Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

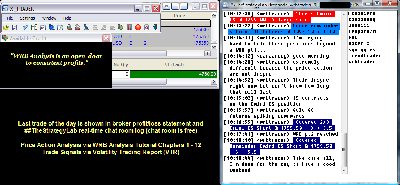

Attachment:

110113-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4760.00.png [ 88.62 KiB | Viewed 326 times ]

110113-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4760.00.png [ 88.62 KiB | Viewed 326 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,310.00 dollars or +13.10 points, Emini ES ($ES_F) futures @

$3,450.00 dollars or +69.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $4,760.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=123&t=1641 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=223&t=2061 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

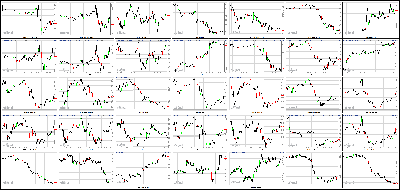

Stocks End Week On A High Note Attachment:

110113-Key-Price-Action-Markets.png [ 538.87 KiB | Viewed 302 times ]

110113-Key-Price-Action-Markets.png [ 538.87 KiB | Viewed 302 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Stocks finished the week with gains on Friday, and investors are cautiously optimistic that this year's rally still has legs.

The Dow Jones industrial average, the S&P 500 and the Nasdaq all rose slightly.

For the week, the Dow and the S&P 500 ended up a bit, while the Nasdaq posted a small loss.

Stocks are coming off a strong month. The S&P 500 gained 5% in October, a significant jump considering the government was shut down for more than two weeks. The Dow and S&P 500 are both hovering near record highs.

If history is any guide, the good times should keep on rolling. The S&P 500 has gained in November more than 60% of the time over the past 30 years, according to Schaeffer's Investment Research.

Ryan Detrick, senior technical analyst Schaeffer's, said November and December have been even stronger in years when stocks have rallied during the first quarter. The theory is that investors who missed the early gains try to make up for it in the final months of the year, he said.

"We expect to see aggressive buyers into the end of year on any and all pullbacks," said Detrick.

Even with the S&P 500 up 23% this year, investors continue to pile into stocks.

Investors poured more than $10 billion into equity funds during the six day period ending Oct. 29, according to data from EPFR Global.

The Fed's bond buying program has been a major catalyst of the bull market over the past few years. While the central bank is expected to stay on hold into next year, investors have been keeping close tabs on the latest economic data to gauge when the Fed might start to pull back on its stimulus efforts.

There was only one major economic report released Friday. But the news was good. The manufacturing sector continued to expand in October. The ISM index rose to 56.4, up from 56.2 in September and topping forecasts.

What's moving: Chevron (CVX, Fortune 500) shares tumbled after the energy company's quarterly results missed expectations. AIG (AIG, Fortune 500) shares sank after the company's sales growth disappointed investors.

Ford (F, Fortune 500) was lower after the company reported that auto sales in the U.S. rose 14% in October. General Motors (GM, Fortune 500) shares rose 1% after the company said U.S. sales were up 16% last month. Toyota (TM) reported an increase in sales as well. Honda (HMC) said sales rose 7.1% last month.

Shares of Madison Square Garden (MSG) fell even though the sports arena operator reported strong results.

Sony (SNE) shares fell after the Japanese electronics maker posted a loss for the second quarter and said profits for the year would be 40% lower than forecast.

Shares in the Royal Bank of Scotland (RBS) slid after the U.K. bank reported far worse than expected quarterly figures.

* China's Craigslist soars in IPOAvon (AVP, Fortune 500) shares rebounded from sharp losses Thursday. The U.S. cosmetics giant has been trying to stage a turnaround but posted much weaker-than-expected quarterly results on Thursday.

But First Solar (FSLR) stock surged after the solar panel company reported quarterly earnings that easily beat expectations.

Container Store cannot be contained. Shares of the home storage retailer doubled in their market debut. The Container Store (TCS) priced its initial public offering at $18 per share. The stock jumped 102% to above $36 a share.

It was the latest in a string of hot IPOs. On Thursday, shares of 58.com (WUBA), the leading classifieds site for local merchants in China, shot up more than 40% on its first day as a public company. And all eyes will soon be on Twitter, which is expected to debut next week.

The strong demand for The Container Store shares took some StockTwits traders by surprise.

"Containers are much more popular than I thought...but is it necessary to dedicate an entire store? $TCS," asked one CapitalObserver.

Others were more blunt.

"$TCS at 35 is a freaking bubble," said momomiester. "That thing up here shows you we are out of control in some areas of the market and it can't last long."

Still, The Container Store has its defenders, including one trader who was apparently still feeling the Halloween spirit.

"Why shouldn't $TCS be almost 2x its issue price? Its an all-weather cyclical. Even surviving a zombie apocalypse requires storage solutions," said andrewunknown.

European markets ended mixed. A tepid report on eurozone inflation gave rise to speculation about an interest rate cut by the European Central Bank. Asian markets also ended mixed. Chinese stocks got a boost as a new report showed Chinese factory activity picked up speed in October.

4:20 pm : The S&P 500 added 0.3% to end the week with a slim advance of 0.1%. Although the broader market ended little changed, small caps were under pressure throughout the session as the Russell 2000 lost 0.4%.

Notably, relative weakness among small caps was a recurring theme throughout the week, causing the Russell to lose 2.0% since Monday.

Outside of the continued underperformance of small caps, the session did not generate too much excitement. The S&P climbed at the open, but slid to lows during the first two hours as the broader market caught down to the Russell's weakness. The S&P was able to battle its way back to the opening high, but could not muster additional gains as energy (-0.3%) and materials (-0.2%) weighed.

The energy sector trailed the broader market throughout the day as Dow component Chevron (CVX 118.01, -1.95) weighed after missing bottom-line estimates by $0.14. Crude oil also pressured the sector, falling 1.8% to $94.61 per barrel.

Elsewhere, materials underperformed as miners displayed broad weakness. The Market Vectors Gold Miners ETF (GDX 24.08, -1.02) tumbled 4.1% while gold futures slid 0.8% to $1313.10 per troy ounce.

On the upside, the relative strength of industrials (+0.8%) and health care (+0.7%) helped the S&P post a modest advance.

Transports paced the gains among industrials as the Dow Jones Transportation Average rallied 1.0%. Meanwhile, the health care sector outperformed with some help from biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 206.06, +0.73) added 0.4%.

Treasuries sold off throughout the session, sending the 10-yr yield higher by six basis points to 2.62%.

Trading volume was a bit above average as just under 810 million shares changed hands on the floor of the New York Stock Exchange.

Although equities endured a relatively quiet session, the same could not be said for the foreign exchange market. The greenback rallied throughout the day, gaining significant strength against the euro and the pound. The Index ended near its high with an advance of 0.7% at 80.72.

The euro was under pressure since yesterday amid rumblings of an ECB rate cut by year-end and continued chatter of negative interest rates. Heavy selling dropped the pair roughly 300 pips off its October highs to 1.3490 against the dollar.

Today's economic data was limited to the October ISM Manufacturing Index, which increased to 56.4 in from 56.2 (Briefing.com consensus 55.0). The common adage throughout the government shutdown was that the manufacturing sector would suffer from lost orders and demand. If the ISM index is an accurate gauge of manufacturing activity in October, then the expected weakness never occurred.

New orders actually strengthened in October. The related index increased to 60.6 in October from 60.5. Meanwhile, order backlogs ended a contraction period and increased to 51.5 from 49.5.

Monday's economic data will be limited to August and September factory orders, which will be released through a single report at 10:00 ET.

Nasdaq +29.9% YTD

Russell 2000 +29.0% YTD

S&P 500 +23.5% YTD

DJIA +19.2% YTD

Week in Review: S&P 500 Holds Ground While Russell Lags

On Monday, the S&P 500 punctuated an uneventful session with a slim advance of 0.1%. Stocks alternated between gains and losses through the first two hours of action before the S&P climbed to a fresh record high of 1764.99. Final-hour selling cut the S&P's gain in half, but the index still finished ahead of the Dow (unch) and the tech-heavy Nasdaq (-0.1%), which was challenged by its flat line throughout the session. The day featured just a handful of notable reports. Health care components caught the eye of some participants with Biogen (BIIB 243.10, -1.09) reporting solid results and Merck (MRK 45.23, +0.14) beating bottom-line estimates on below-consensus revenue. Although Merck weighed, the broader health care sector (+0.3%) drew strength from the 6.7% gain in Bristol-Myers Squibb (BMY 52.48, -0.04) after the company announced positive clinical trial data.

The S&P 500 registered its fourth consecutive advance on Tuesday, climbing 0.6%. The Dow Jones Industrial Average (+0.7%) outperformed the benchmark index while the Nasdaq (+0.3%) lagged after starting the session in-line with the S&P. The tech-heavy Nasdaq posted a modest advance after the exchange experienced an intraday data dissemination issue that prevented index quotes from being sent out for nearly an hour. However, the issue was isolated to the index while individual components traded normally. One of the components that contributed to the Nasdaq's underperformance was Apple (AAPL 520.03, -2.67). The largest tech stock lost 2.5% after its below-consensus gross margin guidance overshadowed its earnings beat on above-consensus revenue.

Wednesday saw the S&P 500 register its first decline in five sessions (-0.5%). Small caps faced additional selling pressure as the Russell 2000 fell 1.4%. Stocks held modest losses into the afternoon, but slid to fresh lows after the Federal Reserve released its latest policy directive, which was little changed from prior statements. Most notably, the directive acknowledged the recent slowdown in the housing sector and noted that fiscal policy is presenting a headwind to growth. In addition, the Committee dropped the reference to "tightening financial conditions" that appeared in the September statement. While the statement did not throw the market any taper-related curveballs, it may have been perceived to be somewhat hawkish as the Committee did not alter its outlook to account for the impact from the partial government shutdown. All ten sectors settled in the red, but their losses were limited to less than 0.8%. Defensive sectors led to the downside, and consumer staples (-0.8%) ended at the bottom of the leaderboard.

On Thursday, the S&P 500 ended with a modest loss of 0.4%, trimming its October gain to 4.5%. Small caps displayed notable weakness during morning trade, but the Russell 2000 ended not far behind the S&P with a loss of 0.5%. Equity indices spent most of the session near their respective flat lines even after more than 250 companies reported their quarterly results since Wednesday's close. Trading volume was subdued until the last 30 minutes of action when a surge in trading activity sent equity indices to lows while pushing the final NYSE volume tally over 900 million shares.DJ30 +69.80 NASDAQ +2.34 SP500 +5.10 NASDAQ Adv/Vol/Dec 1044/1.88 bln/1494 NYSE Adv/Vol/Dec 1359/809.7 mln/1666

3:30 pm : A stronger dollar index put pressure on the commodities space today. The move came on better-than-anticipated October ISM Manufacturing Index data, which increased to 56.4 from 56.2 (Briefing.com consensus called for 55.0).

Dec crude oil extended losses for a fourth consecutive session, falling below the $95.00 per barrel level for the first time since late June. The energy component pulled back from its session high of $95.75 per barrel set at pit trade open and trended lower as the session progressed. It settled 1.8% lower at $94.61 per barrel, just above its session low of $94.54 per barrel. The drop brought losses for the week to 3.3%.

Dec natural gas also traded in the red. It chopped around in a narrow four cent range and settled 2.0% lower at its session low of $3.51 per MMBtu, booking a 7.9% loss for the week.

Dec gold extended yesterday's losses, dipping as low as $1305.60 per ounce. Unable to gain momentum, it settled with a 0.8% loss at $1313.10 per ounce, declining by 2.9% over the week.

Dec silver brushed a session high of $21.95 per ounce in afternoon pit trade after trading as low as $21.77 per ounce. However, it was unable to hold on to the gains and settled just below the unchanged line at $21.85 per ounce, booking a 3.0% loss for the week.DJ30 +57.31 NASDAQ -2.74 SP500 +3.53 NASDAQ Adv/Vol/Dec 899/1.49 bln/1630 NYSE Adv/Vol/Dec 1184/501.3 mln/1800

3:00 pm : The S&P 500 is higher by 0.1% as today's session enters its final hour.

Although equities endured a relatively quiet session, the same could not be said for the foreign exchange market. The greenback has rallied throughout the day, gaining significant strength against the euro and the pound. At this juncture, the Dollar Index hovers near its high with an advance of 0.7% at 80.73.

The euro has been under pressure since yesterday amid rumblings of an ECB rate cut by year-end and continued chatter of negative interest rates. Selling has dropped the pair roughly 300 pips off its October highs, and has action testing support aided by the 50-day moving average (1.3485).DJ30 +44.50 NASDAQ -7.32 SP500 +1.66 NASDAQ Adv/Vol/Dec 869/1.38 bln/1650 NYSE Adv/Vol/Dec 1138/461.5 mln/1856

2:30 pm : The major averages continue to hold their recent levels with the S&P 500 up 0.2%.

Earlier, participants received this week's final economic data point in form of the October ISM Manufacturing Index. The index ticked up 56.4 in from 56.2 (Briefing.com consensus 55.0) despite the partial-government shutdown that affected a good portion of the reporting period.

Next week sets up to be busy in terms of data as the advance third quarter GDP will be released on Thursday at 8:30 ET and October nonfarm payrolls will be reported on Friday at 8:30 ET.

On Monday, factory orders for August and September will be reported at 10:00 ET.DJ30 +47.17 NASDAQ -6.38 SP500 +1.69 NASDAQ Adv/Vol/Dec 923/1.28 bln/1600 NYSE Adv/Vol/Dec 1131/426.6 mln/1843

2:00 pm : The S&P 500 has climbed back into positive territory, but generally speaking, the three major averages remain little changed.

The benchmark index was able to regain its flat line as the financial sector ticked up off the lows. The group trades higher by 0.3%, but only JPMorgan Chase (JPM 52.32, +0.78) and Morgan Stanley (MS 29.29, +0.56) trade with gains larger than 1.0%.DJ30 +51.69 NASDAQ -6.64 SP500 +2.60 NASDAQ Adv/Vol/Dec 866/1.18 bln/1641 NYSE Adv/Vol/Dec 1155/391.5 mln/1810

1:35 pm : The S&P 500 has spent the past 30 minutes within a two-point range just below its flat line. Although the index has not moved much from its midday level, a handful of underperforming sectors have widened their losses.

The technology sector (-0.2%) has turned negative, succumbing to the pressure exerted by Apple (AAPL 516.98, -5.72) as the largest tech stock trades on its lows with a loss of 1.1%.

Elsewhere, the discretionary space has widened its loss to 0.2%. Homebuilders trade broadly lower and the iShares Dow Jones US Home Construction ETF (ITB 22.11, -0.41) trades down 1.8%. Today's loss marks the third consecutive decline, and has placed the ETF on its 50-day moving average.

On a related note, Treasuries remain pinned to their lows with the 10-yr yield up six basis points at 2.62%.DJ30 +23.21 NASDAQ -13.60 SP500 -0.96 NASDAQ Adv/Vol/Dec 808/1.09 bln/1692 NYSE Adv/Vol/Dec 1018/364.2 mln/1936

12:55 pm : At midday, the major averages trade mixed as the Dow holds a modest gain of 0.2% while the S&P 500 hovers just below its flat line. Small caps have underperformed throughout the week, and the Russell 2000 (-1.0%) lags once again today.

Stocks registered modest opening gains, but small caps acted weak from the get-go as the Russell 2000 opened in the red. The small cap index has actually underperformed throughout the week, and including today's decline, the index is on track to end the week with a loss of 2.6%.

Meanwhile, the S&P 500 has held up relatively well in the same timeframe as it sports a week-to-date decline of just 0.2%.

Even though the benchmark index trades lower, only four sectors hover in the red. Two of those four (financials and consumer discretionary) sit just below their respective flat lines while the other two-energy and materials-trade lower by 1.0% and 0.4%, respectively.

The energy space has been pressured by Dow component Chevron (CVX 117.22, -2.74), which trades lower by 2.3% after missing earnings estimates by $0.14. Meanwhile, miners weigh on the materials sector as the Market Vectors Gold Miners ETF (GDX 24.36, -0.74) holds a loss of 3.0%.

On the upside, health care (+0.3%) and industrials (+0.2%) have lent support to the broader market with the industrial sector drawing strength from the Dow Jones Transportation Average, which trades higher by 0.6%.

Despite the weakness among small caps, there hasn't been much of a rush for protection. The CBOE Volatility Index (VIX 13.79, +0.04) has barely budged while Treasuries hover near their lows with the 10-yr yield up five basis points at 2.61%.

Today's economic data was limited to the October ISM Manufacturing Index, which increased to 56.4 in from 56.2 (Briefing.com consensus 55.0). The common adage throughout the government shutdown was that the manufacturing sector would suffer from lost orders and demand. If the ISM index is an accurate gauge of manufacturing activity in October, then the expected weakness never occurred.

New orders actually strengthened in October. The related index increased to 60.6 in October from 60.5. Meanwhile, order backlogs ended a contraction period and increased to 51.5 from 49.5.DJ30 +27.51 NASDAQ -0.42 SP500 -8.07 NASDAQ Adv/Vol/Dec 786/979.8 mln/1683 NYSE Adv/Vol/Dec 1015/333.2 mln/1926

12:35 pm : The major averages remain on their lows as the Dow tries to resist rejoining the remaining indices in the red.

Despite the persistent selling pressure, investors have not rushed in search of protection as indicated by the CBOE Volatility Index (VIX 13.82, +0.06), which holds a modest gain of just 0.4%. The near-term volatility measure has been trapped between 12.0% and 14.0% since October 18.

The bond market has not shown safe-haven buying either as the 10-yr yield trades higher by six basis points at 2.62%.DJ30 +22.99 NASDAQ -5.84 SP500 -0.45 NASDAQ Adv/Vol/Dec 807/917.4 mln/1648 NYSE Adv/Vol/Dec 1015/315.2 mln/1922

12:00 pm : Equity indices have slipped to fresh lows, and the Dow has now surrendered its gain. With today marking the end of the week, the Dow is currently on track to register a modest loss of 0.1%.

While the Dow has held up relatively well through a choppy week, the Russell 2000 has not been as fortunate. The small cap index is down 1.1% today, which has extended its week-to-date loss to 2.7%.

Even though the Russell appears likely to end the week well behind the Dow, it remains up 28.1% this year versus an 18.7% gain in the price-weighted Dow Jones.DJ30 -1.25 NASDAQ -12.89 SP500 -2.65 NASDAQ Adv/Vol/Dec 731/817.2 mln/1700 NYSE Adv/Vol/Dec 987/280.9 mln/1921

11:30 am : Recent action saw an acceleration in selling pressure that sent the S&P 500 and Nasdaq into negative territory. Meanwhile, the Dow continues to hover just above its flat line.

As a result of the slide to lows, individual sectors are now divided evenly as five groups (health care, financials, industrials, utilities, and telecom services) hold modest gains while the other five (consumer discretionary, consumer staples, energy, materials, and technology) trade in negative territory.

Given the onset of weakness, the Russell 2000 (-0.9%) bears watching into the afternoon as the index lagged from the start and has been ahead of the decline in the broader indices. Treasuries have also been of interest as the 10-yr yield sits at its highest level of the session, up five basis points at 2.51%.DJ30 +26.69 NASDAQ -8.14 SP500 -0.69 NASDAQ Adv/Vol/Dec 748/704.9 mln/1646 NYSE Adv/Vol/Dec 1062/245.4 mln/1826

11:00 am : The Dow (+0.4%), Nasdaq (+0.1%), and S&P 500 (+0.3%) continue to sport modest gains while the Russell 2000 (-0.6%) has slipped to a fresh low.

The underperformance of small caps is a bit more difficult to spot among individual sectors as eight of ten groups trade with gains of at least 0.2%. Meanwhile, the energy (-0.6%) sector is the lone decliner while materials trade little changed.

Treasuries have returned to their lows as the 10-yr yield trades higher by five basis points at 2.61%.DJ30 +62.29 NASDAQ +2.43 SP500 +3.99 NASDAQ Adv/Vol/Dec 846/565.2 mln/1505 NYSE Adv/Vol/Dec 1261/205.5 mln/1577

10:30 am : A stronger dollar index is putting pressure on the commodities space this morning, with crude oil and precious metals trading in negative territory. Dec crude oil has been trending lower, retreating from its session high of $95.75 per barrel set at pit trade open. It is currently down 1.3% at $95.12 per barrel.

Dec natural gas has also been slipping lower in the red. Prices pulled back from a session high of $3.55 per MMBtu and are now at $3.53 per MMBtu, or 1.5% lower.

Dec gold is extending morning losses following the release of the ISM Index data that showed an increase to 56.4 in October from 56.2 in September. The yellow metal brushed a session high of $1316.00 per ounce prior to the release, but is now at $1308.50 per ounce, or 1.1% lower.

Dec silver rose to a session high of $21.94 in early morning pit trade but has since retreated into the red. It is currently down 0.1% at $21.84 per ounce.DJ30 +49.45 NASDAQ +2.33 SP500 +2.86 NASDAQ Adv/Vol/Dec 932/427.2 mln/1364 NYSE Adv/Vol/Dec 1318/164.4 mln/1472

10:00 am : The S&P 500 continues to hover near its high with a gain of 0.3%.

The October ISM Index rose to 56.4 from 56.2 while the Briefing.com consensus expected the reading to slip to 55.0.DJ30 +75.26 NASDAQ +12.80 SP500 +6.06 NASDAQ Adv/Vol/Dec 1040/264.8 mln/1166 NYSE Adv/Vol/Dec 1508/112.8 mln/1233

09:45 am : As expected, the Dow (+0.5%), Nasdaq (+0.4%), and S&P 500 (+0.4%) began the session with modest gains while the Russell 2000 (-0.1%) registered an opening loss. The small cap Russell 2000 has underperformed throughout the week, and the early indications suggest the story may repeat today.

Nine of ten sectors trade with early gains while energy (-0.3%) lags as Chevron (CVX 118.00, -1.96) pressures the sector after missing earnings estimates by $0.14. Even though the Dow component is an early laggard, the price-weighted index is the top performer as Boeing (BA 131.90, +1.40) and Visa (V 200.29, +3.62) trade with respective gains of 1.1% and 1.8%.

The October ISM Index will be reported at 10:00 ET.DJ30 +71.06 NASDAQ +15.78 SP500 +6.66 NASDAQ Adv/Vol/Dec 1022/161.4 mln/1132 NYSE Adv/Vol/Dec 1556/78.2 mln/1139

09:14 am : [BRIEFING.COM] S&P futures vs fair value: +2.50. Nasdaq futures vs fair value: +10.50. The S&P 500 futures hover near their pre-market high (+0.2%) as investors anticipate modest gains at the start of today's session. Pre-market action has been relatively quiet with participants receiving a slew of quarterly reports. Although nearly 50 companies announced their results this morning, very few came from market-moving names. Notably, Dow component Chevron (CVX 119.25, -0.71) is lower by 0.6% after missing on earnings and revenue.

Today's economic data will be limited to the October ISM Index, which will be reported at 10:00 ET.

Treasuries hover near their lows with the 10-yr yield up three basis points at 2.59%.

08:58 am : [BRIEFING.COM] S&P futures vs fair value: +3.30. Nasdaq futures vs fair value: +11.20. The S&P 500 futures trade higher by 0.2%.

Markets across Asia ended mixed amid a mostly uneventful session. China's Shanghai Composite (+0.4%) and Hong Kong's Hang Seng (+0.2%) ticked higher following the better than expected Manufacturing PMI (51.4 actual versus 51.2 expected, 51.1 previous) and HSBC Final Manufacturing PMI (50.9 actual versus 50.7 expected, 50.9 previous) reports. Elsewhere, India's Sensex (+0.2%) saw a record close for a third straight session. Japan's Nikkei (-0.9%) lagged as action settled at a one-week low. Inflation readings out overnight showed Indonesia's slip to 8.3% year-over-year (8.4% expected), South Korea's cool to 0.7% year-over-year (0.8% previous), and Thailand's rise to 1.5% year-over-year (1.4% previous). Indonesia's trade balance swung to a 0.66 billion deficit.

In Japan, the Nikkei lost 0.9% as poor guidance weighed. Electronics maker Sony tumbled 11.1% while NTT Data shed 4.8% after both cut their estimates.

Hong Kong's Hang Seng added 0.2% as casino names led the way. Galaxy Entertainment and Sands China both advanced 1.8% after a positive report on Macau gaming revenues.

In China, the Shanghai Composite rose 0.4% as financials booked solid gains. Ping An tacked on 2.0% while China Merchants Bank advanced 1.6%.

Major European indices trade mostly lower with Italy's MIB (-0.3%) pacing the decline. The euro has continued showing weakness after disappointing unemployment and CPI data crossed the wires yesterday. The below-consensus CPI reading contributed to speculation that the European Central Bank could cut its key rate at next week's policy meeting. Since yesterday, the single currency has surrendered nearly 230 pips to the dollar. The pair currently trades near 1.3515. Economic data was limited to just two data points as Great Britain's Manufacturing PMI slipped to 56.0 from 56.3 (56.1 forecast) and Swiss SVME PMI fell to 54.2 from 55.3 (55.5 expected).

Great Britain's FTSE outperforms other regional indices with a slim advance of 0.1%. Vodafone is the top performer, trading higher by 2.8% amid speculation AT&T could take over the British telecom carrier. Defense contractor Meggitt trades lower by 10.0% after cutting its revenue outlook.

Germany's DAX is off 0.1% as producers of basic materials pace the decline. HeidelbergCement and Lanxess are lower by 2.4% and 1.4%, respectively. Volkswagen is the top performer, trading higher by 1.9%.

In France, the CAC holds a loss of 0.3% as Renault weighs. The carmaker trades lower by 4.5%. On the upside, media and telecom names have displayed strength. Orange and Publicis Groupe are both up near 0.7%.

Italy's MIB is lower by 0.3% as 34 of 40 components register losses. Fiat is lower by 2.5% and CNH Industrial trades down 3.0% after reporting disappointing results.

08:29 am : [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +10.20. U.S. equity futures continue to hover near their highs, signaling a modestly upbeat start to the final session of the week.

Overseas action has been subdued with just a handful of notable developments. In China, the Manufacturing PMI rose to 51.4 from 51.1 (51.2 expected) while the HSBC Manufacturing PMI held steady at 50.9 (50.7 forecast). Meanwhile, European markets trade with modest losses as the euro sees continued weakness. The common currency began retreating yesterday after disappointing unemployment and CPI data crossed the wires. The euro hovers near 1.3521 against the dollar after surrendering more than 200 pips since yesterday.

Treasuries have seen some selling over the past three hours as the 10-yr yield trades higher by two basis points at 2.58%.

07:59 am : [BRIEFING.COM] S&P futures vs fair value: +2.30. Nasdaq futures vs fair value: +8.70. U.S. equity futures hold modest pre-market gains with the S&P 500 futures trading higher by 0.2%.

Reviewing overnight developments:

Asian markets ended mixed. Hong Kong's Hang Seng +0.2%, China's Shanghai Composite +0.4%, and Japan's Nikkei -0.9% as the yen endured a volatile session. USDJPY fell below 98.00 before climbing back above 98.25 at the end of the Tokyo session.

Investors received several economic data points:

China's Manufacturing PMI rose to 51.4 from 51.1 (51.2 expected) while the HSBC Manufacturing PMI held steady at 50.9 (50.7 forecast).

South Korea's trade surplus expanded to $4.90 billion from $3.70 billion ($4.35 billion expected). Meanwhile, CPI slipped 0.3% month-over-month (0.1% forecast, 0.2% prior) while the year-over-year reading increased 0.7% (1.0% forecast, 0.8% last).

Australia's AIG Manufacturing Index rose to 53.2 from 51.7. Separately, PPI increased 1.3% quarter-over-quarter (0.7% forecast, 0.1% prior).

India's HSBC Markit Manufacturing PMI held steady at 49.60.

In news:

In China, the Shanghai Interbank Offered rate eased for the second day with the two-week rate registering the most notable decline, down 48 basis points to 5.03%.

Core European indices sport modest losses while peripheral markets lag. Great Britain's FTSE -0.1%, Germany's DAX -0.2%, and France's CAC -0.3%. Elsewhere, Italy's MIB -0.5% and Spain's IBEX -0.4%.

Economic data was limited:

Great Britain's Manufacturing PMI slipped to 56.0 from 56.3 (56.1 forecast).

Swiss SVME PMI fell to 54.2 from 55.3 (55.5 expected).

Looking at news:

The euro has continued its decline after disappointing unemployment and CPI data crossed the wires yesterday. The below-consensus CPI reading contributed to speculation that the European Central Bank could cut its key rate at next week's policy meeting. Since yesterday, the single currency has surrendered nearly 230 pips to the dollar. The pair currently trades near 1.3520.

In U.S. corporate news:

AIG (AIG 49.25, -2.40): -4.7% after reporting in-line earnings on below-consensus revenue.

First Solar (FSLR 53.96, +3.65): +7.3% after cruising past earnings estimates by $1.44 on above-consensus revenue.

Madison Square Garden (MSG 60.52, 0.00): reported a bottom-line beat on better-than-expected revenue.

Netflix (NFLX 329.00, +6.52): +2.0% after Robert W. Baird upgraded the stock to 'Outperform' from 'Neutral' while raising its price target to $420 from $383.

Today's economic data will be limited to the October ISM Index, which will be released at 10:00 ET.

07:26 am : [BRIEFING.COM] S&P futures vs fair value: +2.00. Nasdaq futures vs fair value: +8.50.

07:26 am : Nikkei...14201.57...-126.40...-0.90%. Hang Seng...23249.79...+43.40...+0.20%.

07:26 am : FTSE...6723.53...-8.00...-0.10%. DAX...9021.78...-12.10...-0.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com HomepageMarket Update