Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

073114-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3120.00.png [ 175.66 KiB | Viewed 497 times ]

073114-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3120.00.png [ 175.66 KiB | Viewed 497 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,120.00 dollars or +31.20 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,120.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=132&t=1850 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=242&t=2402 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

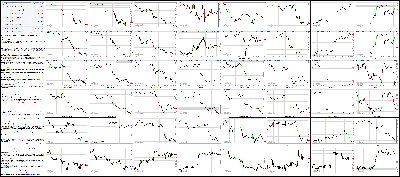

Dow Plunges 317 Points, Now Down For Year Attachment:

073114-Key-Price-Action-Markets.png [ 1.16 MiB | Viewed 471 times ]

073114-Key-Price-Action-Markets.png [ 1.16 MiB | Viewed 471 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

The best thing we can say about Thursday's stock market trading is that it is now over. The Dow fell 317 points, erasing all of its gains for the year.

The S&P 500 and Nasdaq fell sharply as well, each down about 2%. They gave back the all the gains they had made in July.

Heavy selling overseas, driven by worries about Argentina's latest debt default and more problems with a big Portuguese bank, combined with a slew of negative earnings and a disappointing outlook on manufacturing from the Federal Reserve Bank of Chicago to drop stocks.

The VIX (VIX), a gauge of market volatility, jumped almost 27%. CNNMoney's Fear & Greed Index, which includes the VIX and six other gauges of sentiment, is showing signs of "Extreme Fear."

International markets: European markets fell broadly, with the EuroStoxx 50 index ending the day down 1.7%. Lisbon-listed shares of Banco Espirto Santo (BKESF), the Portuguese bank whose deteriorating funding situation have brought the spotlight back to Southern Europe's shaky banks, was down 42%.

Asian markets, outside of strongly performing Chinese stocks, were also lower.

Argentina failed to reach an agreement with bondholders and defaulted late Wednesday. Argentina's benchmark Merval index plunged more than 8%.

Related: No deal in Argentina means second default in 13 yearsFood fails and other movers: Yum Brands (YUM), the conglomerate behind KFC, Taco Bell and Pizza Hut, warned that the tainted meat scandal in China could hurt its profits for the year. The stock dropped 5%.

Related: KFC just can't catch a break in its hugely important Chinese marketWhole Foods (WFM) is also hurting. Despite reporting good earnings, the company disappointed on sales and also cut its outlook guidance once again, raising questions about the company's future direction. Its shares, which have been among the worst performers this year, are down more than 2%.

Kellogg (K) did the same, reporting a good quarter but cutting guidance. Kraft (KRFT) had an out-and-out bad quarter. Both stocks fell more than 6%.

3-D printing stocks are sinking after a poor earnings report from 3D Systems (DDD). Its shares dived almost 11% and that put pressure on rivals voxelJet (VJET), Stratasys (SSYS) and ExOne (XONE), which are all down.

And momentum stock darling GoPro (GPRO), which has surged since going public, failed to live up to the hype. The camera maker's stock fell nearly 10% after hours even though earnings and sales topped forecasts.

Bright Spots: But there was some good news after hours. Tesla (TSLA) and LinkedIn (LNKD, Tech30) both rose in extended trading following better-than-expected results.

A few big names managed to hold up well in regular trading too. T-Mobile (TMUS) was up 6.5% following reports that French telecom firm Iliad made a buyout offer. Sprint (S), long considered a potential merger partner, is down 5%.

Related: Takeover rumor sends T-Mobile higherBusiness card maker Vistaprint (VPRT) surprised analysts by turning a profit on strong sales, skyrocketing 30.5%.

World Wrestling Entertainment (WWE), after announcing that it was cutting 7% of its workforce, rose more than 3%.

Related: WWE slams workersAnd red-hot grilled chicken IPO El Pollo Loco (LOCO) was up 12% today.

Glu not holding: Glu Mobile (GLUU) developed a wildly popular game based around celebrity Kim Kardashian, but Wall Street isn't impressed. Even though results beat expectations, the stock is dropped 18% after announcing that it was buying Cie Games for $100 million.

Related: Kim Kardashian's game makes $700,000 a dayImpossible is Russia: Adidas (ADDDF), which finished the day down 15% in Germany, is also lowering its guidance, saying that its reducing its Russian footprint by closing stores or delaying new openings. Golf sales are also lower. It joins McDonald's (MCD) and Wendy's (WEN) in reporting difficulties operating in the country.

4:20 pm: [BRIEFING.COM] The stock market punctuated July with a broad-based retreat that sent the S&P 500 lower by 2.0% with all ten sectors ending in the red. The benchmark index posted a monthly decline of 1.5%, while the Russell 2000 (-2.3%) underperformed to end the month lower by 6.1%.

To get a better feel for what led to today's retreat, we'd like to look back to Wednesday, when the market had ample reason to rally, but did not. Instead, it ended basically flat after a sloppy day of trading where good news was marveled at -- Q2 GDP and earnings results -- but not acted on with any real conviction from buyers. A spike in long-term rates and worries the Fed could raise the fed funds rate sooner than expected (a worry the FOMC directive didn't refute in unequivocal fashion) garnered most of the blame for the lackluster response.

That inability to rally on a batch of good economic and earnings news left the stock market increasingly vulnerable to a larger pullback in the event any bad news came its way. Sure enough, there were some overnight headlines that rattled weak-handed positions:

Related Stories

Stock Market News for July 14, 2014 Zacks

InPlay from Briefing.com Briefing.com

Dow dives 317 points, turns negative for year: stock market live blog recap MarketWatch

Asia stocks mixed on China PMI, global selloff; Sony rallies 6% CNBC

Worries about consumers drag stocks lower Los Angeles Times

Eurozone CPI was up just 0.4% year-over-year in July (expected 0.5%), triggering renewed worries about deflation

Argentina was deemed to be in default on its bond payments

Portuguese bank Banco Espirito Santo reported a big net loss for the first half of the year that wiped out its capital buffer and drove its stock price down 50%, reminding investors that there are still issues present in the European banking system

With the sentiment taking a turn for the worse, a batch of poor quarterly results from a handful of global players contributed to the slide. Samsung kicked things off overnight with below-consensus earnings that sent the stock lower by 3.7% in Seoul. Things did not get much better during the European session with Adidas and Deutsche Lufthansa posting respective earnings-driven losses of 15.4% and 6.4% in Frankfurt. The DAX Index, meanwhile, lost 1.9%.

Back in the U.S., market participants received a set of earnings that did not quite live up to the high standard that was set during the first two weeks of the reporting period with earnings growth pushing 9.0%, according to S&P Capital IQ.

On that note, 3D Systems (DDD 50.13, -5.94), Mosaic (MOS 46.11, -1.07), Beazer Homes (BZH 15.35, -1.95), and Ocwen Financial (OCN 30.17, -4.49), registered losses between 2.3% and 13.0% after disappointing with their results. Furthermore, even above-consensus earnings from the likes of Akamai Technologies (AKAM 59.02, -1.71), MasterCard (MA 74.15, -1.76), and Yelp (YELP 67.16, -8.44) were met with selling activity.

The ten economic sectors registered losses between 1.7% (utilities) and 2.4% (energy). Rate-sensitive telecom services (-2.3%) and utilities outperformed in the early going as participants sought cover in the defensively-oriented sectors, but the two groups could not avoid being engulfed in the selling activity.

Elsewhere, the top-weighted sector-technology (-2.0%)-suffered from broad pressure. Influential listings like Apple (AAPL 95.60, -2.55), Google (GOOGL 579.55, -15.89), Facebook (FB 72.65, -2.03), and Qualcomm (QCOM 73.72, -2.32) lost between 2.6% and 3.1%, while chipmakers also tumbled. Notably, Micron (MU 30.55, -1.98) plunged 6.1% amid cautious comments from Goldman Sachs, while the broader PHLX Semiconductor Index fell 2.1%.

Biotechnology did not fare much better with the iShares Nasdaq Biotechnology ETF (IBB 250.83, -6.42) sliding 2.5%. For its part, the health care sector lost 2.0%, surrendering its entire monthly gain.

Only technology and telecom services were able to post July gains of 1.4% and 2.6%, respectively, while the utilities sector lost 6.9% for the month.

Treasuries ended flat after regaining their early morning losses. The 10-yr yield settled at 2.56%.

The selloff invited above-average participation with more than 900 million shares changing hands at the NYSE.

Economic data included Initial Claims, the Employment Cost Index, and the Chicago PMI report:

The initial claims level increased to 302,000 from a downwardly revised 279,000 (from 284,000)

The Briefing.com consensus expected the initial claims level to increase to 310,000

The Employment Cost Index increased 0.7% in Q2 2014, up from a 0.3% increase in the first quarter, while the Briefing.com consensus expected an increase of 0.4%

Wages and salaries rose 0.6% in the second quarter, up from a 0.3% increase in Q1

Benefits spending rose 1.0% and is up 2.5% year-over-year

Manufacturing activities in the Chicago region softened significantly in July as the Chicago PMI fell to 52.6 from 62.6 in June

The Briefing.com consensus expected a more modest decline to 61.8

Tomorrow's session will be full of economic data starting with the 8:30 ET release of the Nonfarm Payrolls report for July (Briefing.com consensus 220K). Personal Income/Spending (consensus 0.4%) data and Core PCE Prices (expected 0.2%) will also be reported at 8:30 ET, while the final reading of the Michigan Sentiment survey for July (consensus 82.0) will cross the wires at 9:55 ET. Finally, the July ISM Index (consensus 55.9) and June Construction Spending (expected 0.3%) will both be reported at 10:00 ET.

S&P 500 +4.5% YTD

Nasdaq Composite +4.6% YTD

Dow Jones Industrial Average -0.1% YTD

Russell 2000 -3.7% YTD

3:30 pm: [BRIEFING.COM]

Dec gold fell deeper into negative territory after pulling back from a session high of $1295.30 per ounce set at the open of floor trade. It brushed a session low of $1281.90 per ounce moments before settling with a 1.1% loss at $1283.10 per ounce.

Sep silver touched a session high of $20.70 per ounce in early morning action but retreated into the red. Unable to regain momentum, it settled 0.9% lower at $20.41 per ounce, just above its session low of $20.40 per ounce.

Sep crude oil fell below the $100 per barrel level today, extending losses for a fourth consecutive session. It traded as low as $98.05 per barrel and settled with a 2.1% loss at $98.12 per ounce.

Sep natural gas rallied into positive territory from its session low of $3.76 per MMBtu after inventory data showed a build of 88 bcf vs expectations for a build of 90-93 bcf. It climbed to a session high of $3.89 per MMBtu and settled at $3.84 per MMBtu, or 1.6% higher.

3:05 pm: [BRIEFING.COM] The S&P 500 trades lower by 1.7% with one hour remaining in the final session of the month.

Quarterly earnings will take center stage again after today's closing bell with more than 120 companies appearing on the schedule. High-growth names like Tesla (TSLA 225.05, -3.87), Trulia (TRLA 60.09, -2.51), and LinkedIn (LNKD 181.04, -6.25) will be in focus, while tomorrow's list will be headlined by ArcelorMittal (MT 15.26, -0.31), Chevron (CVX 129.90, -2.63), and Procter & Gamble (PG 77.44, -0.72).

2:30 pm: [BRIEFING.COM] The S&P 500 (-1.4%) remains within five points of its session low, while all ten sectors hold losses in excess of 1.0%.

Interestingly, the broad losses in the market have not stopped a recent IPO-El Pollo Loco (LOCO 38.77, +4.21) from charging higher. The stock made its debut last Friday and has only registered one losing session (Tuesday) since then. The quick-service restaurant opened at $19.00 on Friday and is up 104% since then.

1:55 pm: [BRIEFING.COM] The S&P 500 has inched up from its worst level of the session, but that could be overlooked considering the index remains lower by 28 points.

Today's retreat has sent the benchmark average below its 50-day moving average (1953) for the first time in a while. Specifically, the index tested, but never closed below the 50-day average on six occasions during a three-week stretch between late April and early May. Prior to that span, the S&P 500 dove below the 50-day moving average on April 10, but was back above the key level on April 16.

Elsewhere, the Russell 2000 (-1.8%) has been pressured below its 200-day moving average and if the session ended at this time, the index would register its worst close since early June.

1:30 pm: [BRIEFING.COM] The stock market is experiencing one of its worst days in some time. Every Dow component is lower at this time and every sector is sporting a loss of at least 1.0%. The A/D line at the NYSE favors decliners by a 10-to-1 margin.

We acknowledged many of the reasons in our midday summary why the market is doing so poorly. We won't rehash them here, only we'll add that today is peculiar because there isn't a rotation within the stock market to defensive-oriented sectors.

There is just a broad move out of stocks that speaks to a de-risking trade at work on this last day of the month.

Some of that is owed to the recognition that the stock market has failed to break out to higher levels in convincing fashion despite getting a stream of better than expected economic and earnings news for a while now. To some, that suggests the good news was already priced in and it has prompted a profit-taking mindset. That disposition, in turn, has probably shaken a lot of weak-handed positions out of the market that had been chasing the thought of a breakout move, thereby exacerbating today's losses.

1:05 pm: [BRIEFING.COM] The major averages trade lower across the board at midday. The Dow Jones Industrial Average and S&P 500 hold respective losses of 1.3% and 1.4%, while the Nasdaq Composite (-1.7%) and Russell 2000 (-1.9%) lag.

The concise view of things is that the stock market had ample reason to rally on Wednesday, but did not. Instead, it ended basically flat after a sloppy day of trading where good news was marveled at -- Q2 GDP and earnings results -- but not acted on with any real conviction from buyers. A spike in long-term rates and worries the Fed could raise the fed funds rate sooner than expected (a worry the FOMC directive didn't refute in unequivocal fashion) garnered most of the blame for the lackluster response.

That inability to rally on a batch of good economic and earnings news left the stock market increasingly vulnerable to a larger pullback in the event any bad news came its way. Sure enough, there were some overnight headlines that rattled weak-handed positions:

Eurozone CPI was up just 0.4% year-over-year in July (expected 0.5%), triggering renewed worries about deflation

Argentina was deemed to be in default on its bond payments

Portuguese bank Banco Espirito Santo reported a big net loss for the first half of the year that wiped out its capital buffer and drove its stock price down 50%

Adding insult to injury was a set of disappointing earnings from a handful of global companies. Samsung kicked things off overnight with below-consensus results that sent the stock lower by 3.7% in Seoul. Things did not get much better during the European session with Adidas and Deutsche Lufthansa posting respective earnings-driven losses of 15.4% and 6.4% in Frankfurt. The DAX Index, meanwhile, lost 1.9%.

Domestically, market participants received a batch of earnings that did not quite live up to the high standard that was set during the first two weeks of the reporting period with earnings growth pushing 9.0%, according to S&P Capital IQ.

As such, a modest dose of disappointing results was enough to fuel the fire of broad-based profit taking.

All ten sectors hold midday losses with nine groups down at least 1.2%. The top-weighted S&P 500 sector-technology (1.5%)-sits near the bottom of the leaderboard and only the telecom services (-2.0%) sector separates the influential group from the last spot. Blue chip names like Apple (AAPL 95.88, -2.27), Google (GOOGL 583.05, -12.39), and Qualcomm (QCOM 73.94, -2.10) display losses between 2.1% and 2.8%, while chipmakers also trade broadly lower. The PHLX Semiconductor Index trades down 1.9%.

Also of note, Akamai Technologies (AKAM 59.54, -1.19) and Yelp (YELP 67.50, -8.10) are down 1.9% and 10.7%, respectively, despite beating earnings estimates.

With today's session marking the end of the month, the S&P 500 is on track to end July with a 0.9% decline, while the Russell 2000 has surrendered 6.0% since the end of June.

Treasuries hold slim gains after erasing their earlier losses. The 10-yr note is higher by two ticks with its yield down one basis point at 2.55%.

Economic data included Initial Claims, the Employment Cost Index, and the Chicago PMI report:

The initial claims level increased to 302,000 from a downwardly revised 279,000 (from 284,000)

The Briefing.com consensus expected the initial claims level to increase to 310,000

The Employment Cost Index increased 0.7% in Q2 2014, up from a 0.3% increase in the first quarter, while the Briefing.com consensus expected an increase of 0.4%

Wages and salaries rose 0.6% in the second quarter, up from a 0.3% increase in Q1

Benefits spending rose 1.0% and is up 2.5% year-over-year

Manufacturing activities in the Chicago region softened significantly in July as the Chicago PMI fell to 52.6 from 62.6 in June

The Briefing.com consensus expected a more modest decline to 61.8

12:30 pm: [BRIEFING.COM] The S&P 500 trades lower by 1.6% with dip-buyers showing reluctance to step in amid continued broad weakness.

Recent action saw crude oil drop to a fresh low, which puts the energy component ($98.52/bbl) down 1.7% for the session. Meanwhile, the energy sector (-1.7%) was the weakest performer at the start of the day, but now trades a bit ahead of technology (-1.8%) and telecom services (-2.3%).

The top-weighted S&P 500 sector-technology-lags amid broad pressure. Blue chip names like Apple (AAPL 95.42, -2.73), Google (GOOGL 582.04, -13.40), and Qualcomm (QCOM 73.98, -2.06) display losses between 2.2% and 2.8%, while chipmakers also trade broadly lower. The PHLX Semiconductor Index holds a loss of 2.3%.

12:05 pm: [BRIEFING.COM] Equity indices continue drifting near their lows with eight sectors showing losses of 1.3% or more. Meanwhile, telecom services (-1.7%) and utilities (-0.9%) displayed relative strength earlier, but both have given in to the broad pressure.

While the major averages are now on track to end the month on their lows, the CBOE Volatility Index (VIX 15.78, +2.45) is poised to finish July at its highest level since mid-April. This has marked a quick turn for the near-term volatility measure that registered its lowest close since early 2007 as recently as July 3.

Elsewhere, Treasuries have now climbed into the green, pressuring the 10-yr yield down to 2.55 (-1 bp).

11:35 am: [BRIEFING.COM] Sellers remain in control with the Russell 2000 now down 2.0%. Including its current loss, the index is now lower by 5.6% in July. Meanwhile, the Dow (-1.1%), Nasdaq (-1.7%), and S&P 500 (-1.3%) entered the session with modest July gains that have now been turned into losses between 0.3% and 0.8%.

At this juncture, health care, technology, and telecom services are the only sectors that are on pace to register July gains. Technology and telecom services sport respective month-to-date gains of 2.0% and 4.0%, while the health care sector has added 0.6% this month. On the downside, the utilities sector has surrendered 6.1% in July.

Treasuries have reclaimed all of their losses and the benchmark 10-yr yield is now at 2.56%, which represents a four-basis point increase since the end of June.

10:55 am: [BRIEFING.COM] Not much change in the major averages as they remain near their lowest levels of the session. The S&P 500 has widened its loss to 1.2% with just about every sector extending its decline.

However, two rate-sensitive groups-telecom services (-0.8%) and utilities (-0.6%)-have been able to climb off their lows even as the 10-yr yield remains higher on the day (+2 bps at 2.58%).

On the flip side, the energy sector (-1.5%) occupies the bottom of the leaderboard, while crude oil holds a loss of 0.7% at $99.58/bbl. Top-weighted sector component, ExxonMobil (XOM 100.98, -2.27), reported better than expected earnings this morning, but its stock trades lower by 2.2%.

10:35 am: [BRIEFING.COM]

Natural gas futures sold off this morning ahead of today's EIA weekly natural gas inventory data and hit a new LoD

Nat gas popped to a new HoD following the data and is now +1.5% at $3.84/MMBtu

Crude oil futures have been in the red all day so far and is currently near its LoD. Sept crude is now -0.8% at $99.51/barrel

Precious metals sold off earlier this morning and are also sitting near its LoD.

Dec gold is now -0.7% at $1288.20/oz, while Sept silver is -0.4% at $20.52/oz

Sept copper is -0.2% at $3.24/lb

10:00 am: [BRIEFING.COM] Equity indices remain pinned to their lows with the Russell 2000 (-1.1%) showing the largest loss that has placed the small-cap index back below its 200-day moving average (1144). The Russell 2000 has been battling with that key level during the past two weeks and is now on course to finish the month below its 200-day moving average.

For its part, the S&P 500 (-0.8%) has dipped to its 50-day moving average (1953), which represents the first test of that level since mid-May.

The energy sector (-1.0%) remains at the bottom of the leaderboard, while the utilities sector (-0.3%) trades ahead of the remaining groups.

9:45 am: [BRIEFING.COM] The major averages slipped out of the gate with the S&P 500 (-0.8%) surrendering its July gain. The benchmark index is now down 0.4% in July with today's session representing the last trading day of the month.

All ten sectors began the day in the red with energy (-1.1%), health care (-0.9%), industrials (-0.8%), and consumer discretionary (-0.8%) showing noteworthy losses. Meanwhile, the financial sector is the top performer, but the second-largest group is still down 0.6% in the early going.

Despite the early weakness in equities, Treasuries continue trading near their lowest levels of the morning with the 10-yr yield up two basis points at 2.58%.

Just released, the Chicago PMI for July slipped to 52.6 from 62.6, while the Briefing.com consensus expected a decrease to 61.8.

9:13 am: [BRIEFING.COM] S&P futures vs fair value: -12.90. Nasdaq futures vs fair value: -30.80. The stock market is on track to begin the session on a lower note as futures on the S&P 500 trade 13 points below fair value. Index futures have spent the entire overnight session in the red amid disappointing quarterly results from a handful of major global companies.

In South Korea, Samsung tumbled nearly 4.0% after reporting results in line with its warning from the beginning of the month, while the overall Kospi Index held up relatively well, shedding 0.3%. Meanwhile in Europe, the major averages trade broadly lower with Spain's IBEX down 2.0% amid weakness in companies with exposure to Latin America following Argentina's default. In Germany, Adidas and Deutsche Lufthansa reported below-consensus results.

Domestically, earnings have also been in focus with participants receiving a few more disappointing reports than they have gotten accustomed to in recent days. On that note, 3D Systems (DDD 48.69, -7.38), Kraft (KRFT 55.85, -1.39), and Whole Foods Market (WFM 36.95, -2.16) are indicated to open lower by 12.9% and 5.5%, respectively after disappointing with their earnings or guidance.

Also of note, Akamai Technologies (AKAM 56.50, -4.23) and Yelp (YELP 71.61, -3.99) are indicated to open lower despite beating estimates.

Treasuries are on their lows with the 10-yr yield up three basis points at 2.59%.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: -13.80. Nasdaq futures vs fair value: -33.00. The S&P 500 futures trade 14 points below fair value.

Markets in Asia ended on a mostly lower note, while indices in China and Hong Kong outperformed. Bangko Sentral ng Pilipinas hiked its key rate 25 basis points to 3.75% to fend off an uptick in inflation.

In economic data:

Japan's Average Cash Earnings increased 0.4% year-over-year (expected 0.7%, previous 0.6%), while Housing Starts fell 9.5% year-over-year (consensus -11.5%, previous -15.0%)

Australia's Building Approvals fell 5.0% month-over-month (expected -2.0%, previous 10.3%), while Private Sector Credit rose 0.7% month-over-month (consensus 0.4%, previous 0.4%). Separately, Import Price Index declined 3.0% quarter-over-quarter (expected -1.3%, previous 3.2%)

Hong Kong's Retail Sales fell 6.9% year-over-year (expected -5.1%, previous -4.1%)

Singapore's Unemployment Rate held steady at 2.0%, as expected

------

Japan's Nikkei shed 0.2%, slipping off six-month highs as traders booked profits following four days of gains. Fujifilm shed 0.8% following its earnings miss.

Hong Kong's Hang Seng inched up 0.1% to its best levels in more than three and a half years as buyers remained in control for an eighth session. The recent rally has come on the back of strength in the property sector with China Overseas Land & Development leading today's advance with a 4.6% gain.

China's Shanghai Composite gained 0.9%, rallying to its best level of 2014. Mining stocks saw robust gains as Zijin Mining Group and Zhongjin Goldcorp climbed 7.1% and 9.0%, respectively.

Major European indices trade lower across the board with Spain's IBEX (-2.1%) leading the retreat. Germany and Russia have reportedly engaged in discussions to broker a diplomatic solution to the situation in Ukraine with Russia pushing for the international community to recognize Crimea's independence.

Participants received several data points:

Eurozone CPI rose 0.4% year-over-year (expected 0.5%, previous 0.5%), while Core CPI increased 0.8% (consensus 0.8%, prior 0.8%). Separately, the Unemployment Rate ticked down to 11.5% from 11.6% (expected 11.6%)

Germany's Unemployment declined by 12,000 (expected -5,000, previous 7,000), while the Unemployment Rate held steady at 6.7%, as expected

Great Britain's Nationwide HPI rose 10.6% (expected 11.3%, previous 6.0%)

France's Consumer Spending rose 0.9% month-over-month (expected 0.1%, previous 0.7%), while PPI was unchanged month-over-month (consensus -0.1%, previous -0.5%)

Italy's Monthly Unemployment Rate slipped to 12.3% (expected 12.6%, previous 12.5%), while CPI ticked down 0.1% month-over-month (expected 0.1%, previous 0.1%). Also of note, PPI ticked up 0.1% month-over-month (consensus -0.1%, previous -0.1%)

Spain's Current Account deficit narrowed to EUR580 million from EUR1.60 billion

------

Great Britain's FTSE is lower by 0.3% with financials on the defensive. 3i Group, St James's Place, and Lloyds Banking are down between 2.6% and 3.2%. On the upside, Royal Dutch Shell is higher by 3.8% after beating earnings expectations.

In France, the CAC holds a loss of 1.1%. Alcatel-Lucent is the weakest component, down 6.3%, after reporting disappointing earnings. Financials also lag with AXA, Credit Agricole, and Societe Generale down between 2.1% and 4.1%.

Germany's DAX trades down 1.3%. Adidas and Deutsche Lufthansa hold respective losses of 14.5% and 5.2% after reporting disappointing earnings. Health care names outperform with Fresenius SE up 4.0% after beating earnings estimates.

Spain's IBEX holds a loss of 2.1%. Santander and Telefonica, both of which have a large exposure to Latin America, weigh with losses close to 1.7% apiece after Argentina's default. Drug maker Grifols is the weakest component, down 10.5% after reporting disappointing results.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: -10.30. Nasdaq futures vs fair value: -25.50. The S&P 500 futures trade ten points below fair value.

The latest weekly initial jobless claims count totaled 302,000, while the Briefing.com consensus expected a reading of 310,000. Today's tally was above the revised prior week count of 279,000 (from 284,000). As for continuing claims, they rose to 2.539 million from 2.508 million.

Separately, the Q2 Employment Cost Index rose 0.7%, while the Briefing.com consensus expected an increase of 0.4%.

8:05 am: [BRIEFING.COM] S&P futures vs fair value: -9.40. Nasdaq futures vs fair value: -25.00. U.S. equity futures are on the defensive amid cautious action overseas. Global equities have been pressured by disappointing earnings from heavyweights like Adidas, Samsung, and Lufthansa. The S&P 500 futures hover nine points below fair value.

Reviewing overnight developments:

Asian markets ended mixed. Japan's Nikkei -0.2%, Hong Kong's Hang Seng +0.1%, and China's Shanghai Composite +0.9%

In economic data:

Japan's Average Cash Earnings increased 0.4% year-over-year (expected 0.7%, previous 0.6%), while Housing Starts fell 9.5% year-over-year (consensus -11.5%, previous -15.0%)

Australia's Building Approvals fell 5.0% month-over-month (expected -2.0%, previous 10.3%), while Private Sector Credit rose 0.7% month-over-month (consensus 0.4%, previous 0.4%). Separately, Import Price Index declined 3.0% quarter-over-quarter (expected -1.3%, previous 3.2%)

Hong Kong's Retail Sales fell 6.9% year-over-year (expected -5.1%, previous -4.1%)

Singapore's Unemployment Rate held steady at 2.0%, as expected

In news:

Samsung tumbled 3.7% in Seoul after reporting earnings in line with the warning that was issued earlier in the month

Major European indices trade lower across the board. Great Britain's FTSE -0.2%, France's CAC -1.0%, and Germany's DAX -1.2%. Elsewhere, Italy's MIB -1.5% and Spain's IBEX -1.9%

Participants received several data points:

Eurozone CPI rose 0.4% year-over-year (expected 0.5%, previous 0.5%), while Core CPI increased 0.8% (consensus 0.8%, prior 0.8%). Separately, the Unemployment Rate ticked down to 11.5% from 11.6% (expected 11.6%)

Germany's Unemployment declined by 12,000 (expected -5,000, previous 7,000), while the Unemployment Rate held steady at 6.7%, as expected

Great Britain's Nationwide HPI rose 10.6% (expected 11.3%, previous 6.0%)

France's Consumer Spending rose 0.9% month-over-month (expected 0.1%, previous 0.7%), while PPI was unchanged month-over-month (consensus -0.1%, previous -0.5%)

Italy's Monthly Unemployment Rate slipped to 12.3% (expected 12.6%, previous 12.5%), while CPI ticked down 0.1% month-over-month (expected 0.1%, previous 0.1%). Also of note, PPI ticked up 0.1% month-over-month (consensus -0.1%, previous -0.1%)

Spain's Current Account deficit narrowed to EUR580 million from EUR1.60 billion

In news:

Germany and Russia have reportedly engaged in discussions to broker a diplomatic solution to the situation in Ukraine with Russia pushing for the international community to recognize Crimea's independence

In U.S. corporate news:

Alcatel Lucent (ALU 3.54, -0.30): -7.8% after missing bottom-line estimates

AstraZeneca (AZN 73.40, +0.21): +0.3% after beating earnings and revenue expectations

Colgate-Palmolive (CL 65.01, -1.10): -1.7% following its in-line earnings on better than expected revenue

Sony (SNE 18.00, +0.47): +2.7% after reporting strong results and raising its guidance

Western Digital (WDC 97.25, -3.92): -3.9% after its cautious guidance overshadowed better than expected earnings and revenue

Whole Foods Market (WFM 37.75, -1.36): -3.5% after beating estimates and issuing disappointing guidance. The company announced a share repurchase program in the amount of $1 billion

Yelp (YELP 71.00, -4.60): -6.1% despite beating earnings estimates and guiding above consensus

Weekly initial claims (Briefing.com consensus 310K) and the Q2 Employment Cost Index (consensus 0.4%) will be released at 8:30 ET and the day's data will be topped off with the 9:45 ET release of the Chicago PMI for July (expected 61.8).

8:01 am: [BRIEFING.COM] S&P futures vs fair value: -9.50. Nasdaq futures vs fair value: -24.50.

8:01 am: [BRIEFING.COM] Nikkei...15620.77...-25.50...-0.20%. Hang Seng...24756.85...+24.60...+0.10%.

8:01 am: [BRIEFING.COM] FTSE...6762.52...-10.90...-0.20%. DAX...9466.30...-127.40...-1.30%.

http://www.bloomberg.com/news/2014-07-3 ... ncies.html http://www.bloomberg.com/news/2014-07-3 ... cline.html Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage