Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

011514-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3597.50.png [ 176 KiB | Viewed 301 times ]

011514-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3597.50.png [ 176 KiB | Viewed 301 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,180.00 dollars or +11.80 points, Emini ES ($ES_F) futures @

$1,937.50 dollars or +38.75 points, Light Crude Oil CL ($CL_F) futures @

$480.00 dollars or +0.48 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,597.50 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1698 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

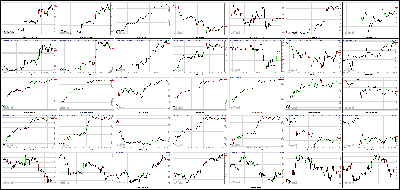

S&P 500 Ekes Out New Record High Attachment:

011514-Key-Price-Action-Markets.png [ 519.73 KiB | Viewed 317 times ]

011514-Key-Price-Action-Markets.png [ 519.73 KiB | Viewed 317 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Stocks rose for a second day Wednesday, with the S&P 500 ending at a new record on strong bank earnings and solid economic reports.

The S&P 500 inched above its previous closing high from Dec. 31, led by big gains in shares of technology companies, such as NetApp (NTAP, Fortune 500) and Citrix Systems (CTXS). The Dow Jones industrial average gained more than 100 points, but is still down for the year. The Nasdaq rose to its highest levels in more than 13 years.

CNNMoney's Tech 30 index was also higher, with Twitter (TWTR) and Apple (AAPL, Fortune 500) both up.

Bank of America (BAC, Fortune 500) boosted investor confidence by reporting better-than-expected earnings and revenue for the fourth quarter. The report followed solid earnings Tuesday from JPMorgan Chase (JPM, Fortune 500) and Wells Fargo (WFC, Fortune 500). Shares of Bank of America rose on the news, as did major banks that have yet to report such as Goldman Sachs (GS, Fortune 500) and Citigroup (C, Fortune 500).

The financial sector is expected to have the best profit growth in the fourth quarter, according to FactSet Research. Overall, earnings for the companies in the S&P 500 are expected to be up 6.1% versus the fourth quarter of last year.

In economic news, producer prices increased 0.4% in December, the government said. Manufacturing activity in the New York area expanded at a rapid pace in January, according to the Federal Reserve Bank of New York.

The Fed's latest snapshot of economic conditions across the country showed that growth continued at a modest pace in recent weeks. Most of the central bank's regions expect "more of the same" or an improvement in activity going forward, according to the Beige Book.

Wednesday's reports "added to renewed market optimism," following solid December retail sales and business inventories data on Tuesday, said Michael Englund, an economist at Action Economics. Despite an unexpected slowdown in hiring last month, "the bulk of U.S. economic surprises remain upward," he added.

* How to invest when the market feels scaryGeneral Motors (GM, Fortune 500) shares fell even though the automaker announced on Tuesday that it will pay its first dividend since 2008. The stock was down because the company said Wednesday morning that it expects 2014 profit margins to be similar to last year and that restructuring costs for fixing problems in Europe are expected to be about $1.1 billion.

The automaker also predicted most growth globally for the industry this year. But GM still has fans on StockTwits.

"$GM Buying on today's weakness," said JDR1983.

Shares of electric automaker Tesla Motors (TSLA) were up again after CEO Elon Musk told CNN late Tuesday that the company is on track to produce a cheaper, mass-market car in three years and still plans to offer a full-size pickup similar to the Ford (F, Fortune 500) F-150 in four to five years.

The stock traded as high as $172 a share, but some traders are betting on more upside.

"$TSLA this is $200+ share... their car is amazing," said Dexterslab.

Netflix (NFLX) shares fell one day after a federal appeals court struck down Federal Communications Commission rules that prohibit Internet service providers from restricting access to legal Web content. The stock was the biggest loser in the Tech 30 index.

"$NFLX change in net neutrality rules makes this too crazy to get in yet," said StockTwits user shakerguy.

Shares of 3D printer maker ExOne (XONE) fell sharply after it warned late Tuesday that revenue would be far below its earlier forecasts. The warning follows disappointing guidance from 3D printer maker Stratasys (SSYS) earlier in the day. Fellow 3D printer companies 3D Systems (DDD) and Voxeljet (VJET) were down in early trading as well.

A few traders on StockTwits said the selling in 3D printing stocks was overdone and were stepping in to buy.

"$VJET $DDD 3D usually loses momentum a few times a year. Eager shorts love call the top. Every significant dip has been a buying opp," said MTPennybags.

The main European stock market indexes all finished the day higher. Burberry (BBRYF) shares surged in London after the luxury retailer reported a 14% jump in retail revenue in the third quarter, which includes the holiday season. Asian markets mostly closed the day with gains.

4:15 pm: [BRIEFING.COM] Equities built on their Tuesday gains, turning in their best two-day stretch since mid-December. During that two-day swing, the S&P 500 jumped from its lowest level of the year to a fresh record close of 1848.38. Stocks spent the entire session in positive territory after receiving an opening boost from the World Bank hiking its 2014 global GDP growth forecast to 3.2% from 3.0%.

Seven of ten sectors finished in the green with cyclical groups driving the advance. Financials (+1.2%) and technology (+1.2%) displayed early strength and their outperformance lasted into the close.

The financial sector was buoyed by its top components after Bank of America (BAC 17.15, +0.38) beat on earnings and revenue. The stock jumped 2.4% while JPMorgan Chase (JPM 59.49, +1.75) and Wells Fargo (WFC 46.40, +0.81), both of which turned in satisfactory reports on Tuesday, gained 3.0% and 1.8%, respectively.

Elsewhere, the tech sector was underpinned by some of its most influential members. Apple (AAPL 557.36, +10.97) did some heavy lifting, climbing 2.0% amid upbeat commentary surrounding its upcoming iPhone launch in China. Chipmakers also displayed strength after Intel (INTC 26.67, +0.16) received an upgrade for the second day in a row. The stock gained 0.6% while the PHLX Semiconductor Index rose 0.9%.

Outside of the two largest sectors, gains in other areas were much more subdued. Industrials (+0.7%) and materials (+0.7%) outperformed while the remaining cyclical groups-consumer discretionary (+0.2%) and energy (-0.3%)-lagged.

Notably, the discretionary sector was pressured by homebuilders and retailers. The iShares Dow Jones US Home Construction ETF (ITB 24.31, -0.05) and SPDR S&P Retail ETF (XRT 84.02, -0.29) both slipped 0.3% with the retail ETF extending its 2014 loss to 4.6%.

On the countercyclical side, telecom services (+1.5%) outperformed while consumer staples (unch), health care (-0.1%), and utilities (-0.2%) lagged.

Treasuries posted modest losses as the 10-yr yield ticked up one basis point to 2.88%.

Participation was a bit below average as 704 million shares changed hands at the NYSE.

Also of note, the Federal Reserve released its January Beige Book, but true to form, the report was essentially ignored by the market. The report indicated that during the six weeks of 2013, the twelve Fed Districts observed a continued expansion of economic activity. Nine districts characterized the expansion as 'moderate' while Boston and Philadelphia Districts described the pace as 'modest.' For its part, the Kansas City region saw little change in activity.

With regard to manufacturing, nearly all districts reported steady growth in the sector but Kansas City saw a decline in production and shipments.

Lastly, prices were largely unchanged across all regions. However, Kansas City was singled out again in this section for observing a rise in some raw material prices.

Today's economic news included three data points:

December PPI increased 0.4% while the Briefing.com consensus expected an uptick of 0.3%. Energy prices were a main contributor, increasing 1.6%. Most of the gain in energy costs was a result of a 2.2% increase in gasoline prices. Food prices fell 0.6% due to a 13.4% decrease in vegetable prices. Excluding food and energy, core prices unexpectedly spiked in December. Prices increased 0.3%, the largest monthly jump since rising 0.5% in July 2012. The consensus forecast called for a more modest uptick of 0.1%.

The Empire Manufacturing Survey for January jumped to 12.5 from 1.0 while the Briefing.com consensus expected the survey to improve to 3.5.

The weekly MBA Mortgage Application Index jumped 11.9% to follow last week's 4.2% decline.

Tomorrow, weekly initial claims and December CPI will be released at 8:30 ET while Net long-term TIC flows for November will be announced at 9:00 ET. The January Philadelphia Fed survey and the January NAHB Housing Market Index will both be released at 10:00 ET.

Nasdaq +0.9% YTD

Russell 2000 +0.7% YTD

S&P 500 0.0% YTD

DJIA -0.6% YTD

3:35 pm: [BRIEFING.COM] Natural gas futures ended today's pit trading session selling off and ending at a new LoD. By the time floor trading ended, Feb nat gas fell 5 cents to $4.32/MMBtu, off the HoD of $4.43/MMBtu.

Crude oil slowly slid lower in the last 50 minutes of trading, but held gains and finished $1.64/barrel higher at $94.16/barrel.

Precious metals were weak today, while copper rose. Feb gold lost $6.20/oz today and finished at $1239/oz. Mar silver fell $0.15 to $20.13/oz and Mar copper rose 2 cents to $3.36/lb.

3:05 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.6% with one hour remaining in today's session. Equities notched their highs during the first two hours of action and the key indices have been trapped inside narrow ranges since the late morning.

The range-bound afternoon has been reflected by a slowdown in intraday volume. At this juncture, only 425 million shares have traded hands at the NYSE, which means the final tally is likely to come in below the long-run average of 716 million.

Yesterday's final volume (636 million) was also below average after Monday's selloff (719 million) invited above-average activity.

2:30 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.5% as seven of ten sectors display gains.

As expected, the recently-released Beige Book was essentially ignored by the equity market. The report indicated that during the six weeks of 2013, the twelve Fed Districts observed a continued expansion of economic activity. Nine districts characterized the expansion as 'moderate' while Boston and Philadelphia Districts described the pace as 'modest.' For its part, the Kansas City region saw little change in activity.

With regard to manufacturing, nearly all districts reported steady growth in the sector but Kansas City saw a decline in production and shipments.

Lastly, prices were largely unchanged across all regions. However, Kansas City was singled out again in this section for observing a rise in some raw material prices.

1:55 pm: [BRIEFING.COM] Quiet afternoon continues with the major averages hovering within a striking distance of their session highs.

Similar to the broader market, today's top sectors-financials (+1.0%) and technology (+1.1%)-also trade just below their best levels of the day. However, the industrial sector, which was a notable outperformer earlier, has trimmed its gain to less than 0.5%.

Also of note, three of four countercyclical groups-consumer staples (unch), health care (-0.2%), and utilities (-0.3%)-have slipped from their recent levels. Although their underperformance has not been an issue for the broader market today, it may become problematic if the third-largest S&P 500 group-health care-shows additional weakness.

On a separate note, the Federal Reserve will release its January Beige Book at the top of the hour but the report is not known for eliciting a strong reaction in equities. We will summarize the report in our upcoming 14:30 ET update.

1:30 pm: [BRIEFING.COM] After a sluggish start to the year, the stock market has rediscovered some of the bullish swagger it displayed so readily in 2013. Over the course of the past two sessions, the Nasdaq has tacked on close to 100 points, or 2.4%, with Apple (AAPL 558.30, +11.91) playing a key part in the advance. Apple for its part has gained more than 4.0% over the last two sessions.

The reversal of fortune for the broader market has been noteworthy and certainly surprising for many who were thinking about, and positioning for, further downside extension on the other side of Monday's rout. That didn't happen and some short-covering has ensued that has been an expedient for the market's recovery effort.

While today's gains are robust, the buying interest is not as broad-based as yesterday. Thus far, the utilities (-0.3%), health care (-0.1%), and energy (-0.3%) sectors continue to sit this one out.

1:00 pm: [BRIEFING.COM] At midday, the stock market is enjoying an extension of yesterday's rally with the S&P 500 trading higher by 0.6%. Given its current level, the benchmark index is on track to register its best two-day swing since mid-October. Furthermore, today's advance has pushed the S&P to a fresh record high (1850.89).

Equities began the day on an upbeat note after the World Bank hiked its 2014 GDP growth forecast to 3.2% from 3.0%. This also provided early support for markets across Europe, where the core indices settled on their highs.

In addition to the upbeat global outlook, the two largest S&P 500 sectors-financials (+0.9%) and technology (+1.2%)-displayed early strength, which underpinned the broader market.

The financial sector has received support from top components after Bank of America (BAC 17.18, +0.41) beat on earnings and revenue. The stock trades higher by 2.4% with today's gain running its 2014 return to 10.4%.

Elsewhere, the outperformance of the technology space has been driven, in part, by its largest component. Apple (AAPL 559.26, +12.87) trades up 2.4% after China Mobile (CHL 50.56, +0.08) said iPhone pre-orders are 'in the millions.' Chipmakers are also playing a part in the sector's outperformance after Intel (INTC 26.83, +0.32) was upgraded to 'Outperform' from 'Market Perform' at BMO Capital Markets. Intel trades higher by 1.2% while the PHLX Semiconductor Index holds an advance of 0.8%.

Outside of financials and technology, gains in other sectors are much more subdued. The telecom services sector (+1.5%) is also showing notable strength, but the smallest S&P 500 group has little influence over the broader market.

Although the telecom sector outperforms, the remaining defensive sectors lag. Consumer staples (+0.1%), health care (unch), and utilities (-0.2%) all trade little changed.

Treasuries hold modest losses with the 10-yr yield up two basis points at 2.90%.

Today's economic news included three data points but one more report (January Beige Book) is set to be released at 14:00 ET.

December PPI increased 0.4% while the Briefing.com consensus expected an uptick of 0.3%. Energy prices were a main contributor, increasing 1.6%. Most of the gain in energy costs was a result of a 2.2% increase in gasoline prices. Food prices fell 0.6% due to a 13.4% decrease in vegetable prices. Excluding food and energy, core prices unexpectedly spiked in December. Prices increased 0.3%, the largest monthly jump since rising 0.5% in July 2012. The consensus forecast called for a more modest uptick of 0.1%.

The Empire Manufacturing Survey for January jumped to 12.5 from 1.0 while the Briefing.com consensus expected the survey to improve to 3.5.

The weekly MBA Mortgage Application Index jumped 11.9% to follow last week's 4.2% decline.

12:30 pm: [BRIEFING.COM] The S&P 500 remains near its best level of the day with the index in the midst of its strongest two-day run since mid-October. Although the benchmark average ended Monday's session at its lowest level of 2014, yesterday's rally combined with today's advance have sent the index to a fresh all-time high (1850.89).

Even though the S&P 500 now sports a slight January gain (+0.1%), seven of ten sectors remain lower for the month. Telecom services (-2.7%) and energy (-2.4%) have endured a slow start to the year while health care (+2.9%), financials (+1.1%), and technology (+1.0%) have displayed strength.

Elsewhere, Treasuries have regained a portion of their losses but they remain lower on the day (10-yr yield +2 bps at 2.90%).

12:00 pm: [BRIEFING.COM] The major averages continue to hold solid gains between 0.5% (S&P 500) and 0.7% (Dow Jones) as seven of ten sectors hover in the green.

As mentioned earlier, cyclical sectors trade mixed with respect to the broader market as financials, industrials, and technology outperform while consumer discretionary (+0.1%) and energy (-0.2%) lag. The last cyclical group, materials, trades in-line with the S&P 500.

Notably, the discretionary sector is being pressured by homebuilders and retailers. The iShares Dow Jones US Home Construction ETF (ITB 24.32, -0.05) is lower by 0.2% while the SPDR S&P Retail ETF (XRT83.93, -0.38) trades down 0.5%.

Elsewhere, the energy sector hovers in the red even as crude oil trades higher by 1.9% at $94.34 per barrel. Dow component ExxonMobil (XOM 98.90, -0.22) lags, trading lower by 0.2%.

11:25 am: [BRIEFING.COM] Recent action saw the S&P 500 (+0.5%) climb to a fresh record high (1850.89) in a move that also pulled the index out of negative territory for the month.

Financials (+0.9%) and technology (+1.0%) remain in the lead and the industrial sector (+0.7%) has also climbed into a position of strength. Transports lag (+0.2%), but their underperformance is being outweighed by the relative strength of defense contractors. The PHLX Defense Index is higher by 1.0% with the top industrial component, General Electric (GE 27.36, +0.39), trading higher by 1.5%.

Machinery manufacturers are also seeing strength after the World Bank raised its 2014 global GDP growth forecast to 3.2% from 3.0%. Caterpillar (CAT 92.58, +2.02) and Joy Global (JOY 56.51, +1.11) sport respective gains of 2.3% and 2.0%.

10:55 am: [BRIEFING.COM] The major averages continue to hover just below their best levels of the session but the Dow Jones Industrial Average (+0.6%) has overtaken the Nasdaq (+0.5%) for the lead.

The price-weighted Dow outperforms as 25 of its 30 components register gains. Of the 25 advancers, nine trade with gains of at least 1.0%. Microsoft (MSFT 36.48, +0.70) is the top index component, trading higher by 2.0% on top of yesterday's 2.3% gain.

On the downside, Merck (MRK 52.52, -0.48) is the weakest component, trading down 0.9%. On a related note, the health care sector holds a modest loss of 0.2%. Biotechnology weighs with the iShares Nasdaq Biotechnology ETF (IBB 241.64, -2.41) trading lower by 1.0%.

10:35 am: [BRIEFING.COM] Commodities are mixed this morning with the dollar index trading above 81 and currently just under its HoD.

Ahead of the weekly EIA inventory data figures, crude oil futures were sitting just under highs for the day (current contract is February)

Following the data, crude oil prices popped to new highs for the day and are now +1.1% at $93.64/barrel (Feb contract)

Natural gas futures sold off this morning from its HoD, which was hit in early morning action, following recent strong weather-driven gains. Feb nat gas is now +0.1% at $4.37/MMBtu.

Gold and silver futures have been in the red all day so far. Feb gold is now -0.6% at $1237.80/oz, Mar silver is -1.0% at $20.09/oz.

10:00 am: [BRIEFING.COM] Equity indices have continued inching higher after starting the session with gains. As a result of the early advance, the Russell 2000 has joined the Nasdaq Composite in positive territory for the month. The Russell is higher by 0.5% so far this month versus the 0.6% gain for the Nasdaq. For its part, the S&P 500 remains lower by 0.3% so far in January.

Although the major averages hover near their highs, only two sectors-financials and technology-trade well ahead of the broader market. However, since the two groups represent just over a third of the entire S&P 500, their performance bears watching throughout the day.

9:40 am: [BRIEFING.COM] The major averages began the session on a higher note with gains paced by the Nasdaq (+0.5%) once again. Meanwhile, the S&P 500 displays a more modest gain of 0.3% as eight of ten sectors hover in the green.

The financial sector (+0.8%) has climbed into an early lead while technology (+0.7%) follows not far behind. The remaining cyclical groups all trade with gains of no more than 0.4%.

Notably, the financial sector has received support from Bank of America (BAC 17.29, +0.52), which reported a bottom-line beat on better-than-expected revenue. Including today's 3.0% gain, the stock is up nearly 11.0% so far in January.

Treasuries hover on their lows with the 10-yr yield up four basis points at 2.91%.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: +4.20. Nasdaq futures vs fair value: +14.20. With 15 minutes to go before the start of the cash session, the stock market is on track for a modestly higher open. The S&P 500 futures trade four points above fair value as the benchmark index will look to continue its rally after turning in its best performance of the month on Tuesday.

Futures received an overnight boost after the World Bank hiked its 2014 GDP growth forecast to 3.2% from 3.0%. This also provided early support for markets across Europe, where the key indices trade at their best levels of the session.

Domestically, investors received the latest Producer Price Index, which pointed to a December increase of 0.4% (Briefing.com consensus 0.3%). Energy prices were a main contributor, increasing 1.6%. Most of the gain in energy costs was a result of a 2.2% increase in gasoline prices. Food prices fell 0.6% due to a 13.4% decrease in vegetable prices. Excluding food and energy, core prices unexpectedly spiked in December. Prices increased 0.3%, the largest monthly jump since rising 0.5% in July 2012. The consensus forecast called for a more modest uptick of 0.1%.

Separately, the Empire Manufacturing Survey for January jumped to 12.5 from 1.0 while the Briefing.com consensus expected the survey to improve to 3.5.

The futures market was little changed following the data but Treasuries fell to lows (10-yr yield +3 bps at 2.90%).

Although pre-market action has been relatively quiet, a handful of individual names have garnered considerable early interest. On that note, Bank of America (BAC 17.23, +0.46) sports a pre-market gain of 2.7% on heavy volume after reporting a bottom-line beat on above-consensus revenue. On the flip side, General Motors (GM 39.47, -0.53) is lower by 1.3% after the company forecast modest global industry growth in 2014 and declared a quarterly dividend of $0.30.

8:56 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +12.70. The S&P 500 futures trade three points above fair value.

Markets rallied across most of Asia, buoyed by yesterday's strong gains on Wall Street. In economic data, China's M2 money supply was light at 13.6% year-over-year (13.9% expected) while new loans (CNY438 billion actual versus CNY589 billion expected) also missed. Elsewhere, Japan's M2 money stock rose 4.2% year-over-year (4.5% forecast, 4.4% prior) and Machine Tool Orders jumped 28.0% year-over-year (15.4% last). Also of note, India's Wholesale Price Index eased to 6.2% year-over-year (7.0% expected, 7.5% previous), a five-month low.

Japan's Nikkei jumped 2.5%, posting its best gain in four months and nearly erasing Tuesday's entire fall as the weak yen fueled the rally. Exporters were in favor as TDK surged 6.8% and Toyota Motor gained 1.5%.

Hong Kong's Hang Seng added 0.5% but trade remained trapped in the tight range that has been in place for nearly all of 2014. PC maker Lenovo was the top performer, climbing 5.5%, to its best level since the spring of 2000, as momentum continues following last week's upbeat PC shipments report. The company posted solid numbers despite many of its competitors seeing weak demand.

China's Shanghai Composite slipped 0.2% as shares traded lower for the eighth time in ten 2014 sessions. Financials lost ground after new loans fell short of estimates. ICBC gave up 1.7% and Huxia Bank slid 2.4%.

Major European indices sit at their best levels of the session after rallying steadily through the first half of action. Investors received a handful of economic data points as eurozone trade surplus expanded to EUR16.00 billion from EUR14.30 billion (EUR16.70 billion forecast), Great Britain's CB Leading Index rose 0.5% month-over-month (0.4% last), and Swiss retail sales rose 4.2% year-over-year (1.6% consensus, 1.6% last). Elsewhere, Spain's CPI ticked up 0.1% month-over-month, as expected (0.2% prior). On an annualized basis, CPI rose 0.3% (0.2% forecast, 0.2% prior).

Among news of note, the Bank of France has proposed cutting the Livret savings rate from 1.25% to 1.00%, but the proposal has been met with pushback from Finance Minister Pierre Moscovici.

Great Britain's FTSE is higher by 0.5% with Burberry in the lead. The apparel manufacturer trades higher by 4.9% after reporting better-than-expected holiday sales. Financials have also displayed strength with Prudential and Standard Life both up near 2.3%.

In France, the CAC holds an advance of 0.6% as bank shares outperform. BNP Paribas and Credit Agricole hold gains close to 2.0% apiece. On the downside, consumer names Danone, L'Oreal, and Pernod Ricard hold display losses between 0.7% and 1.0%.

Germany's DAX trades up 1.3% with Deutsche Lufthansa leading. The airline is higher by 4.9%. Utilities also outperform with E.ON and RWE up 1.9% and 3.4%, respectively.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +12.00. The S&P 500 futures trade three points above fair value.

December producer prices rose 0.4% while the Briefing.com consensus expected an uptick of 0.3%. Core producer prices rose 0.3% while the consensus expected an uptick of 0.1%.

Separately, the Empire Manufacturing Survey for January registered a reading of 12.5, which was up from the prior month's revised reading of 2.2 (from 1.0). Economists polled by Briefing.com expected the survey to improve to 3.5.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +12.70. U.S. equity futures hover near their highs amid upbeat overseas action. The S&P 500 futures trade three points above fair value.

Reviewing overnight developments:

Asian markets ended mostly higher. China's Shanghai Composite -0.2%, Hong Kong's Hang Seng +0.5%, and Japan's Nikkei +2.5%.

Investors received several economic data points:

China's M2 money stock grew 13.6% year-over-year (13.8% expected, 14.2% prior) while new loans increased CNY483 billion (CNY600 billion expected, CNY625 billion previous).

Japan's M2 money stock rose 4.2% year-over-year (4.5% forecast, 4.4% prior) and Machine Tool Orders jumped 28.0% year-over-year (15.4% last).

India's WPI rose 6.16% year-over-year (7.00% forecast, 7.52% previous).

South Korea's unemployment rate ticked up to 3.0% from 2.9% (2.9% expected).

Singapore's retail sales fell 8.7% year-over-year (-9.0% expected, -9.4% prior).

Australia's new motor vehicle sales increased 1.7% month-over-month (2.1% prior).

New Zealand's FPI ticked down 0.1% month-over-month (-0.2% last).

In news:

People's Bank of China statistics director Sheng said the central bank does not plan to tinker with monetary policy in 2014, instead maintaining a prudent stance.

Major European indices sit at their best levels of the session. Great Britain's FTSE +0.4%, France's CAC +0.7%, and Germany's DAX +1.4%. Elsewhere, Spain's IBEX +0.4% and Italy's MIB +1.0%.

Looking at economic data:

Eurozone trade surplus expanded to EUR16.00 billion from EUR14.30 billion (EUR16.70 billion forecast).

Great Britain's CB Leading Index rose 0.5% month-over-month (0.4% last).

Spain's CPI ticked up 0.1% month-over-month, as expected (0.2% prior). On an annualized basis, CPI rose 0.3% (0.2% forecast, 0.2% prior).

Swiss retail sales rose 4.2% year-over-year (1.6% consensus, 1.6% last).

Among news of note:

The Bank of France has proposed cutting the Livret savings rate from 1.25% to 1.00%, but the proposal has been met with pushback from Finance Minister Pierre Moscovici.

In U.S. corporate news:

Bank of America (BAC 17.14, +0.37): +2.3% after reporting a three-cent beat on above-consensus revenue.

General Motors (GM 39.65, -0.40): -1.0% after the company forecast modest global industry growth in 2014 and declared a quarterly dividend of $0.30. Peer Ford (F 16.36, -0.04) is lower by 0.2%.

Regeneron Pharmaceuticals (REGN 297.00, -3.32): -1.1% after BMO Capital Markets downgraded the stock to 'Market Perform' from 'Outperform.'

The weekly MBA Mortgage Application Index jumped 11.9% to follow last week's 4.2% decline.

December PPI and the January Empire Manufacturing survey will both be reported at 8:30 ET while the day's data will be topped off with the 14:00 ET release of the Federal Reserve's Beige Book for January.

6:19 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +12.00.

6:19 am: [BRIEFING.COM] Nikkei...15808.73...+386.30...+2.50%. Hang Seng...22902.00...+110.70...+0.50%.

6:19 am: [BRIEFING.COM] FTSE...6788.91...+22.10...+0.30%. DAX...9627.88...+87.20...+0.90%.

Aussie Falls to Three-Year Low as Asian Stocks Erase Gain By Richard Frost and Candice Zachariahs Jan 16, 2014 1:31 AM ET

Australia’s dollar weakened to a three-year low after a surprise drop in employment, while the country’s bonds and equities rose. Asian stocks were little changed before U.S. jobs and inflation data.

The Australian dollar lost 1.2 percent to 88.10 U.S. cents at 3:22 p.m. in Tokyo, heading for the lowest close since July 2010, as traders stepped up bets the central bank will cut interest rates. Yields on the nation’s 10-year government bonds fell six basis points, and the S&P/ASX 200 Index (AS51) rallied 1.2 percent. The MSCI Asia Pacific Index erased an earlier 0.3 percent advance. Standard & Poor’s 500 Index futures were little changed. The greenback gained 0.2 percent to 104.72 yen.

Australian employers cut 22,600 jobs last month, data today showed, boosting odds of a rate reduction by July to 45 percent from 24 percent. U.S. initial jobless claims will be released today as investors gauge the outlook for trimming of stimulus. Inflation data in the U.S. and euro zone are also due. Goldman Sachs Group Inc. and Citigroup Inc. are among S&P 500 members to release earnings today after Bank of America Corp. (BAC) joined JPMorgan Chase & Co. in posting profit that beat estimates.

“One of the largest distortions in FX markets is being unwound and that’s the Federal Reserve starting to back away from the market,” said David Forrester, a currency strategist at Macquarie Bank Ltd. in Singapore. “The Aussie and Australia are still expensive relative to things such as productivity as well as commodity prices, and we continue to estimate the fair value of the Aussie in the low to mid 80s.”

Photographer: Brendon Thorne/Bloomberg

Office workers sit outside 1 Martin Place during lunch hour in Sydney.

Jobs Data

The Aussie declined against all 16 major peers. It dropped as low as NZ$1.0579, the weakest since December 2005.

The December decline in Australian employment followed a 15,400 gain the previous month, the statistics bureau said, and compared with a 10,000 increase predicted by economists. The unemployment rate held at 5.8 percent, the highest in four years.

The dollar added to a two-day, 1.5 percent advance against the yen. The greenback was 0.2 percent lower at $1.3626 per euro from yesterday, when it advanced 0.5 percent.

Initial jobless claims in the U.S. probably fell to 328,000 in the week ended Jan. 11, the fewest since November, according to the median estimate of economists surveyed before the Labor Department report today. The Federal Reserve Bank of Philadelphia’s general economic index is also due.

Business Outlook

The Fed in its Beige Book business survey released yesterday said that growth in December was buoyed by gains in holiday spending by consumers, an improving labor market and strength in manufacturing. Nine of 12 Fed districts grew at a moderate pace, up from seven in the previous report, released on Dec. 4. Two districts said growth was modest, down from four.

About the same number of stocks rose as fell on MSCI’s Asian index. The Topix closed little changed, erasing an earlier 1.1 percent advance. The Nikkei 225 Stock Average dropped 0.4 percent. Hong Kong’s Hang Seng Index gained 0.4 percent while a gauge of mainland Chinese companies traded in the city fell than 0.1 percent.

Tencent Holdings Ltd., Asia’s largest Internet company by market value, rallied to a record in Hong Kong after announcing an investment in a Chinese logistics-center operator to boost its e-commerce business.

The S&P 500 rose 0.5 percent yesterday, pushing the index above its 2013 close of 1,848.36. Sixty-one percent of the 31 S&P 500 members that have posted quarterly earnings this season have exceeded analysts’ estimates, while 64 percent beat projections on sales, data compiled by Bloomberg show.

U.S. consumer prices probably rose 1.5 percent in December from a year earlier, after gaining 1.2 percent in the previous month, according to a Bloomberg survey before today’s report.

Atlanta Fed President Dennis Lockhart, who doesn’t vote on monetary policy this year, said yesterday he expects inflation that’s been “too low” will accelerate toward the Fed’s 2 percent target. Chairman Ben S. Bernanke speaks today.

Brazil raised its target Selic rate by 50 basis points to 10.5 percent yesterday, increasing key borrowing costs for the sixth straight meeting as policy makers strive to contain accelerating inflation.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage