Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Quote:

No trades today due to personal day off to have fun with the kids.

Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points, EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks and Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $0.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the free

##TheStrategyLab chat room. You can read

today's ##TheStrategyLab trading chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=117&t=1518 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=209&t=1820 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

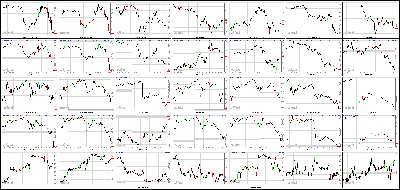

Stocks End Strong May With Sell-Off Attachment:

053113-Key-Price-Action-Markets.png [ 537.19 KiB | Viewed 469 times ]

053113-Key-Price-Action-Markets.png [ 537.19 KiB | Viewed 469 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

A strong month on Wall Street ended on a weak note Friday after a late-day sell-off sent stocks down more than 1%.

The Dow Jones industrial average fell 209 points, or 1.3%, with most of the selling in the final hour of trading. The S&P 500 sank 1.4% and Nasdaq slid 1%.

Despite Friday's losses, all three indexes ended May in the black. The Dow and S&P 500 both gained about 2%, while the Nasdaq advanced nearly 4%.

It's the first time the Dow has ended higher in May since 2009, and marks the sixth monthly gain for the index. So far this year, the major gauges are all up about 16%.

Hewlett-Packard (HPQ, Fortune 500) was the best performing blue chip in May. Shares of the PC maker rose nearly 20% this month. Cisc (CSCO, Fortune 500)o and JPMorgan (JPM, Fortune 500) have also logged double-digit percentage gains.

The main laggards were safe-haven stocks that investors had flocked to earlier this year because they pay dividends. Telecoms Verizon (VZ, Fortune 500) and AT&T (T, Fortune 500) were the worst Dow performers this month, along with consumer staples McDonalds (MCD, Fortune 500) and Coca-Cola (KO, Fortune 500).

The rush out of safe haven investments has also hurt the bond market. Yields on the 10-year Treasury note rose to a high of 2.2% earlier this week, up from about 1.6% at the end of April.

T is for Taper. The jump in Treasury yields, which rise when prices fall, came as investors brace for a potential slowdown in the Federal Reserve's bond buying campaign.

Fed chairman Ben Bernanke caused some confusion this month after he told lawmakers that withdrawing monetary stimulus too soon would jeopardize the economic recovery. Later, he said the Fed could decide to slow the pace of its bond buying at one of its next few meetings, depending on how the economy performs.

"The bond market suffered through another week of tapering tantrums," said Anthony Valeri, fixed income strategist for LPL Financial. "Ben Bernanke did little to clear the uncertainty over the timing of reducing, or tapering, bond purchases."

E is for Economy. Some investors say concerns about the Fed tapering are overblown, since any reduction in bond buying would signal that the economy is improving.

While overall economic growth remains sluggish, investors have been encouraged by a robust housing market and signs that consumers are becoming more confident.

An index of consumer sentiment rose in May to the highest level in nearly six years. The final reading of the Reuters/University of Michigan index showed that consumers are becoming more optimistic about the economy.

But a separate report Friday showed that personal income and spending both fell in April, surprising economists who had predicted a rise.

* The dividend craze may be overMeanwhile, the Chicago Purchasing Managers' Index bounced back in April, rising to the highest level since March 2012.

"Over the past few years, we've seen the economy slow a bit in spring, but we haven't seen that to the same degree this year," said Joel Huffman, a managing director at The Private Client Reserve of U.S. Bank in Milwaukee. "That has helped the market."

Huffman added that stocks could continue to move higher as corporate profits rise along with the economy. But he acknowledged that the market remains vulnerable to a correction given the run stocks have had so far this year.

"Corporate profits have been positive, but stock prices have gone up more than profits," he said. "A correction of 5% to 10% is certainly within reason."

* Best deals in investingD is for doughnuts. In corporate news Friday, Krispy Kreme (KKD) said sales and earnings jumped in the first quarter, sending shares of the doughnut maker up 13%.

Lions Gate (LGF) shares rose after the media company said sales jumped 71% in the past fiscal year, helped by movies in the teen-oriented "Hunger Games" and "Twilight" franchises.

Shares of Palo Alto Networks (PANW) plunged after the technology company swung to a big loss in the most recent quarter.

Nasdaq said Netflix (NFLX) will join the Nasdaq-100 (NDX) on June 6, replacing healthcare supplier Perrigo (PRGO).

European markets took a tumble, but ended off the lows of the day. The London stock market fell nearly 1%, while indexes in France and Germany had smaller losses.

Unemployment in the troubled eurozone region hit a record high of 12.2% last month, according to the latest statistics from Eurostat.

Asian markets ended the week with mixed results. The Nikkei advanced by 1.4%, rebounding from Thursday's steep decline brought on by mounting concerns over the country's economic turnaround plan.

Market Update

Market Update 4:10 pm : The major averages ended on their lows as afternoon selling caused the S&P 500 to settle lower by 1.4%.

Equities saw losses in the opening minutes of the session as cautious overseas action kept buyers at bay. Contributing to the overseas softness was chatter questioning the strength of tonight's manufacturing PMI report out of China.

Shortly after the open, the key indices were able to erase most of their early losses in reaction to a pair of better-than-expected economic data points.

The Chicago PMI jumped to its highest level since March 2012 as the May print of 58.7 followed April's contractionary reading of 49.0. The large increase was fueled by an improvement in all of the key subcomponents as employment, order backlogs, production, and new orders all posted notable gains.

Separately, the final reading of the May University of Michigan Consumer Sentiment Survey moved up to 84.5, its best level since July 2007. The Briefing.com consensus expected no change from the preliminary reading of 83.7.

The positive surprises gave a brief boost to equities, but failed to spark a sustained rally as the major averages hovered near yesterday's closing levels until late afternoon selling took hold.

All ten sectors settled in the red as two defensive groups, consumer staples and health care, led to the downside. Most staple components registered losses and Dow member Procter & Gamble (PG 76.80, -2.29) fell 2.9%. Consumer staples endured selling pressure throughout the week as the group declined 3.2%, which erased its May gain.

Elsewhere, the health care sector fell 2.2% and trimmed its year-to-date gain to 20.1%, surrendering its spot atop this year's sector leaderboard to financials.

Financials were mixed in early action until afternoon selling splashed the component list with a wide-ranging shade of red, leaving Morgan Stanley (MS 25.90, +0.08) as the lone advancer. Even with today's 1.6% loss, the financial sector ended the week with a gain of 5.9%.

Technology stocks also enjoyed a strong week, but unlike financials, the group held up relatively well through the selloff. The relative strength of major components like Apple (AAPL 449.74, -1.84), IBM (IBM 208.02, -1.34), and Intel (INTC 24.28, +0.07) overshadowed the weakness in biotechnology and chipmakers. The iShares Nasdaq Biotechnology ETF (IBB 179.50, -3.73) fell 2.0% while the PHLX Semiconductor Index shed 1.2%.

Today's afternoon selling caused the CBOE Volatility Index (VIX 16.25, +1.72) to jump to its highest level since April 19 as market participants raised their near-term volatility expectations.

Looking at today's remaining economic data reveals a disappointment in the Personal Income and Spending report for April. Income was flat and spending declined 0.2% while the Briefing.com consensus expected both measures to be up 0.1%. Core PCE was also flat compared to a 0.1% increase in March.

Personal income for March was revised up to 0.3% from 0.2% while spending was revised down to 0.1% from 0.2%.

On Monday, April construction spending and the May ISM Index will be released at 10:00 ET while auto and truck makers will be reporting their May sales throughout the day.

Week in Review: Choppy Week Leaves S&P in the Red

On Monday, equity and bond markets were closed in observance of Memorial Day.

Tuesday ended with solid gains for the major indices as the Dow Jones Industrial Average logged its 20th consecutive advance on a Tuesday. The early action saw nine of ten sectors register gains of at least 1.0%. However, the defensively-geared utilities spent the entire day in negative territory before ending lower by 1.2%. A Deutsche Bank downgrade of Exelon (EXC 31.34, -0.16) weighed on the rate-sensitive sector, which extended its May loss to 7.8%. The health care space was able to outperform other counter-cyclical groups as biotechnology displayed strength. The iShares Nasdaq Biotechnology ETF settled higher by 1.3%.

Wednesday saw the major averages settle with modest losses as the S&P 500 shed 0.7%. Equities slipped out of the gate as sellers drove the major averages to their lows 90 minutes into the session. This marked the return of bargain hunters, who helped the S&P return to its opening levels. However, the relative weakness of several influential groups like energy and health care kept the benchmark average from regaining its flat line.

On Thursday, stocks settled with modest gains as late afternoon selling knocked the major averages from their highs following a headline from Nikkei news, indicating Japan plans to impose new foreign exchange margin trading rules. The news caused dollar/yen to slip into the red while also weighing on equities. Most major financials saw gains of at least 1.0% as Morgan Stanley climbed 3.4% to outperform its peers. Meanwhile, the broader financial sector rose 1.1% to extend its May gain to 7.6%.DJ30 -208.96 NASDAQ -35.38 SP500 -23.67 NASDAQ Adv/Vol/Dec 694/1.79 bln/1789 NYSE Adv/Vol/Dec 464/1.13 bln/2596

3:30 pm :

July crude oil traded in the red today as OPEC left its production policy unchanged at 30 mln barrels per day for the rest of the year. A stronger dollar index also put pressure on prices. The energy component traded in a fairly consolidative pattern for most of its floor trade but dipped to a session low of $91.83 per barrel moments before settling with a 1.8% loss at $91.93 per barrel. For the month of May, crude oil booked a 1.9% loss.

July natural gas oscillated between positive and negative territory, touching a session high of $4.06 per MMBtu as floor trade opened. It sold off heading into the close and settled 1.0% lower at its session low of $3.98 per MMBtu. Today's decline brought losses for the month to 9.3%. o Precious metals also fell during today's floor trade as the stronger dollar following encouraging consumer confidence data put pressure on prices.

June gold slipped off its session high of $1411.90 per ounce and touched a session low of $1389.20 per ounce by late morning action. It then traded in a consolidative pattern for the remainder of the session and settled 1.3% lower at $1393.70 per ounce, bringing losses for the month to 5.4%.

July silver pulled back from a session high of $22.39 per ounce set moments after pit trade opened. It chopped around just above its session low of $22.10 per ounce for the remainder of its session and settled at $22.25 per ounce, or 2.0% lower. During the month of May, silver declined by 8.0%.

DJ30 -107.82 NASDAQ -16.65 SP500 -13.06 NASDAQ Adv/Vol/Dec 852/1303.2 mln/1634 NYSE Adv/Vol/Dec 603/479 mln/2433

3:00 pm : The major averages have slid to fresh afternoon lows as all ten sectors retreated from their recent levels while the CBOE Volatility Index (VIX 15.46, +0.93) notched a fresh session high.

In the foreign exchange market, the Dollar Index hovers near 83.43 after early buying ran the index to session highs near 83.60. The bulk of today's dollar strength has come at the expense of the Australian dollar and the euro.

The EURUSD pair is off by 65 pips near 1.2980 as bulls struggle to retake the 1.3000 resistance level. Early buying produced a bid through 1.3055, but sellers were able to regain control, pushing the pair back below both its 50- and 200-day moving averages.

Elsewhere, AUDUSD is lower by 85 pips at .9570 as action probes key .9600 support. Early weakness dropped the pair to a low of .9550, but the hard currency was able to hold above the week's low. The pair remains susceptible to a squeeze as conditions remain heavily oversold.DJ30 -88.14 NASDAQ -16.22 SP500 -11.47 NASDAQ Adv/Vol/Dec 768/1.14 bln/1723 NYSE Adv/Vol/Dec 573/416.5 mln/2442

2:30 pm : The S&P 500 has slumped to its lows as the weakest sectors of the day widened their losses.

Major banks saw mixed performance earlier, but the recent selling has caused most names to slide to their lows. In addition, two other influential sectors, energy and health care, also registered further losses amid the recent selling.

As the S&P returned to its session lows, the CBOE Volatility Index (VIX 15.00, +0.47) climbed back to its highs.DJ30 -33.83 NASDAQ -5.22 SP500 -5.86 NASDAQ Adv/Vol/Dec 984/1.03 bln/1499 NYSE Adv/Vol/Dec 830/370.7 mln/2151

2:00 pm : The S&P 500 has slipped to its afternoon highs while the Dow has returned to its flat line. Elsewhere, the Nasdaq continues to trade slightly higher.

The Nasdaq has been able to outperform the other two indices thanks, in part, to the strength of its largest components like Apple (AAPL 455.08, +3.50), Microsoft (MSFT 35.20, +0.17), and IBM (IBM 211.05, +1.69).

However, the tech-heavy index has been kept from getting too far ahead of the other averages by the weakness of chipmakers and biotechnology. The PHLX Semiconductor Index is off by 0.4% and the iShares Nasdaq Biotechnology ETF (IBB 182.40, -0.83) trades down 0.5%.DJ30 -2.08 NASDAQ +0.76 SP500 -2.62 NASDAQ Adv/Vol/Dec 1051/949.1/1420 NYSE Adv/Vol/Dec 930/341.5 mln/2050

1:30 pm : The broader market remains little changed as individual sectors hold their recent levels.

The recent strength in financials and technology has vaulted the pair to the top of this month's sector leaderboard. However, the two sectors have headed in opposite directions today.

Mixed performance among major banks has contributed to the sector's weakness as the SPDR Financial Select Sector ETF (XLF 20.12, -0.05) trades lower by 0.3%.

In turn, the relative strength of major tech components has given a boost to the broad sector. The SPDR Technology Select Sector ETF (XLK 32.04, +0.08) is higher by 0.3%.DJ30 +0.97 NASDAQ +2.62 SP500 -1.98 NASDAQ Adv/Vol/Dec 1053/883.1 mln/1404 NYSE Adv/Vol/Dec 967/316.3 mln/1994

1:05 pm : At midday, the major averages trade within 0.1% of yesterday's closing levels.

Equities began the session in negative territory as cautious overseas action weighed on the early sentiment. In addition, worries surrounding the 21:00 ET release of China's Manufacturing PMI cooled some buying interest.

Shortly after the open, investors received a pair of better-than-expected economic releases, but the upside surprises did not result in a bid strong enough to spark a rally.

The Chicago PMI jumped to its highest level since March 2012 as the May print of 58.7 followed April's contractionary reading of 49.0. The large increase was fueled by an improvement in all of the key subcomponents as employment, order backlogs, production, and new orders all posted notable gains.

Separately, the final reading of the May University of Michigan Consumer Sentiment Survey moved up to 84.5, its best level since July 2007. The Briefing.com consensus expected no change from the preliminary reading of 83.7.

The major averages have since huddled near their flat lines as the ten sectors display mixed performance.

Two of the biggest recent laggards, telecom and utilities, have been able to register gains today.

The utilities sector trades higher by 0.6%, but remains down 8.5% in May. Meanwhile, a slim 0.2% gain in telecom services has helped the sector trim its month-to-date loss to 6.0%.

While two defensive sectors trade higher, two others have lagged since the open. The health care space is off by 0.6% with biotechnology contributing to the weakness. The iShares Nasdaq Biotechnology ETF (IBB 182.35, -0.88) trades down 0.5%.

Elsewhere, the consumer staples sector is lower by 0.7% as major members lag. Notably, Dow component Procter & Gamble (PG 77.52, -1.57) registers a loss of 2.0%.

Similar to defensively-geared groups, cyclical sectors trade in mixed fashion. Industrials, technology, and discretionary shares have shown strength while energy, financials, and materials have spent the session in the red.

Looking at today's remaining economic data reveals a disappointment in the Personal Income and Spending report for April. Income was flat and spending declined 0.2% while the Briefing.com consensus expected both measures to be up 0.1%. Core PCE was also flat compared to a 0.1% increase in March.

Personal income for March was revised up to 0.3% from 0.2% while spending was revised down to 0.1% from 0.2%.DJ30 +5.91 NASDAQ +1.95 SP500 -1.81 NASDAQ Adv/Vol/Dec 1027/814.3 mln/1420 NYSE Adv/Vol/Dec 976/292.4 mln/1990

12:30 pm : The broader market continues to show little change as the three averages hover within 0.1% of their respective flat lines.

With indecision persisting in the market, the CBOE Volatility Index (VIX 14.84, +0.31) is higher by 2.1% after spending some time in negative territory.

Elsewhere, the Treasury market has been subject to some early selling, which was followed by a modest bid. As a result, the 10-yr yield has climbed six basis points to 2.168%.DJ30 +5.73 NASDAQ +0.73 SP500 -1.59 NASDAQ Adv/Vol/Dec 991/740.1 mln/1439 NYSE Adv/Vol/Dec 987/265.4 mln/1969

12:00 pm : The S&P 500 has retreated off its highs, but continues to trade 0.1% above its flat line.

Today's leading sector, utilities, has been victimized by heavy selling throughout the month. The group trades higher by 0.8% today, but remains down 8.4% in May. The month-long weakness has knocked the space down in the year-to-date sector rankings from its earlier spot among the leaders to its current slot in the bottom three, slightly ahead of telecom services and materials.

On the flip side, the second-best performing sector of the year, health care, is among today's laggards as biotechnology weighs. The iShares Nasdaq Biotechnology ETF (IBB 182.38, -0.85) is off by 0.5%.DJ30 +28.71 NASDAQ +5.79 SP500 +0.67 NASDAQ Adv/Vol/Dec 1052/661.3 mln/1350 NYSE Adv/Vol/Dec 1100/237.9 mln/1824

11:30 am : Recent action saw the three indices break into positive territory with the Dow leading the move higher.

The price-weighted index has been boosted by the relative strength of its top three components as IBM (IBM 211.62, +2.26), 3M (MMM 112.04, +0.61), and Boeing (BA 100.76, +0.22) all trade with gains between 0.2% and 1.1%.

The S&P 500 trails behind the Dow as consumer staples, energy, and health care sectors continue to hover in the red.DJ30 +50.38 NASDAQ +6.77 SP500 +2.84 NASDAQ Adv/Vol/Dec 1000/577.1 mln/1390 NYSE Adv/Vol/Dec 1114/208.8 mln/1783

11:00 am : The three major averages trade with slim losses of less than 0.2%.

Although the key indices trade within an earshot of their respective flat lines, some divergence has taken place among the individual sectors. The utilities space adds 0.4% in a rebound from month-long selling that leaves the high-yielding sector with a May loss of 8.6%.

Recent sessions saw a shift in leadership from defensive groups to cyclical ones, but today's action takes place amid mixed sector performance. While the utilities sector trades ahead of the broader market, two other countercyclical groups, consumer staples and health care, trade with respective losses of 0.9% and 0.6%.DJ30 -16.21 NASDAQ -4.92 SP500 -3.54 NASDAQ Adv/Vol/Dec 815/459.6 mln/1539 NYSE Adv/Vol/Dec 884/170.1 mln/1986

10:30 am : Commodities are mostly lower this morning with crude oil, gold, silver and copper all near session lows. Natural gas dipped just below $4.00/MMBtu, just barely, while crude has come down below $93/barrel.

Precious metals have been under pressure this morning, and extended losses following today's econ data. Aug gold is now -1.2% at $1395.90/oz and July silver is -1.9% at $22.27/oz. July copper is -0.7% at $3.29/lb.

Energy is now mixed as nat gas moved back near the unchanged line. July natural gas is now -0.1% at $4.02/MMBtu. Meanwhile, July crude oil is -0.8% at $92.91/barrel.

DJ30 -19.83 NASDAQ -4.13 SP500 -3.99 NASDAQ Adv/Vol/Dec 748/352.3 mln/1554 NYSE Adv/Vol/Dec 837/138 mln/1987

10:00 am : Equities continue to trade lower after the major averages made a brief appearance in positive territory. The S&P 500 is off by 0.1%.

The University of Michigan's final May Consumer Sentiment Survey rose to 84.5 from the 83.7 that was posted in the preliminary Survey. The Briefing.com consensus expected the reading would remain at 83.7.DJ30 -1.12 NASDAQ -1.98 SP500 -1.48 NASDAQ Adv/Vol/Dec 814/207.9 mln/1434 NYSE Adv/Vol/Dec 990/93.2 mln/1747

09:50 am : The major averages have approached their respective flat lines in reaction to the May Chicago PMI, which jumped to 58.7 from 49.0. This was better than the 49.3 expected by the Briefing.com consensus.

Three defensive sectors are among the early laggards while consumer discretionary, utilities, and industrial sectors trade with slim gains.DJ30 -3.11 NASDAQ -1.88 SP500 -0.72 NASDAQ Adv/Vol/Dec 711/143.1 mln/1485 NYSE Adv/Vol/Dec 1028/73.9 mln/1678

09:16 am : [BRIEFING.COM] S&P futures vs fair value: -6.70. Nasdaq futures vs fair value: -13.30. Equity index futures continue to hover in the red as the start of today's cash session nears.

The S&P 500 futures trade lower by 0.4% after sliding into the red in a move coinciding with the European open. The old continent has been subject to cautious trade amid news of Eurozone unemployment reaching a new record high of 12.2%. In addition, Italian unemployment rose to 12.0%, reaching a level not seen in 36 years. Also of note, China is scheduled to report its manufacturing PMI tonight, with some speculation suggesting the reading could fall below the expansion/contraction threshold of 50.

Domestically, the Personal Income and Spending report for April was disappointing. It showed that income was flat and that spending declined 0.2%. The Briefing.com consensus expected both measures to be up 0.1%. Core PCE was also flat compared to a 0.1% increase in March.

Following the open, investors will receive the May Chicago PMI report at 9:45 ET while the final Michigan Consumer Sentiment Survey for May will be reported 10 minutes later.

Pre-market action in individual stocks has been relatively quiet. Among the movers of note, Guess? (GES 30.90, +1.55) is higher by 5.3% after the company beat on earnings and guided second quarter revenue above consensus.

09:00 am : [BRIEFING.COM] S&P futures vs fair value: -7.70. Nasdaq futures vs fair value: -14.50.

U.S. equity futures remain in the red with the S&P 500 futures off by 0.5%.

The major Asian bourses ended mostly lower with India's Sensex (-2.3%) leading to the downside after its economy grew at an in-line 4.8% year-over-year clip. Meanwhile, Hong Kong's Hang Seng (-0.4%) and China's Shanghai Composite (-0.7%) ended lower as rumors that tonight's Chinese Manufacturing PMI was going to be weak weighed on the averages. Japan's Nikkei (+1.4%) outperformed, but was unable to climb back into the green for May as it posted its first losing month since July. The gains came after household spending climbed 1.5% year-over-year (+3.1% expected) while Tokyo core CPI edged up 0.1% year-over-year (-0.2% expected), and preliminary industrial production advanced 1.7% month-over-month (0.8% expected).

In Japan, the Nikkei closed higher by 1.4% as trade rebounded following Thursday's steep slide. Heavyweight Fast Retailing jumped 5.1% as bargain hunters stepped in following Thursday's 11% plunge. Elsewhere, exporters were firm with Fanuc climbing 4.3% and Tokyo Electron adding 3.6%.

Hong Kong's Hang Seng shed 0.4% amid a choppy trade. Energy shares weighed with China Coal sliding 1.6%. On the upside, Foxconn surged 18% after receiving a tier 1 upgrade.

In China, the Shanghai Composite settled lower by 0.7% as real estate and materials stocks weighed. China Vanke shed 2.7% and Anhui Conch Cement gave up 0.9%.

Major European indices have spent the first half of the session in negative territory after investors received a slew of economic releases. The Eurozone unemployment rate edged up to a record 12.2% from 12.1% (12.2% forecast). Meanwhile, Italian monthly unemployment rate ticked up to a 36-year high of 12.0% from 11.9% (11.6% expected). Elsewhere, German retail sales declined 0.4% month-over-month (0.2% consensus, -0.1% previous) while the year-over-year reading rose 1.8% (0.8% forecast, -2.5% prior). French consumer spending declined 0.3% (-0.6% forecast, 1.3% prior) while the PPI decreased 0.9% (-0.2% expected, 0.0% previous). In the United Kingdom, mortgage lending rose GBP0.90 billion (GBP0.50 billion expected, GBP0.50 billion previous) while mortgage approvals were reported at 54,000 (55,000 expected, 54,000 prior). Also of note, net lending to individuals came in at GBP1.4 billion (GBP0.90 billion expected, GBP1.10 billion prior).

Reports indicate European Central Bank President Mario Draghi has been asked to attend the upcoming German Constitutional Court hearing regarding the euro and the European Stability Mechanism.

In Germany, the DAX is off by 0.6% as 23 of 30 components register losses. Consumer names Beiersdorf and Fresenius SE are both down near 1.5%. On the upside, Daimler trades with a gain of 1.1%.

France's CAC is lower by 0.6% as France Telecom leads to the downside with a loss of 2.6%. On the flip side, financials have held up relatively well with AXA and BNP Paribas both up near 0.5%.

The United Kingdom's FTSE sheds 0.9% as cyclical names weigh. Evraz, IMI, and Old Mutual are all down between 1.6% and 3.8%.

08:32 am : [BRIEFING.COM] S&P futures vs fair value: -7.70. Nasdaq futures vs fair value: -14.50. Equity futures continue to trade lower with the S&P 500 futures off by 0.5%.

April personal income was unchanged while the Briefing.com consensus expected an uptick of 0.1% to follow the prior month's increase of 0.2%. Meanwhile, personal spending decreased 0.2%, below the Briefing.com consensus, which called for an uptick of 0.1% to follow last month's rise of 0.2%.

Lastly, core PCE prices were unchanged to follow last month's increase of 0.1%. The Briefing.com consensus expected the reading to climb 0.1%.

08:02 am : [BRIEFING.COM] S&P futures vs fair value: -7.80. Nasdaq futures vs fair value: -14.00.

U.S. equity futures trade lower after sliding into the red around the European open. The S&P 500 futures are off by 0.5%.

Looking at overseas developments:

Asian markets ended on a mixed note as Japan's Nikkei rose 1.4%, while Hong Kong's Hang Seng shed 0.4%, and China's Shanghai Composite fell 0.7%.

In regional economic data:

In Japan, investors received a series of data points. The country's Manufacturing PMI ticked up to 51.5 from 51.1 while industrial production climbed 1.7% month-over-month (0.6% expected, 0.9% prior). The national CPI declined 0.7% (-0.9% prior) while national core CPI slipped 0.4% (-0.4% expected, -0.5% previous). Tokyo CPI rose 0.1% (-0.2% consensus, -0.3% prior) while Tokyo core CPI decreased 0.2% (-0.7% previous). Also of note, the unemployment rate held steady at 4.1% while household spending increased 1.5% year-over-year (3.1% forecast, 5.2% prior). Lastly, housing starts rose 5.8% (4.3% forecast, 7.3% previous).

South Korean retail sales declined 0.5% month-over-month (0.3% forecast, 1.6% prior).

Indian GDP rose 4.8%, in line with expectations.

Looking at news:

The Bank of Japan said April Japanese Government Bond holdings of major Japanese banks fell 10.8% month-over-month, and below JPY100 trillion for the first time in almost two years.

Major European indices have spent the entire first half of the session in negative territory. France's CAC and Germany's DAX are both down 0.7% while the United Kingdom's FTSE is off by 0.9%.

Looking at economic news:

German retail sales declined 0.4% month-over-month (0.2% consensus, -0.1% previous) while the year-over-year reading rose 1.8% (0.8% forecast, -2.5% prior).

French consumer spending declined 0.3% (-0.6% forecast, 1.3% prior) while the PPI decreased 0.9% (-0.2% expected, 0.0% previous).

In Italy, the monthly unemployment rate ticked up to 12.0% from 11.9% (11.6% expected) while the quarterly rate rose to 11.9% from 11.2% (11.2% expected).

The Eurozone unemployment rate edged up to 12.2% from 12.1% (12.2% forecast).

In the United Kingdom, mortgage lending rose GBP0.90 billion (GBP0.50 billion expected, GBP0.50 billion previous) while mortgage approvals were reported at 54,000 (55,000 expected, 54,000 prior). Also of note, net lending to individuals came in at GBP1.4 billion (GBP0.90 billion expected, GBP1.10 billion prior).

In news:

The increase in Eurozone unemployment puts the figure at a fresh record high while Italy's unemployment rate of 12.0% marks a 36-year high.

Reports indicate European Central Bank President Mario Draghi has been asked to attend the upcoming German Constitutional Court hearing regarding the euro and the European Stability Mechanism.

In U.S. corporate news:

Guess? (GES 32.20, +2.85) is higher by 9.7% after the company beat on earnings and guided second quarter revenue above consensus.

Palo Alto Networks (PANW 47.76, -6.63) trades down 12.2% after its bottom-line beat was overshadowed by a revenue miss and cautious fourth quarter guidance.

April personal income, personal spending, and core PCE prices will all be announced at 8:30 ET. This will be followed by the 9:45 ET release of the May Chicago PMI while the final Michigan Consumer Sentiment Survey for May will cross the wires at 9:55 ET.

06:30 am : [BRIEFING.COM] S&P futures vs fair value: -10.00. Nasdaq futures vs fair value: -21.00.

06:30 am : Nikkei...13774.54...+185.50...+1.40%. Hang Seng...22392.16...-92.20...-0.40%.

06:30 am : FTSE...6583.76...-73.20...-1.10%. DAX...8314.79...-85.40...-1.00%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage