Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

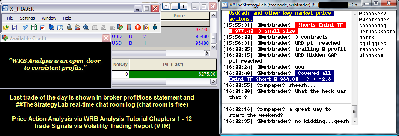

Attachment:

062813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6275.00.png [ 81.01 KiB | Viewed 533 times ]

062813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6275.00.png [ 81.01 KiB | Viewed 533 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$4400.00 dollars or +44.00 points, Emini ES ($ES_F) futures @

$1875.00 dollars or +37.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6275.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the free

##TheStrategyLab chat room. You can read

today's ##TheStrategyLab trading chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=118&t=1541 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=212&t=1853 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

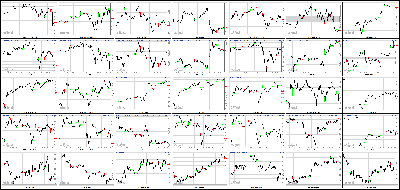

Stocks: Rocky End To A Positive Quarter Attachment:

062813-Key-Price-Action-Markets.png [ 515.8 KiB | Viewed 556 times ]

062813-Key-Price-Action-Markets.png [ 515.8 KiB | Viewed 556 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Stocks wrapped up the second quarter with all three indexes recording gains of between 2% and 5%, despite a challenging June.

The Dow, S&P, and Nasdaq are all up between 12% and 14% as the first half of the year ends.

June was not as sunny. All indexes ended the month down roughly 1%, making June the first losing month this year.

It wasn't the June swoon, but perhaps the June jitterbug? The Dow has swung more than 100 points on 15 out of the 20 trading days this month.

* Big winners on Wall Street are yesterday's dogsFears of Fed taper: Fed officials have been in major damage control mode, since Fed chairman Ben Bernanke kicked off tumult in the stock, bond and gold markets last week. He said the central bank could wind down its stimulus program later this year, if the economy continues to improve.

Fed governor Jeremy Stein, while trying to allay investor fears, appeared to have inadvertently stoked them Friday. He said the Fed could "hypothetically" consider tapering its bond buying in September.

* Fed officials in damage control modeAt the same time, he said investors were overreacting, but that didn't seem to make a dent in sentiment.

The Dow Jones industrial average dipped 114 points, or 0.8%, Friday. The S&P 500 lost 0.4%. Only the Nasdaq gained ground, moving just slightly positive.

All three indexes finished the week higher.

Richmond Fed president Jeremy Lacker said the Fed will keep buying bonds, "though at a decreasing rate over the next year."

Bond, gold carnage: The mere mention of any end to bond buying has recently sent bond investors scrambling for the exits. The yield on the 10-year Treasury note hit 2.65% earlier this week -- its highest level since August 2011 and well above the 1.6% in early May. The yield hovered around 1.5% at the end of Friday's trading day.

Gold prices have been slammed as well. Gold rose 1% Friday, but the precious metal slid 13% this month.

As volatility rose in June, so did the CBOE Volatility Index (VIX). The VIX rose 4% this month, and 37% for the quarter.

CNNMoney's Fear and Greed Index has had a wild quarter as well. A month ago it was in greed and even nudged into extreme greed in mid-May. But once Bernanke hinted at tapering, the needle quickly shot over to extreme fear.

* Fear & Greed Index slides back into extreme fearBlackBerry bombs: Embattled mobile company BlackBerry (BBRY) reported first-quarter results Friday that fell short of analysts' forecasts. Shares tumbled 25%.

Nike (NKE, Fortune 500) reported better-than-expected earnings, but analysts remain worried about Nike's ability to cut costs.

Shares of Accenture (ACN) moved lower after the consulting firm slashed expectations for its year-end results.

Shares of Pfizer (PFE, Fortune 500) edged higher after the drug maker announced late Thursday that it would increased its share buyback program by $10 billion.

The restaurant chain Noodles & Co (NDLS)'s stock more than doubled from its $18 IPO price.

Market Update

Market Update 4:15 pm : Stocks concluded their down week on a lower note as the S&P 500 shed 0.4%.

Equities slipped out of the gate amid weakness in Treasuries. The 10-yr note sold off into the cash session open before erasing most of its losses. The benchmark 10-yr yield ended higher by two basis points at 2.493%.

A disappointing Chicago PMI report for June (51.6 actual, 55.5 Briefing.com consensus, 58.7 prior) also contributed to the early weakness, but stocks were able to find support shortly thereafter.

Today's session lows coincided with the release of a better-than-expected final University of Michigan Consumer Sentiment Index (84.1 final, 82.7 consensus, 82.7 preliminary).

Stocks spent the following hour in a steady climb, allowing the S&P to erase its opening losses. However, the early buying interest fizzled out after the benchmark average returned to its flat line, where it held until the closing minutes of the session.

The final five minutes of action saw the index return into the red as the small cap Russell 2000 index underwent its annual rebalancing.

The S&P was anchored to its unchanged level for most of the afternoon as financials and technology weighed. The financial sector ended with a loss of 0.7% while the tech space shed 0.4%.

While the tech sector was able to settle above its lows, not all components were as fortunate. Accenture (ACN 71.96, -8.26) tumbled 10.3% after its earnings beat was overshadowed by below-consensus revenue as well as downside fourth quarter revenue guidance. Separately, BlackBerry (BBRY 10.46, -4.02) plunged 27.8% after the company reported disappointing first quarter earnings and revenue. In addition, BB10 shipments of 2.7 million disappointed as investors expected BlackBerry to ship about 3.5 million units of its latest device.

On the flip side, discretionary shares and utilities ended in positive territory. The discretionary sector received a boost from retailers after Finish Line (FINL 21.86, +0.66) surprised to the upside with its earnings and revenue. Meanwhile, homebuilders kept the discretionary space from logging further gains. Most major builders settled in the red while the iShares Dow Jones US Home Construction ETF (ITB 22.38, -0.37) shed 1.6%.

Also of note, a 0.4% advance in utilities extended the sector's weekly gain to 3.0%, placing it atop this week's leaderboard. Meanwhile, the materials sector was the weakest group of the week, ending with a loss of 1.5%. However, gold miners had a strong showing today as the Market Vectors Gold Miners ETF (GDX 24.49, +1.70) surged 7.5%. On a related note, gold futures gained 1.6% to $1230.70 per ounce while silver futures jumped 5.6% to $19.60 per ounce.

Week in Review: S&P 500 Tests 100-Day Moving Average

On Monday, the stock market began the week on a fitful note as rising interest rates at home and falling equity markets abroad conspired to keep the major averages in negative territory throughout the day. The S&P 500 registered its first close below its 100-day moving average this year. Overseas, the drop in China was attributed to a growing sense of angst that a liquidity crisis and credit crunch are brewing there. The growth concerns weighed heavily on the cyclical sectors throughout the day. Financials (-1.8%) led the losses and were joined by materials (-1.7%), industrials (-1.7%), energy (-1.5%), and technology (-1.4%) as the worst-performing areas.

Equities ended Tuesday's session near their highs, but were unable to erase their Monday losses. The S&P 500 climbed 1.0% as all ten sectors ended with gains. The bulk of the advance occurred in the first 90 minutes of the session amid a global rebound. Interestingly, two rate-sensitive sectors vaulted to the top of this month's leaderboard despite the continued climb in Treasury yields. The telecom services sector rose 2.0%, which turned its month-to-date loss to a gain of 1.0%.

Wednesday began on an upbeat note despite some disappointing economic news. The final first quarter GDP reading was revised down to 1.8% from 2.4%. Typically, revisions to GDP in the third estimate are very minor. The large decline in this report was very unusual and caught all economists by surprise. Most of the downward revision came from consumption in services. In the previous estimate, services spending increased 3.1%. That was revised down to 1.7% growth and contributed 0.6 percentage points less to GDP growth. Stocks received this news in stride as sluggish growth suggests the Federal Reserve is less likely to withdraw its support from the markets. To that end, the Treasury complex received an aggressive bid immediately after the GDP revision crossed the wires. The benchmark 10-yr yield ended lower by seven basis points at 2.542%.

On Thursday, the S&P 500 settled higher by 0.6% as nine sectors posted gains. Equities were off to the races at the sound of the opening bell, aided by the personal income report, which pointed to an increase of 0.5% in May. The Briefing.com consensus expected personal income to rise 0.2%. Stocks received a secondary boost from the pending home sales report as May sales rose 6.7% (1.5% consensus). The S&P notched its high of 1620 shortly after the market digested the latest housing data point. However, the index was unable to rise above that level as the 20- and 50-day moving averages served as resistance at the session high.DJ30 -114.89 NASDAQ +1.38 SP500 -6.92 NASDAQ Adv/Vol/Dec 1322/2.15 bln/1180 NYSE Adv/Vol/Dec 1541/1.75 bln/1488

3:35 pm :

Aug gold rose for the first time this week despite a stronger dollar index. The yellow metal rallied sharply into positive territory after trading as low as $1186.00 per ounce in morning action. It settled 1.1% higher at $1224.40 per ounce, slightly below its session high of $1228.90 per ounce. Despite today's advance, gold suffered its biggest quarterly loss on record according to various media outlets, declining by over 23% since Mar 28, 2013.

Sep silver also rose alongside gold today as it lifted off its session low of $18.50 per ounce. It brushed a session high of $19.57 per ounce moments before closing with a 4.8% gain at $19.45 per ounce. The metal, however, declined by 31.6% over the quarter.

Aug crude oil fell for the first time this week despite spending most of its pit session chopping around slightly above the unchanged line.

The energy component brushed a session high of $97.63 per barrel in morning action but sold off into negative territory as it headed into the close. Crude oil settled the session 0.5% lower at $96.52 per barrel, booking a 1.1% loss for the quarter.

Aug natural gas advanced to a session high of $3.61 per MMBtu after lifting from its session low of $3.53 per MMBtu in morning action. However, it lost momentum ahead of the close and slipped back into negative territory where it settled with a 0.6% loss at $3.56 per MMBtu. Natural gas declined by 13.8% over the quarter.

DJ30 -31.95 NASDAQ -18.32 SP500 +1.95 NASDAQ Adv/Vol/Dec 1388/1351.1 mln/1070 NYSE Adv/Vol/Dec 1807/482 mln/1196

3:00 pm : The S&P 500 sits on its flat line as today's session enters its final hour.

Today's session in the foreign exchange market has been a bit more active than yesterday's affair. The Dollar Index is on track for its sixth gain in eight days after today's bid reclaimed the 83.00 level. Currently, the index is poised for its best close in a month. Today's dollar strength has pressured the British pound as well as the euro.

Pound/dollar is lower by 50 pips at 1.5210 as sellers remain in control for a fourth session. Notably, the Bank of England will have a different look on Monday as former Bank of Canada head Mark Carney takes the reins from outgoing Governor Mervyn King. British data scheduled for a Monday release is limited to Manufacturing PMI and net lending to individuals.

Elsewhere, Australian dollar/U.S. dollar is lower by 120 pips near .9150 as trade breaks down to a fresh 33-month low amid ongoing concerns of a disruption in the Chinese economy. The pair now trades 1400 pips below the April highs. The Australian dollar could display some volatility Sunday night when China reports its Manufacturing PMI and the final HSBC Manufacturing PMI.DJ30 -56.72 NASDAQ +10.97 SP500 -0.69 NASDAQ Adv/Vol/Dec 1377/1.21 bln/1069 NYSE Adv/Vol/Dec 1708/422.1 mln/1297

2:30 pm : The S&P 500 has ticked to a fresh high in the 1615 area before slipping back towards its flat line. Outside of the early morning rebound, buying interest has been very limited in afternoon action.

With 90 minutes left in today's session only 381 million shares have changed hands on the floor of the New York Stock Exchange. However, a volatile close is expected as the small cap Russell 2000 index undergoes its annual rebalancing.

Although the past three sessions saw the S&P register solid gains, those advances have not been able to fully erase Monday's loss. At its current levels, the benchmark average is poised to end the week lower by 1.0%.DJ30 -41.55 NASDAQ +12.28 SP500 +0.21 NASDAQ Adv/Vol/Dec 1398/1.09 bln/1047 NYSE Adv/Vol/Dec 1717/383.7 mln/1273

2:00 pm : Afternoon action has not produced much change in the major averages. The S&P 500 continues to hug its flat line while the Nasdaq outperforms with a slim gain of 0.4%.

Although the technology sector is among today's laggards, the tech-heavy Nasdaq has received some support from companies specializing in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 174.90, +0.51) is higher by 0.3%.

Also of note, gold futures have extended their gains. The yellow metal trades higher by 1.2% at $1226.30 per ounce after being down nearly 2.0%. On a related note, silver futures trade with a gain of 5.2% at $19.51 per ounce.DJ30 -38.10 NASDAQ +11.95 SP500 +0.85 NASDAQ Adv/Vol/Dec 1332/990.9 mln/1102 NYSE Adv/Vol/Dec 1698/347.8 mln/1267

1:30 pm : The major averages remain mixed in early afternoon trading. The S&P 500 is essentially flat for the day, so it will need to get going if it wants to end June with another monthly gain. It will take a 1.09% advance today to do it.

Looking at the month as a whole to this point, the countercylical sectors generally fared better than the cyclical sectors. The consumer discretionary sector (+1.0% for the month) snuck in among the countercyclical sectors as a relative strength leader, yet the cyclical sectors for the most part have been the weak links this month.

The worst-performing sector in June has been the basic materials sector (-4.2%) followed by the information technology sector (-3.6%) and then the energy sector (-1.6%). On the flip side, the telecom services sector (+2.4%) has led all sectors this month.DJ30 -43.20 NASDAQ +7.79 SP500 -0.48 NASDAQ Adv/Vol/Dec 1240/911 mln/1168 NYSE Adv/Vol/Dec 1598/320 mln/1370

1:00 pm : At midday, the S&P 500 trades lower by 0.2%.

Equities slipped out of the gate and continued their slide through the first 30 minutes of action. A disappointing Chicago PMI report (51.6 actual, 55.5 Briefing.com consensus, 58.7 prior) for June contributed to the early weakness, but stocks found support shortly thereafter.

In addition, the 10-yr note displayed early weakness, which also pressured equities. Currently, the benchmark 10-yr yield is higher by six basis points at 2.529%.

Today's lows in the S&P coincided with the release of a better-than-expected final University of Michigan Consumer Sentiment Index (84.1 final, 82.7 consensus, 82.7 preliminary).

Stocks spent the following hour in a steady climb, but the S&P was only able to make a brief appearance in positive territory before slipping back into the red due to significant weakness in financials and technology.

The financial sector trades lower by 0.4% as most major components register losses.

Elsewhere, the technology space has been pressured by Accenture (ACN 71.81, -8.41) after the company's earnings beat was overshadowed by below-consensus revenue as well as downside fourth quarter revenue guidance.

While most sectors trade with losses, utilities and the discretionary space hover near their highs.

The discretionary sector has been supported by retailers after Finish Line (FINL 22.25, +1.05) delivered a solid earnings report. However, homebuilders have not contributed to the sector's strength. The iShares Dow Jones US Home Construction ETF (ITB 22.52, -0.23) trades lower by 1.0%. The homebuilder ETF has had a rough June, and is down 7.4% month-to-date.

Today's session is likely to experience a volatile close as the small cap Russell 2000 index undergoes its annual rebalancing.DJ30 -57.33 NASDAQ +1.54 SP500 -2.77 NASDAQ Adv/Vol/Dec 1138/845.2 mln/1260 NYSE Adv/Vol/Dec 1456/297.1 mln/1494

12:30 pm : After holding near its flat line for about an hour, the S&P 500 has returned into the red.

Utilities and discretionary stocks have been able to withstand the broader market weakness as both groups remain near their highs. The discretionary space has been supported by retailers after Finish Line (FINL 22.08, +0.88) delivered a solid earnings report.

Although the discretionary sector sits near its highs, homebuilders have not contributed to the strength. The iShares Dow Jones US Home Construction ETF (ITB 22.55, -0.20) trades lower by 0.9%. The homebuilders ETF has had a rough June, and is down 7.4% month-to-date.DJ30 -67.39 NASDAQ -0.54 SP500 -3.86 NASDAQ Adv/Vol/Dec 1104/774.9 mln/1290 NYSE Adv/Vol/Dec 1409/272.9 mln/1516

12:00 pm : The S&P 500 has spent the past hour within just a couple points of its flat line.

With regard to individual sectors, utilities and the discretionary space hold gains near 0.6% while financials and technology trade lower by 0.3% and 0.4%, respectively. The remaining six groups are little changed.

Treasuries were in focus this morning when the complex fell to its lows. However, Treasuries have regained a good portion of their losses. The benchmark 10-yr yield remains higher by three basis points at 2.499%.DJ30 -19.35 NASDAQ +5.58 SP500 -0.03 NASDAQ Adv/Vol/Dec 1174/694.4 mln/1188 NYSE Adv/Vol/Dec 1504/243.3 mln/1401

11:30 am : The S&P 500 has made a brief appearance in positive territory before returning into the red. Utilities and discretionary stocks continue to hover near their highs while financials and technology pressure the broader market.

Most major banks trade in the red while the financial sector holds a loss of 0.4%.

Elsewhere, the technology space has been pressured by Accenture (ACN 70.24, -9.98) after the company's earnings beat was overshadowed by below-consensus revenue as well as downside fourth quarter revenue guidance.DJ30 -32.26 NASDAQ +4.09 SP500 -1.24 NASDAQ Adv/Vol/Dec 1174/604.2 mln/1148 NYSE Adv/Vol/Dec 1459/212.5 mln/1427

10:55 am : The S&P 500 has been able to climb off its lows, but the index continues to hover in the red. Of the ten economic sectors, the utilities space is the top performer, sporting a gain of 0.6%. The discretionary sector is the only other advancer, trading higher by 0.5%.

Discretionary stocks have received a boost from Finish Line's (FINL 22.02, +0.82) better-than-expected earnings. Finish Line trades higher by 4.0% while the SPDR S&P Retail ETF (XRT 76.90, +0.33) adds 0.4%.

Also of note, recent action saw gold and silver futures register significant gains. Gold futures jumped over $30 off their lows to $1213.50 per ounce while silver futures trade higher by 3.8% at $19.25 per ounce. On a related note, the Market Vectors Gold Miners ETF (GDX 23.78, +0.99) trades up 4.3%.DJ30 -42.01 NASDAQ -1.02 SP500 -1.55 NASDAQ Adv/Vol/Dec 1058/478.2 mln/1220 NYSE Adv/Vol/Dec 1219/172.4 mln/1630

10:35 am : Precious metals just rallied sharply, pushing gold and silver prices to new highs for the day. Gold surged back above $1200 and silver moved back above $19. In current trade, Aug gold is +0.3% at $1215/oz and July silver is +4.3% at $1935/oz.

Energy is mixed with crude oil higher and natural gas in the red. Crude oil rallied back into positive territory in recent trade after hitting a new LoD. Aug crude is now +0.3% at $97.29/barrel. Aug natural gas is currently -1.2% at $3.54/MMBtu.DJ30 -75.68 NASDAQ -4.15 SP500 -4.87 NASDAQ Adv/Vol/Dec 856/379.0 mln/1378 NYSE Adv/Vol/Dec 1028/144 mln/1792

10:00 am : The major averages have continued their push lower. The S&P 500 trades with a loss of 0.6% as financials and technology lead to the downside.

The University of Michigan's final June Consumer Sentiment Survey rose to 84.1 from the 82.7 that was posted in the preliminary Survey. The Briefing.com consensus expected the reading would remain at 82.7.DJ30 -117.70 NASDAQ -15.24 SP500 -10.29 NASDAQ Adv/Vol/Dec 707/234.7 mln/1478 NYSE Adv/Vol/Dec 631/91.7 mln/2146

09:45 am : The major averages have slid to their lows in reaction to the June Chicago PMI, which fell to 51.6 from 58.7. This was worse than the 55.5 expected by the Briefing.com consensus.

Cyclical sectors are among the early laggards while the health care space outperforms with a slim gain of 0.2%.

Also of note, the 10-yr note trades near its lows with its yield higher by five basis points at 2.525%.

Today's session is likely to experience a volatile close as the small cap Russell 2000 index undergoes its annual rebalancing.DJ30 -66.06 NASDAQ -7.01 SP500 -5.47 NASDAQ Adv/Vol/Dec 723/154.2 mln/1381 NYSE Adv/Vol/Dec 827/67.2 mln/1864

09:15 am : [BRIEFING.COM] S&P futures vs fair value: -3.80. Nasdaq futures vs fair value: -8.80. With 15 minutes left to go before the start of today's cash session, the S&P 500 futures trade with a slim loss of 0.2%. Futures displayed earlier gains but slid into the red in a move coinciding with weakness in the Treasury market. The 10-yr note has seen some heavy selling in the past hour, sending its yield higher by six basis points to 2.528%.

Among earnings of note, BlackBerry (BBRY 11.10, -3.38) trades lower by 23.3% on heavy pre-market volume after the company reported disappointing first quarter earnings and revenue. The company's BB10 shipments of 2.7 million disappointed as investors expected BlackBerry to ship about 3.5 million units.

Today's session is likely to experience a volatile close as the small cap Russell 2000 index undergoes its annual rebalancing.

08:59 am : [BRIEFING.COM] S&P futures vs fair value: -2.60. Nasdaq futures vs fair value: -6.00.

The S&P 500 futures trade lower by 0.1%.

It was a sea of green across Asia as all of the major bourses, aside from Australia's ASX (-0.2%) finished in positive territory. Strong gains across the region were paced by Japan's Nikkei (+3.5%), but almost the entire region was higher by at least 1.5%. The Nikkei's gains came following mostly better than expected data as it appears Abenomics is beginning to take hold. Meanwhile, China's Shanghai Composite (+1.5%) surged off its lowest levels since January 2009 after a PBOC official commented the economy is now in check. The soothing words helped push the overnight SHIBOR back below 5.0%. Elsewhere, peripheral markets remained strong with Indonesia's Jakarta Composite (+3.1%) and the Philippines Psei (+2.2%) setting the pace. The Philippines' Psei is up nearly 12% over the past three sessions. Data from the region saw Japan's household spending miss estimates (-1.6% year-over-year actual versus 1.5% expected) and Tokyo Core CPI (0.2% year-over-year actual versus 0.2% expected) meet expectations while both retail sales (0.8% year-over-year actual versus 0.1% expected) and preliminary industrial production (2.0% month-over-month actual versus 0.2% expected) beat. Also, Thailand's industrial production plunged 7.8% year-over-year as its current account deficit narrowed to $1.05 billion ($1.3 billion previous).

In Japan, the Nikkei rose 3.5% as trade closed at a one-month high. Real estate shares were once again strong as Mitsui Fudosan jumped 4.6% to lead the space higher. Financials were also bid with Mitsubishi UFJ Financial and Mizuho Financial both adding at least 4.0%.

Hong Kong's Hang Seng finished higher by 1.8% as shares rallied for a fourth day. Financials continued their recent advance with ICBC climbing 2.7%. Meanwhile, coal-based China Shenhua Energy slumped almost 2.0% as coal prices fell to their lowest in five years.

In China, the Shanghai Composite settled higher by 1.5% as shares gained for the first time in three days. Property developers and financials were among the leaders with Poly Real Estate surging 6.8% and China Minsheng Bank adding 2.3% to finish among the leaders of their respective sectors.

Major European indices trade in the red despite showing earlier gains. Regional economic data was plentiful as Germany's retail sales climbed 0.8% month-over-month (0.2% expected, -0.1% prior). French PPI slid 1.2% month-over-month (-0.3% expected, -1.2% prior) while consumer spending rose 0.5% month-over-month (-0.1% expected, -0.5% previous). Great Britain's Nationwide HPI increased 0.3% month-over-month (0.3% forecast, 0.4% previous) while the Index of Services rose 0.2%, as expected (0.6% previous). Elsewhere, Italian CPI rose 0.3% month-over-month (0.2% expected, 0.0% prior) while PPI eased 0.1% month-over-month (-0.1% expected, -0.4% previous). Lastly, Business Confidence climbed to 90.2 from 88.7 (89.0 consensus).

Reports out of German newspaper Sueddeutsche Zeitung suggest the European Central Bank is considering a bond-buying program similar to the Fed's quantitative easing. These reports have been promptly refuted by an ECB spokesman, who said the article was 'completely wrong.' Also of note, Latvia is in the process of clearing the final hurdles in its bid to become part of the Eurozone starting on January 1, 2014.

Great Britain's FTSE is lower by 0.2%. Miners are among the decliners as Antofagasta, Eurasian Natural Resources, and Fresnillo, hold losses between 1.5% and 3.2%. On the upside, Schroders trades higher by 4.2% following supportive comments from Exane BNP Paribas.

In Germany, the DAX is off by 0.6% with SAP leading to the downside. The software company is lower by 2.8% after Accenture's lower-than-expected revenue forecast cast some doubt on the strength of demand for SAP products.

France's CAC trades with a loss of 0.7% as financials weigh. BNP Paribas, Credit Agricole, and Societe Generale are all down between 1.6% and 2.8%.

08:32 am : [BRIEFING.COM] S&P futures vs fair value: +0.30. Nasdaq futures vs fair value: -1.50. After the past three sessions saw the S&P 500 gap up at the open, today's affair appears poised for a start near yesterday's closing levels. Currently, the S&P futures are little changed after showing earlier gains of 0.3%. Overseas action has been mixed as Asian markets ended broadly higher while European indices hover in the red.

Also of note, the 10-yr note recently slipped to its lows, causing its yield to rise two basis points to 2.499%

In notable pre-market movers, Blackberry (BBRY 11.44, -3.04) trades lower by 21.3% on heavy pre-market volume after the company reported disappointing first quarter earnings and revenue. Notably, the company's smartphone shipments of 6.8 million fell well below the expected 7.6 million units.

08:00 am : [BRIEFING.COM] S&P futures vs fair value: +4.50. Nasdaq futures vs fair value: +6.00.

U.S. equity futures hover near their pre-market highs with the S&P 500 futures up 0.3%.

Looking at overnight developments:

Asian markets ended the week on a positive note. China's Shanghai Composite rose 1.5% while Hong Kong's Hang Seng added 1.8%, and Japan's Nikkei advanced 3.5%.

In regional economic data:

Japan's Manufacturing PMI rose to 52.3 from 51.5. Meanwhile, industrial production increased 2.0% month-over-month (0.2% expected, 0.9% prior). Household spending declined 1.6% year-over-year (1.4% expected, 1.6% prior) while retail sales rose 0.8% year-over-year (0.1% expected, -0.2% prior). The national CPI ticked down 0.3% (-0.4% expected, -0.7% previous) while Tokyo CPI was unchanged (0.1% expected, -0.2% prior). Construction orders surged 26.0% year-over-year (2.0% prior) while housing starts jumped 14.5% year-over-year (6.2% expected, 5.8% previous). Lastly, the unemployment rate held steady at 4.1% (4.0% forecast).

South Korea's industrial production declined 1.4% year-over-year (0.8% expected, 1.6% prior) while the services sector output rose 0.2% month-over-month (0.40% prior). Also of note, retail sales ticked down 0.2% month-over-month (0.2% expected, -0.5% prior).

Looking at news:

In China, the overnight Shanghai Interbank Offered Rate (SHIBOR) declined 62 basis points to 4.94% while the one-week rate eased 52 basis points to 6.16%.

Reports out of the Chinese press indicate Beijing may loosen financing rules for property companies.

Major European indices trade in mixed fashion as midday nears. Great Britain's FTSE is higher by 0.1%, Germany's DAX trades down 0.2%, and France's CAC is lower by 0.3%.

Investors received a fair share of economic data:

Germany's retail sales climbed 0.8% month-over-month (0.2% expected, -0.1% prior).

French PPI slid 1.2% month-over-month (-0.3% expected, -1.2% prior) while consumer spending rose 0.5% month-over-month (-0.1% expected, -0.5% previous).

Great Britain's Nationwide HPI increased 0.3% month-over-month (0.3% forecast, 0.4% previous) while the Index of Services rose 0.2%, as expected (0.6% previous).

Italian CPI rose 0.3% month-over-month (0.2% expected, 0.0% prior) while PPI eased 0.1% month-over-month (-0.1% expected, -0.4% previous). Lastly, Business Confidence climbed to 90.2 from 88.7 (89.0 consensus).

In news:

Reports out of German newspaper Sueddeutsche Zeitung suggest the European Central Bank is considering a bond-buying program similar to the Fed's quantitative easing. These reports have been promptly refuted by an ECB spokesman, who said the article was 'completely wrong.'

Latvia is in the process of clearing the final hurdles in its bid to become part of the Eurozone starting on January 1, 2014.

In U.S. corporate news:

Blackberry (BBRY 11.62, -2.86) trades lower by 19.5% on heavy pre-market volume after the company reported disappointing first quarter earnings and revenue. Notably, the company's smartphone shipments of 6.8 million fell well below the expected 7.6 million units.

Finish Line (FINL 21.56, +0.36) is higher by 1.7% after beating on earnings and revenue. In addition, the company guided full-year earnings below analyst expectations.

Nike (NKE 61.49, -0.83) trades down 1.3% after reporting an earnings beat on in-line revenue.

June Chicago PMI and the final reading of the June Michigan Consumer Sentiment Survey will cross the wires at 9:45 and 9:55 ET, respectively.

06:52 am : [BRIEFING.COM] S&P futures vs fair value: +3.50. Nasdaq futures vs fair value: +5.00.

06:52 am : Nikkei...13677.32...+463.80...+3.50%. Hang Seng...20803.29...+363.20...+1.80%.

06:52 am : FTSE...6236.95...-6.50...-1.00%. DAX...7970.24...-20.50...-0.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage