Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

010914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4485.00.png [ 174.11 KiB | Viewed 394 times ]

010914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4485.00.png [ 174.11 KiB | Viewed 394 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,110.00 dollars or +31.10 points, Emini ES ($ES_F) futures @

$1,375.00 dollars or +27.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $4,485.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1694 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

Investors Twiddle Their Thumbs, Wait For Jobs Attachment:

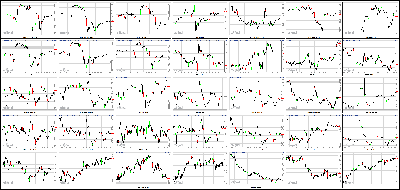

010914-Key-Price-Action-Markets.png [ 549.44 KiB | Viewed 325 times ]

010914-Key-Price-Action-Markets.png [ 549.44 KiB | Viewed 325 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Stocks were in a holding pattern Thursday as investors digested the latest economic data and awaited the government's key jobs report Friday.

The Dow Jones Industrial Average and Nasdaq dipped slightly, while the S&P 500 was flat. CNNMoney's new Tech 30 index was off more than 1%, dragged down by an 8% drop in wireless chip company ARM Holdings (ARMH) after Goldman Sachs downgraded the stock.

The Labor Department said Thursday that the number of people filing jobless claims for the first time last week fell to 330,000, a drop of 15,000 compared to the previous week and better than what economists were predicting.

On Friday, the government will release its all-important December jobs report.

Hopes for another strong month of job growth were raised Wednesday when payroll processor ADP reported that private-sector businesses added 238,000 workers in the month.

Economists surveyed by CNNMoney predict the report will show 193,000 jobs were added in December, consistent with the solid hiring during the last four months of 2013. The unemployment rate is expected to remain at 7%.

On Wednesday, the Federal Reserve released minutes from its December meeting saying it would proceed cautiously in scaling back its support of the economy.

The Fed has maintained that it will let economic data dictate the pace of its slowdown in bond purchases, so investors are trying to read the tea leaves in any economic reports.

On the corporate front, Macy's shares surged over 7% after the department store operator revealed cost-cutting plans late Wednesday that included laying off of 2,500 workers and closing five stores. The retailer maintained its financial forecasts. One trader on StockTwits noted the irony of a stock surging on layoff news.

"$M Nothing like job cuts to make analysts drool," quipped xtremezz.

Bed Bath & Beyond (BBBY, Fortune 500) tumbled more than 12% after the retailer reported quarterly earnings that missed estimates and was downgraded by an analyst at Credit Suisse.

But one trader saw the stock's drop as a glass half-full.

"Bad quarter from $BBBY but I wonder if this presents an opportunity," said TopGunFP. "Great operator and stock is cheap."

Family Dollar (FDO, Fortune 500) shares plunged after the budget-oriented retailer missed estimates for revenue and profits, reported a drop in same-store sales and lowered its guidance for the year.

"Another ugly show from Family Dollar," said StockTwits trader retail_guru. "Consistently over-estimating sales is $FDO hallmark."

Airline stocks took off, with United Continental Holdings (UAL, Fortune 500) soaring almost 7% after reporting an increase in a key revenue metric for December.

Delta (DAL, Fortune 500) rose over 4% and hit an all-time high.

One StockTwits user felt the momentum was justified.

"$DAL the weather is clearing up and blue skies ahead," said Weston.

Shares rose for Costco (COST, Fortune 500) after it reported an increase in same-store sales.

Twitter (TWTR), the second-worst performer in CNNMoney's Tech 30 index this year, dropped 4% after a bearish analyst report from Cowen & Co. Twitter's stock has fallen recently due to concerns about its valuation.

Aluminum producer Alcoa (AA, Fortune 500) finished the day lower after reaching a $384 agreement with the Securities and Exchange Commission relating to allegations that it bribed officials in Bahrain in its business dealings there. The stock fell further in after-hours trading after reporting earnings that came in slightly below estimates.

Most major European and Asian markets posted losses Thursday.

4:15 pm: [BRIEFING.COM] The major averages ended today's choppy session on a mixed note. The S&P 500 added less than a point while the Dow Jones Industrial Average (-0.1%) and Nasdaq (-0.2%) posted modest losses.

Equities displayed early strength, but sellers were quick to knock the indices off their opening highs. The Nasdaq outperformed out of the gate, but ultimately led the broader market into the red. Despite the late-morning weakness, the S&P 500 was able to find support at Wednesday's low where dip buyers stepped up and helped the index return to its flat line.

Individual sectors ended with an even split as five groups posted gains while the other five ended lower.

The early weakness took place as consumer discretionary (-0.1%) and technology (-0.6%) sectors slumped. The discretionary space was able to recover nearly all of its losses by the close but retailers were less fortunate. The SPDR S&P Retail ETF (XRT 85.81, -0.68) lost 0.8% after Bed Bath & Beyond (BBBY 69.75, -9.93) and Family Dollar (FDO 64.97, -1.37) reported disappointing earnings. One retailer, Macy's (M 55.80, +3.96), stood out with a 7.6% gain after boosting its guidance and announcing plans to close five stores and lay off 2,500 employees.

Elsewhere, the technology sector was pressured by several top components as Apple (AAPL 536.52, -6.94), Cisco Systems (CSCO 22.09, -0.20), and Google (GOOG 1130.24, -10.99) lost between 0.9% and 1.3%.

Other cyclical sectors were mixed as energy (-0.4%) and materials (-0.4%) lagged while financials (+0.3%) and industrials (+0.4%) outperformed. Notably, the industrial sector was underpinned by airlines after United Continental (UAL 43.80, +2.78) reported a 4.1% increase in December traffic. The stock spiked 6.8% while the broader Dow Jones Transportation Average advanced 1.0%.

Over on the countercyclical side, consumer staples (+0.4%), health care (+0.7%), and utilities (+0.6%) outperformed while telecom services (-1.9%) endured another rough session. The rate-sensitive sector widened its January loss to 3.8%.

Speaking of rates, they ended on their lows. The benchmark 10-yr yield fell three basis points to 2.97%.

Participation was on the light side as only 683 million shares changed hands on the floor of the New York Stock Exchange.

Today's economic data was limited to just two reports.

The weekly initial claims level fell to 330,000 from an upwardly revised 345,000 (from 339,000) while the Briefing.com consensus expected the claims level to fall to 338,000. The Labor Department stressed that the post-holiday period tends to be volatile as businesses dismiss their temporary work staff. Once the volatility is gone, we expect the initial claims level to stabilize at roughly its current level of 330,000. Normal volatility, however, could last another week or two. No states were estimated and the drop in claims was not attributed to the winter storm activity that began at the end of last week. Any effects of the storm will likely occur over the next week or two.

The December Challenger Job Cuts report pointed to a 6.0% decline in planned job cuts.

Tomorrow's data will also focus on jobs with December nonfarm payrolls set to be reported at 8:30 ET. Separately, the November Wholesale Inventories report will be released at 10:00 ET.

Russell 2000 -0.4% YTD

Nasdaq -0.5% YTD

S&P 500 -0.6% YTD

DJIA -0.8% YTD

3:35 pm: [BRIEFING.COM]

Commodities were mixed today with precious metals trading higher and crude oil and natural gas falling deeper into the red

Feb gold rose for the first time in four sessions after oscillating between positive and negative territory. It touched a session high of $1230.90 per ounce in early morning pit trade and dipped as low as $1222.80 per ounce later in the session. The yellow metal eventually settled with a 0.3% gain at $1229.30 per ounce

Mar silver dipped to a session low of $19.38 per ounce in late morning floor action but regained momentum and climbed back into positive territory. It settled 0.8% higher at $19.68 per ounce, just below its session high of $19.71 per ounce

Feb crude oil extended yesterday's losses despite opening up in the black. The energy component retreated from its session high of $92.84 per barrel and fell into negative territory by mid-morning pit action. It trended lower to a session low of $91.24 per barrel and settled with a 0.7% loss at $91.68 per barrel

Feb natural gas spent all of today's pit trade in the red. It popped to a session high of $4.19 per MMBtu following inventory data that showed a draw of 157 bcf when a draw of 155 bcf was anticipated but quickly lost momentum. It trended lower for the remainder of the session and settled with a 5.0% loss at $4.01 per MMBtu.

3:00 pm: [BRIEFING.COM] The S&P 500 sits right below its flat line with one hour remaining in the trading day. The first half the session saw some volatility as equity indices spent time on either side of their respective flat lines. Afternoon action, however, has been much more subdued.

Following today's closing bell, Alcoa (AA 10.63, -0.20) will report its fourth quarter results, but the earnings season will not kick into high gear until the final two weeks of the month. Although there aren't too many names on next week's schedule, several major financials will be reporting with JPMorgan Chase (JPM 58.70, -0.17) and Wells Fargo (WFC 46.06, +0.14) set to report their results before the opening bell on Tuesday.

2:30 pm: [BRIEFING.COM] Recent action saw the major averages slip back towards their late morning lows. The Nasdaq (-0.4%) continues to lag while the S&P 500 holds a more modest loss of 0.2%.

Earlier, investors received the latest weekly initial claims reading (330K actual versus 338K consensus) but the report was met with a muted reaction. However, tomorrow's December nonfarm payrolls report is expected to create some volatility in the markets. The Briefing.com consensus expects the reading to come in at 197,000.

Following the report, participants will keep a close eye on the bond market and a strong reading is likely to increase expectations for continued tapering from the Fed.

2:00 pm: [BRIEFING.COM] The major averages remain just below their flat lines as the quiet afternoon continues. Although the broader market has not moved much during the past hour, a pair of cyclical sectors-energy (-0.9%) and technology (-0.6%)-have slipped from their recent levels.

The energy sector has continued its steady, daylong, slide with Dow components Chevron (CVX 122.30, -0.99) and ExxonMobil (XOM 99.22, -1.52) dropping to fresh lows. The two hold respective losses of 0.8% and 1.5%.

Elsewhere, the technology sector has returned to its earlier low. The top sector component, Apple (AAPL 537.60, -5.86), is now lower by 1.1% after opening the session in the green.

1:25 pm: [BRIEFING.COM] Not much has changed since our midday update as equity indices continue to hover right below their flat lines.

Elsewhere, Treasuries have climbed back into positive territory following the recently-concluded $13 billion 30-yr bond reopening. The auction drew a yield of 3.899% with a solid bid/cover ratio of 2.57x. Indirect and direct bidders were active, taking 44.4% and 17.5% of the supply, respectively. As a result, primary dealers were left with just 38.1% of the supply. Following the auction, the benchmark 10-yr yield slipped two basis points to 2.980%.

With just one more session remaining in the first full week of 2014, the benchmark yield is on track to end little changed after finishing last week at 2.995%.

1:00 pm: [BRIEFING.COM] At midday, the major averages hover just below their flat lines with the Nasdaq (-0.2%) displaying the largest loss.

Equities began the day on an upbeat note but the early strength turned into late-morning weakness as the key indices headed into the red. Most cyclical sectors slumped along with the broader market while defensive groups held up well. At this juncture, individual sectors are mixed with five groups trading higher and five groups on the defensive.

Heavily-weighted consumer discretionary (-0.2%) and technology (-0.4%) were largely responsible for the morning reversal. Retailers pressured the discretionary sector after Bed Bath & Beyond (BBBY 69.21, -10.47) and Family Dollar (FDO 62.85, -3.49) reported disappointing earnings. The broader SPDR S&P Retail ETF (XRT 85.93, -0.56) is lower by 0.6% after seeing losses in excess of 1.0% earlier.

Elsewhere, the technology sector displayed early strength, but the subsequent slide coincided with Apple (AAPL 539.75, -3.71) giving up its opening gain. Chipmakers have not fared much better as the PHLX Semiconductor Index trades lower by 0.6%.

Other cyclical sectors trade in mixed fashion as financials (+0.1%) and industrials (+0.2%) outperform while the two commodity-related sectors-energy (-0.5%) and materials (-0.3%)-lag.

On the countercyclical side, consumer staples (+0.3%), health care (+0.5%), and utilities (+0.5%) outperform while the telecom services sector (-1.7%) endures yet another rough session. Including today's loss, the sector is lower by 3.5% in 2014. Treasuries trade little changed with the 10-yr yield at 2.99%.

Today's economic data was limited to just two reports.

The weekly initial claims level fell to 330,000 from an upwardly revised 345,000 (from 339,000) while the Briefing.com consensus expected the claims level to fall to 338,000. The Labor Department stressed that the post-holiday period tends to be volatile as businesses dismiss their temporary work staff. Once the volatility is gone, we expect the initial claims level to stabilize at roughly its current level of 330,000. Normal volatility, however, could last another week or two. No states were estimated and the drop in claims was not attributed to the winter storm activity that began at the end of last week. Any effects of the storm will likely occur over the next week or two.

The December Challenger Job Cuts report pointed to a 6.0% decline in planned job cuts.

12:30 pm: [BRIEFING.COM] Not much has changed since our last update as equity indices remain near their recent levels. Similarly, all six cyclical sectors have held their levels for the past 30 minutes while a pair of defensive groups inched higher.

The consumer staples (+0.2%) sector has climbed back to its opening high while health care (+0.4%) has continued its rebound after a brief test of its flat line. Elsewhere, the utilities sector continues to hold a modest gain of 0.3% while the telecom services space has spent the entire session in steady retreat, extending its loss to 1.7%.

12:00 pm: [BRIEFING.COM] The Dow, Nasdaq, and S&P 500 continue to trade with modest losses between 0.2% and 0.4% as seven sectors hover in the red.

As mentioned earlier, technology and consumer discretionary sectors were largely responsible for the morning reversal, but the remaining cyclical groups display losses as well. Financials and industrials are little changed while energy (-0.4%) and materials (-0.5%) lag.

Including today's decline, energy and materials are the two weakest cyclical groups so far in 2014. Crude oil has contributed to today's losses in energy, trading lower by 0.5% at $91.87/bbl. Elsewhere, the materials space has had to contend with losses among steelmakers as the Market Vectors Steel ETF (SLX 46.93, -0.60) trades lower by 1.3%.

11:30 am: [BRIEFING.COM] Equities have continued their slide and the Nasdaq, which outperformed during the opening minutes, is now leading the retreat. It is also worth mentioning that the major averages have been tracking the weakness of the USD/JPY carry pair, which trades near its session low at 104.60.

In recent months, the USD/JPY pair has been closely correlated with equity indices and continued yen weakness has translated into equity strength. However, the pair has been trapped in a narrow range over the past few sessions and today's yen strength appears to be posing a headwind to the equity market.

Elsewhere, Treasuries continue to hold modest gains with the 10-yr yield off one basis point at 2.99%.

10:55 am: [BRIEFING.COM] Unable to build on their opening gains, the major averages have slid into the red. At this juncture, individual sectors trade mostly lower with only two groups-health care (+0.1%) and utilities (+0.2%)-holding gains. Meanwhile, cyclical sectors trade broadly lower with heavily-weighted technology (-0.4%) and consumer discretionary (-0.5%) leading the retreat.

The tech sector displayed early strength, but experienced a swift reversal when its top component, Apple (AAPL 541.63, -1.83), and biotechnology (IBB 231.93, +0.35) surrendered their opening gains.

Elsewhere, the discretionary sector has been pressured by retailers after Bed Bath & Beyond (BBBY 69.72, -9.96) and Family Dollar (FDO 61.76, -4.58) reported disappointing earnings. The broader SPDR S&P Retail ETF (XRT 85.44, -1.05) is lower by 1.2%.

10:35 am: [BRIEFING.COM]

Commodities are mixed this morning. WTI crude oil, gold and silver sold off this morning on a rally in the dollar index

Feb crude oil rose as high as $92.93 earlier this morning, but dipped into the red momentarily a short while ago. Feb crude is now +0.1% at $92.40/barrel

Ahead of weekly EIA inventory data, natural gas was about 1.5% lower and has been in the red the whole day so far

Following the inventory data, Feb natural gas rallied higher, but remained in the red. Feb nat gas is now -1.3% at $4.16/MMBtu

After selling off this morning, gold and silver are mixed. Feb gold is now +0.1% at $1226.20/oz, Mar silver is -0.3% at $19.49/oz

10:00 am: [BRIEFING.COM] Equity indices have taken a step back from their opening highs but they remain in positive territory.

Seven of ten sectors trade with gains while consumer discretionary (-0.1%), energy (-0.1%), and telecom services (-0.7%) hover in the red. On the upside, the industrial sector (+0.4%) is among the leaders as transports display considerable strength.

The Dow Jones Transportation Average trades higher by 1.1% with airlines providing support. Delta Airlines (DAL 31.37, +1.57) and United Continental (UAL 45.75, +4.73) hold respective gains of 5.1% and 11.4% after United reported a 4.1% increase in December traffic.

9:45 am: [BRIEFING.COM] As expected, the major averages began the session on an upbeat note with the Nasdaq (+0.2%) leading the early charge. The tech-heavy index has drawn strength from a pair of top components as Apple (AAPL 545.68, +2.22) and Amazon.com (AMZN 406.45, +4.53) hold respective gains of 0.4% and 1.1%.

Biotechnology has also factored into the early outperformance of the Nasdaq. The iShares Nasdaq Biotechnology ETF (IBB 234.40, +2.82) is higher by 1.2% while the health care sector trades ahead of the remaining groups with a gain of 0.5%.

Treasuries hold slim gains with the benchmark 10-yr yield off one basis point at 2.98%.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: +3.90. Nasdaq futures vs fair value: +8.20. The major averages are expected to register opening gains as the S&P 500 will look to avoid posting its second consecutive loss. The S&P 500 futures trade four points above fair value.

Earlier, it was reported that weekly initial claims fell to 330,000 from an upwardly revised 345,000 (from 339,000). The Briefing.com consensus expected the initial claims level to fall to 338,000. The Labor Department stressed that the post-holiday period tends to be volatile as businesses dismiss their temporary work staff. Once the volatility is gone, we expect the initial claims level to stabilize at roughly its current level of 330,000. Normal volatility, however, could last another week or two.

Turning the focus to quarterly results, a pair of retailers, Bed Bath & Beyond (BBBY 72.70, -6.98) and Family Dollar (FDO 61.11, -5.23), are under pressure in pre-market action after missing earnings estimates. Another retailer, Macy's (M 55.05, +3.21), is on track to begin the session at a fresh all time high after boosting its guidance and announcing plans to close five stores and lay off 2,500 employees.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: +4.30. Nasdaq futures vs fair value: +9.20. The S&P 500 futures hover four points above fair value.

Major Asian indices ended lower across the board with Japan's Nikkei (-1.5%) pacing the slide. Economic data out of China was in focus as CPI ticked up 0.3% month-over-month (0.4% forecast, -0.1% prior) while the year-over-year reading reflected an increase of 2.5% (2.7% expected, 3.0% last). Also of note, PPI fell 1.4% year-over-year (-1.3% forecast, -1.4% previous). Elsewhere, Australia's building approvals fell 1.5% month-over-month (-1.0% consensus, -1.6% previous) while retail sales increased 0.7% (0.3% forecast, 0.5% prior). New Zealand's building consents rose 11.1% month-over-month (-0.6% previous) and the ANZ Commodity Price Index increased 1.0% month-over-month (-0.3% last). Lastly, The Bank of Korea held its key interest rate steady at 2.50%, as expected.

Japan's Nikkei settled lower by 1.5% after spending the entire session in the red as heavyweight names lagged. Fast Retailing, FANUC, and Furukawa lost between 2.8% and 3.8%. Sony was a notable outperformer, gaining 3.8%.

Hong Kong's Hang Seng lost 0.9% as consumer names lagged. Belle International and Want Want China Holdings fell 4.2% and 2.0%, respectively. On the upside, utility provider China Resources Power Holdings gained 3.6%.

China's Shanghai Composite slid 0.8% despite holding a modest gain through the first half of the session. Industrial & Commercial Bank of China fell 1.1%.

Core European indices trade little changed while markets in Italy (+1.3%) and Spain (+0.9%) outperform. Investors received several economic data points. The European Central Bank held its key interest rate steady at 0.25%, as expected. Eurozone Consumer Confidence improved to -14.0 from -15.4, as expected. Separately, Business and Consumer Survey rose to 100.0 from 98.4 (99.1 expected). Elsewhere, the Bank of England held its key interest rate and purchasing program steady at their respective 0.50% and GBP375 billion, as expected. Separately, the trade deficit narrowed to GBP9.44 billion from GBP9.65 billion (GBP9.45 billion consensus). Germany's industrial production rose 1.9% month-over-month (1.5% expected, -1.2% prior) and French trade deficit widened to EUR5.70 billion from EUR4.80 billion (EUR4.60 billion forecast).

Among news of note, the deputy leader of Spain's People's Party, Maria Dolores de Cospedal, said the country may beat its 0.7% 2014 GDP forecast.

In France, the CAC is lower by 0.1% as consumer names lag. Danone, L'Oreal, and LVMH Moet Hennessy Louis Vuitton are down between 0.9% and 1.7%. Medical equipment supplier Essilor International is the top performing name, up 2.4%.

Great Britain's FTSE is higher by 0.2%. Tullow Oil is among the leaders, trading higher by 3.1%. Morrison Supermarkets is lower by 7.6% after saying sales during the holiday period were down 1.9% excluding fuel. Peer J Sainsbury trades down 2.4%.

Germany's DAX holds a modest gain of 0.2% as financials lead. Deutsche Boerse and Commerzbank are both up near 2.4%. Chemical manufacturers BASF and Lanxess lag with respective losses of 0.7% and 1.0%.

8:33 am: [BRIEFING.COM] S&P futures vs fair value: +3.80. Nasdaq futures vs fair value: +10.70. The S&P 500 futures have slipped from their highs, but continue to hold a four-point gain against fair value.

The latest weekly initial jobless claims count totaled 330,000, which was lower than the 338,000 that had been expected by the Briefing.com consensus. Today's tally was below the revised prior week count of 345,000 (from 339,000). As for continuing claims, they rose to 2.865 million from 2.815 million.

7:55 am: [BRIEFING.COM] S&P futures vs fair value: +5.30. Nasdaq futures vs fair value: +10.70. U.S. equity futures hover near their pre-market highs with the S&P 500 futures up five points against fair value.

Reviewing overnight developments:

Asian markets ended broadly lower. China's Shanghai Composite -0.8%, Hong Kong's Hang Seng -0.9%, and Japan's Nikkei -1.5%.

Investors received several economic data points:

China's CPI ticked up 0.3% month-over-month (0.4% forecast, -0.1% prior) while the year-over-year reading reflected an increase of 2.5% (2.7% expected, 3.0% last). Also of note, PPI fell 1.4% year-over-year (-1.3% forecast, -1.4% previous).

Australia's building approvals fell 1.5% month-over-month (-1.0% consensus, -1.6% previous) while retail sales increased 0.7% (0.3% forecast, 0.5% prior).

New Zealand's building consents rose 11.1% month-over-month (-0.6% previous) and the ANZ Commodity Price Index increased 1.0% month-over-month (-0.3% last).

The Bank of Korea held its key interest rate steady at 2.50%, as expected.

In news:

Bank of Japan member Sayuri Shirai said reaching the 2.0% inflation target may take longer than previously expected. Ms. Shirai also said the central bank could ease more if needed.

Major European indices hold modest gains while peripheral indices outperform. France's CAC +0.1%, Great Britain's FTSE +0.2%, and Germany's DAX +0.3%. Elsewhere, Italy's MIB +1.3% and Spain's IBEX +1.2%.

In economic data:

The European Central Bank held its key interest rate steady at 0.25%, as expected. Eurozone Consumer Confidence improved to -14.0 from -15.4, as expected. Separately, Business and Consumer Survey rose to 100.0 from 98.4 (99.1 expected).

Germany's industrial production rose 1.9% month-over-month (1.5% expected, -1.2% prior).

The Bank of England held its key interest rate and purchasing program steady at their respective 0.50% and GBP375 billion, as expected. Separately, the trade deficit narrowed to GBP9.44 billion from GBP9.65 billion (GBP9.45 billion consensus).

French trade deficit widened to EUR5.70 billion from EUR4.80 billion (EUR4.60 billion forecast).

Among news of note:

In Spain, deputy leader of the People's Party, Maria Dolores de Cospedal, said the country may beat its 0.7% 2014 GDP forecast.

In U.S. corporate news:

Bed Bath & Beyond (BBBY 71.96, -7.72): -9.7% after missing on earnings and lowering its fourth quarter earnings guidance below consensus.

Family Dollar (FDO 60.55, -5.79): -8.7% following its bottom-line miss on in-line revenue. The company guided second quarter earnings below consensus and lowered its full-year 2014 guidance below consensus.

Macy's (M 55.50, +3.66): +7.1% after boosting its guidance and announcing plans to close five stores and lay off 2,500 employees.

McDonald's (MCD 96.81, +1.40): +1.5% after Morgan Stanley upgraded the stock to 'Overweight' from 'Equal-Weight.'

The December Challenger Job Cuts report pointed to a 6.0% decline in planned job cuts.

Weekly initial claims will be reported at 8:30 ET.

6:07 am: [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +13.00.

6:00 am: [BRIEFING.COM] Nikkei...15880.33...-241.10...-1.50%. Hang Seng...22787.33...-209.30...-0.90%.

6:00 am: [BRIEFING.COM] FTSE...6744.17...+22.30...+0.30%. DAX...9541.77...+43.90...+0.40%.

Gold Rises Before Jobs Data as Investors Weigh Demand, Tapering By Phoebe Sedgman Jan 9, 2014 10:35 PM ET

Gold climbed before U.S. jobs data as investors weighed the outlook for physical demand against speculation that the Federal Reserve may make further cuts to stimulus. Silver pared the biggest weekly loss since November.

Bullion for immediate delivery rose as much as 0.6 percent to $1,235.80 an ounce and traded at $1,233.95 at 11:31 a.m. in Singapore. Prices, which fell 0.2 percent earlier, ended at $1,237.01 last week. Gold for February delivery rose 0.3 percent to $1,233.30 on the Comex in New York, paring a weekly decline.

Minutes of the Fed’s December meeting released this week showed that some officials saw diminishing economic benefits from purchasing debt. The Fed said Dec. 18 that it will reduce its monthly bond purchases to $75 billion from $85 billion, citing improvements in the labor market. A report today may show employers added more jobs in 2013 than at any point in the past eight years, even as payrolls declined from a month earlier.

“The performance of the U.S. economy is going to drive U.S. monetary policy, so employment numbers are very closely watched,” said Victor Thianpiriya, an analyst at Australia & New Zealand Banking Group Ltd. in Singapore. “The only thing supporting the market at the moment is Chinese demand.”

The premium for gold for immediate delivery in China rose to $31.21 an ounce on Jan. 7, the highest in more than two weeks, and was at $15.3013 today. While premiums and volumes on the Shanghai Gold Exchange have eased in the past couple of days, they are still “decent,” UBS AG said in a report yesterday.

Employment GainsThe Labor Department report may show nonfarm payrolls rose 197,000 last month, according to the median estimate in a Bloomberg survey. While that’s down from 203,000 a month earlier, it would bring the total for the year to 2.27 million, the most since 2005. A report from the ADP Research Institute on Jan. 8 showed companies added 238,000 workers in December, the biggest increase since November 2012.

The Fed minutes didn’t describe a detailed schedule for asset-purchase reductions. The central bank will “continue to do, probably at each meeting, a measured reduction” in the pace of purchases, Chairman Ben S. Bernanke said last month.

Silver for immediate delivery gained 0.4 percent to $19.654 an ounce. Prices are still 2.5 percent lower this week, heading for the biggest drop since the period to Nov. 22.

Platinum gained 0.2 percent to $1,420.90 an ounce, heading for a third weekly advance. Palladium was little changed at $737.43 an ounce, also set for a third weekly gain.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage