Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

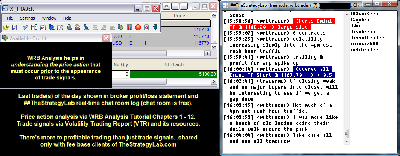

Attachment:

062414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5190.00.png [ 174.56 KiB | Viewed 310 times ]

062414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5190.00.png [ 174.56 KiB | Viewed 310 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$5,190.00 dollars or +51.90 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $5,190.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=131&t=1823 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=240&t=2365 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

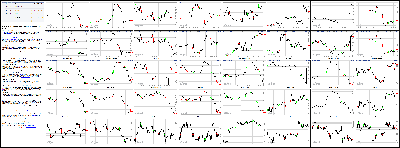

Ouch. Dow Sinks Over 100 Points Attachment:

062414-Key-Price-Action-Markets.png [ 937.22 KiB | Viewed 348 times ]

062414-Key-Price-Action-Markets.png [ 937.22 KiB | Viewed 348 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

So much for another record-setting day. The stock market's early gains evaporated like Italy's chances in the World Cup.

The Dow Jones industrial average ended the day down 119 points (0.7%). It was the biggest one-day percentage drop for the Dow in over a month. There was hope that the Dow would cross 17,000 for the first time this week. It's now down at 16,818. The S&P 500 and the Nasdaq both fell as well.

The reversal came as Italy suffered a biting defeat to Uruguay in the World Cup, ending the Italian team's hopes of advancing in the global soccer tournament.

Economic news not good enough? A key measure of consumer sentiment rose to the highest level since January 2008. The Conference Board's index of consumer confidence increased to 85.2 in May from 82.2 in April, suggesting that Americans remain optimistic about the economy. But it wasn't enough to lift stocks.

Home prices nationwide continued to rise in April. The S&P/Case-Shiller index measuring the value of residential real estate in 20 U.S. cities increased 1.1%. Separately, the government said sales of new homes rose more than 18% in May from April.

"The new home sales data and consumer confidence were very, very strong," said Randy Frederick, a managing director at the Schwab Center for Financial Research. "The market is not rallying in a big way, but given the run we've had that's not surprising."

Related: Will the Dow crack 17,000 this week?Stocks to watch -- Buffalo Wild Wings, Carnival, Walgreens: The World Cup has been good for business at Buffalo Wild Wings (BWLD), according to one analyst. Shares of the sports-themed restaurant chain jumped 6% Monday after an analyst at Wunderlich Securities increased his price target for shares after seeing all the standing room only crowds for at "B-dubs" at recent games. But the stock fell 2.4% Tuesday as the enthusiasm waned.

Carnival Corp (CCL)reported quarterly results that topped expectations, but the company's forecasts for the rest of the year weren't as rosy. The stock dropped 3%. The cruise line operator blamed fuel prices and currency exchange rates, which it said will reduce earnings full-year by 6 cents per share.

Walgreens (WAG) said earnings rose nearly 16% in the first quarter, but the results missed analysts' expectations. Shares fell more than 1%.

You might not have heard of Vertex Pharmaceuticals (VRTX), but it's worth looking up today. Shares soared 40% after the company said a study of its cystic fibrosis drug produced positive results.

Groupon (GRPN) was another company that managed to avoid the discount slashing today. Shares were up 4.5% on an upbeat analyst report.

Dubai enters bear market. Stocks in Dubai have been battered by concerns about the growing turmoil in Iraq, where insurgents have been gaining ground in the oil-rich nation. Shares of Arabtec --a major construction company responsible for building the Burj Khalifa -- have also been sinking, adding more concern about the Dubai market.

The Dubai DFM General index plunged more than 6% overnight. It was the worst one-day drop since October 2008, according to a note from analysts at ETX Capital. The index is down more than 22% so far this month, putting the Persian Gulf Emirate in a bear market.

"There is a possibility that traders are liquidating positions as a result of the current situation in Iraq which has eaten at sentiment in the Emirate region," the analysts wrote.

Abe lets another arrow fly in Japan: Japan's government has released details on the third and final phase of Prime Minister Shinzo Abe's ambitious plan to jolt the country's economy out of stagnation. Companies may pay less tax as a result, but the response in the stock market was muted. The Nikkei ended flat.

European markets ended mixed.

The ruble and Moscow stock index were stronger, continuing their recovery from sharp losses earlier this year as fears about an escalation of the crisis in Ukraine fade. A ceasefire between government forces and pro-Russian separatists declared last Friday appears to be holding. Sentiment was also improving after Abbott Laboratories (ABT) said Monday it would buy Russian pharmaceutical company Veropharm for as much as $495 million, underlining the waning threat of sanctions.

4:15 pm: [BRIEFING.COM] The stock market ended the Tuesday session on a lower note despite seeing early strength. The Dow Jones Industrial Average and S&P 500 posted respective losses of 0.7% and 0.6%, while the Nasdaq Composite shed 0.4%.

Equity indices displayed modest losses at the start, but were quick to regain their flat lines after a pair of economic data points surprised to the upside. Briefly, the New Home Sales report for May came in well ahead of estimates (504K versus Briefing.com consensus 440K), while the Consumer Confidence report (85.2) registered its highest reading since early 2008.

The economic news gave a boost to the consumer discretionary sector (-0.2%) and especially homebuilders. DR Horton (DHI 23.89, +0.29) and Toll Brothers (TOL 36.56, +0.43) both jumped 1.2%, while the iShares Dow Jones US Home Construction ETF (ITB 24.36, +0.21) advanced 0.9%. For its part, the discretionary sector fell into the red during the afternoon when the overall market reversed and surrendered its gain.

Before looking at the afternoon reversal, we'd like to point out that the discretionary space was just one of three influential sectors that slumped into the close.

The largest S&P 500 sector-technology (-0.5%)-saw intraday strength that was fueled by gains among chipmakers after Micron (MU 32.50, +1.24) reported better than expected earnings. The stock settled higher by 4.0%, while the PHLX Semiconductor Index lost 0.7% after being up as much as 0.7%.

Elsewhere, the health care sector (unch) surged out of the gate in reaction to positive cystic fibrosis treatment trial data from Vertex Pharmaceuticals (VRTX 93.53, +26.92). VRTX surged 40.4%, while the iShares Nasdaq Biotechnology ETF (IBB 255.48, +2.57) narrowed its gain to 1.0% after being up more than 2.0% intraday.

The intraday gains among three of the four largest sectors were not enough to prevent the key indices from tumbling into the red. The afternoon turnaround occurred shortly after the Wall Street Journal reported that a Syrian fighter jet struck targets in western Iraq, killing 50 people. The news was followed by broad-based selling activity that saw the energy sector (-2.0%) lead to the downside.

In all likelihood, the noteworthy dive was a function of profit taking, considering the sector trimmed its quarter-to-date gain to 10.6%. For comparison, no other sector shows an increase of more than 4.9% for the second quarter.

Meanwhile, the second-best sector of the second quarter-utilities-ended in the lead, climbing 0.3%.

Treasuries settled on their highs after spending the entire session in positive territory. The benchmark 10-yr yield fell five basis points to 2.58%.

Participation remained light with 635 million shares changing hands at the NYSE floor.

Economic data featured the April Case-Shiller 20-city Index, April FHFA Housing Price Index, New Home Sales for May, and the June Consumer Confidence report:

The Case-Shiller 20-city Home Price Index for April rose 10.8%, while an 11.6% increase had been expected by the Briefing.com consensus. This followed the previous month's increase of 12.4%.

The April Housing Price Index from the FHFA was unchanged, which followed an unrevised uptick of 0.7% observed during the prior month.

New home sales increased 18.6% in May to 504,000 from a downwardly revised 425,000 (from 433,000). The Briefing.com consensus expected new home sales to increase to 440,000.

Sales topped 500,000 for the first time since May 2008.

The spike in new home sales coincided with a large decline in mortgage rates. As rates turn higher, it could dent future sales growth.

The Conference Board's Consumer Confidence Index increased to 85.2 in June from a downwardly revised 82.2 (from 83.0). The Briefing.com consensus expected the index to increase to 84.0.

The index climbed to its highest point since the recession began in January 2008.

A surging stock market and general improvements in overall employment conditions were enough to offset higher gasoline/oil prices and drive consumer confidence to a 6-year high.

Tomorrow, the weekly MBA Mortgage Index will be reported at 7:00 ET, while Durable Orders for May (Briefing.com consensus 0.4%) and the third estimate of Q1 GDP (consensus -1.8%) will cross the wires at 8:30 ET.

S&P 500 +5.5% YTD

Nasdaq Composite +4.2% YTD

Dow Jones Industrial Average +1.5% YTD

Russell 2000 +0.8% YTD

3:30 pm: [BRIEFING.COM]

Aug gold touched a session low of $1317.20 per ounce in late morning pit trade after retreating from a session high of $1323.70 per ounce. The yellow metal eventually settled with a 0.2% gain at $1321.20 per ounce.

July silver traded in a tight range between $20.93 per ounce and $21.07 per ounce today and closed at $21.05 per ounce, or 0.6% higher.

Aug crude oil extended yesterday's losses despite trading in positive territory in morning action.

The energy component touched a session high of $106.51 per barrel but dipped to a session low of $105.68 per barrel in afternoon floor trade and settled with a 0.2% loss at $106.01 per barrel.

July natural gas trended higher today. It lifted from its session low of $4.47 per MMBtu and rose as high as $4.56 per MMBtu before settling with a 1.8% gain at $4.53 per MMBtu.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.3% with one hour remaining in the session. The benchmark index had several reasons to rally today (positive trial data in biotech space, strong new home sales numbers, and strong earnings from a key chipmaker), but could only put together a modest rally in the morning before surrendering all of its intraday gains and dipping into the red.

Stocks slumped from their highs amid headlines indicating a Syrian warplane struck targets in Iraq, but it is worth pointing out that the S&P 500 notched its session high roughly two hours ahead of those reports.

Interestingly, the energy sector, which has lagged throughout the session, accelerated its retreat during the afternoon. The growth-sensitive group enters the final hour with a loss of 1.6%, narrowing its quarter-to-date gain to 11.0%.

2:30 pm: [BRIEFING.COM] Stocks continue holding near their recent levels with the S&P 500 (-0.2%) trading less than four points below its flat line. Similarly, the Dow (-0.4%) and Russell 2000 (-0.4%) also hover in the red, while the tech-heavy Nasdaq (+0.3%) continues showing relative strength.

The Nasdaq has been able to stay ahead of the S&P 500 thanks to daylong strength in the biotech space. The iShares Nasdaq Biotechnology ETF (IBB 257.03, +4.12) has slipped from its high, but continues holding a solid gain of 1.6%.

Also of note, the technology sector (+0.2%) and the PHLX Semiconductor Index (+0.2%) have both retreated from their highs, but remain modestly positive.

1:55 pm: [BRIEFING.COM] The S&P 500 (-0.2%) has been trying to put together a rebound during the past 30 minutes, but the index has yet to reclaim its flat line.

Following the recent retreat, only four sectors remain in the green, while the other six groups hold losses between 0.2% and 1.0%. The consumer staples sector (-0.2%) holds the slimmest loss, but the decline has been large enough to erase its gain from yesterday.

Elsewhere, the energy sector (-1.1%) is the weakest performer, which has been the case throughout the session. The sector is the only group that shows a loss larger than 0.6% and today's decline has trimmed its quarter-to-date gain to 11.6%.

1:30 pm: [BRIEFING.COM] Selling efforts have picked up in the past 30 minutes. The catalyst for the slide is unclear, although reports of a Syrian warplane striking Iraq and killing 50 people have made the rounds as the potential culprit.

Geopolitical developments have acted as the spoiler before. If nothing else, in a thinly-traded market like this, worrisome headlines on the geopolitical front can be enough to keep the market from running away to the upside and encourage some profit-taking activity after a big run during the quarter.

There hasn't been a rush to the exits, however, nor has there been a spike in oil prices after the aforementioned headline. The Treasury market, though, has seen a little pop despite an average 2-yr note auction that drew a high yield of 0.511% on a light indirect bid (23.2%) that trailed the prior 12-auction average of 27.4%. Similarly, the 3.23 bid-to-cover ratio was below the prior 12-auction average of 3.34.

The 10-yr note is up 12 ticks with its yield at 2.587%.

12:55 pm: [BRIEFING.COM] At midday, the Dow Jones Industrial Average (unch) and S&P 500 (+0.1%) hover near their flat lines, while the Nasdaq Composite (+0.6%) and Russell 2000 (+0.4%) outperform.

Equity indices started the session in the red, but jumped back into the green following today's better than expected New Home Sales report for May (504K versus Briefing.com consensus 440K). The strong data, coupled with the highest consumer confidence reading since early 2008, helped most cyclical sectors climb off their lows.

The economic data underpinned homebuilders, which in turn has sent the consumer discretionary sector (+0.6%) to the top of today's leaderboard. DR Horton (DHI 24.24, +0.64) and Toll Brothers (TOL 37.16, +1.03) hold respective gains of 2.7% and 2.9%, while the broader iShares Dow Jones US Home Construction ETF (ITB 24.63, +0.48) trades up 2.0%.

Similar to the discretionary sector, other top-weighted groups like technology (+0.5%) and health care (+0.6%) display relative strength, while financials (unch) lag.

The tech sector owes its outperformance to chipmakers following better than expected earnings from Micron (MU 32.75, +1.49). The stock has jumped 4.8%, while the PHLX Semiconductor Index is higher by 0.6%. Furthermore, the gains among microchip names have also played a part in the outperformance of the Nasdaq Composite.

Chipmakers notwithstanding, the Nasdaq has also drawn considerable strength from biotech names. Vertex Pharmaceuticals (93.52, +26.93) has soared 40.5% after announcing its cystic fibrosis treatment met the primary endpoints in Phase 3 trials. The big gain has contributed to the 2.1% advance in the iShares Nasdaq Biotechnology ETF (IBB 258.32, +5.41) and the outperformance of the health care sector (+0.6%).

Interestingly, blue chip indices like the Dow and S&P 500 have not been able to keep up with their high-beta counterparts, which could be a reflection of some profit taking ahead of the end of the second quarter. Including today's gain, the S&P 500 has added 5.0% during the quarter versus an increase of 1.5% for the Russell 2000.

On the fixed income side, Treasuries rallied overnight, but have since slipped from their highs. The 10-yr yield is lower by two basis points at 2.61%.

Economic data featured the April Case-Shiller 20-city Index, April FHFA Housing Price Index, New Home Sales for May, and the June Consumer Confidence report:

The Case-Shiller 20-city Home Price Index for April rose 10.8%, while an 11.6% increase had been expected by the Briefing.com consensus. This followed the previous month's increase of 12.4%.

The April Housing Price Index from the FHFA was unchanged, which followed an unrevised uptick of 0.7% observed during the prior month.

New home sales increased 18.6% in May to 504,000 from a downwardly revised 425,000 (from 433,000). The Briefing.com consensus expected new home sales to increase to 440,000.

Sales topped 500,000 for the first time since May 2008.

The spike in new home sales coincided with a large decline in mortgage rates. As rates turn higher, it could dent future sales growth.

The Conference Board's Consumer Confidence Index increased to 85.2 in June from a downwardly revised 82.2 (from 83.0). The Briefing.com consensus expected the index to increase to 84.0.

The index climbed to its highest point since the recession began in January 2008.

A surging stock market and general improvements in overall employment conditions were enough to offset higher gasoline/oil prices and drive consumer confidence to a 6-year high.

12:30 pm: [BRIEFING.COM] The S&P 500 (+0.2%) has not moved too far away from its session high, while the Dow Jones Industrial Average (+0.1%) has been quietly slipping from its best level of the day.

At this juncture, 12 of 30 Dow components hover in the red, but their losses have been held in check. JPMorgan Chase (JPM 57.86, -0.33), Microsoft (MSFT 41.81, -0.18), and Verizon (VZ 49.48, -0.25) represent the three weakest index members with losses close to 0.5% apiece.

On the upside, Intel (INTC 30.75, +0.52) trades higher by 1.7%, drawing strength from the PHLX Semiconductor Index (+0.6%).

12:00 pm: [BRIEFING.COM] Equity indices remain near their highs with the S&P 500 up 0.2%. The benchmark index trades just four points above its flat line, but it is worth mentioning that seven of ten sectors trade in the green.

Health care (+0.5%) led the market higher out of the gate, but the third-largest sector has stepped back from its best level of the day, leaving consumer discretionary (+0.6%) and technology (+0.5%) as the top two sectors.

The discretionary space has received a big boost from homebuilders following today's better than expected New Home Sales report for May (504K versus Briefing.com consensus 440K). DR Horton (DHI 24.39, +0.79) is higher by 3.3%, while the broader iShares Dow Jones US Home Construction ETF (ITB 24.65, +0.50) trades up 2.1%.

Elsewhere, the tech sector remains supported by chipmakers with the PHLX Semiconductor Index trading higher by 0.6%.

11:25 am: [BRIEFING.COM] After rallying through the first hour of the session, the major averages have spent the past 60 minutes near their best levels of the day.

A bit of a divergence has been spotted in the market as indices that contain a large portion of high-growth names (Russell 2000, Nasdaq Composite, S&P Mid Cap 400) trade ahead of their peers that are comprised of large-cap stocks (Dow Jones Industrial Average, S&P 500). On that note, the Dow Jones Industrial Average (+0.1%) and S&P 500 (+0.2%) hover just above their flat lines, while the Nasdaq Composite (+0.7%) and Russell 2000 (+0.6%) outperform.

With stocks on highs, participants are not showing increased demand for volatility protection as evidenced by a slight downtick in the CBOE Volatility Index (VIX 10.94, -0.04).

10:55 am: [BRIEFING.COM] The major averages hover at their best levels of the session after erasing their early losses. The Nasdaq, which has outperformed from the start, remains in the lead with a gain of 0.7%.

The tech-heavy index has climbed to new highs thanks to continued strength within the biotech space. The iShares Nasdaq Biotechnology ETF (IBB 259.35, +6.44) is now higher by 2.6%, while the health care sector trades ahead of the remaining groups (+0.8%).

Furthermore, the Nasdaq has also drawn strength from chipmakers following above-consensus earnings from Micron (MU 32.66, +1.42). The stock trades up 4.5%, while the broader PHLX Semiconductor Index is higher by 0.6%. For its part, the technology sector trades ahead of the remaining cyclical sectors (+0.5%).

The rally off the opening lows has lured some money out of the bond market as Treasuries hover near their lows with the 10-yr yield down two basis points at 2.61%.

10:30 am: [BRIEFING.COM]

The dollar index just rallied in recent trade to a new HoD and is now +0.1% at 80.37

This hit precious metals, but only modestly. The same goes for crude and copper.

Aug gold is now +0.2% at $1321.50/oz, July silver is +0.6% at $21.03/oz

Overnight, WTI crude oil and Brent crude oil extended yesterday's losses as Iraq supply fears eased

But, in more recent trade, crude has come back a little and is back near the unchanged line.

July crude is now +0.1% at $106.31/barrel, Brent crude is +0.4% at $114.45/barrel

Natural gas has been rallying this morning and just hit a new HoD of $4.51/MMBtu. July nat gas is currently +1.4% a $4.51/MMBtu

July copper is currently +0.1% at $3.15/lb

10:00 am: [BRIEFING.COM] The S&P 500 trades lower by 0.1%.

New home sales in May hit an annualized rate of 504,000, which was up from the revised April rate of 425,000 (from 433,000), and better than the rate of 440,000 that had been broadly expected by the Briefing.com consensus.

Separately, the consumer confidence reading for June came in at 85.2. Economists polled by Briefing.com expected the survey to come in at 84.0. This followed the prior month's unrevised reading of 83.0.

9:40 am: [BRIEFING.COM] The major averages began the session in the red, but the early strength in biotechnology has helped the Nasdaq (+0.1%) erase its opening loss.

The iShares Nasdaq Biotechnology ETF (IBB 258.21, +5.30) trades up 2.1% thanks to a 47.3% surge in the shares of Vertex Pharmaceuticals (VRTX 98.11, +31.50) after the company's cystic fibrosis treatment met its primary endpoints. The big gain has also given a boost to the health care sector, which trades higher by 0.3%.

Similar to health care, utilities (+0.1%) and telecom services (+0.1%) also hover in the green, while consumer staples (-0.6%) lag.

Meanwhile, the six cyclical sectors trade broadly lower, but their losses have been contained to no more than 0.3% so far.

New Home Sales for May (consensus 440K) and the June Consumer Confidence report (consensus 84.0) will cross the wires at 10:00 ET.

9:11 am: [BRIEFING.COM] S&P futures vs fair value: -3.90. Nasdaq futures vs fair value: -0.50. The stock market is on track for a lower start as futures on the S&P 500 trade four points below fair value. Index futures have been trading in the red since late last night, but they have been able to erase more than half of their losses.

Nasdaq futures, meanwhile, have returned to their flat line thanks to a boost from Vertex Pharmaceuticals (VRTX 99.31, +32.70), which is indicated to surge 49.1% at the open following positive trial data. The biotech stock is likely to underpin the rest of the industry group as the iShares Nasdaq Biotechnology ETF (IBB 257.75, +4.84) holds a pre-market gain of 1.9%.

Elsewhere among high-beta names, Micron (MU 31.61, +0.35) is indicated to open with a 1.0% gain following its better than expected earnings.

Despite the rebound in equity futures, Treasuries continue holding gains with the 10-yr yield down three basis points at 2.60%.

9:03 am: [BRIEFING.COM] S&P futures vs fair value: -3.60. Nasdaq futures vs fair value: -0.80. The S&P 500 futures trade four points below fair value.

The Case-Shiller 20-city Home Price Index for April rose 10.8% while an 11.6% increase had been expected by the Briefing.com consensus. This follows the previous month's increase of 12.4%.

Separately, the April Housing Price Index from the FHFA was unchanged, which followed an unrevised uptick of 0.7% observed during the prior month.

8:28 am: [BRIEFING.COM] S&P futures vs fair value: -3.20. Nasdaq futures vs fair value: -0.50. The S&P 500 futures trade three points below fair value.

Asian markets finished the Tuesday session on a higher note. Japan's Prime Minister Shinzo Abe unveiled a plan to lower the corporate tax rate to below 30% in the coming years and pledged to reform the Government Pension Investment Fund.

Japan's Nikkei added 0.1%, holding at five-month highs. Automakers were broadly lower with Honda Motor and Nissan Motor falling 1.4% and 1.0%, respectively.

Hong Kong's Hang Seng rose 0.3%, bouncing off the 50- and 200-day moving averages. Utility Power Assets Holdings was the top performer, adding 1.9%.

China's Shanghai Composite advanced 0.5%, posting its second gain in three days. Liquor-related names outperformed as Kweichow Moutai climbed 4.6% and Sichuan Swellfun Co climbed the daily limit, 10%.

Major European indices trade in mixed fashion with Italy's MIB (-0.3%) showing relative weakness for the second day in a row. Bank of England Governor Mark Carney testified before the Treasury Select Committee, reiterating that the first rate hike will be data-dependent and gradual. Mr. Carney also pointed to recent wage data, saying it was softer than expected

In economic data:

Great Britain's BBA Mortgage Approvals came in at 41,800 (expected 41,300, previous 41,900)

Germany's Ifo Business Climate Index slipped to 109.7 from 110.4 (expected 110.2) as Business Expectations ticked down to 104.8 from 106.2 (consensus 105.9) and Current Assessment held steady at 114.8 (expected 115.0)

Italy's Wage Inflation rose 0.1% month-over-month (expected 0.0%, previous 0.0%) and the non-EU trade surplus expanded to EUR2.45 billion from EUR1.65 billion

Swiss trade surplus expanded to CHF2.77 billion from CHF2.45 billion (expected surplus of CHF2.71 billion)

------

In France, the CAC is higher by 0.2% with utilities and industrials in the lead. GDF Suez and Schneider Electric hold respective gains of 1.5% and 0.8%. Financials lag with AXA, Credit Agricole, and Societe Generale down between 0.4% and 1.0%.

Germany's DAX holds a loss of 0.1%. Bank shares are also showing relative weakness as Commerzbank and Muenchener Re trade lower by 1.1% and 0.6%, respectively.

Great Britain's FTSE is lower by 0.1%. Sports Direct International is the weakest performer, down 4.0%. Homebuilder Barratt Developments underperforms for the second day in a row with a loss of 1.6%.

Italy's MIB trades down 0.3% amid weakness in financials. BMPS has tumbled 7.6% as the bank sells shares to improve its capital position. Unicredit and Intesa Sanpaolo also underperform with respective losses of 1.7% and 1.4%.

7:57 am: [BRIEFING.COM] S&P futures vs fair value: -4.70. Nasdaq futures vs fair value: -3.30. U.S. equity futures hold modest losses amid cautious action overseas. The S&P 500 futures hover five points below fair value.

Reviewing overnight developments:

Asian markets ended higher. Japan's Nikkei +0.1%, Hong Kong's Hang Seng +0.3%, and China's Shanghai Composite +0.5%.

There was no economic data of note

In news:

Yin Jianfeng, who conducts research for China Academy of Social Sciences said the country's central bank should cut the reserve requirement ratio on time deposits.

Major European indices trade in mixed fashion. France's CAC +0.1%, Great Britain's FTSE -0.1%, and Germany's DAX is flat. Elsewhere, Italy's MIB -0.3% and Spain's IBEX -0.1%.

In economic data:

Great Britain's BBA Mortgage Approvals came in at 41,800 (expected 41,300, previous 41,900)

Germany's Ifo Business Climate Index slipped to 109.7 from 110.4 (expected 110.2) as Business Expectations ticked down to 104.8 from 106.2 (consensus 105.9) and Current Assessment held steady at 114.8 (expected 115.0)

Italy's Wage Inflation rose 0.1% month-over-month (expected 0.0%, previous 0.0%) and the non-EU trade surplus expanded to EUR2.45 billion from EUR1.65 billion

Swiss trade surplus expanded to CHF2.77 billion from CHF2.45 billion (expected surplus of CHF2.71 billion)

Among news of note:

Bank of England Governor Mark Carney testified before the Treasury Select Committee, reiterating that the first rate hike will be data-dependent and gradual. Mr. Carney also pointed to recent wage data, saying it was softer than expected

In U.S. corporate news:

Micron (MU 31.89, +0.63): +2.0% after beating earnings and revenue estimates.

Vertex Pharmaceuticals (VRTX 100.01, +33.39): +50.1% after the company announced positive trial results.

Walgreen (WAG 72.35, -1.38): -1.9% following its bottom-line miss.

The April Case-Shiller 20-city Index (Briefing.com consensus 11.6%) and FHFA Housing Price Index will both be released at 9:00 ET, while New Home Sales for May (consensus 440K) and June Consumer Confidence (consensus 84.0) will cross the wires at 10:00 ET.

6:34 am: [BRIEFING.COM] S&P futures vs fair value: -5.50. Nasdaq futures vs fair value: -9.50.

6:34 am: [BRIEFING.COM] Nikkei...15376.24...+7.00...+0.10%. Hang Seng...22880.64...+75.80...+0.30%.

6:34 am: [BRIEFING.COM] FTSE...6781.15...-19.40...-0.30%. DAX...9920.67...+0.20...0.00.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage