Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

110813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2045.00.png [ 83.85 KiB | Viewed 343 times ]

110813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2045.00.png [ 83.85 KiB | Viewed 343 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$400.00 dollars or +4.00 points, Emini ES ($ES_F) futures @

$1,125.00 dollars or +22.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$520.00 dollars or +5.20 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $2,045.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=123&t=1646 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=223&t=2061 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

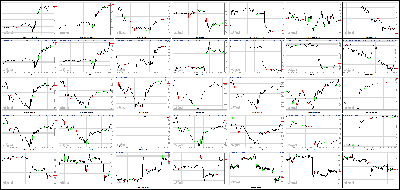

Hooray! Stocks Pop On Solid Jobs Report Attachment:

110813-Key-Price-Action-Markets.png [ 510.75 KiB | Viewed 314 times ]

110813-Key-Price-Action-Markets.png [ 510.75 KiB | Viewed 314 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Good news is good news! Stocks bounced back Friday thanks to a much better-than-expected jobs report.

The Dow Jones industrial average rose more than 167 points, or 1%, to end at another record closing high. The S&P 500 gained 1.3% and the Nasdaq added 1.6%. This comes one day after stocks tumbled following a surprise interest rate cut by the European Central Bank and stronger than expected U.S. economic reports.

The S&P 500 and the Dow both ended higher for a fifth straight week. The Nasdaq, despite Friday's big gains, was still down for the week.

The economy added 204,000 jobs in October, according to the Labor Department. That is higher than the 120,000 estimate of economists surveyed by CNNMoney. The gains came despite a partial government shutdown in October, which many economists had feared would hurt the economy.

Separately, the Commerce Department said personal income rose 0.5% in September, while spending edged up 0.2%. But consumer sentiment was down in October, according to an index from Reuters and the University of Michigan.

Still, Friday's jobs report and other good economic news has revived speculation on when the Federal Reserve will begin scaling back, or tapering, its $85 billion per month bond buying program. Many market experts believe the Fed's stimulus is a key reason why stocks have surged this year.

But bond prices fell, with the yield on the 10-year Treasury note rising to 2.75%, from 2.61% Thursday. Bond prices and rates move in opposite directions. The spike in yields Friday could be another sign that the market believes the Fed will taper sooner rather than later.

Alan Levenson, an economist at T. Rowe Price Associates, said the jobs report increases the chance that the Fed could announce it will start to taper at its December meeting.

Yields surged earlier this summer on expectations the Fed would cut back its bond buying sometime this year. But not everyone believes the Fed will make a move next month. Hank Smith, chief investment officer at Haverford Trust, said many investors are still looking for tapering to begin early next year once a new Fed chairman is in place.

Current Fed chair Ben Bernanke's term is set to expire at the end of January. President Obama has nominated Fed vice chair Janet Yellen to replace him. She must still be confirmed by the Senate.

But even when the tapering process begins, monetary policy is likely to remain "extraordinarily accommodative," said Smith.

Stocks on the move: Twitter (TWTR) shares fell 7% on Friday, their second day of trading. Twitter shares closed at $44.90 on Thursday, a whopping 73% gain from its initial public offering price of $26 a share.

Some StockTwits users were quick to say I told you so.

"$TWTR Several of us warned bulls yesterday that the sell-off hadn't even started. Hope you listened," said BlackBerril.

Others were relieved that they stayed away from the highly-anticipated IPO.

"$TWTR Back to IPO price pretty soon. Whoever held back on buying is probably feeling good about now," said Sanjit69.

Still, some traders see Twitter, which is not yet profitable, as an attractive investment at the right price.

"$TWTR This stock has nothing but hopes and dreams. I do believe some of their dreams will come true, for now I stay out. Will buy in 20's," said Brwood6980.

Shares of the Gap (GPS, Fortune 500) jumped nearly 10% after the apparel retailer reported strong sales for October. That's a sharp contrast with Abercrombie & Fitch (ANF), which warned of weak sales earlier this week and shut down its lingerie business.

"Khakis are cool again in Oct after being uncool in Sep. $GPS," said bigelam.

Groupon (GRPN) shares rose despite disappointing earnings and a weak outlook. The daily deal site announced it was buying Korean site Ticket Monster from its top rival LivingSocial.

Walt Disney (DIS, Fortune 500) reported slightly better-than-expected earnings and sales. The stock rose on the news.

Tesla (TSLA) shares continued to fall Friday after a Model S caught fire after a crash Thursday in Tennessee. It's the third widely-reported fire involving one of the all-electric plug-in luxury cars in just two months. The stock has plunged more than 20% since it reported its latest quarterly results on Tuesday.

European markets ended mixed. The Paris stock market tumbled after Standard & Poor's downgraded France's credit rating. Asian markets chalked up big losses despite strong China trade data.

4:20 pm : Equities climbed throughout the session despite showing early signs of a potential continuation to yesterday's weakness. The S&P 500 advanced 1.3% while the Nasdaq and Russell 2000 outperformed with respective gains of 1.6% and 1.9%.

Before today's opening bell, it was announced that nonfarm payrolls increased by 204,000 in October (Briefing.com consensus 100,000). The immediate reaction was consistent with increased expectations of tapering sooner rather than later as bonds and futures fell to lows. However, equity futures returned into positive territory by the opening bell while Treasuries settled on their lows with the 10-yr yield up 15 basis points at 2.75%. The dollar also strengthened, sending the Dollar Index higher by 0.5% to 81.24.

Stocks rallied with the financial sector (+2.3%) paving the way after the group struggled to keep pace with the S&P earlier in the week. All major banks posted solid gains, and JPMorgan Chase (JPM 53.96, +2.31) surged 4.5%.

Other cyclical sectors also displayed strength, but only financials added more than 2.0%. Meanwhile, the materials space was the second-best performer (+1.8%) as steelmakers provided support. The Market Vectors Steel ETF (SLX 49.37, +0.81) gained 1.7%. Miners posted modest gains as the Market Vectors Gold Miners ETF (GDX 24.28, +0.14) added 0.6% despite weakness in gold. The yellow metal fell 1.8% to $1284.60 per troy ounce.

Elsewhere, the technology sector (+1.1%) was the only cyclical group unable finish ahead of the broader market as top components traded in mixed fashion. Apple (AAPL 520.56, +8.07) and Cisco Systems (CSCO 23.51, +0.40) gained 1.6% and 1.7%, respectively, while IBM (IBM 179.99, -0.01) and Intel (INTC 24.09, +0.03) ended little changed.

Yesterday, the Nasdaq was pressured by biotechnology and momentum names, but both groups displayed relative strength today. The iShares Nasdaq Biotechnology ETF (IBB 204.18, +6.36) climbed 3.2% while Priceline.com (PCLN 1073.20, +50.31) paced the gains among momentum names after beating on earnings.

Also of note, Twitter (TWTR 41.65, -3.25) endured a forgettable second-day of trading after Hudson Square initiated coverage of the stock with a 'Sell' rating. The social media stock tumbled 7.2%.

Trading volume was well above average as 823 million shares changed hands on the floor of the New York Stock Exchange.

Taking another look through today's data, with the exception of government, every sector reported positive payroll gains in October. That included a 44,400 increase in retail employees. It has been reported that retailers started hiring earlier than normal for the holiday season.

Private payrolls added 212,000 new jobs in October, up from 150,000 in September. That was the biggest monthly gain since February when 319,000 jobs were added. The consensus expected only 110,000 new private jobs.

The average workweek remained at 34.4 hours and hourly wages increased by 0.1%. Combined with the solid increase in private payrolls, aggregate wages increased 0.3%. That is enough to keep consumption growth moving ahead.

The unemployment rate increased to 7.3% in October from 7.2% in September, as expected.

Separately, the November University of Michigan Consumer Sentiment Index dropped to 72.0 in the preliminary reading from 73.2 in October. The Briefing.com consensus expected the index to increase to 75.0. With the government shutdown over and the economy returning to its normal, albeit weak, trends, it was expected that consumer sentiment would return to September (77.5) or August (82.1) levels.

There is no economic data scheduled to be reported on Monday.

Nasdaq +29.8% YTD

Russell 2000 +29.5% YTD

S&P 500 +24.2% YTD

DJIA +20.3% YTD

Week in Review: Stocks Test Record Highs

The major averages kicked off the week with modest gains as the S&P 500 added 0.4%. The Russell 2000 (+1.1%) outperformed, but its relative strength came after the small cap index struggled to keep pace with the prior week's advance in the broader market. Outside of the notable outperformance among small caps, the session unfolded in an uneventful fashion. Overseas markets did little to upset the state of affairs as Japan's Nikkei was closed for Culture Day while China's Shanghai Composite ended flat despite its Non-Manufacturing PMI rising to a 14-month high of 56.3 from 55.4. All ten sectors ended in the green, but only energy (+1.3%) and telecom services (+0.8%) posted gains in excess of 0.4%. Energy was responsible for pacing much of the advance as the sector rallied throughout the session. Meanwhile, crude oil ended little changed at $94.59 per barrel.

On Tuesday, the major averages ended on a mixed note as the S&P 500 shed 0.3% while the Nasdaq added 0.1%. Equities spent the entire session climbing off their early lows after weakness in Europe set the stage for a lower open. European indices hovered near their worst levels of the day at the outset of the U.S. session after the European Commission lowered its 2014 GDP forecast for the region to 1.1% from 1.2%. Similar to equities, core EU bonds also sold off as Germany's 10-yr yield added four basis points to 1.74% while the French 10-yr yield rose six basis points to 2.21%. Although stocks began the U.S. session in negative territory, the buy-the-dip trade was at work once again, fueling a day-long rebound. The tech-heavy Nasdaq was able to eke out a modest gain thanks to the outperformance of biotechnology as the iShares Nasdaq Biotechnology ETF rose 0.7%.

Wednesday saw the major averages register broad gains at the open, but only the Dow Jones Industrial Average (+0.8%) and S&P 500 (+0.4%) were able to end in positive territory while the Nasdaq (-0.2%) and Russell 2000 (-0.4%) posted modest losses. The Dow finished at a fresh record high of 15,746.63 as 27 of 30 components registered gains. Of those 27, twelve added at least 1.0%. Microsoft (MSFT 37.78, +0.28) was the top index performer, climbing 4.2% amid reports Ford (F 16.85, +0.30) Chief Executive Officer Alan Mullaly remains on the list of candidates hoping to replace outgoing CEO Steve Ballmer.

The major averages ended Thursday on their lows after opening gains turned into broad-based losses. The S&P 500 fell 1.3% while the Nasdaq underperformed with a decline of 1.9%. Prior to the open, the European Central Bank cut its key interest rate by 25 basis points to 0.25% after recent data suggested the price level is moving away from the ECB's inflation target. The rate cut fueled a surge in the dollar while also sparking a risk bid. However, the equity gains were capped after a better-than-expected headline Q3 GDP reading (2.8% versus 2.5% Briefing.com consensus) fostered renewed speculation about a potential tapering announcement coming sooner rather than later. The immediate reaction in Treasuries also reflected a 'taper on' trade as bonds sold off, sending the 10-yr yield from its low to a session high. However, Treasuries returned to their best levels of the day as weakness among equities redirected some flows into safe-haven assets. The 10-yr yield ended lower by four basis points at 2.61%.

DJ30 +167.80 NASDAQ +61.90 SP500 +23.46 NASDAQ Adv/Vol/Dec 1932/1.92 bln/642 NYSE Adv/Vol/Dec 1744/823.4 mln/1289

3:30 pm :

A rally in the dollar index on this morning's strong U.S. jobs data weighed on precious metals. It was reported that nonfarm payrolls increased by 204,000 in October, which was much higher than the 100,000 expected by the Briefing.com consensus

Dec gold slid below the $1300.00 per ounce level as the dollar index gained strength. The yellow metal fell from its session high of $1310.20 per ounce and touched a session low of $1280.50 per ounce in morning pit trade. Unable to gain momentum, it settled 1.8% lower at $1284.60 per ounce, booking a 2.2% loss for the week

Dec silver also traded lower after slipping from its session high of $21.78 per ounce set moments after pit trade opened. It fell as low as $21.25 per ounce and eventually settled at $21.32 per ounce, or 1.6% lower. Today's decline brought losses for the week to 2.4%

Dec crude oil chopped around in positive territory for most of today's pit trade despite the stronger dollar index. Numerous reports indicated that the U.S. is close to reaching a nuclear deal with Iran. The energy component touched a session high of $94.92 per barrel and closed with a 0.4% gain at $94.58 per barrel, ending the week just three cents below last Friday's closing price

Dec natural gas extended gains for a fourth consecutive session as it advanced to a session high of $3.59 per MMBtu in late morning floor action. It eventually settled 1.1% higher at $3.56 per MMBtu, booking a 1.4% gain for the week.

DJ30 +117.23 NASDAQ +52.62 SP500 +17.38 NASDAQ Adv/Vol/Dec 1874/1614.1 mln/673 NYSE Adv/Vol/Dec 1585/530 mln/1445

3:00 pm : With one hour remaining in today's session, the Dow, Nasdaq, and S&P 500 sit on their highs while the Russell 2000 hovers a couple points below its best level of the day.

Investors received the last heavy batch of Q3 earnings this week, and while roughly 50 S&P 500 components have yet to report their results, the remaining announcements will be more spread out.

Only eight companies are scheduled to report their results ahead of Monday's opening bell with Cooper Tires (CTB 26.48, -0.42) headlining the list.DJ30 +109.62 NASDAQ +53.98 SP500 +18.11 NASDAQ Adv/Vol/Dec 1898/1.46 bln/652 NYSE Adv/Vol/Dec 1574/482.8 mln/1435

2:30 pm : The S&P 500 has continued its climb, and now trades just five points below yesterday's opening level.

This week was busy in terms of economic data with participants receiving the advance Q3 GDP report (2.8% versus 1.9% Briefing.com consensus), October nonfarm payrolls (204K versus 100K consensus), and the preliminary November Michigan Sentiment Survey (72.0 versus 75.3 consensus).

However, next week will feature just a handful of economic releases with Thursday's September trade balance report and Friday's reading on October industrial production headlining the releases.DJ30 +18.28 NASDAQ +56.32 SP500 +108.65 NASDAQ Adv/Vol/Dec 1909/1.37 bln/629 NYSE Adv/Vol/Dec 1591/451.2 mln/1413

2:00 pm : Recent action saw the S&P 500 climb to a fresh high as the index continues retracing yesterday's slide. Meanwhile, Treasuries remain pinned to their lows with 10-yr yield up 15 basis points at 2.75%.

In addition to sparking a sell off in Treasuries, today's jobs report boosted the greenback, sending the Dollar Index higher by 0.5% to 81.27. Today's dollar rally has weighed on all major currencies with the yen seeing heaviest pressure. Currently, USDJPY is higher by 85 pips just above 99.00.DJ30 +101.32 NASDAQ +56.64 SP500 +17.62 NASDAQ Adv/Vol/Dec 1888/1.29 bln/641 NYSE Adv/Vol/Dec 1591/424.9 mln/1404

1:30 pm : The buy-the-dip mentality that has factored so prominently in the market's run to a new record high appears to be alive and well today. The Russell 2000, Nasdaq Composite, and S&P 400 Midcap Index were yesterday's worst-performing averages with losses of 1.8%, 1.9%, and 1.8%, respectively.

Today those same averages are leading the gains. Small caps in particular are catching a nice, buy-the-dip bid as evidenced by the 1.8% gain in the Russell 2000. The Nasdaq Composite is up 1.4% and the S&P 400 Midcap Index is up 1.3%.

The major averages continue to look good at this juncture as they are all trading near their best levels of the session. Participants will be watching keenly to see if the bullish bias holds or, if like yesterday, sellers show up and precipitate a disappointing finish.

The S&P financials sector (+1.8%) has offered a supportive foundation thus far today and should remain a focal point as the trading day progresses. DJ30 +94.14 NASDAQ +56.36 SP500 +17.01 NASDAQ Adv/Vol/Dec 1905/1.18 bln/618 NYSE Adv/Vol/Dec 1592/385 mln/1400

12:55 pm : Equity indices sport solid midday gains as they rebound from yesterday's broad weakness. The Nasdaq and Russell 2000, which lagged on Thursday, have paced the first-half rally with respective advances of 1.4% and 1.8%.

Prior to the opening bell, it was reported that nonfarm payrolls increased by 204,000 in October, which was much higher than the 100,000 expected by the Briefing.com consensus. The immediate reaction was consistent with increased expectations of tapering in the near-term as bonds and futures fell to lows. However, futures erased their losses by the opening bell while Treasuries continued their retreat. At this juncture, the 10-yr yield is up 15 basis points at 2.75%, its highest level since mid-September.

Stocks have been climbing steadily since the open with cyclical sectors pacing the rally. The financial sector underperformed throughout the week, but is higher by 1.8% today with JPMorgan Chase (JPM 53.50, +1.85) trading ahead of the other majors.

Elsewhere, four of the remaining five cyclical groups sport gains of at least 1.0% while technology (+0.7%) lags. Gains among chipmakers have been limited by reports suggesting Taiwan Semiconductor (TSM 17.98, -0.15) could see weaker orders during the fourth quarter.

Also of note, the health care sector (+1.2%) is the only countercyclical group trading in positive territory with significant support coming from biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 203.90, +6.08) trades up 3.1%.

Taking another look through today's data, with the exception of government, every sector reported positive payroll gains in October. That included a 44,400 increase in retail employees. It has been reported that retailers started hiring earlier than normal for the holiday season.

Private payrolls added 212,000 new jobs in October, up from 150,000 in September. That was the biggest monthly gain since February when 319,000 jobs were added. The consensus expected only 110,000 new private jobs.

The average workweek remained at 34.4 hours and hourly wages increased by 0.1%. Combined with the solid increase in private payrolls, aggregate wages increased 0.3%. That is enough to keep consumption growth moving ahead.

The unemployment rate increased to 7.3% in October from 7.2% in September, as expected.

Separately, the November University of Michigan Consumer Sentiment Index dropped to 72.0 in the preliminary reading from 73.2 in October. The Briefing.com consensus expected the index to increase to 75.0. With the government shutdown over and the economy returning to its normal, albeit weak, trends, it was expected that consumer sentiment would return to September (77.5) or August (82.1) levels.DJ30 +86.82 NASDAQ +52.95 SP500 +15.57 NASDAQ Adv/Vol/Dec 1881/1.09 bln/622 NYSE Adv/Vol/Dec 1540/356.7 mln/1438

12:30 pm : The S&P 500 (+0.9%) has climbed to a fresh high as cyclical sectors continue building on their gains. Interestingly, the technology sector (+0.8%) trails the remaining growth-sensitive groups even as the tech-heavy Nasdaq (+1.4%) outpaces the broader market.

Chipmakers have prevented the tech sector from rallying alongside other cyclical groups as Taiwan Semiconductor (TSM 17.98, -0.15) trades lower by 0.8% amid reports suggesting the company could see weaker orders during the fourth quarter. Meanwhile, the broader PHLX Semiconductor Index is higher by 0.8%.DJ30 +95.30 NASDAQ +54.29 SP500 +16.28 NASDAQ Adv/Vol/Dec 1857/1.02 bln/626 NYSE Adv/Vol/Dec 1524/334.9 mln/1432

12:05 pm : Stocks remain near their highs with small caps seeing the strongest buying interest (Russell 2000 +1.7%). Meanwhile, the S&P 500 trades higher by 0.9%, which puts the index on track to end the week little changed.

The financial sector (+1.6%) has led from the start, and remains ahead of the other nine groups. The discretionary space (+1.1%) also holds a gain of at least 1.0% while the remaining cyclical sectors are up between 0.7% and 0.9%.

Among countercyclical groups, only the health care sector trades in positive territory (+1.0%) while consumer staples (-0.3%), utilities (-0.7%), and telecom services (-0.9%) lag. Health care has been able to outperform the remaining defensive groups amid significant strength in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 204.00, +6.18) is higher by 3.1%.DJ30 +81.65 NASDAQ +52.60 SP500 +14.86 NASDAQ Adv/Vol/Dec 1851/923.5 mln/616 NYSE Adv/Vol/Dec 1523/305.8 mln/1442

11:30 am : The major averages hover near their highs with the Russell 2000 sporting the largest gain (+1.5%) while the Dow (+0.5%) lags. Although the price-weighted index trails the remaining indices, it is the only average on track to post a weekly gain (+0.3%).

Even though the Dow lags, 21 of 30 index components sport gains with nine listing trading higher by at least 1.0%. However, the second-largest Dow member, IBM (177.98, -2.02), weighs with a loss of 1.1%.

With stocks hovering near their highs, the CBOE Volatility Index (VIX 13.52, -0.39) is lower by 2.8%. Notably, the near-term volatility measure has held below 15.00% since mid-October.DJ30 +73.31 NASDAQ +44.71 SP500 +12.59 NASDAQ Adv/Vol/Dec 1785/803.5 mln/663 NYSE Adv/Vol/Dec 1453/266.8 mln/1499

11:00 am : Equity indices have continued their rally with some of yesterday's weakest performers providing leadership. The Russell 2000 and Nasdaq paced the Thursday decline, but the two indices hold respective gains of 1.3% and 1.0%. Furthermore, thanks to its rebound, the Russell is now down just 0.2% for the week.

Elsewhere, the broader market is following in the footsteps of the financial sector, which trades higher by 1.7%. Bank shares lagged throughout the week, but today's notable outperformance has turned the sector into this week's top performer.

Also of note, Treasuries remain pinned to the mat with the 10-yr yield up 15 basis points at 2.75%, its highest level since late September.DJ30 +89.71 NASDAQ +41.63 SP500 +13.12 NASDAQ Adv/Vol/Dec 1750/661.5 mln/668 NYSE Adv/Vol/Dec 1401/226.2 mln/1512

10:30 am :

Commodities are showing some volatility this morning, which began after the jobs report came out

Following the jobs numbers, gold and silver futures dropped sharply lower, with gold falling below the $1300/oz level, while the dollar index spiked higher

Dec gold is now -2.1% at $1281.50/oz, while Dec silver is -1.5% at $21.33/oz

Crude oil fell below $94/barrel in early morning electronic trading, but climbed off that LoD throughout morning trade

Dec crude hit levels as high as $94.71/barrel and is now +0.1% at $94.27/barrel

Natural gas futures have been in positive territory the whole day so far and rose as high as $3.58/MMBtu. Dec nat gas is now +1.1% at $3.56/MMBtu

DJ30 +82.90 NASDAQ +41.79 SP500 +11.86 NASDAQ Adv/Vol/Dec 1668/498.8 mln/682 NYSE Adv/Vol/Dec 1335/180 mln/1546

10:00 am : The major averages remain in positive territory as the Nasdaq (+0.5%) and Russell 2000 (+0.5%) lead. Meanwhile, the S&P 500 trades higher by 0.2% as seven of ten sectors hold gains between 0.1% (technology) and 1.1% (financials).

Just released, the preliminary University of Michigan Consumer Sentiment report for November decreased to 72.0 from the October reading of 73.2. The Briefing.com consensus expected the reading to improve to 75.3.DJ30 +14.35 NASDAQ +19.37 SP500 +3.86 NASDAQ Adv/Vol/Dec 1508/283.3 mln/756 NYSE Adv/Vol/Dec 1184/113.4 mln/1623

09:45 am : Stocks climbed out of the gate with the Nasdaq (+0.4%) leading the advance after plunging 1.9% yesterday. The tech-heavy index has received some early support from a handful of momentum names like Facebook (FB 47.88, +0.32) and Priceline.com (PCLN 1058.08, +35.19) with Priceline seeing additional strength after beating on earnings and revenue.

Biotechnology has also provided a measure of support to the index as the iShares Nasdaq Biotechnology ETF (IBB 200.57, +2.75) trades higher by 1.5%.

Although stocks trade modestly higher, Treasuries remain on their lows after sliding in reaction to a better-than-expected nonfarm payrolls report. The 10-yr yield is higher by 13 basis points at 2.74%.DJ30 +2.37 NASDAQ +12.06 SP500 +1.93 NASDAQ Adv/Vol/Dec 1239/163.2 mln/932 NYSE Adv/Vol/Dec 1042/77.8 mln/1705

09:16 am : [BRIEFING.COM] S&P futures vs fair value: +4.20. Nasdaq futures vs fair value: +13.50. Equities are expected to begin today's session just north of their flat lines as the S&P 500 futures hover four points above fair value. Index futures held gains through overnight action, but fell to lows in reaction to an October nonfarm payrolls report, which came in well ahead of estimates with a headline reading of 204,000 (Briefing.com consensus 100,000).

Although the report appears strong at first glance, there are some notable areas of weakness. Namely, the labor force participation rate dropped 0.4 to 62.8%; the unemployment rate rose to 7.3% from 7.2%; and the U-6 unemployment rate, which also accounts for marginally attached workers and the total employed part-time for economic reasons, jumped to 13.8% from 13.6%.

Despite the soft spots in the data, the Dollar rallied and Treasuries sold off in a reaction consistent with increased tapering expectations. The Dollar Index is higher by 0.4% at 81.17 while Treasuries hover near their lows with the 10-yr yield up 11 basis points at 2.71%.

The preliminary reading of the November Michigan Sentiment Survey will be released at 9:55 ET.

08:58 am : [BRIEFING.COM] S&P futures vs fair value: -1.30. Nasdaq futures vs fair value: +4.70. The S&P 500 futures trade lower by 0.2% after sliding into the red in reaction to a better-than-expected headline nonfarm payrolls number.

It was a sea of red across Asia as all of the major bourses saw losses. China's Shanghai Composite (-1.1%) slid despite the latest trade data from the Middle Kingdom showing a surplus of $31.1 billion ($23.5 billion expected, $15.2 billion previous) as exports jumped 5.6% year-over-year (1.5% expected). The selloff comes following yesterday's weakness on Wall Street and as traders remain jittery ahead of this weekend's Third Plenum of Communist Party policy makers, which will likely produce an economic blueprint for the next decade. Hong Kong's Hang Seng gave up 0.6%. The latest minutes from the Reserve Bank of Australia showed the central bank downgraded its 2014 growth forecast to 2%-3% from 2.5%-3.5%; however, the ASX (-0.4%) only saw modest losses. Elsewhere, Japan's Nikkei (-1.0%) managed to recover some of yesterday's losses that developed in the futures market as trade was down as much as 3.0%. Data from the rest of the region was limited to Malaysia's trade balance, which posted a wider than anticipated surplus of MYR8.7 billion (MYR5.0 billion expected, MYR7.1 billion previous).

In Japan, the Nikkei lost 1.0% as trade slid to a one-month low. Heavyweights like Fast Retailing and Softbank weight, posting losses of 3.6% and 2.7%, respectively.

Hong Kong's Hang Seng slid 0.6% as trade avoided its lowest close in two months. Energy names were pressured as Sinopec lost 1.3% and Cnooc slipped 1.0%. Meanwhile, real estate names provided support as Sun Hung Kai Properties and Henderson Land Development tacked on 0.5% and 0.2%, respectively.

In China, the Shanghai Composite settled lower by 1.1% with trade ending at its worst level in more than two months. Property stocks were weak after Shanghai announced it would require a 70% down payment (60% previous) from second-home buyers. China Vanke and Poly Real Estate both surrendered 1.1%.

Major European indices hover near their lows as yesterday's weakness, which developed after the ECB rate cut, continues. Among news of note, Standard & Poor's lowered the credit rating of France to 'AA' from 'AA+.' The rating agency cited subpar economic growth, high unemployment, and government spending limitations as the reasons for the downgrade. In regional economic data, Germany's trade surplus expanded to EUR18.80 billion from EUR15.80 billion (EUR15.50 billion forecast). Great Britain's trade deficit narrowed to GBP9.82 billion from GBP9.56 billion (GBP9.20 billion prior). France reported a government budget deficit of EUR80.80 billion (-EUR90.80 billion expected, -EUR93.60 billion prior) while the trade deficit widened to EUR5.80 billion from EUR5.10 billion (-EUR4.80 billion last). Separately, industrial production slipped 0.5% month-over-month (0.1% expected, 0.7% previous).

Great Britain's FTSE is lower by 0.5% as miners lag. Antofagasta, Randgold Resources, and Vedanta Resources are all down between 2.2% and 2.6%. On the upside, International Consolidated Airlines Group and Rolls Royce Holdings outperform with respective gains of 5.3% and 3.2% after both issued upbeat guidance.

Germany's DAX holds a loss of 0.7% with HeidelbergCement leading to the downside (-1.8%). Meanwhile, Adidas sits among top performers with a gain of 2.2%.

In France, the CAC trades down 1.2% as 35 of 40 components hover in the red. Banks lag with Credit Agricole and Societe Generale down 1.5% and 3.2%, respectively. ArcelorMittal leads with an advance of 2.5% after boosting its guidance.

08:34 am : [BRIEFING.COM] S&P futures vs fair value: -4.90. Nasdaq futures vs fair value: -5.30. The S&P 500 futures and Treasuries tumbled to their lows in reaction to a better-than-expected October jobs report. The S&P 500 futures trade lower by 0.4% while the 10-yr yield is higher by 11 basis points at 2.72%.

October nonfarm payrolls came in at 204K versus the 100K expected by the Briefing.com consensus. Nonfarm private payrolls added 212K against the 110K consensus. The unemployment rate ticked up to 7.3%, as expected by the Briefing.com consensus.

Hourly earnings ticked up 0.1% while the Briefing.com consensus expected an increase of 0.2%. Average workweek was reported at 34.4, in-line with the consensus expectations.

September personal income rose 0.5%, above the increase of 0.2% expected by the Briefing.com consensus. Meanwhile, personal spending rose 0.2%, in-line with the Briefing.com consensus.

Lastly, core PCE prices ticked up 0.1%, as expected.

08:00 am : [BRIEFING.COM] S&P futures vs fair value: +3.10. Nasdaq futures vs fair value: +8.00. U.S. equity futures have slipped from their highs, but the S&P 500 futures continue to hover just above their flat line. Some additional volatility is expected around 8:30 ET when the October nonfarm payrolls report crosses the wires. The Briefing.com consensus expects the reading to come in at 100,000 while the unemployment rate is expected to tick up to 7.3% from 7.2%.

Reviewing overnight developments:

Asian markets ended broadly lower. Hong Kong's Hang Seng -0.6%, Japan's Nikkei -1.0%, and China's Shanghai Composite -1.1%.

Economic data was limited:

China reported a trade surplus of $31.10 billion ($23.90 billion forecast, $15.20 billion prior) as exports grew at 5.6% (3.2% expected, -0.3% prior) while imports increased 7.6% (8.5% forecast, 7.4% last).

In news:

Former People's Bank of China adviser Li Daokui said he expects China's economic growth to slow in the next two to three years.

Major European indices hover near their lows. Great Britain's FTSE -0.5%, Germany's DAX -0.7%, and France's CAC -1.0%.

In regional economic data:

Germany's trade surplus expanded to EUR18.80 billion from EUR15.80 billion (EUR15.50 billion forecast).

Great Britain's trade deficit narrowed to GBP9.82 billion from GBP9.56 billion (GBP9.20 billion prior).

France reported a government budget deficit of EUR80.80 billion (-EUR90.80 billion expected, -EUR93.60 billion prior) while the trade deficit widened to EUR5.80 billion from EUR5.10 billion (-EUR4.80 billion last). Separately, industrial production slipped 0.5% month-over-month (0.1% expected, 0.7% previous).

Looking at news:

Standard & Poor's lowered the credit rating of France to 'AA' from 'AA+.' The rating agency cited subpar economic growth, high unemployment, and government spending limitations as the reasons for the downgrade.

In U.S. corporate news:

Molycorp (MCP 4.95, +0.19): +4.0% after reporting a bottom-line beat on below-consensus revenue.

NVIDIA (NVDA 14.81, +0.27): +1.8% following its in-line earnings and cautious fourth quarter revenue guidance.

Priceline.com (PCLN 1038.00, +15.11): +1.5% after beating on earnings and revenue. However, the company guided Q4 earnings below consensus.

Santarus (SNTS 31.84, +8.62): +37.1% after reporting strong results and announcing it will be acquired by Salix Pharmaceuticals (SLXP 71.31, 0.00) for $32.00 per share, representing a 37.8% premium to yesterday's closing price.

Walt Disney (DIS 66.32, -0.83): -1.2% despite beating earnings estimates by one cent on above-consensus revenue.

Today's economic data will be topped off with the preliminary reading of the November Michigan Sentiment Survey, which will be released at 9:55 ET.

07:58 am : [BRIEFING.COM] S&P futures vs fair value: +2.50. Nasdaq futures vs fair value: +8.00.

07:58 am : Nikkei...14086.80...-141.60...-1.00%. Hang Seng...22744.39...-136.60...-0.60%.

07:58 am : FTSE...6670.37...-26.90...-0.40%. DAX...9024.31...-56.70...-0.60%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com HomepageMarket Update