Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

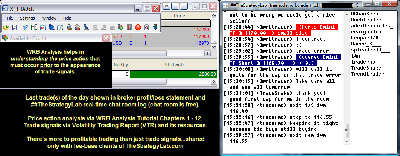

Attachment:

070914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2880.00.png [ 175.95 KiB | Viewed 328 times ]

070914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2880.00.png [ 175.95 KiB | Viewed 328 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$2,880.00 dollars or +28.80 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $2,880.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=132&t=1835 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=242&t=2402 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

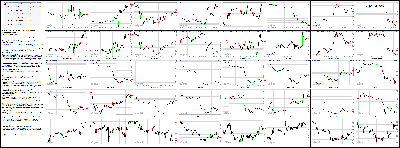

Smile, Stocks Have A Better Day Attachment:

070914-Key-Price-Action-Markets.png [ 950.76 KiB | Viewed 304 times ]

070914-Key-Price-Action-Markets.png [ 950.76 KiB | Viewed 304 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

There are probably some high fives on the trading floor. Stocks snapped a two-day losing streak Wednesday as worries about the Fed's interest rate policy abated.

The Dow Jones industrial average, the S&P 500 and the Nasdaq all gained ground, bouncing back from losses over the past two days. The Dow and S&P 500 ended up about 0.5%. The Nasdaq gained 0.6%.

Here's what you need to know:

1. Fed minutes: Stocks got a boost after the Federal Reserve released minutes from its latest policy meeting, which seemed to assuage fears about any precipitous interest rate increases.

"Overall, no major surprises," said Jim O'Sullivan, chief U.S. economist at High Frequency Economics.

The Fed could end its bond buying program as soon as October, assuming the economy continues to perform as officials expect, according to minutes from the central bank's June policy meeting.

Related: Fed signals the economy is getting betterThe central bank has been shrinking its monthly bond purchases since January and is widely expected to complete the program this year. But it had not mentioned a specific month until now.

Most Fed officials predict interest rates to remain low for the next few years. According to the minutes, 12 meeting participants said hiking interest rates would not be warranted until "sometime in 2015," while three said "policy firming" wouldn't be appropriate until 2016. Only one participant argued for a rate hike in 2014.

Stocks tumbled Tuesday on concerns that interest rates could be going up sooner rather than later.

2. Stock market movers -- Alcoa up, The Container Store down: Shares in Alcoa (AA) rose after kicking off earnings season by beating analyst estimates.

Overall, earnings for the companies in the S&P 500 are expected to be up 4.9% in the second quarter, compared with the same period last year, according to FactSet.

Shares in Gigamon (GIMO) were down again Wednesday after plunging a whopping 33% on Tuesday. The technology company had lowered its revenue guidance for the second quarter.

The Container Store (TCS) was also suffering -- down over 8% -- after reporting sluggish same-store sales.

3. Next big banking fine: Citigroup (C) is reported to be close to agreeing to pay $7 billion to settle a U.S. government investigation into the sale of mortgage backed securities. The deal would include billions in help for borrowers, according to the reports. The stock moved little.

JP Morgan (JPM) paid $13 billion last year to settle similar charges.

European banks have been in regulators' cross hairs more recently.

Earlier this month, French bank BNP pleaded guilty to criminal charges for breaching U.S. sanctions and will pay a record penalty of almost $9 billion. The bank violated U.S. money laundering laws by helping clients dodge sanctions on Iran, Sudan and other countries.

U.S. officials are also said to be investigating Germany's Commerzbank for sanctions violations.

4. International markets overview: The stock market in Brazil was closed for a holiday Wednesday, one day after the Brazilian national soccer team suffered a humiliating defeat to the Germans in the World Cup. But investors seemed to view the loss as a boon for Brazilian stocks. The iShares MSCI Brazil Capped ETF (EWZ), which tracks shares of several leading Brazilian companies, gained more than 1%.

And if stocks are anything to go by, Argentina's market is up 2% so far this week while the Netherlands' is down 2%. The two countries face off in World Cup action today.

European markets ended mixed. Asian markets lost ground as subdued China inflation data provided more evidence that the economy is struggling to pick up pace after a below-target performance in the first quarter.

4:20 pm: [BRIEFING.COM] The major averages snapped their two-day losing streak with the Nasdaq Composite leading today's charge. The tech-heavy index rose 0.6%, while the S&P 500 advanced 0.5% with nine sectors posting gains.

Equity indices displayed opening strength, but the early advance was a bit shaky as the Russell 2000 (+0.1%) had a tough time keeping pace with the broader market. The small-cap index underperformed throughout the session, while the other key indices powered to new highs after the Federal Reserve released the minutes from the June FOMC meeting.

Most notably, the minutes revealed the belief among officials that investors have displayed too much complacency with regard to risk. Furthermore, the minutes indicated that the committee has discussed its exit strategy tools with the general expectation of a final $15 billion taper taking place in October if the current outlook holds up.

The subsequent rally in equities could likely be attributed to participants being encouraged by the relatively consistent language in the minutes. However, it was a bit striking to see a concurrent spike in Treasuries and gold futures.

The 10-yr note hovered on its session low ahead of the release, but reclaimed its entire loss in short order. As a result, the benchmark yield ended at 2.55% after being near 2.60% when the minutes crossed the wires. One could argue that this spike was also related to the consistent language in the minutes with participants viewing the status quo at the Fed as a sign that the central bank could fall behind on its growth forecast.

Elsewhere, gold futures spiked to $1329.00/ozt to register a solid 1.0% gain, suggesting some participants believe the Fed could be underestimating inflationary pressures given the apparent lack of urgency to move off the zero bound.

The consumer discretionary sector (+1.2%) spent the entire session in the lead thanks to support from restaurants and retail names. Interestingly, the retail sector appeared unaffected by cautious comments made by the CEO of The Container Store (TCS 24.80, -2.27). The specialty retailer tumbled 8.9% following its earnings miss while the CEO said the retail industry as a whole was in a 'funk.'

Unlike the discretionary sector, other top-weighted groups settled on a mixed note with respect to the broader market. Health care (+0.4%) and technology (+0.5%) ended essentially in line with the S&P 500, while financials (+0.3%) and industrials (+0.2%) were limited to slim gains.

The modest uptick among industrials masked the relative strength of transport stocks. The Dow Jones Transportation Average rose 0.5% with 16 components settling higher. Matson (MATX 28.99, +1.64) was a standout, surging 6.0% after BB&T upgraded the stock to 'Buy' from 'Hold.' Airlines also displayed broad strength following positive monthly data from American Airlines (AAL 41.98, +1.73).

On the downside, the utilities sector (-0.2%) was the lone decliner following two days of relative strength.

Participation was below average with 557 million shares changing hands at the NYSE floor.

Economic data was limited to the weekly MBA Mortgage Index, which rose 1.9% to follow last week's downtick of 0.2%.

Tomorrow, weekly initial claims will be reported at 8:30 ET (Briefing.com consensus 311K), while the Wholesale Inventories report for May will cross the wires at 10:00 ET (consensus 0.5%).

Related Stories

InPlay from Briefing.com Briefing.com

S&P 500 on track for 6th straight quarterly gain MarketWatch

Stocks Fade From Higher Open; Lam Hits New High Investor's Business Daily

Stocks end higher after 2-day drop; end of QE in view CNBC

Once Again the Stock Market Climbs Higher on Air TheStreet.com

S&P 500 +6.7% YTD

Nasdaq Composite +5.8% YTD

Dow Jones Industrial Average +2.5% YTD

Russell 2000 +0.8% YTD

3:35 pm: [BRIEFING.COM]

Precious metals traded higher ahead of today's release of the latest FOMC minutes from the June meeting at 14:00 ET.

Aug gold traded as high as $1327.90 per ounce and settled with a 0.6% gain at $1324.40 per ounce.

Sep silver pulled back from a session high of $21.22 per ounce set in early morning action. It brushed a session low of $21.04 per ounce and settled with a 0.2% gain at $21.07 per ounce.

Both gold and silver popped to their respective HoD of $1333.40 per ounce and $21.28 per ounce in recent electronic trade and are currently trading slightly below those levels.

Aug crude oil trended lower in negative territory today as inventory data and reports that the El Sharara oil field in Libya was restarted put pressure on prices.

Although crude oil inventories for the week ending July 4 fell by 2.37 mln barrels when consensus called for a draw of 1.7-2.2 mln barrels, gasoline inventories grew 0.579 mln barrels (a draw of 0.2-0.4 mln barrels was anticipated). The energy component pulled back from its session high of $102.91 per barrel set at pit trade open and traded as low as $102.00 per barrel. Unable to find buying support, it settled with a 1.1% loss at $102.24 per barrel.

Aug natural gas rose to a session high of $4.23 per MMBtu but slipped back into negative territory in afternoon action. It settled 0.7% lower at $4.17 per MMBtu, just above its session low of $4.16 per MMBtu.

2:55 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.5% with one hour remaining in the session. Stocks enter the final hour of action on their highs despite testing their lows shortly after the release of the FOMC minutes from the June meeting.

Interestingly, the strength in equities has not lured participants away from the bond market. The 10-yr note enters the last hour of the trading day little changed with its yield at 2.55% after notching a high at 2.60%.

Similar to Treasuries, gold futures are also on their highs (+1.0% at $1329.10/ozt), while crude oil (-1.2% at $102.17/bbl) and the Dollar Index (-0.2% at 80.01) sit on their lows.

2:30 pm: [BRIEFING.COM] Recent action saw the S&P 500 (+0.5%) climb to a fresh high, while today's top-performing sector-consumer discretionary-has extended its gain to 1.2%. The sector has held the lead since the open and no other group trades with a gain larger than 0.5% at this time.

Elsewhere among influential sectors, health care (+0.5%) and technology (+0.5%) both trade in line with the broader market, while financials (+0.3%) and industrials (+0.2%) continue showing relative weakness.

With stocks on highs, participants are not showing much concern about a potential slide as the CBOE Volatility Index (VIX 11.57, -0.41) hovers near its session low.

Also of note, Treasuries have reclaimed virtually all of their losses. The 10-yr note has trimmed its loss to just one tick and its yield is now at 2.56%.

2:10 pm: [BRIEFING.COM] The major averages have ticked down from their highs in reaction to the FOMC minutes that were just released.

Most notably, the minutes indicated that some officials believed that investors have displayed too much complacency with regard to risk.

Also of note, the minutes revealed that the committee has discussed its exit strategy tools with the general expectation of a final $15 billion taper taking place in October if the current outlook remains steady.

Treasuries inched lower in reaction to the release, but are now back at their previous levels. The 10-yr note is lower by 10 ticks with its yield up four basis points at 2.59%.

1:25 pm: [BRIEFING.COM] The Dow, Nasdaq, and S&P 500 are pushing close to their best levels of the day in the final lead up to the release of the minutes for the June FOMC meeting at 2:00 p.m. ET.

Every sector, with the exception of the utilities sector (-0.6%), is trading higher today. Accordingly "weak" sectors are measured mostly in terms of which sectors are up the least than they are by which sectors are down the most. With the S&P 500 (+0.3%) serving as the benchmark, the financial (+0.1%), industrials (+0.1%), and telecom services (+0.1%) fit that bill.

Elsewhere, the $21 bln 10-yr note reopening didn't help matters for the benchmark note, which has been on the defensive throughout the day. It was a relatively weak auction on the demand side, yet it may have been asking too much of bidders to take down the supply a short time in front of the FOMC Minutes being released.

The reopening drew a high yield of 2.597% with a bid-to-cover ratio of 2.57 that trailed the prior 12-auction average of 2.68x. The 10-yr note slipped to new lows for the day in the wake of the results.

1:00 pm: [BRIEFING.COM] At midday, the major averages hold modest gains with the Nasdaq Composite (+0.4%) trading a bit ahead of the S&P 500 (+0.2%). For its part, the Russell 2000 (+0.1%) displayed early strength before slipping behind the benchmark index.

Stocks rallied at the open, but slumped from their early highs as small-caps proved unable to hold their opening gains. However, that slip was not enough to spook investors as they pushed the S&P 500 to a test of its early high at 1971. At this time, the benchmark index hovers within three points of its best level of the day.

It is worth mentioning that trading ranges have narrowed noticeably over the past 90 minutes or so as some participants stick to the sidelines ahead of this afternoon's (14:00 ET) release of the FOMC minutes from the June meeting.

Eight of ten sectors hold gains at this juncture with the consumer discretionary space (+0.9%) in the lead. The sector has been supported by restaurant and retail stocks, which have rallied despite cautious comments about the strength of the industry made by the CEO of The Container Store (TCS 24.23, -2.84). Shares of TCS trade lower by 10.5% following disappointing earnings.

Elsewhere among top-weighted cyclical sectors, technology (+0.3%) trades a bit ahead of the broader market, while financials (unch) and industrials (unch) lag.

The industrial sector trades flat even as transport stocks outperform. The Dow Jones Transportation Average is higher by 0.3% with Delta Air Lines (DAL 36.81, +0.37), Southwest Airlines (LUV 26.97, +0.27), and JetBlue (JBLU 10.70, +0.21) up between 1.0% and 2.0% after American Airlines (AAL 41.75, +1.49) reported strong metrics for June. However, the industry-wide strength has overshadowed a 7.0% gain in the shares of Matson (MATX 29.25, +1.90) after BB&T upgraded the stock to 'Buy' from 'Hold.'

Treasuries hover near their lows that were notched this morning. The 10-yr note is lower by six ticks with its yield up two basis points at 2.580%.

Economic data reported this morning was limited to the weekly MBA Mortgage Index, which rose 1.9% to follow last week's downtick of 0.2%.

12:30 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.2% after having spent the better part of the past hour in a two-point range. Meanwhile, the tech-heavy Nasdaq (+0.4%) sits right below its best level of the trading day.

The Nasdaq owes its outperformance to a handful of top-weighted components like Apple (AAPL 95.74, +0.39), Google (GOOGL 582.78, +4.38), and Facebook (FB 64.45, +1.69). The three names hold gains between 0.4% and 2.7% with Facebook in the lead. The stock has erased a portion of yesterday's plunge, while other social media names are somewhat mixed. Twitter (TWTR 38.20, +0.79) is higher by 2.2%, whereas Yelp (YELP 70.40, -0.31) trades down 0.4%.

In addition, the Nasdaq has benefitted from the relative strength of biotechnology as the iShares Nasdaq Biotechnology ETF (IBB 255.05, +1.42) trades up 0.6%.

12:00 pm: [BRIEFING.COM] Equity indices remain near their recent levels as range-bound action continues. With the FOMC minutes from the June meeting scheduled for a 14:00 ET release, there is a good chance that the action in the stock market will be largely uneventful until then.

Once the minutes cross the wires this afternoon, the top-weighted sectors will be in focus considering they have the potential to send the market to fresh highs or fuel a noteworthy reversal. At this time, the five largest sectors trade in mixed fashion. Consumer discretionary (+0.7%) and technology (+0.3%) outperform, while financials (unch) and industrials (unch) lag.

Elsewhere, Treasuries remain near their lowest levels of the day with the 10-yr yield up two basis points at 2.58%.

11:30 am: [BRIEFING.COM] Stocks continue drifting inside relatively narrow ranges with the S&P 500 trading higher by 0.3%. Small-cap stocks, however, are struggling to gain traction with the Russell 2000 back near its flat line once again.

Unlike the small-cap index, high-beta biotech names remain near their best levels of the session. The iShares Nasdaq Biotechnology ETF (IBB 254.85, +1.22) trades higher by 0.5%, while the broader health care sector (+0.1%) sits just above its flat line.

It is worth mentioning that health care is not the only heavily-weighted group that has had a tough time maintaining its opening gain. The industrial sector is back at its flat line, while financials (+0.1%) continue holding a slim gain.

10:55 am: [BRIEFING.COM] The major averages have returned to their opening highs after a brief dip took the S&P 500 back near its flat line. The benchmark index now trades higher by 0.3% with nine sectors in the green.

Today's top performing sector-consumer discretionary-has extended its advance to 0.8%, while another group that showed early strength-industrials-hovers near its low (+0.1%). Elsewhere among influential sectors, technology (+0.3%) trades in line with the broader market, while health care (+0.2%) and financials (+0.2%) follow a bit behind.

On the downside, the lone decliner-utilities-holds a loss of 0.3% after showing relative strength during the past two sessions.

10:35 am: [BRIEFING.COM]

Dollar index sold off and hit a new LoD, but this really isn't doing anything for commodities. The dollar index is now -0.1% at 80.07.

Crude oil sold off this morning and hit a new LoD just ahead of the weekly EIA oil inventory data. Crude remained near that LoD just ahead off the EIA inventory data

Following this data, Aug crude oil popped a little higher and is now -0.8% at $102.58/barrel

Gold and silver have been in positive territory all day so far

Aug gold is currently +0.6% at $1324.40/oz, while Sept silver is +0.5% at $21.12/oz

Sept copper sold off in recent trade, erasing morning gains. Sept copper is currently +0.1% at $3.26/lb

Natural gas rallied in morning trade to the current HOD of $4.23/MMBtu. Aug NG is now +0.4% at $4.22/MMBtu

10:00 am: [BRIEFING.COM] Equity indices have come down from their opening highs with the Russell 2000 dipping into the red, while eight S&P 500 (+0.2%) sectors hold gains of no more than 0.5%.

The consumer discretionary space is the top performer at this time with homebuilders contributing to the strength. DR Horton (DHI 24.63, +0.28) trades up 1.2%, while the broader iShares Dow Jones US Home Construction ETF (ITB 24.45, +0.10) is higher by 0.5%.

Meanwhile, retailers also trade ahead of the broader market despite cautious comments from the Container Store (TCS 23.85, -3.27) CEO on the state of the industry. The SPDR S&P Retail ETF (XRT 86.97, +0.24) is higher by 0.3%.

9:40 am: [BRIEFING.COM] The major averages climbed out of the gate with yesterday's laggard-Russell 2000-in the lead. The index trades higher by 0.6%, while the S&P 500 sports an advance of 0.3% with all ten sectors showing opening gains.

In general, cyclical sectors that were battered over the past two days have been able to start the trading day in the lead. On that note, consumer discretionary (+0.5%), technology (+0.4%), and industrials (+0.4%) all trade ahead of the broader market.

Notably, the industrial sector has received support from transport stocks after American Airlines (AAL 42.01, +1.75) released upbeat metrics. All 20 components of the Dow Jones Transportation Average (+0.9%) hold gains with Matson (MATX 28.91, +1.56) in the lead. The stock trades higher by 5.7% after being upgraded at BB&T Capital Markets to 'Buy' from 'Hold.'

9:13 am: [BRIEFING.COM] S&P futures vs fair value: +5.70. Nasdaq futures vs fair value: +12.50. For the first time this week, the stock market is on track for a higher open as futures on the S&P 500 trade six points above fair value.

Futures spent the bulk of the overnight session in the green and resisted the selling efforts that pressured markets in Shanghai (-1.2%) and Hong Kong (-1.6%) following a softer than expected CPI reading from China (2.3% year-over-year versus expected 2.4%).

Index futures then cruised to new highs in reaction to upbeat June metrics provided by American Airlines (AAL 42.38, +2.12). The stock holds a pre-market gain of 5.3%, while Dow Jones Transportation Average members like Delta Air Lines (DAL 37.61, +1.17) and United Continental (UAL 40.59, +1.05) are on track to jump 3.1% and 2.7%, respectively at the open.

While the transports are expected to receive an early boost, the same cannot be said for retailers. Last evening, Container Store (TCS 22.94, -4.13) reported disappointing results for the quarter, but forward-looking comments made during the conference call were just as concerning with the company's CEO acknowledging the retail sector is in a 'funk.'

Treasuries hold modest losses after spending the entire night in the red. The 10-yr yield is higher one basis point at 2.57%.

8:56 am: [BRIEFING.COM] S&P futures vs fair value: +5.40. Nasdaq futures vs fair value: +12.50. The S&P 500 futures trade five points above fair value.

Markets in Asia finished lower across the board. The Hong Kong Monetary Authority injected HKD1.938 billion into the system in defense of the strong-end of its range. Elsewhere, early indications suggest Jakarta Governor Joko Widodo has claimed a narrow victory in the Indonesian presidential election, but nothing has been made official yet.

In economic data:

China's CPI slipped 0.1% month-over-month (previous 0.1%), while the year-over-year reading rose 2.3% (consensus 2.4%, prior 2.5%). Separately, PPI fell 1.1% year-over-year (expected -1.0%, last -1.4%)

Australia's Westpac Consumer Sentiment rose 1.9% (previous 0.2%)

New Zealand's Electronic Card Retail Sales were unchanged month-over-month (expected 0.2%, previous 1.3%), while the year-over-year reading increased 4.0% (last 7.6%)

------

Japan's Nikkei slipped 0.1%, remaining near its best level in almost six months. Exporters were pressured with Toyota Motor falling 1.1% and Sony Corp losing 1.2%

Hong Kong's Hang Seng fell 1.6%, sliding off its best levels of 2014. Casino stocks remained under pressure for a third session after Standard Chartered downgraded the sector. Sands China gave up 2.2% and Wynn Macau tumbled 4.1%.

China's Shanghai Composite fell 1.2% to its lowest level in a week and a half with trade settling on the 50-day moving average. Financials were weak with Bank of China off 0.8% and ICBC down 1.4%.

Major European indices trade mostly higher, but Great Britain's FTSE (-0.4%) is struggling to keep up with the rest of the region. European Central Bank member Peter Praet commented on regional inflation, saying weak price pressure has extended into non-stressed countries and that core inflation was also trending below potential

Economic data was limited:

Great Britain's Halifax House Price Index fell 0.6% month-over-month (consensus 0.2%, previous 4.0%), while the year-over-year reading jumped 8.8% (forecast 8.9%, prior 8.7%)

------

Great Britain's FTSE holds a loss of 0.4% with Admiral Group factoring into the weakness. The insurer trades down 5.9% after issuing a cautious outlook. Airlines outperform with easyJet and International Consolidated Airlines up 2.8% and 1.0%, respectively.

In France, the CAC trades up 0.1%. Technology and telecom names appear among the leaders with Gemalto and Orange holding respective gains of 2.0% and 0.7%. Financials lag with BNP Paribas and Societe Generale both down near 1.5%.

Germany's DAX is higher by 0.2%. Deutsche Lufthansa leads with a 2.9% gain, while adidas is the weakest performer, down 1.8%.

Italy's MIB outperforms with a gain of 0.9%. Financials are responsible for the bulk of the move as BMPS, Banco Popolare, Mediobanca, and Intesa Sanpaolo trade up between 1.7% and 2.9%.

8:28 am: [BRIEFING.COM] S&P futures vs fair value: +6.70. Nasdaq futures vs fair value: +13.70. U.S. equity futures remain bid with the S&P 500 futures recently climbing to fresh highs.

Index futures spiked after American Airlines (AAL 42.25, +1.99) reported solid June metrics, which also gave a boost to the likes of Delta Air Lines (DAL 37.40, +0.96), Southwest Airlines (LUV 27.44, +0.74), and United Continental (UAL 40.60, +1.06). If the early indication holds into the opening bell, the strength among airlines should underpin the Dow Jones Transportation Average.

7:55 am: [BRIEFING.COM] S&P futures vs fair value: +5.00. Nasdaq futures vs fair value: +10.70. U.S. equity futures trade modestly higher amid subdued action overseas. The S&P 500 futures hover five points above fair value.

Reviewing overnight developments:

Asian markets ended on a lower note. Japan's Nikkei -0.1%, China's Shanghai Composite -1.2%, and Hong Kong's Hang Seng -1.6%

Participants received several data points:

China's CPI slipped 0.1% month-over-month (previous 0.1%), while the year-over-year reading rose 2.3% (consensus 2.4%, prior 2.5%). Separately, PPI fell 1.1% year-over-year (expected -1.0%, last -1.4%)

Australia's Westpac Consumer Sentiment rose 1.9% (previous 0.2%)

New Zealand's Electronic Card Retail Sales were unchanged month-over-month (expected 0.2%, previous 1.3%), while the year-over-year reading increased 4.0% (last 7.6%)

In news:

Markets in China and Hong Kong slumped after the release of the latest inflation data that showed softer than expected growth in consumer prices. Japan's Nikkei, however, outperformed thanks to a measure of support provided by dollar strength against the yen. The dollar/yen pair is currently modestly higher at 101.69

Major European indices trade in mixed fashion. Great Britain's FTSE -0.6%, France's CAC is flat, and Germany's DAX +0.1%. Elsewhere, Italy's MIB +0.5% and Spain's IBEX +0.2%

Economic data was limited:

Great Britain's Halifax House Price Index fell 0.6% month-over-month (consensus 0.2%, previous 4.0%), while the year-over-year reading jumped 8.8% (forecast 8.9%, prior 8.7%)

Among news of note:

European Central Bank member Peter Praet commented on regional inflation, saying weak price pressure has extended into non-stressed countries and that core inflation was also trending below potential

In U.S. corporate news:

Alcoa (AA 15.16, +0.31): +2.1% after beating earnings and revenue estimates. The company reaffirmed its global aluminum demand growth guidance at 7.0% and hiked its commercial transportation guidance for N. America

AeroVironment (AVAV 32.52, +1.56): +5.0% following its better than expected results

Container Store (TCS 22.88, -4.19): -15.5% in reaction to a bottom-line miss and soft guidance that cited weak retail environment

Reynolds American (RAI 62.60, +1.29): +2.1% following reports in the IFA Magazine, suggesting British American Tobacco (BAT 121.97, -0.89) could make an offer the company. Lorillard (LO 60.58, -2.35) was previously mentioned as a suitor for RAI, but the stock trades lower by 3.7% in reaction to today's reports

The weekly MBA Mortgage Index rose 1.9% to follow last week's downtick of 0.2%.

The minutes from the June FOMC meeting will be released at 14:00 ET.

6:40 am: [BRIEFING.COM] S&P futures vs fair value: +4.00. Nasdaq futures vs fair value: +10.00.

6:39 am: [BRIEFING.COM] Nikkei...15302.65...-11.80...-0.10%. Hang Seng...23176.07...-365.30...-1.60%.

6:39 am: [BRIEFING.COM] FTSE...6708.84...-29.50...-0.40%. DAX...4337.60...-4.90...-0.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage