Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

103113-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5825.00.png [ 82.59 KiB | Viewed 458 times ]

103113-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5825.00.png [ 82.59 KiB | Viewed 458 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$700.00 dollars or +7.00 points, Emini ES ($ES_F) futures @

$5125.00 dollars or +102.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $5,825.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=122&t=1640 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=221&t=2029 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

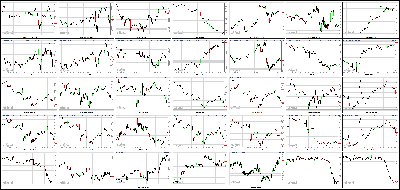

Stocks End A Winning October With A Thud Attachment:

103113-Key-Price-Action-Markets.png [ 526.1 KiB | Viewed 486 times ]

103113-Key-Price-Action-Markets.png [ 526.1 KiB | Viewed 486 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Investors clocked big wins for the month of October but didn't add to their gains on the last trading day.

Stocks fell modestly Thursday, one day after the Federal Reserve said that it will do exactly what the market wanted. The Fed will keep buying $85 billion a month in bonds.

Still, even though the last day of October looks more like a trick than a treat, the S&P 500 has rallied nearly 5% this month, and the Dow Jones Industrial Average has run up more than 3%. It's been Rocktober as opposed to Shocktober. The Dow and S&P are also still hovering near all-time highs.

The question now is whether the bull is running out of steam.

The Fed's bond buying program has been a catalyst for an epic stock market run this year, but investors now seem to need more compelling reasons to keep pushing stocks higher.

Some investors had hoped the Fed would mention what impact the recent government shutdown had on economic growth. If the Fed sounded more negative about the economy, that might have been interpreted as a sign that the central bank may keep buying bonds well into 2014.

Investors around the globe also appear to be suffering from rally fatigue. European markets closed mixed and nearly all Asian markets ended in the red.

* Are investors joining rally too late?Facebook's flip flop: Facebook (FB, Fortune 500) faked out investors Wednesday night. The social media site's stock spiked 15% after hours when it announced that earnings and revenues easily beat forecasts thanks to strong mobile growth.

But investors became spooked when the company said during its conference call that the number of teen users who were visiting the social networking site on a daily basis had fallen.

Facebook's stock fell in early morning trading but reversed course again and closed up more than 2%, as some analysts downplayed the fears that teens weren't as active on the site.

StockTwits user Cyanus was happy to have sat out Wednesday and Thursday's wild ride. "$FB Doing nothing & staying long was the correct play, after all. Bullish."

Other investors said that there was an opportunity to make a quick buck on the volatility. "$FB honestly this stock has been a day traders dream since late yesterday," wrote TeslaMan.

* Is Puerto Rico the next Detroit?China's Craigslist is booming: China's equivalent of Craigslist, 58.com (WUBA), debuted Thursday, and shares closed up more than 40%.

Expedia's (EXPE) stock jumped more than 18% on better-than-expected earnings. Meanwhile, Priceline's (PCLN, Fortune 500) stock dipped. Shares of Priceline have been extremely hot this year, recently surging above the $1,000 mark.

StockTwits commenter contrarianspeculator thought Priceline's move down on Expedia's win as the right move. ""$EXPE: taking market share from $PCLN? A great paired trade: Long EXPE and short PCLN."

Painful quarter for the Avon Lady: Shares of Avon (AVP, Fortune 500) dropped 25% due to disastrous quarterly results and a warning from the makeup retailer that it might have to pay a larger-than-expected fine to the SEC to settle a bribery probe.

Exxon Mobil (XOM, Fortune 500) reported a sharp drop in profits but the oil company's shares still rallied Thursday.

4:15 pm : The S&P 500 ended with a modest loss of 0.4%, trimming its October gain to 4.5%. Small caps displayed notable weakness during morning trade, but the Russell 2000 ended not far behind the S&P with a loss of 0.5%.

Equity indices spent most of the session near their respective flat lines even after more than 250 companies reported their quarterly results between yesterday's close and today's opening bell. Trading volume was subdued until the last 30 minutes of action when a surge in trading activity sent equity indices to lows while pushing the final NYSE volume tally over 900 million shares.

The benchmark index displayed early weakness as the broader market followed in the footsteps of the financial sector (-1.1%), which slipped out of the gate and spent the entire session in the red. Financials finished at the bottom of the leaderboard while also ending the month behind the remaining nine sectors with an October gain of 3.2%.

Following the early dip, the S&P returned to its flat line, where it hovered until selling accelerated during the final hour.

Only the consumer discretionary space posted a gain (+0.2%) with media names providing support after Time Warner Cable (TWC 120.15, +3.27) reported better-than-expected results. Homebuilders did not take part in the rally as the iShares Dow Jones US Home Construction ETF (ITB 22.52, -0.46) lost 2.0%.

Elsewhere, the energy sector outperformed (-0.2%), receiving support from Exxon Mobil (XOM 89.62, +0.81) after the Dow component reported results ahead of analyst expectations. Another Dow member, Chevron (CVX 119.96, -0.34), also announced above-consensus earnings, but ended lower by 0.3%.

Among other earnings of note, Facebook (FB 50.20, +1.20) posted a gain of 2.4% after enduring some after-hours drama yesterday. The social media stock jumped as high as 14.0% in reaction to its solid quarter, but relinquished the gain after company management said during the conference call that a decline in daily traffic among younger users has been observed.

Treasuries ended modestly lower with the 10-yr yield up one basis point at 2.55%.

In overseas news of note, eurozone unemployment (12.2% actual versus 12.0% expected) and CPI (0.7% actual versus 1.1% consensus) came in well-below estimates, which stoked expectations for additional liquidity provisions from the European Central Bank. On that note, governing council member Ewald Nowotny said the ECB will ensure a smooth transition once long-term refinancing operations come to an end. The euro was under pressure throughout the session, falling over 150 pips against the dollar to 1.3584.

Investors received just two economic data points today. Weekly initial claims decreased to 340,000 from 350,000 (Briefing.com consensus 335,000). This initial claims report represented the first clean reading for the labor market since August as issues with California's numbers have now been ironed out. Unfortunately, the report reflected a modest increase in layoff levels over the past couple of months.

An initial claims reading of 340,000 is enough to keep the unemployment rate steady but not enough to drive steady payroll gains above 200,000. The continuing claims level increased to 2.881 million from a downwardly revised 2.859 million (from 2.874 million). The consensus pegged the continuing claims level at 2.850 million.

Separately, the October Chicago PMI registered its largest one-month spike in more than 30 years, jumping to 65.9 from 55.7 (Briefing.com consensus 55.0). We are skeptical that the sharp increase is legitimately showing vast improvement in the manufacturing sector. Most of the Federal Reserve regional manufacturing surveys were either flat or softened slightly from lost demand due to the government shutdown. In contrast, the manufacturers in the Chicago region recorded their strongest activity since March 2011.

Tomorrow, the October ISM Index will be released at 10:00 ET.

Nasdaq +29.8% YTD

Russell 2000 +29.5% YTD

S&P 500 +23.2% YTD

DJIA +18.6% YTD

DJ30 -73.01 NASDAQ -10.91 SP500 -6.77 NASDAQ Adv/Vol/Dec 976/2.15 bln/1578 NYSE Adv/Vol/Dec 1190/908.1 mln/1822

3:30 pm :

The dollar index gained strength following yesterday's FOMC statement which was viewed as slightly more hawkish than was anticipated and fueled assumptions of a tapering in the December meeting. The move higher weighed on the commodities space, especially precious metals

Dec gold fell as low as $1318.70 per ounce and settled with a 1.9% loss at $1323.50 per ounce

Dec silver dropped even harder, falling to a session low of $21.73 per ounce. Like gold, it was unable to gain momentum and settled 5.1% lower at $21.86 per ounce

Dec crude oil fell for a third consecutive session. It brushed a session high of $97.03 per barrel moments after equity markets opened but quickly retreated back into negative territory. Despite chopping around near the break-even line in late afternoon pit action, it settled with a 0.4% loss at $96.37 per barrel

Dec natural gas pulled back from its session high of $3.65 per MMBtu set at pit trade open and spent the remainder of the session in the red. It fell as low as $3.56 per MMBtu following inventory data that showed a build of 38 bcf when a build of 36-43 bcf was anticipated. It eventually settled with a 1.1% loss at $3.58 per MMBtu.

DJ30 -16.50 NASDAQ -2.08 SP500 -0.81 NASDAQ Adv/Vol/Dec 1021/1753.4 mln/1521 NYSE Adv/Vol/Dec 1335/485 mln/1648

3:05 pm : With one hour remaining in today's session, the S&P 500 sits at its best level of the day. Participants received an avalanche of quarterly reports between yesterday's close and today's open with another busy week ahead.

However, before moving into next week, roughly 100 more quarterly reports are scheduled to be released between today's closing bell and tomorrow's open. Notably, CBOE Holdings (CBOE 48.84, -0.45), Chevron (CVX 121.00, +0.70), and NextEra Energy (NEE 85.00, -0.54) will release their results prior to tomorrow's open.DJ30 -7.25 NASDAQ +2.20 SP500 +0.30 NASDAQ Adv/Vol/Dec 1119/1.58 bln/1414 NYSE Adv/Vol/Dec 1406/440.7 mln/1551

2:30 pm : Recent action saw the major averages climb to fresh highs in a move that involved upticks in all ten S&P 500 sectors. Even the financial space, which has lagged throughout the day, was able to climb to a fresh rebound high. However, the sector remains lower by 0.4% as nearly all major components trade lower. Dow member Goldman Sachs (GS 162.61, +0.56) is the lone outperformer, trading higher by 0.3%.

With today's session marking the end of October, financials are on track to finish the month behind the remaining nine sectors with a gain of 3.9%. Meanwhile, the telecom services sector has had the best showing, rising 8.0% this month.DJ30 +33.10 NASDAQ +14.35 SP500 +5.20 NASDAQ Adv/Vol/Dec 1225/1.45 bln/1303 NYSE Adv/Vol/Dec 1578/406.6 mln/1362

2:00 pm : Equity indices remain near their flat lines and the Russell 2000, which lagged during the early portion of the session, now trades in-line with the S&P 500.

Five of six cyclical groups remain in positive territory, but the top-weighted S&P sector, technology, sits just above its flat line while the second largest sector, financials (-0.7%), remains near its lows.

With trading volume drying up into the afternoon, the two largest sectors could become a factor in the broader market's performance into the close.DJ30 -2.12 NASDAQ +7.42 SP500 +1.36 NASDAQ Adv/Vol/Dec 1131/1.34 bln/1379 NYSE Adv/Vol/Dec 1359/373.8 mln/1555

1:20 pm : There has been a bit of a tug-of-war between bears and bulls today as the major indices have danced on either side of the unchanged line.

Currently, the overall standing of the market is pretty flat, which is not a bad position considering market breadth skews negative with declining issues outnumber advancing issues at the NYSE (4-to-3 margin) and Nasdaq (7-to-5 margin). The underlying message is that the broader market is drawing support from its larger cap, and more heavily weighted, issues.

ExxonMobil (XOM 90.18, +1.38) is among the heaviest of them all and is riding a 1.5% gain after reporting better-than-expected earnings. Separately, we can see the influence of many of the large-cap technology stocks like Google (GOOG 1038.36, +7.84) in the outperformance of the Nasdaq 100 (+0.3%).DJ30 +1.16 NASDAQ +6.27 SP500 +1.02 NASDAQ Adv/Vol/Dec 1063/1.22 bln/1425 NYSE Adv/Vol/Dec 1304/340 mln/1605

1:00 pm : At midday, the major averages hover near their flat lines. Equities saw some opening weakness, but the early dip was limited in scope as bargain hunters stepped in and bid stocks off their lows.

The broader market appears to have found support in quarterly earnings after more than 250 companies (42 S&P 500 members) reported results that were mostly better-than-expected. Moreover, the S&P 500 was able to climb off its lows despite continued calls for a pullback after the index rallied over 6.5% during the past three weeks.

Seven of ten sectors sport midday gains with the discretionary space (+0.6%) in the lead. The cyclical sector has received support from media names after Time Warner Cable (TWC 121.10, +4.22) reported better-than-expected earnings. Internet retailers and travel sites have also contributed to the sector's strength with Expedia's (EXPE 58.30, +8.34) earnings-driven 16.7% gain leading the way.

Elsewhere, the industrial sector (+0.3%) also outperforms even as transports lag. The Dow Jones Transportation Average is off 0.2%, but the sector has been underpinned by defense contractors. The PHLX Defense Index is higher by 0.6% with the second-largest component, Boeing (BA 131.42, +1.75), holding a gain of 1.3% amid news the company is nearing a deal to sell over 250 model 777X jetliners.

Although five of six cyclical sectors trade in positive territory, the underperformance of the financial space (-0.6%) is notable. Should the second-largest S&P sector see continued weakness through the afternoon, it could become a drag on the broader market.

Meanwhile, the top-weighted sector, technology, outperforms with a gain of 0.1%. Facebook (FB 51.04, +2.04) is higher by 4.2% after displaying some volatility following its better-than-expected earnings report. The stock was up as much as 14.0% after-hours, but surrendered its gain after company officials acknowledged a decline in daily traffic among younger users.

Treasuries hold modest losses with the 10-yr yield up two basis points at 2.56%.

Investors received just two economic data points today. Weekly initial claims decreased to 340,000 from 350,000 (Briefing.com consensus 335,000). This initial claims report represented the first clean reading for the labor market since August as issues with California's numbers have been ironed out. Unfortunately, the report reflected a modest increase in layoff levels over the past couple of months.

An initial claims reading of 340,000 is enough to keep the unemployment rate steady but not enough to drive steady payroll gains above 200,000. The continuing claims level increased to 2.881 million from a downwardly revised 2.859 million (from 2.874 million). The consensus pegged the continuing claims level at 2.850 million.

Separately, the October Chicago PMI registered its largest one-month spike in more than 30 years, jumping to 65.9 from 55.7 (Briefing.com consensus 55.0). We are skeptical that the sharp increase is legitimately showing vast improvement in the manufacturing sector. Most of the Federal Reserve regional manufacturing surveys were either flat or softened slightly from lost demand due to the government shutdown. In contrast, the manufacturers in the Chicago region recorded their strongest activity since March 2011.DJ30 -8.48 NASDAQ +4.95 SP500 +0.44 NASDAQ Adv/Vol/Dec 1031/1.14 bln/1453 NYSE Adv/Vol/Dec 1256/321.2 mln/1637

12:35 pm : The S&P 500 remains just above its flat line while the Nasdaq outperforms with a slim advance of 0.2%. Similar to the Nasdaq, the technology sector (+0.3%) is one of today's leaders after a slew of sector components reported earnings between yesterday's closing bell and today's open.

Notably, Facebook (FB 50.77, +1.76) has displayed some considerable volatility following its better-than-expected earnings report. The stock was up as much as 14.0% after-hours, but surrendered its gain after company officials acknowledged a decline in daily traffic among younger users. Currently, Facebook holds a solid gain of 3.7%.

Another large tech (and Dow) component, Visa (V 197.68, -6.14), is lower by 3.0% after missing earnings estimates by one cent on below-consensus revenue.DJ30 +3.02 NASDAQ +8.35 SP500 +1.63 NASDAQ Adv/Vol/Dec 1030/1.06 bln/1432 NYSE Adv/Vol/Dec 1252/300.1 mln/1640

12:00 pm : The S&P 500 has clawed its way back to the flat line while the Dow (-0.1%) and the Russell 2000 (-0.1%) remain modestly lower. The discretionary sector (+0.5%) continues to provide support to the broader market while consumer staples (-0.2%), financials (-0.6%), and health care (-0.1%) remain in the red.

Treasuries have held their levels near session lows with the 10-yr yield higher by three basis points at 2.56%.DJ30 -22.35 NASDAQ +0.09 SP500 +0.48 NASDAQ Adv/Vol/Dec 970/959.2 mln/1476 NYSE Adv/Vol/Dec 1158/271.6 mln/1721

11:30 am : The major averages have battled their way back from session lows, but continue to hold modest losses. Despite the ongoing rebound among key indices, the financial sector (-0.7%) has slipped to a fresh low.

Since the sector represents the second-largest S&P 500 group, its performance should be watched for the remainder of the session. Continued weakness could become a drag on the broader market while a sustained rebound off lows would provide the broader market with a measure of support.

At this juncture, the S&P is building on the relative strength of technology (+0.2%), industrials (+0.1%), and discretionary shares (+0.4%).DJ30 -36.38 NASDAQ -0.63 SP500 -1.58 NASDAQ Adv/Vol/Dec 904/806.2 mln/1506 NYSE Adv/Vol/Dec 1057/230.9 mln/1780

11:00 am : Equities have continued their retreat with the Russell 2000 (-0.5%) pacing the slide. As mentioned earlier, the small cap index has lagged throughout the week, and it underperforms once again today. Including today's decline, the Russell is lower by 1.6% this week, but remains up 2.5% in October.

Meanwhile, the S&P 500 sports a more modest downtick of 0.2% as seven of ten sectors trade lower. Utilities (-1.0%) and financials (-0.6%) hold notable losses while the remaining laggards hold losses that don't exceed 0.3%.

On the upside, the discretionary sector (+0.2%) leads as media names display relative strength after Time Warner Cable (TWC 119.75, +2.87) reported a bottom-line beat. Meanwhile, homebuilders trade lower as the 10-yr yield sits at its highest level of the day (+3 bps at 2.56%). The iShares Dow Jones US Home Construction ETF (ITB 22.80, -0.18) trades down 0.8%.DJ30 -42.19 NASDAQ -3.84 SP500 -3.04 NASDAQ Adv/Vol/Dec 839/698.1 mln/1539 NYSE Adv/Vol/Dec 960/201.7 mln/1670

10:35 am : Strength in dollar index hit commodities this morning, especially precious metals. Silver tanked over 5% this morning and both gold and silver are well in the red. Silver fell below $22 and gold fell below $1325.

Crude oil has been volatile this morning. After selling off sharply from just below $97 to as low as $96.06/barrel (Dec contract). In current trade, Dec crude oil is -0.9% at $96.17/barrel.

Natural gas was lower ahead of today's inventory data and dropped further to a new LoD following the data (Natural gas inventory showed a build of 38 bcf vs expectations for a build of 36-43 bcf.) Nov nat gas is now -1.0% at $3.59/MMBtu.

Precious metals remains well in the red, led by silver. Dec silver is currently -4.2% at $22.03/oz, Dec gold is -1.8% at $1324.50/oz. DJ30 -40.36 NASDAQ -11.65 SP500 -3.56 NASDAQ Adv/Vol/Dec 762/542.2 mln/1537 NYSE Adv/Vol/Dec 925/163 mln/1854

10:00 am : The S&P 500 made a brief run to fresh highs after the Chicago PMI report for October blew past estimates (65.9 actual, 55.7 expected), but the index has since slipped to fresh lows. The other indices have followed suit and the Russell 2000 (-0.3%) now trails the benchmark average.

Only two sectors continue to trade in positive territory (energy and health care), but both hold slim gains of just 0.1% apiece. On the downside, the utilities sector (-0.9%) is the weakest performer with consumer discretionary (-0.6%) and financials (-0.5%) following not too far behind.DJ30 -34.93 NASDAQ -13.80 SP500 -3.53 NASDAQ Adv/Vol/Dec 842/321.1 mln/1371 NYSE Adv/Vol/Dec 1015/100.4 mln/1672

09:45 am : The major averages slipped at the start of the session, but the S&P 500 has climbed into positive territory. The Russell 2000, which has trailed the S&P in recent days, began the session in-line with the benchmark average.

Among individual sectors, energy (+0.3%) has displayed some early strength as ConocoPhillips (COP 73.83, +0.58) and Exxon Mobil (XOM 89.64, +0.83) contribute to the early outperformance after beating earnings estimates.

On the downside, financials (-0.2%), technology (-0.1%), and utilities (-0.3%) trailed the broader market during the opening minutes.

Just released, the October Chicago PMI rose to 65.9 from 55.7 while the Briefing.com consensus expected an uptick to 53.7.DJ30 -1.41 NASDAQ +2.27 SP500 +1.74 NASDAQ Adv/Vol/Dec 1027/213.2 mln/1088 NYSE Adv/Vol/Dec 1366/70.9 mln/1264

09:15 am : [BRIEFING.COM] S&P futures vs fair value: -1.40. Nasdaq futures vs fair value: -6.00. The major averages are poised to begin today's session near their respective flat lines as the S&P 500 will look to maintain its October gain of 4.9% through the final session of the month.

In overseas news of note, Eurozone unemployment (12.2% actual versus 12.0% expected) and CPI (0.7% actual versus 1.1% consensus) came in well-below estimates, which has stoked expectations for additional liquidity provisions from the European Central Bank. On that note, governing council member Ewald Nowotny said the ECB will ensure a smooth transition once long-term refinancing operations come to an end.

In domestic news of note, weekly initial claims decreased to 340,000 from 350,000 (Briefing.com consensus 335,000). Notably, the Department of Labor said the issues with California's numbers have now been worked out.

Investors received a full slate of quarterly earnings between yesterday's close and today's opening bell. Dow component Visa (V 198.68, -5.14) holds a pre-market loss of 2.5% after reporting a bottom-line miss on below-consensus revenue. The company reaffirmed its full-year 2014 earnings and revenue guidance while the Board of Directors authorized a new repurchase program in the amount of $5.0 billion. Peer Mastercard (MA 732.00, +6.32) sports a pre-market gain of 0.9% after beating on earnings and revenue.

Also of note, shares of Facebook (FB 46.90, -2.11) are expected to open lower by 4.2% after the company reported better-than-expected Q3 results yesterday. The stock was up as much as 14.0% in initial earnings reaction, but tumbled into the red when company officials acknowledged on the conference call that a decline in daily traffic among young users has been observed.

Treasuries hover near their highs with the 10-yr yield off three basis points at 2.51%.

08:57 am : [BRIEFING.COM] S&P futures vs fair value: +0.10. Nasdaq futures vs fair value: -1.50. The S&P 500 futures hover just above fair value.

Markets across Asia were broadly lower as only India's Sensex (+0.6%) and Thailand's SET (+0.8%) saw gains. The gain in the Sensex (+0.6%) was noteworthy as the index climbed to a fresh all-time high. The Bank of Japan opined overnight, opting to keep policy on hold. The inaction did not resonate well with the Nikkei (-1.2%) as a stronger yen pressured the index. Markets in China (-0.9%) and Hong Kong (-0.4%) were lower despite efforts from the People's Bank of China to provide liquidity into the system. The PBOC injected CNY16 bln into the system through 14-day reverse repo, causing short-term rates to tumble. The 2w rate paced the decline, plunging 84 basis points to 5.51%. Data from the region showed Australian building approvals surged 14.4% month-over-month (2.9% expected) and import prices jumped 6.1% quarter-over-quarter (3.5% expected). Elsewhere, Japan's average cash earnings data was released overnight, posting a better than expected 0.1% year-over-year (-0.5% expected).

In Japan, the Nikkei settled lower by 1.2% as trade gave up Wednesday's gains. Shipping stocks were the worst performers as Nippon Yusen and Mitsui OSK Lines tumbled 8.3% and 6.6%, respectively. Elsewhere, Honda Motor sank 1.3% after failing to change its full-year earnings guidance.

Hong Kong's Hang Seng shed 0.4% as trade lingers near the September/October highs. Casino stocks lagged following yesterday's outperformance as Sands China fell 2.2% and Galaxy Entertainment shed 2.0%. Energy names were also weak as China Shenhua Energy and PetroChina lost 1.7% and 1.3%, respectively.

In China, the Shanghai Composite lost 0.9% as financials led the way lower. Bank of China Communications fell 1.9% while Citic Securities slipped 1.7%.

Core European indices are little changed while Spain's IBEX outperforms with a gain of 1.0%. In Germany, a member of the SPD party indicated an agreement has been reached with Angela Merkel's CSU/CDU alliance on a coalition government. Economic data was plentiful as Eurozone unemployment jumped to 12.2% from 12.0% (12.0% expected) while CPI came in at 0.7% year-over-year (1.1% expected, 1.1% prior). Separately, core CPI increased 0.8% year-over-year (1.0% forecast, 1.0% last). Following the disappointing data, European Central Bank governing council member Ewald Nowotny said the ECB will provide more liquidity to the eurozone. Moving to other data points, Germany's retail sales slipped 0.4% month-over-month (0.4% expected, -0.2% prior) while the year-over-year reading reflected an uptick of 0.2% (1.0% forecast, 0.4% prior). Separately, GfK Consumer Climate slipped to 7.0 from 7.1 (7.2 expected) and the import price index was unchanged month-over-month (0.1% forecast, 0.1% prior). Great Britain's Nationwide HPI rose 1.0% month-over-month (0.7% consensus, 0.9% last). French consumer spending slipped 0.1% month-over-month (0.3% expected, -0.3% previous) while PPI ticked up 0.3% month-over-month (0.2% forecast, 0.3% last). Italy's CPI slipped 0.3% month-over-month (0.4% expected, -0.3% prior) while the year-over-year reading rose 0.7% (1.2% forecast, 0.9% last). PPI was unchanged month-over-month (0.1% expected, 0.1% last) and the year-over-year reading fell 1.8% (-2.1% forecast, -2.1% prior). Spain's government budget surplus expanded to EUR3.30 billion from a deficit of EUR2.40 billion (EUR2.50 billion surplus expected) while business confidence slipped to -14 from -12 (-11 consensus).

Great Britain's FTSE is lower by 0.4% as energy names pace the decline. Petrofac trades down 2.3% and Royal Dutch Shell holds a loss of 4.8% after reporting disappointing results.

Germany's DAX is higher by 0.2% as exporters outperform. BMW, Daimler, and Volkswagen are all up between 1.1% and 2.4%. Deutsche Boerse is the weakest index component, down 3.2%.

In France, the CAC holds a modest gain of 0.5% as banks lead. BNP Paribas, Credit Agricole, and Societe Generale are all up between 2.6% and 2.8%. Energy producer Technip is the weakest index component, down 8.7% after missing third-quarter profit estimates.

In Spain, the IBEX is higher by 1.0% as financials lead. Banco de Sabadell and Banco Popular Espanol hold respective gains of 4.7% and 7.1%.

08:33 am : [BRIEFING.COM] S&P futures vs fair value: +1.00. Nasdaq futures vs fair value: +3.70. The S&P 500 futures hover near their flat line.

The latest weekly initial jobless claims count totaled 340,000, which was higher than the 335,000 that had been expected by the Briefing.com consensus. Today's tally was below the prior week count of 350,000. As for continuing claims, they rose to 2.881 million from 2.850 million.

08:05 am : S&P futures vs fair value: -0.30. Nasdaq futures vs fair value: +1.20. U.S. equity futures sport modest losses with the S&P 500 futures trading just below fair value.

Reviewing overnight developments:

Asian markets ended lower. Hong Kong's Hang Seng -0.4%, China's Shanghai Composite -0.9%, and Japan's Nikkei -1.2%.

In regional economic data:

The Bank of Japan maintained its key interest rate and made no changes to its purchasing program following last night's policy meeting. In addition, average cash earnings ticked up 0.1% year-over-year (-0.5% expected, -0.9% prior) while Manufacturing PMI improved to 54.2 from 52.5. Separately, the foreign bonds buying report indicated net inflows in the amount of JPY1.04 trillion. (JPY1.41 trillion prior). Also of note, construction orders surged 89.8% year-over-year (21.4% last) and housing starts spiked 19.4% year-over-year (12.2% forecast, 8.8% last).

Australia's Import Price Index rose 6.1% quarter-over-quarter (4.0% expected, -0.3% prior) while the Export Price Index increased 4.2% quarter-over-quarter (3.0% forecast, -0.3% last). Separately, building approvals jumped 14.4% (2.7% forecast, -1.6% prior) while private sector credit ticked up 0.3% month-over-month (0.4% forecast, 0.3% last).

Singaporean unemployment rate fell to 1.8% from 2.1% (2.1% consensus).

Hong Kong's retail sales rose 5.1% year-over-year (7.7% expected, 8.1% last).

In news:

The People's Bank of China moved to alleviate the ongoing liquidity crunch by conducting reverse repurchase operations. The two-week SHIBOR rate registered the most notable decline, falling nearly 84 basis points to 5.51%.

Core European indices are little changed while peripheral markets outperform. Germany's DAX +0.1%, Great Britain's FTSE -0.4%, and France's CAC +0.4%. Elsewhere, Italy's MIB +0.8% and Spain's IBEX +0.6%.

Economic data was plentiful:

Eurozone unemployment jumped to 12.2% from 12.0% (12.0% expected) while CPI came in at 0.7% year-over-year (1.1% expected, 1.1% prior). Separately, core CPI increased 0.8% year-over-year (1.0% forecast, 1.0% last).

Germany's retail sales slipped 0.4% month-over-month (0.4% expected, -0.2% prior) while the year-over-year reading reflected an uptick of 0.2% (1.0% forecast, 0.4% prior). Separately, GfK Consumer Climate slipped to 7.0 from 7.1 (7.2 expected) and the import price index was unchanged month-over-month (0.1% forecast, 0.1% prior).

Great Britain's Nationwide HPI rose 1.0% month-over-month (0.7% consensus, 0.9% last).

French consumer spending slipped 0.1% month-over-month (0.3% expected, -0.3% previous) while PPI ticked up 0.3% month-over-month (0.2% forecast, 0.3% last).

Italy's CPI slipped 0.3% month-over-month (0.4% expected, -0.3% prior) while the year-over-year reading rose 0.7% (1.2% forecast, 0.9% last). PPI was unchanged month-over-month (0.1% expected, 0.1% last) and the year-over-year reading fell 1.8% (-2.1% forecast, -2.1% prior).

Spain's government budget surplus expanded to EUR3.30 billion from a deficit of EUR2.40 billion (EUR2.50 billion surplus expected) while business confidence slipped to -14 from -12 (-11 consensus).

Looking at news:

In Germany, a member of the SPD party has indicated an agreement has been reached with Angela Merkel's CSU/CDU alliance on a coalition government.

In U.S. corporate news:

AmerisourceBergen (ABC 65.29, +0.07): +0.1% after beating on earnings and revenue.

Avon Products (AVP 20.40, -2.00): -8.9% in reaction to missing on earnings and revenue.

Avis Budget (CAR 28.70, 0.00): is little changed after reporting an earnings miss on above-consensus revenue.

CIGNA (CI 76.00, +1.36): +1.8% following its better-than-expected earnings on above-consensus revenue. The company issued full-year 2013 earnings guidance above consensus.

ConocoPhillips (COP 74.11, +0.86): +1.2% after beating bottom-line estimates by two cents.

Expedia (EXPE 58.81, +8.85): +17.7% after reporting earnings and revenue ahead of analyst estimates. Following the report, Bank of America/Merrill Lynch upgraded the stock to 'Buy' from 'Neutral.'

Facebook (FB 50.44, +1.43): +2.9% following its better-than-expected earnings and revenue. The stock was up as much as 14.0% in after-hours action, but surrendered most of the advance during the earnings conference call after company officials said a decline in daily usage among young users has been observed.

MetLife (MET 48.30, -0.70): -1.4% after missing revenue estimates.

Visa (V 197.50, -6.32): -3.1% following its earnings miss on below-consensus revenue. The company reaffirmed its full-year 2014 earnings and revenue guidance while the Board of Directors has authorized a new repurchase program in the amount of $5.0 billion.

Weekly initial claims will be reported at 8:30 ET and the October Chicago PMI will be released at 9:45 ET.

07:19 am : [BRIEFING.COM] S&P futures vs fair value: -2.30. Nasdaq futures vs fair value: -2.50.

07:19 am : Nikkei...14327.94...-174.40...-1.20%. Hang Seng...23206.37...-97.70...-0.40%.

07:19 am : FTSE...6744.67...-33.00...-0.50%. DAX...8988.47...-21.80...-0.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com HomepageMarket Update