the smallest producer in the Organization of Petroleum Exporting Countries at one stage.

The U.S. and its European and Arab allies have conducted thousands of air missions against Islamic State militants in Syria and Iraq.

In northern Syria, Islamic State’s offensive against the town of Kobani sparked an exodus of tens of thousands of Syrian Kurds, raising concern that the conflict would widen. Tensions increased yesterday after errant shells fired by Islamic State militants landed inside Turkey, injuring five people, Turkish Kurdish officials said.

To contact the reporter on this story: Moming Zhou in New York at

mzhou29@bloomberg.netTo contact the editors responsible for this story: David Marino at

dmarino4@bloomberg.net Richard Stubbe, Stephen Cunningham

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage