Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

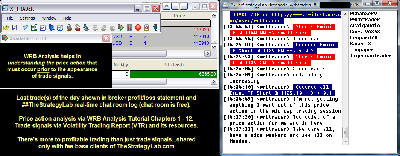

Attachment:

012414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6365.00.png [ 175.66 KiB | Viewed 334 times ]

012414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6365.00.png [ 175.66 KiB | Viewed 334 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,490.00 dollars or +14.90 points, Emini ES ($ES_F) futures @

$4,875.00 dollars or +97.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6,365.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1705 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

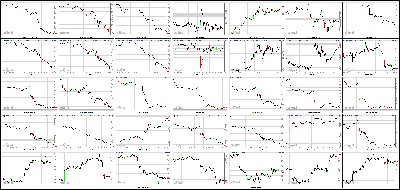

Dow Suffers Worst Week Since 2011 Attachment:

012414-Key-Price-Action-Markets.png [ 511.85 KiB | Viewed 315 times ]

012414-Key-Price-Action-Markets.png [ 511.85 KiB | Viewed 315 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Good riddance to this week. It was another ugly day on Wall Street -- and for markets around the globe.

The Dow dropped nearly 320 points Friday, or almost 2%. The S&P 500 and Nasdaq fell more than 2%. CNNMoney's Tech 30 index also fell about 2%, despite a jump in shares of Microsoft (MSFT, Fortune 500) following strong quarterly sales and earnings.

The losses come at the end of the worst week for stocks in recent memory. The Dow tumbled more than 3.5%, its work week since November 2011. The S&P 500 slid more than 2.6%, logging its biggest weekly decline since May 2012.

Meanwhile, the Nasdaq tumbled almost 1.7%, its first weekly decline of the year and the worst since August.

All three indexes are now in negative territory for the year. The selling has some investors bracing for a correction, usually defined as a decline of 10% or more.

"$SPY If market doesn't bounce here, I imagine this will end up being a full 10% correction," said StockTwits trader kgpittm.

StockTwits user Fundraising pointed out that he'd prefer a correction sooner rather than later so that stocks can resume their upward trend.

"$SPY with how much correction talk out there I would rather have it now so it has more legs to run later Bullish," he said.

Investors dump stocks around the world: Concerns about an economic slowdown in China pressured markets around the globe.

Asian markets ended mixed after the HSBC survey showed that Chinese manufacturing activity slowed in January for the first time in six months and as a high-yield investment product from China's largest bank faces imminent default.. The Shanghai Composite did wind up notching a 0.6% gain, but markets in Hong Kong and Tokyo both dropped more than 1%.

European markets closed sharply lower, with Germany's DAX and France's CAC 30 dropping more than 2% each. And emerging market currencies were also in sell-off mode.

* Video - Stocks down? It's about time! Argentina's peso has tumbled more 15% against the dollar over the past two days amid concerns over the country's foreign exchange reserves. Meanwhile, the Turkish lira fell to a record low for a ninth straight day against the dollar. The lira is down more than 8% this year. India's rupee also lost significant ground against the dollar.

As investors fled riskier assets like stocks and emerging market currencies, they moved into safe havens like gold and Treasuries. The yield on the benchmark 10-year Treasury fell to 2.73%, its lowest level since late November. (Bond yields and prices move in opposite directions.)

Earnings continue to disappoint: News from Corporate America wasn't helping either. After last year's big rally, investors are looking for signs the economy will be strong enough to keep the bull market going but so far, this earnings season has been decent, as opposed to spectacular.

102 S&P 500 companies have reported fourth-quarter results, with only 66 beating analysts' estimates, according to S&P Capital IQ. Of the remainder, 26 have missed, and 10 have met expectations.

* Keep track of CNNMoney's Tech 30 indexXerox (XRX, Fortune 500)shares took a dive after the copy machine company reported declines in quarterly revenue and profit.

Honeywell (HON, Fortune 500)shares were also down as the defense contractor reported a slip in quarterly sales.

Procter & Gamble (PG, Fortune 500) was one of the few bright spots in the market Friday. The stock rose nearly 2% after reporting quarterly profits that, while lower than a year ago, beat estimates.

Starbucks (SBUX, Fortune 500) shares were also rising after the coffee giant reported better-than-expected earnings.

Natural gas jumps to almost 4-year high: As frigid temperatures continued to bite across many parts of the country, natural gas prices soared almost 10% above $5 per million British Thermal Unit, crossing the milestone for the first time since the summer of 2010.

Many home across the country use natural gas as their man heating fuel.

The ongoing surge in prices was a hot topic among traders, with many touting the United States Natural Gas (UNG) commodity ETF.

"$UNG Burning through tomorrow's household fuel....TODAY!" quipped chumpville.

"Look at Nat Gas go! #trendfollowing is loving this #polarvortex weather! $UNG" said attaincapital.

But StockTwits trader LinvestResearch predicted there could be a pullback in prices soon and pointed to the VelocityShares 3x Inverse Natural Gas ETN (DGAZ), which goes down when natural gas prices go up. It plunged 17% Friday.

"There will be correction after these gaps," she said. "#Natgas has reached multi-year highs. Profit taken soon $UNG $DGAZ."

* Video - Stocks plunge in U.S., Dow sinks 318 points

* Video - Stocks plunge in U.S., Dow sinks 318 points4:20 pm: [BRIEFING.COM] Equities endured a rough end to the abbreviated week with the S&P 500 seeing its largest weekly loss since June 2012. The benchmark index fell 2.1%, extending its January decline to 3.1%.

The market spent the entire session in a steady slide amid continued concerns regarding China. Furthermore, participants kept a close eye on the foreign exchange market where emerging market currencies weakened while the Japanese yen saw its second consecutive day of gains. Dollar/yen fell below the 102.50 level after trading near 104.50 on Wednesday. The yen strength came about after Bank of Japan officials said the Japanese economy remains on track and there is no need for additional easing at this time. In turn, this posed a headwind to yen-based carry trades, which played a significant part in last year's market rally.

Like yesterday, the weakness began overnight; however, unlike yesterday, the aggressive selling did not start until the European session kicked off. Regional indices saw broad losses with peripheral markets leading the slide. Spain's IBEX plunged 3.6% while Italy's MIB fell 2.3%.

The overseas weakness set the tone for a lower start in U.S. equities with cyclical sectors leading the decline. Consumer discretionary (-1.9%) and technology (-2.1%) finished just ahead of the broader market thanks to the relative strength of Starbucks (SBUX 74.98, +1.59) and Microsoft (MSFT 36.80, +0.75) after both beat their bottom-line estimates.

Staying on the earnings theme, most of the reports received between yesterday's close and today's open were ahead of expectations but that mattered little to the broader market. However, Kansas City Southern's (KSU 99.49, -17.79) seven-cent miss mattered quite a bit as the stock plunged 15.2% while also weighing on the Dow Jones Transportation Average, which tumbled 4.1%. This marked the largest one-day loss for the bellwether complex since September 2011 as the broad liquidation resulted in 17 of 20 components posting losses in excess of 2.0%. Due to the sharp losses, the industrial sector (-3.1%) ended at the bottom of the leaderboard.

Elsewhere, financials (-2.3%) and materials (-2.7%) lagged while energy (-2.1%) ended in-line.

Meanwhile, defensive sectors-sans health care-outperformed with losses between 0.9% and 1.1%. Procter & Gamble (PG 79.18, +0.94) contributed to the relative strength of the consumer staples sector after reporting a one-cent beat. For its part, the health care sector lost 2.3%.

Treasuries booked gains with the 10-yr yield ending lower by five basis points at 2.73%.

The aggressive selling fueled strong demand for volatility protection as indicated by a 30.0% surge in the CBOE Volatility Index (VIX 17.89, +4.12), which ended at its highest level since October 15.

For the second day in a row, the selloff was accompanied by above-average volume as 902 million shares changed hands at the NYSE.

Monday's data will be limited to the December New Home Sales report, which will be released at 10:00 ET.

Nasdaq Composite -1.2% YTD

Russell 2000 -1.7% YTD

S&P 500 -3.1% YTD

Dow Jones Industrial Average -4.2% YTD

Week in Review: From Highs to Lows in Less Than a Week

On Monday, bond and equity markets were closed for Martin Luther King Jr. Day.

Tuesday saw the major averages begin the abbreviated week on a mixed note as the Nasdaq added 0.7% while the Dow Jones Industrial Average shed 0.3%. For its part, the S&P 500 rose 0.3% as eight of ten sectors finished in the green. Stocks began the day with solid gains but the early strength faded quickly when the S&P 500 was unable to extend above the 1850 level during the opening minutes. That rejection emboldened sellers, who promptly drove the indices to their lows. Adding insult to injury was the fact that mostly better-than-expected earnings reported ahead of the opening bell failed to entice buyers.

The market endured an uninspiring Wednesday session, which unfolded in similar fashion to Tuesday's affair. Once again, the major averages ended mixed with the Dow Jones Industrial Average (-0.3%) coming out on the losing end while the Nasdaq (+0.4%) and S&P 500 (+0.1%) eked out modest gains. The price-weighted Dow spent the entire session in the red as 19 of its 30 components registered losses. Most notably, the second-largest index member, IBM (IBM 179.64, -3.09), plunged 3.3% after beating its Capital IQ earnings estimate by 13 cents on below-consensus revenue. Despite the bottom-line beat, the report was scrutinized due to the company accounting for a lower tax rate than in previous quarters.

On Thursday, the S&P 500 snapped its modest two-day win streak with its second-largest decline of the month. The index lost 0.9% as nine of ten sectors registered losses. Although stocks sold off throughout the day, the weakness actually started during the overnight futures session when three China-related developments began fueling the risk-off sentiment:

The HSBC flash PMI reading for January was below expectations at 49.6. The sub-50 reading is indicative of manufacturing activity contracting; and the January reading marked a six-month low for the series.

A Financial Times report indicated Chinese authorities are working to prevent a default of a $500 million high-yield investment trust, failure of which could trigger an unnerving fallout in China's shadow banking system.

An SEC administrative law judge issued a ruling that censures the accounting arms of the "Big Four" in China for six months due to their unwillingness to turn over requested documents involving US-listed Chinese companies under investigation for accounting fraud.

The three developments did enough damage to sentiment that a slate of mostly better-than-expected earnings could not halt the day-long slide. The discretionary sector (-0.7%) finished just ahead of the broader market after last year's top S&P 500 component, Netflix (NFLX 386.08, -2.64), surged 16.5% in reaction to its bottom-line beat and above-consensus guidance.

3:35 pm: [BRIEFING.COM] Natural gas futures rose above $5/MMBtu today, soaring over 10%. This was the first time the front-month contract rose above $5/MMBtu since Nov 2011 and the first time the continuous nat gas futures contract rose above $5/MMBtu since June 2010.

Feb natural gas ended the day 9.8% higher as $5.03/MMBtu. Crude oil futures sold off overnight, falling below $97/barrel level. Mar crude ended $0.55 lower at $96.70/barrel.

Metals ended the day mixed with Feb gold rising $1.90 to $1264.50/oz and Mar silver losing $0.25 to $19.76/oz.

3:05 pm: [BRIEFING.COM] The S&P 500 trades less than one point above its session low with one hour remaining in the trading day. This week was not very busy with economic data, but that is expected to change next week. Monday's economic data will be limited to the December New Home Sales report (Briefing.com consensus 457,000), but Wednesday will bring the latest policy statement from the Federal Reserve.

On Thursday, the advance reading of fourth quarter GDP (consensus 3.0%) will be released at 8:30 ET while Friday will bring the January Chicago PMI (58.0 expected) and the final reading of the Michigan Consumer Sentiment Survey for January (80.4 forecast).

2:35 pm: [BRIEFING.COM] Equity indices have dropped to fresh lows as dip-buyers remain unwilling to step in after two days of broad-based losses. Finding pockets of relative strength has been difficult today considering declining issues at the NYSE outpace advancers by a 6.7:1 margin. Things are not looking any better at the Nasdaq where there are 6.9 decliners for each listing trading higher.

The recent slide to new session lows has sent the CBOE Volatility Index (VIX 17.06, +3.29) past the 17.00% level for the first time since October 16.

2:00 pm: [BRIEFING.COM] Not much has changed since our last update as the major averages continue to linger near their lows. Similarly, sector standing has not changed much as four of six growth-sensitive groups continue to lag while consumer discretionary (-1.2%) and technology (-1.3%) trade just ahead of the broader market thanks to better-than-expected earnings from Microsoft (MSFT 37.10, +1.05) and Starbucks (SBUX 75.57, +2.18).

The fourth-quarter earnings season will kick into high gear next week with Dow component Caterpillar (CAT 86.28, -2.20) set to release its results ahead of Monday's opening bell. Following Monday's session, Apple (AAPL 549.48, -6.70), Seagate (STX 58.92, -1.82), STMicroelectronics (STM 7.69, -0.18), and U.S. Steel (X 25.50, -0.84) will be in focus.

1:30 pm: [BRIEFING.COM] Elements of risk aversion are readily apparent today with buyers few and far between. The major stock indices are down big across the board, Treasuries are up, gold prices are firm, and the CBOE Volatility Index (VIX 16.16, +2.39) has surged 17%.

Every sector is down at the moment, but relative strength leaders include the consumer staples (unch), telecom services (-0.1%), and utilities (-0.1%) sectors, which are known for their defensive orientation.

The move in Treasuries has been particularly noteworthy. The yield on the benchmark 10-yr note has dropped 9 basis points this week to 2.74%. This move precedes next week's FOMC meeting. There is some chatter today that the strength in Treasuries isn't just a safety trade, but a trade rooted in a budding sense that the distress in emerging market currencies could spur the FOMC to hold off on a second tapering announcement.

1:00 pm: [BRIEFING.COM] At midday, equity indices hover near their lows as the stock market sees an extension of yesterday's selling amid continued China-related worries. In addition, weakness in emerging markets and their currencies has increased fears of a potential currency crisis while continued yen strength has posed a headwind to carry trades, which supported much of last year's rally in global equities.

Similar to yesterday, the weakness began overnight, but unlike yesterday, the aggressive selling did not start until the European session kicked off. Regional markets endured a forgettable session as Germany's DAX tumbled 2.5% and Spain's IBEX plunged 3.6%.

This set the tone for a lower start in U.S. equities with growth-sensitive sectors leading the decline. At this juncture, only consumer discretionary (-1.2%) and technology (-1.1%) trade ahead of the S&P 500 (-1.3%) while the remaining four groups hold losses between 1.5% (energy) and 2.4% (industrials).

The tech sector has drawn strength from Microsoft (MSFT 37.09, +1.04) while the discretionary space owes its slight outperformance to Starbucks (SBUX 75.80, +2.41). The two names hold respective gains of 2.8% and 3.2% after both beat their bottom-line estimates.

Elsewhere among cyclical sectors, the industrial space is seeing considerable losses among transports after Kansas City Southern (KSU 101.53, -15.75) missed earnings estimates by seven cents. The stock trades lower by 13.5% while the Dow Jones Transportation Average holds a loss of 3.1%. It should be noted, the bellwether complex is now red for the year (-0.9%) after ending yesterday's session at a fresh all-time high.

On the countercyclical side, health care (-1.5%) trails the broader market while consumer staples (-0.2%), telecom services (-0.1%), and utilities (-0.2%) trade little changed.

Today's selling has stirred up some serious interest in volatility protection, sending the CBOE Volatility Index (VIX 16.16, +2.39) to its highest level since mid-October.

Treasuries hold solid gains with the benchmark 10-yr yield down four basis points at 2.74%.

12:35 pm: [BRIEFING.COM] Recent action saw the S&P 500 continue inching off its session low in the 1800 area; however, the index still has ways to go before putting a notable dent in today's loss.

Growth-sensitive sectors led the early weakness and four of six cyclical groups continue to lag at this juncture; however, the consumer discretionary sector (-1.1%) has joined technology (-1.0%) among the outperformers.

The tech sector owes its outperformance to Microsoft (MSFT 37.09, +1.04) while the discretionary space is drawing strength from Starbucks (SBUX 75.80, +2.41). The two issues hold respective gains of 2.9% and 3.3% after both beat their bottom-line estimates.

12:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 1.3% after making a brief appearance below the 1800 level. Even though the index remains sharply lower, a handful of sectors-consumer discretionary (-1.2%), energy (-1.6%), financials (-1.4%), have ticked up off their lows.

It remains to be seen whether the upticks represent the start of a rebound or if the sectors are simply retracing a small portion of their losses before heading lower once again. From a broader standpoint, the S&P 500, which hovers near 1807, will face the next resistance level around 1810.

11:35 am: [BRIEFING.COM] Equity indices remain pinned to their lows with small caps continuing their underperformance. The Russell 2000 has extended its loss to 2.5%, which marks the largest one-day drop for the index since mid-June.

Elsewhere, the Dow Jones Transportation Average (-3.3%) finds itself in the midst of its biggest one-day decline since mid-April as broad-based weakness pressures the bellwether complex. 15 of 20 components hold losses of 2.0% or more while Kansas City Southern (KSU 101.81, -15.47) trades down 13.2% following its bottom-line miss.

Also of note, demand for volatility protection remains alive and well with the CBOE Volatility Index (VIX 16.83, +3.06) hovering at its best level in more than three months.

10:55 am: [BRIEFING.COM] The major averages have dropped to fresh lows with the Russell 2000 leading the weakness (-1.9%). As a result, all of the key indices are now red for the year. The small-cap index now holds a month-to-date loss of 1.0%.

As mentioned earlier, three of four defensive sectors-consumer staples, telecom services, and utilities-remain in positive territory while health care trails the S&P 500 with a loss of 1.3%. However, things are not as upbeat on the cyclical side where the technology sector (-0.9%) is the lone outperformer. Although most sector components are on the defensive, Microsoft (MSFT 36.83, +0.77) trades higher by 2.1% following its ten-cent beat on a 14.3% year-over-year increase in revenue.

Elsewhere, the financial sector, which has displayed considerable weakness since yesterday, continues to lag with a loss of 1.4%.

10:35 am: [BRIEFING.COM] Natural gas futures are the big mover again today as frigid weather continues in parts of the U.S. Front-month (Feb) nat gas futures hit a high of $4.996/MMBtu. Fen nat gas is now +4.7% at $4.95/MMBtu.

The dollar index recovered off its LoD this morning and is now just above the unchanged line.

However, this didn't seem to affect precious metals earlier as gold and silver futures held gains and remained just below its highs for the day. Both precious metals have pulled a little below the HoD, but remain nicely in positive territory.

Feb gold is currently +0.4% at $1267.90/oz, Mar silver is +0.7% at $20.16/oz.

Crude oil futures sold off earlier this morning and is now back in the red. Mar crude is currently -0.3% at $97.07/barrel.

10:05 am: [BRIEFING.COM] Equity indices remain near their lows as the underperformance of the six cyclical groups continues to weigh. Meanwhile, three of four defensive sectors have climbed to fresh highs while health care (-0.6%) remains in the red.

We would also like to call attention to the foreign exchange market where the Japanese yen has been strengthening since yesterday. Given the Bank of Japan's policy course, yen strength is indicative of a risk-off sentiment among traders. Similarly, yen weakness tends to accompany equity strength, as it has during 2013. Dollar/yen trades below 102.50 after ending Wednesday's session at 104.57.

9:45 am: [BRIEFING.COM] The major averages began the day in the red with the Russell 2000 (-1.2%) pacing the early retreat. Meanwhile, the S&P 500 holds a loss of 0.8% as it hovers just one point above its 50-day moving average (1812).

Nine of ten sectors are seeing early pressure while telecom services (+0.6%) display a modest early gain. The remaining countercyclical groups, consumer staples, utilities, and health care, outperform with respective losses of 0.2%, 0.8%, and 0.1%.

On the cyclical side, the financial sector (-1.0%) is showing noteworthy weakness again, but it the industrial space (-1.7%) is the weakest sector at this juncture as transports lag after Kansas City Southern (KSU 98.05, -19.23) missed bottom-line estimates by seven cents. The stock has plunged 16.6% while the broader Dow Jones Transportation Average trades lower by 3.1%. Strikingly, the bellwether complex is now down 0.9% in January after ending yesterday's session at a fresh all-time high.

The early weakness has fueled a search for protection as the CBOE Volatility Index (VIX 15.25, +1.48) sits at its highest level in over a month.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: -11.00. Nasdaq futures vs fair value: -12.50. The major averages are on track for a sharply lower open for the second day in a row as the S&P 500 futures trade 11 points below fair value. Index futures held up well during the cautious Asian session, but the relative strength was short-lived as futures slid to lows in conjunction with the start of the European session. A bit of a rebound has taken place since then, but the S&P 500 futures have only reclaimed about three points.

With global equities on the defensive, participants have shown interest in gold and Treasuries. Gold futures trade higher by 0.4% at $1266.70 while the 10-yr note holds a nine-tick gain with its yield down four basis points at 2.75%.

Investors received another slate of mostly better-than-expected earnings, but today's reports have not generated a broad-market response. Notably, Microsoft (MSFT 37.31, +1.26) trades higher by 3.5% after reporting a ten-cent beat on a 14.3% year-over-year increase in revenue.

8:58 am: [BRIEFING.COM] S&P futures vs fair value: -9.00. Nasdaq futures vs fair value: -11.00. The S&P 500 futures trade nine points below fair value.

The major Asian bourses ended mostly lower as selling persisted for a second session. Bank of Japan Governor Haruhiko Kuroda said the economy remains on track for 1.5% growth. This has caused quite the stir among traders as it adds credence to yesterday's comments from an official who said the Bank of Japan does not see a current need for additional easing. Elsewhere, liquidity concerns remain in China ahead of the New Year as overnight SHIBOR edged up almost two basis points to 3.719% and two-week SHIBOR surged nearly 83 basis points to 6.765%.

Economic data was limited to Singapore's industrial production (+6.2% year-over-year versus -0.4% expected) and the Philippine trade balance, which swung to a $940 million deficit (-$740 million expected).

Japan's Nikkei tumbled 1.9% as a result of the stronger yen. Robotics maker Fanuc, who relies heavily on China, lost 3.0%.

Hong Kong's Hang Seng fell 1.3% as trade slipped below the 200-day moving average. Internet gaming company Tencent Holdings saw heavy selling, ending down 4.0%.

China's Shanghai Composite advanced 0.6% with shares gaining for the third time in four days. Property stocks were out in front as China Vanke climbed 4.0% and Poly Real Estate added 3.0%.

Major European indices trade near their lowest levels of the session with Spain's IBEX (-2.0%) leading the retreat. Economic data was limited as Great Britain's BBA Mortgage Approvals came in at 46,500 (47,200 expected, 45,400 prior); Italy's Retail Sales were unchanged month-over-month (0.4% forecast, -0.1% last) while the year-over-year reading ticked up 0.1% (-1.6% prior); and Spain's PPI rose 0.6% year-over-year (-0.4% consensus, 4.0% last).

Among news of note, Bank of England Governor Mark Carney said there are no plans for an imminent rate hike even with the unemployment rate within 0.1% of the BoE's tightening target. This comes after an article in The Financial Times indicated the central bank plans to scrap its forward guidance.

Great Britain's FTSE trades lower by 0.8% as financials lag. Aberdeen Asset Management, Aggreko, and Prudential are all down between 2.9% and 3.4%. On the upside, miners are showing strength with Fresnillo and Randgold Resources up 3.4% and 2.7%, respectively.

In Germany, the DAX holds a loss of 1.0% as 28 of its 30 components trade lower. Adidas is the weakest member, trading lower by 4.2% after Deutsche Bank cut its earnings estimates for the apparel maker. Fresenius Medical Care is the top performer, up 0.2%.

In France, the CAC trades down 1.3% with 38 components on the defensive. Software company Gemalto leads the decline with a loss of 3.9%. On the upside, industrials Legrand and Vinci hold respective gains of 1.7% and 1.0%.

Spain's IBEX sports a loss of 2.0% as all 35 components trade in the red. Banco Bilbao Vizcaya Argentaria and International Consolidated Airlines Group weigh, trading lower by 3.8% and 4.2%, respectively.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: -7.70. Nasdaq futures vs fair value: -8.80. Equity index futures remain pressured with the S&P 500 futures trading eight points below fair value. Overnight, markets in Asia followed the risk-off sentiment observed yesterday in the U.S. with Japan's Nikkei (-1.9%) leading the retreat as the yen strengthened. The currency continued rallying after the Asian session ended and USD/JPY now trades near 102.50.

Similar to yesterday, the continued weakness in equities has been a supportive factor for the bond market. Treasuries hold gains with the 10-yr yield down three basis points at 2.75% after being down as much as seven basis points roughly two hours ago. Elsewhere, gold futures are also seeing strength. The yellow metal trades higher by 0.4% at $1266.60 per troy ounce.

7:59 am: [BRIEFING.COM] S&P futures vs fair value: -11.20. Nasdaq futures vs fair value: -15.80. U.S. equity futures hover near their pre-market lows amid cautious overseas action. The S&P 500 futures trade 11 points below fair value with the entire decline coming after the start of the European session where the core indices display losses close to 1.0% apiece. Similar to yesterday, the equity weakness has turned into a supportive factor for the bond market. Treasuries hover near their highs with the 10-yr yield down five basis points at 2.73%.

Reviewing overnight developments:

Asian markets ended mixed. China's Shanghai Composite +0.6%, Hong Kong's Hang Seng -1.3%, and Japan's Nikkei -1.9%.

Economic data was limited:

Singapore's Industrial Production increased 6.2% year-over-year (-0.4% consensus, 4.0% last).

New Zealand's Credit Card Spending rose 4.7% year-over-year (6.9% prior).

In news:

In South Korea, Samsung added 0.6% after beating revenue estimates and issuing upbeat guidance.

Major European indices trade near their lowest levels of the session. Great Britain's FTSE -1.0%, Germany's DAX -1.3%, and France's CAC -1.4%. Elsewhere, Italy's MIB -1.7% and Spain's IBEX -2.7%.

Looking at economic data:

Great Britain's BBA Mortgage Approvals came in at 46,500 (47,200 expected, 45,400 prior).

Italy's Retail Sales were unchanged month-over-month (0.4% forecast, -0.1% last) while the year-over-year reading ticked up 0.1% (-1.6% prior).

Spain's PPI rose 0.6% year-over-year (-0.4% consensus, 4.0% last).

Among news of note:

Bank of England Governor Mark Carney said there are no plans for an imminent rate hike even with the unemployment rate within 0.1% of the BoE's tightening target. This comes after an article in The Financial Times indicated the central bank plans to scrap its forward guidance.

In U.S. corporate news:

Bristol-Myers (BMY 54.85, +0.90): +1.7% after beating earnings estimates by eight cents on above-consensus revenue.

Honeywell (HON 89.57, -0.23): -0.3% despite beating its earnings forecast by two cents.

Intuitive Surgical (ISRG 414.00, -25.00): -5.7% after reporting a bottom-line beat on revenue in-line with its preannouncement. In addition, the company said it will not be providing fiscal-year 2014 revenue guidance.

Juniper Networks (JNPR 27.60, +1.59): +6.1% after beating on earnings and revenue. Following its earnings beat, the stock was upgraded at Barclays, Goldman Sachs, and William Blair.

Kimberly-Clark (KMB 106.70, +1.28): +1.2% after beating bottom-line estimates by five cents on in-line revenue.

Microsoft (MSFT 37.10, +1.05): +2.9% following its ten-cent beat on a 14.3% year-over-year increase in revenue.

Procter & Gamble (PG 78.50, +0.26) +0.3% after reporting a one-cent beat on in-line revenue.

Starbucks (SBUX 73.65, +0.26): +0.4% following its mixed report that included a bottom-line beat on below-consensus revenue.

There is no economic data of note on today's schedule.

6:41 am: [BRIEFING.COM] S&P futures vs fair value: -13.50. Nasdaq futures vs fair value: -23.00.

6:40 am: [BRIEFING.COM] Nikkei...15391.56...-304.30...-1.90%. Hang Seng...22450.06...-283.80...-1.30%.

6:40 am: [BRIEFING.COM] FTSE...6700.76...-75.30...-1.10%. DAX...9529.15...-101.90...-1.10%.

S&P 500 Slides Most Since June on Emerging Market Turmoil By Nick Taborek Jan 24, 2014 4:54 PM ET

U.S. stocks sank the most since June, capping the worst week for benchmark indexes since 2012, as a selloff in developing-nation currencies spurred concern global markets will become more volatile.

Caterpillar Inc., General Electric Co. and Boeing Co. slid at least 2.6 percent to pace losses in the Dow Jones Industrial Average. (INDU) Kansas City Southern plunged 15 percent, the biggest retreat since 2008, after reporting lower-than-estimated earnings. International Game Technology tumbled 15 percent as the maker of slot machines posted first-quarter profit that missed analysts’ projections.

The Standard & Poor’s 500 Index (SPX) retreated 2.1 percent to 1,790.29 at 4 p.m. in New York to close at the lowest level since Dec. 17. The benchmark index declined 2.6 percent this week. The Dow slid 318.24 points, or 2 percent, to 15,879.11 today. The 30-stock gauge lost 3.5 percent this week. About 8.8 billion shares changed hands on U.S. exchanges, the busiest trading day of the year.

Opinion: Look Out Below, Follow-Through Edition

“The volatility of the emerging markets and the currency impacts are affecting U.S. markets,” Eric Teal, who helps oversee $3.5 billion as the chief investment officer at First Citizens BancShares Inc. in Raleigh, North Carolina, said by phone. “Following the strong gains of last year, I think it’s to be expected that you might have an overreaction here of selling.”

Photographer: Jason DeCrow/AP Photo

Attachment:

![iyzrZAyFePyA[1].jpg](./download/file.php?id=3101&t=1&sid=65d04c3bca06ca2152bb31674703c3a0) iyzrZAyFePyA[1].jpg [ 66.69 KiB | Viewed 276 times ]

iyzrZAyFePyA[1].jpg [ 66.69 KiB | Viewed 276 times ]

Specialist Vincent Surace works on the floor of the New York Stock Exchange on Jan. 24, 2014.

Emerging ConcernsEmerging-market currencies had their worst selloff in five years yesterday as Argentine policy makers devalued the peso by reducing support in the foreign-exchange market. The Turkish lira plunged, Ukraine’s hryvnia sank to a four-year low and South Africa’s rand weakened beyond 11 per dollar for the first time since 2008. China (EC11FLAS)’s banking regulator ordered its regional offices to increase scrutiny of credit risks in the coal-mining industry, said two people with knowledge of the matter, signaling government concern about possible defaults.

Investors are losing confidence in some of the biggest developing nations, extending the rout in currencies that began last year when the Federal Reserve signaled it would slow the pace of its monthly purchases of Treasuries and mortgage bonds. The S&P 500 fell 0.9 percent yesterday and the Dow dropped to a one-month low after a gauge of manufacturing activity in China unexpectedly contracted.

The MSCI Emerging Markets Index lost 1.5 percent today, extending its decline for the year to more than 5 percent, while Europe’s equity benchmark slid the most since June.

‘Massive Selloff’Three rounds of Fed monetary stimulus have helped the S&P 500 rise about 165 percent from a 12-year low in 2009. The U.S. equity benchmark rallied 30 percent to a record last year, the most since 1997. Equities have since pared those gains, with the index down more than 3 percent for 2014.

“You’ve had a massive selloff in these emerging-market currencies,” Nick Xanders, a London-based equity strategist at BTIG Ltd., said by telephone. “Ruble, rupee, real, rand: they’ve all fallen and the main cause has been tapering. A lot of companies that have benefited from emerging-markets growth are now seeing it go the other way.”

The S&P 500 trades at about 15.2 times the estimated earnings of its members, more than the five-year average multiple of 14.1, data compiled by Bloomberg show.

Ten companies in the S&P 500, including Procter & Gamble Co. (PG) and Bristol-Myers Squibb Co., reported results today. Of the 122 index members that have released earnings so far this season, 74 percent have beaten estimates for profit and 67 percent have exceeded sales projections, according to data compiled by Bloomberg.

VIX SurgePer-share profit for companies in the benchmark probably climbed 6.6 percent in the fourth quarter, while sales increased 2.6 percent, according to analysts surveyed by Bloomberg.

The Chicago Board Options Exchange Volatility Index (VIX), the gauge of S&P 500 options known as the VIX, surged the most since April, adding 32 percent to 18.14 today. The gauge rallied 46 percent this week, for the biggest weekly increase since May 2010.

All 10 main S&P 500 groups retreated today. Industrial and materials stocks lost at least 2.7 percent to pace declines. Boeing sank 3.3 percent to $136.65 and Caterpillar lost 2.6 percent to $86.17, among the biggest declines in the Dow.

Companies whose earnings are most tied to economic swings dropped. The Morgan Stanley Cyclical Index lost 3 percent, the most since April, as Whirlpool Corp. slid 5 percent to $145.68. An S&P gauge of homebuilders fell 3.4 percent for the steepest decline since August. D.R. Horton Inc. slipped 4.9 percent to $20.88 and PulteGroup Inc. fell 4.1 percent to $18.84.

Transportation IndexThe Dow Jones Transportation Average (TRAN), which reached a record yesterday, slid 4.1 percent for the biggest one-day decline since 2011. Delta Air Lines Inc. fell 4.3 percent to $31.11.

Kansas City Southern lost 15 percent to $99.49. The railroad operator reported fourth-quarter profit that missed analysts’ estimates as energy revenue fell 17 percent due to a decline in coal shipments.

International Game Technology tumbled 15 percent to $15.04. The Las Vegas-based company posted earnings of 25 cents a share, missing the average analyst estimate by 6 cents.

Intuitive Surgical Inc. lost 6.4 percent to $410.76. The maker of a robotic-surgery device said fourth-quarter systems revenue decreased by 23 percent from a year earlier.

Phone, utility and consumer-staples stocks, which have the highest dividend yields among 10 S&P 500 groups, fell less than 1.2 percent, as yields on 10-year Treasuries fell to an eight-week low, boosting the allure of equity income.

Dividend StocksProcter & Gamble climbed 1.2 percent to $79.18. The world’s largest consumer-goods maker posted second-quarter profit that topped analysts’ estimates as sales of products such as Pampers diapers rose in emerging markets.

Microsoft Corp. added 2.1 percent, the most in the Dow, to $36.81. Customers flocked to the company’s game consoles and cloud software last quarter, helping sales beat analysts’ projections.

Juniper Networks Inc. (JNPR) rallied 6.6 percent to $27.72 for the biggest gain in the S&P 500. The networking-equipment maker reported sales that exceeded analysts’ estimates. Revenue in the fourth quarter increased 12 percent to $1.27 billion from $1.14 billion a year earlier, the Sunnyvale, California-based company said yesterday in a statement. Analysts had predicted sales of $1.22 billion.

Discover Financial Services climbed 2.8 percent to $53.88. Discover rose the most in three months after reporting profit that beat analysts’ estimates as credit-card spending and loan demand increased.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage