Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

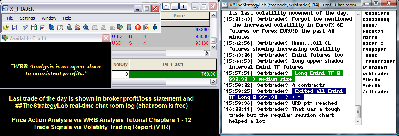

040213-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+760.00.png [ 82.89 KiB | Viewed 292 times ]

040213-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+760.00.png [ 82.89 KiB | Viewed 292 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$640.00 dollars or +6.40 points, Light Crude Oil CL ($CL_F) futures @

$120.00 dollars or +0.12 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points, EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks and Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $760.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

##TheStrategyLab chat room. You can read

today's ##TheStrategyLab trading chat room logs for details about each one of my trades from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=116&t=1474 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=207&t=1794 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

Dow, S&P Close At New Highs On Health Care Rally Attachment:

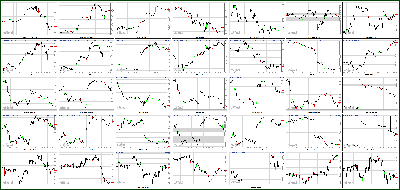

040213-Key-Price-Action-Markets.png [ 527.9 KiB | Viewed 291 times ]

040213-Key-Price-Action-Markets.png [ 527.9 KiB | Viewed 291 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Strength in the health care sector gave stocks a shot in the arm Tuesday, pushing the Dow and S&P 500 to new record highs.

All three major indexes closed at least 0.5% higher. The Dow Jones industrial average hit two new records: an intraday high of about 14,684, and a record close at 14,662.

The S&P 500 closed at a record high of 1,570.

The Dow and S&P have hit several new records during a solid 2013. Even with a slight retreat Monday, all three indexes are still up between about 8% and 12% for the year.

Tuesday's rally was fueled by the health care sector, one day after the government announced welcome news for the industry: Medicare Advantage rates will jump by 3.3% next year, rather than the 2.3% cut that had been proposed previously.

Shares of insurers Humana (HUM, Fortune 500), United Health (UNH, Fortune 500) and Aetna (AET, Fortune 500) closed about 4% to 6% higher.

* Expect the bond bubble to fizzle, not popAs the bull market continues, some analysts are worried that stocks are due for a major correction. Famed investor Wilbur Ross, however, says the market is "fairly priced."

"I think the market is where it should be right now," Ross told CNNMoney. "That doesn't mean there won't be volatility, but I don't think current levels are overdone or underdone."

Outside of the big move in health care stocks, there was little else on the corporate or economic docket Tuesday.

The Census Bureau reported that factory orders jumped 3% in February. That was slightly better than expected, and follows an underwhelming report on U.S. manufacturing Monday.

Major automakers reported solid monthly sales figures for March. Auto sales at General Motors (GM, Fortune 500), Ford (F, Fortune 500) and Chrysler all posted U.S. sales gains of 5% or better, while Toyota (TM) sales edged up 1% from a year ago. Chrysler posted its best sales month since December 2007.

* CNNMoney's Hot StocksNot all sectors were flying high Tuesday. Tech received a few spots of bad news, courtesy of Goldman Sachs analysts.

* Video - HP Gets A Reality CheckHewlett-Packard (HPQ, Fortune 500) shares slid 5% after Goldman downgraded the company to "sell."

Goldman also kicked Apple (AAPL, Fortune 500) off its "conviction buy" list and cut the price target to $575 from $600. Still, the investment firm is retaining its "buy" rating for Apple, whose shares closed slightly higher Tuesday.

Nasdaq (NDAQ) shares slumped 13% after the exchange operator said it planned to buy eSpeed, an electronic market for Treasuries, from BGC Partners. Investors may be punishing Nasdaq for paying a whopping $1.2 billion. BGC (BGCA) shares, meanwhile, soared 47%.

* Fear & Greed Index steeped in greedEuropean markets closed higher, while Asian markets ended mixed. The Hang Seng added 0.3% while the Nikkei dropped 1.1% and the Shanghai Composite lost 0.3%.

Commodities, including oil and gold, were lower, while the yield on the U.S. Treasury 10-year note ticked up to 1.86%.

4:15 pm : Equities spent the bulk of today's session near their highs before a late afternoon stumble dropped the S&P 500 back near the middle of its range. As a result, the benchmark average finished higher by 0.5%.

Notably, the Russell 2000, which tracks small cap stocks, ended lower by 0.5% after losing more than 1.0% yesterday.

Equities began today's session with solid gains amid an upbeat European trade. The overseas advance followed the release of several Manufacturing PMI readings across the eurozone. Although most reports exceeded expectations, all five remained below 50, signifying an ongoing contraction.

Domestically, the health care sector showed strength out of the gate with managed care stocks jumping after the Centers for Medicare and Medicaid Services said 2014 Medicaid Advantage and prescription drug benefit rates will increase by 3.3%. Dow component UnitedHealth Group (UNH 61.74, +2.77) gained 4.7% while the broader SPDR Health Care Select Sector ETF (XLV 46.74, +0.67) rose 1.5%.

The health care sector was not the only defensively-minded space which outperformed the broader market. Consumer staples and telecoms finished among the session leaders as well.

One cyclical group which finished among the leaders was the consumer discretionary sector. Apparel stocks provided support after Urban Outfitters (URBN 39.87, +1.46) gave an optimistic update on its first quarter sales.

Elsewhere in the discretionary space, Ford Motor (F 13.01, +0.11) and General Motors (GM 27.93, +0.13) settled with respective gains of 0.9% and 0.5% after reporting their monthly sales. In March, Ford saw its sales climb 6.0% to 236,160 vehicles while General Motors reported an increase of 6.4% to 245,950 units.

While discretionary shares ended firmly higher, the same could not be said for other growth-sensitive sectors.

Producers of basic materials saw a continuation of their recent weakness. Downbeat trade in steelmakers caused the Market Vectors Steel ETF (SLX 41.87, -1.06) to lose 2.5% while the broader SPDR Materials Select Sector ETF (XLB 38.46, -0.38) fell 1.0%. Since March 14, the sector ETF is down almost 4.0% while the S&P 500 is little changed over that time.

While materials spent the entire session in negative territory, intraday weakness sent the industrial sector to its lows, where it settled for the day. Transportation-related stocks contributed to the sector's softness, and the Dow Jones Transportation Average lost 1.2%. Airlines pressured the 20-stock complex after Delta (DAL 14.94, -1.31) trimmed its guidance, citing the sequester as one of the reasons for lower targets.

Trading volume was below average once again as 640 million shares changed hands on the floor of the New York Stock Exchange.

Looking back at the final sector performance, health care (+1.4%), consumer staples (+1.1%), and consumer discretionary (+0.9%) paced the advance while materials (-0.9%), energy (-0.5%), and industrials (-0.1%) weighed.

Reviewing today's economic data, manufacturing orders rose 3.0% in February after declining an upwardly revised 1.0% (from -2.0%) in January. The Briefing.com consensus expected manufacturing orders to increase 2.6%.

Durable goods orders were revised down slightly from a 5.7% gain to 5.6%. A 75.0% increase in aircraft sales accounted for nearly the entire increase. Excluding transportation, durable goods orders fell 0.7%, which was slightly worse than the originally reported 0.5% decline.

Tomorrow, the weekly MBA Mortgage Index will be reported at 7:00 ET. In addition, March ADP Employment Change and ISM Services will be released at 8:15 ET and 10:00 ET, respectively.DJ30 +89.16 NASDAQ +15.69 SP500 +8.08 NASDAQ Adv/Vol/Dec 1093/1.53 bln/1368 NYSE Adv/Vol/Dec 1435/639.4 mln/1546

3:35 pm : Crude oil futures managed to recover it losses today, crossing back above the $97 level. By the close, May crude ended the day unchanged at $97.22/barrel.

Natural gas continued to trade in the red for today's session, trading between approx. $3.94-$4.00/MMBtu. May natural gas ended the day in the red, losing 5 cents to $3.97/MMBtu.

Precious metals were just ugly today. Both gold and silver trended lower and lower all session, ultimately finishing today's session just above session lows. June gold lost $30.30 at $1576.30, while May silver fell $1.03 to finish the session at $27.25/oz.DJ30 +71.92 NASDAQ +13.11 SP500 +6.17 NASDAQ Adv/Vol/Dec 1141/1293.2 mln/1297 NYSE Adv/Vol/Dec 1453/431 mln/1514

3:00 pm : After spending the bulk of today's action in a two point range, recent trade saw the S&P 500 slide to fresh afternoon lows. Although the index has slipped from its best levels of the day, it remains higher by 0.4%.

The recent weakness occurred as energy and materials slid to fresh lows. In addition, the selling pressure pushed the industrial sector into negative territory as well. The SPDR Industrial Select Sector ETF (XLI 41.16, -0.09) is off by 0.2%, and the relative weakness of transportation-related stocks has pressured the Dow Jones Transportation Average to session lows of its own. The bellwether complex is down 1.1%.DJ30 +73.23 NASDAQ +14.54 SP500 +6.90 NASDAQ Adv/Vol/Dec 1215/1.15 bln/1225 NYSE Adv/Vol/Dec 1483/384.3 mln/1443

2:30 pm : The S&P 500 is higher by 0.5% as the benchmark index continues to hover within several points of notching a fresh record high. Afternoon trade has been very quiet with the index spending the past four hours within a two point range. Notably, even as the broader market trades in the positive territory, several pockets of weakness can be spotted.

The growth-oriented materials sector is near its lows with the SPDR Materials Select Sector ETF (XLB 38.60, -0.24) down 0.6%.

Elsewhere, the Dow Jones Transportation Average is lower by 0.6% with airlines contributing to the weakness.

Lastly, the Russell 2000, which tracks small cap stocks, is unchanged after underperforming notably in yesterday's action.DJ30 +74.58 NASDAQ +16.32 SP500 +7.31 NASDAQ Adv/Vol/Dec 1271/1.06 bln/1150 NYSE Adv/Vol/Dec 1550/352.6 mln/1366

2:00 pm : The major averages continue to hover near their highs, and the S&P 500 is rising 0.6%. Afternoon trade has been very quiet with the benchmark average spending the past three hours within a two point range.

Consumer staples and health care have led the broader market from the open, and the two defensive sectors remain atop today's leaderboard. On the downside, producers of basic materials have extended their recent weakness and the SPDR Materials Select Sector ETF (XLB 38.64, -0.20) is down 0.5%. Notably, the growth-oriented group is down nearly 3.5% since March 14, and is the weakest performer year-to-date. So far in 2013, the materials sector has added only 2.6% while the S&P 500 trades with a year-to-date gain of 10.2%.DJ30 +95.40 NASDAQ +23.70 SP500 +9.76 NASDAQ Adv/Vol/Dec 1396/966.4 mln/1025 NYSE Adv/Vol/Dec 1711/320.7 mln/1218

1:30 pm : Quiet afternoon trade continues with the S&P 500 higher by 0.6%. As the broader market remains near its best levels of the day, little change has been observed in sector leadership. Health care and consumer staples remain in the lead with discretionary shares showing relative strength as well.

On the downside, the materials sector has declined steadily through the first half of the session, and the SPDR Materials Select Sector ETF (XLB 38.59, -0.25) is down 0.6%. Chemical producers trade firmly lower with Monsanto (MON 103.30, -2.49) and Mosaic (MOS 57.65, -1.61) down 2.4% and 2.7%, respectively.

In addition, recent trade saw the energy sector slip to its lowest level of the day. The SPDR Energy Select Sector ETF (XLE 78.77, -0.38) is down 0.5%.DJ30 +87.21 NASDAQ +22.96 SP500 +9.04 NASDAQ Adv/Vol/Dec 1384/889.1 mln/1000 NYSE Adv/Vol/Dec 1674/296.3 mln/1234

1:00 pm : The major averages trade near their intraday highs, and the S&P 500 is firmer by 0.7%.

Equities opened the session on a higher note with the health care sector leading out of the gate. The strength followed the Centers for Medicare and Medicaid Services decision to increase 2014 rates for Medicaid Advantage and prescription drug benefits.

As a result, health care names trade with broad gains. Humana (HUM 80.16, +5.14) and UnitedHealth Group (UNH 62.28, +3.33) are higher by 6.8% and 5.6% while the broader SPDR Health Care Select Sector ETF (XLV 46.73, +0.67) is firmer by 1.4%.

In addition to health care, other top sectors also fall in the defensive category. However, one cyclical group appearing among today's leaders is the consumer discretionary sector.

In the discretionary space, Ford Motor (F 13.12, +0.22) and General Motors (GM 28.00, +0.20) trade with respective gains of 1.7% and 0.7% after reporting their March sales. Ford saw its sales climb 6.0% to 236,160 vehicles while General Motors reported a March increase of 6.4% to 245,950 units.

Despite the broader market advance, growth-sensitive materials have remained under pressure. The SPDR Materials Select Sector ETF (XLB 38.62, -0.23) is off by 0.6% today, and down more than 3.0% since March 14.

Today, steelmakers are among the weakest sector components, and the Market Vectors Steel ETF (SLX 42.45, -0.48) is lower by 1.1%.

The industrial space is also among today's laggards, and the SPDR Industrial Select Sector ETF (XLI 41.36, +0.12) trades with a gain of just 0.3%. Although industrials trade in positive territory, transportation-related stocks have shown some weakness.

The Dow Jones Transportation Average is down 0.5% with airlines leading to the underperformance. Air carriers trade in the red after Delta (DAL 15.10, -1.14) lowered its guidance, citing the sequester as one of the reasons for lower targets.

Looking back at today's economic data, manufacturing orders rose 3.0% in February after declining an upwardly revised 1.0% (from -2.0%) in January. The Briefing.com consensus expected manufacturing orders to increase 2.6%.

Durable goods orders were revised down slightly from a 5.7% gain to 5.6%. A 75.0% increase in aircraft sales accounted for nearly the entire increase.

Excluding transportation, durable goods orders fell 0.7%, which was slightly worse than the originally reported 0.5% decline.DJ30 +99.52 NASDAQ +26.99 SP500 +10.83 NASDAQ Adv/Vol/Dec 1433/810.3 mln/944 NYSE Adv/Vol/Dec 1765/270.3 mln/1125

12:35 pm : Equities saw little change in recent action as the S&P 500 remains near its best level of the day. The benchmark index is higher by 0.7% and the health care sector is the top performer of the session after the announcement of higher Medicaid Advantage rates in 2014. Humana (HUM 80.42, +5.40) trades with a gain of 7.2% and Dow component UnitedHealth Group (UNH 62.39, +3.42) is firmer by 5.8%.

In addition to health care, today's other leading sectors also fall in the defensive category.

On the flip side, most cyclical groups trail behind the broader market. The consumer discretionary space is the lone exception as the SPDR Consumer Discretionary Select Sector ETF (XLY 53.08, +0.48) trades higher by 0.9%. Ford Motor (F 13.07, +0.17) is contributing to the sector strength after reporting March sales growth of 6.0% to 236,160 vehicles.DJ30 +95.97 NASDAQ +26.56 SP500 +10.41 NASDAQ Adv/Vol/Dec 1425/748.1 mln/929 NYSE Adv/Vol/Dec 1768/248.8 mln/1104

12:00 pm : Recent trade saw little change in the major indices and the S&P 500 continues to trade higher by 0.7%.

Today's sector leadership favors defensively-minded groups with health care, consumer staples, and telecoms leading the way. Meanwhile, the other cyclical sector, utilities, trades with a slim gain of 0.3%.

On the downside, producers of basic materials have extended their recent weakness as the SPDR Materials Select Sector ETF (XLB 38.70, -0.14) hovers near its lowest level of the day. Steelmakers are among the weakest components and world's largest steel producer, ArcelorMittal (MT 12.34, -0.44), is down 3.4%.DJ30 +95.04 NASDAQ +23.52 SP500 +9.98 NASDAQ Adv/Vol/Dec 1368/674.1 mln/966 NYSE Adv/Vol/Dec 1720/226.2 mln/1156

11:30 am : Equities continue to hover near their highs and the S&P 500 is firmer by 0.7%. Although the broader market trades firmly higher, defensive sectors are among the top performers of the day.

Health care stocks trade higher across the board after regulators announced a 3.3% rate increase for Medicaid Advantage and prescription drug benefits in 2014. The SPDR Health Care Select Sector ETF (XLV 46.74, +0.67) is rising 1.5%.

The consumer staples sector is the day's other leader. McCormick (MKC 73.07, +0.36) is rising 0.5% after its quarterly report met earnings and revenue expectations.DJ30 +100.91 NASDAQ +26.75 SP500 +10.73 NASDAQ Adv/Vol/Dec 1492/589.5 mln/827 NYSE Adv/Vol/Dec 1806/200.4 mln/1043

11:00 am : The major averages continue to trade firmly higher with the S&P 500 up 0.7%. The health care sector is the top performer of the day with managed care providers garnering notable interest after regulatory authorities announced a 3.3% rate increase for Medicaid Advantage and prescription drug benefits in 2014. As a result of broad sector strength, the SPDR Health Care Select Sector ETF (XLV 46.72, +0.65) trades higher by 1.4%.

On the downside, the economically-sensitive materials sector is continuing its recent weakness. The SPDR Materials Select Sector ETF (XLB 38.73, -0.11) is off by 0.3% today, and the ETF is down more than 3.0% since March 14. In that same timeframe, the S&P 500 has added 0.5%.

Today, steelmakers are among the weakest sector components and the Market Vectors Steel ETF (SLX 42.59, -0.34) is lower by 0.8%.DJ30 +101.32 NASDAQ +27.21 SP500 +10.72 NASDAQ Adv/Vol/Dec 1520/478.8 mln/741 NYSE Adv/Vol/Dec 1898/168.2 mln/953

10:30 am : Commodities are taking a hit today as the dollar index in showing gains and at its session high.

Gold and silver futures have basically continued to extend losses this morning and again hit new session lows in recent activity. Jun gold is now -1.2% at $1581.90/oz and May silver is now -1.8% at $27.46/oz. May copper is -0.4% at $3.36/lb.

May crude oil futures have spent today's in the red except for a couple of brief moments where it showed gains. May crude began to lose steam about 50 minutes before floor trading was to begin and continued to extend losses following the open. May crude put in a new LoD of $95.93/barrel and is now -0.5% at $96.55/barrel.

Natural gas sold off as wel this morning and is now -1.6% at $3.95/MMBtu. DJ30 +83.91 NASDAQ +22.55 SP500 +8.48 NASDAQ Adv/Vol/Dec 1458/347.3 mln/752 NYSE Adv/Vol/Dec 1815/131 mln/997

10:00 am : The major averages ticked to fresh highs in reaction to the latest factory orders data. The S&P 500 is higher by 0.6%.

February factory orders rose 3.0%, which was better than the 2.6% increase expected by the Briefing.com consensus. Today's uptick follows last month's decrease of 2.0%.DJ30 +82.56 NASDAQ +25.12 SP500 +9.48 NASDAQ Adv/Vol/Dec 1480/212.7 mln/658 NYSE Adv/Vol/Dec 1849/95.7 mln/895

09:50 am : The major averages are hovering near their early highs with the S&P 500 firmer by 0.5%.

The health care sector is the clear early leader after the Centers for Medicare and Medicaid Services announced a planned 2014 rate hike of 3.3%. UnitedHealth Group (UNH 63.15, +4.18) is higher by 7.1% and the broader SPDR Health Care Select Sector ETF (XLV 46.63, +0.56) is rising 1.2%.

On the downside, energy and materials trade in the red. The energy sector is the weakest performer as crude oil trades lower by 0.9% at $96.26.DJ30 +61.03 NASDAQ +22.41 SP500 +7.38 NASDAQ Adv/Vol/Dec 1504/138.1 mln/595 NYSE Adv/Vol/Dec 1872/73.1 mln/827

09:14 am : [BRIEFING.COM] S&P futures vs fair value: +6.30. Nasdaq futures vs fair value: +13.50. Heading into the open, equity futures indicate a higher start to the session with the S&P 500 futures up 0.4%. The upbeat early trade takes places amid strength in health care names after the Centers for Medicare and Medicaid Services announced a 3.3% rate hike for 2014. This comes after a February announcement indicated rates would decline 2.3%. Dow component UnitedHealth Group (UNH 61.43, +2.46) is higher by 4.2% and its peers have shown relative strength as well.

Upbeat European trade is also contributing to the early strength after several economies reported manufacturing PMI readings ahead of expectations. Although most regional reports exceeded expectations, all readings remained below 50, which indicates continued contraction.

In today's economic data, February factory orders will be reported at 10:00 ET. In addition, auto and truck manufacturers will be reporting their March sales throughout the day.

08:58 am : [BRIEFING.COM] S&P futures vs fair value: +6.30. Nasdaq futures vs fair value: +12.70. Equity indices trade near their pre-market highs with the S&P 500 futures firmer by 0.4%. The upbeat pre-market sentiment comes as European markets trade broadly higher after several economies reported better-than-feared manufacturing PMI readings. Although most reports exceeded expectations, they all remained below 50, signifying ongoing contraction.

In addition to upbeat overseas trade, equity futures are receiving some support from health care names after the Centers for Medicare & Medicaid Services announced a 2014 rate increase for Medicaid Advantage and prescription drug benefits. Aetna (AET 54.93, +2.55) is rising 4.9% and Dow component UnitedHealth Group (UNH 61.49, +2.52) is higher by 4.3%.

February factory orders will be reported at 10:00 ET. In addition, auto and truck manufacturers will be reporting their March sales throughout the day.

08:30 am : [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +14.00.

U.S. equity futures continue to hover near their pre-market highs with the S&P 500 futures up 0.4%.

The major Asian bourses ended mixed as Japan's Nikkei (-1.1%) lagged thanks to the strong yen. The Reserve Bank of Australia opined overnight, opting to hold its key rate unchanged at 3.00% while indicating there is still room to cut rates because of a tame inflation picture. Data out overnight was limited to Japan's average cash earnings, which posted a weaker than anticipated -0.7% year-over-year (-0.1% expected).

In Japan, the Nikkei closed lower by 1.1% to end at its worst level in four weeks. Exporters were under pressure thanks to the strong yen as Canon and Nissan Motor both shed close to 3.5%. Elsewhere, real estate and financials outperformed ahead of the Bank of Japan's two-day meeting. Mitsui Fudosan and Mitsubishi Estate surged 4.4% and 6.1% respectively to lead real estate names while Mitsubishi UFJ Financial jumped 2.3% to finish among the top performing financials.

Hong Kong's Hang Seng added 0.3% amid a choppy trade. Angang Steel surged 12.5% after announcing it expects a profit in Q1 after posting a loss in Q4 2012. Meanwhile, HSBC eked out a 1.2% advance as European markets traded higher.

In China, the Shanghai Composite settled lower by 0.3% to finish at its worst level in three months. Health care stocks were under significant pressure after some negative commentary on the space. Beijing SL Pharmaceutical was the worst performer, plunging 9.1%. Elsewhere, real estate stocks advanced as Vanke and Poly Real Estate added 1.8% and 1.4% respectively.

European indices are broadly higher after regional manufacturing PMI readings were reported mostly ahead of expectations. However, it should be noted all of the readings were reported below 50, which delineates the difference between expansion and contraction. The eurozone manufacturing PMI was reported at 46.8, while the consensus expected a reading of 46.6. Meanwhile, the eurozone unemployment rate was reported at an all-time high of 12.0%, in-line with expectations. French manufacturing PMI was reported at 44.0 (43.9 consensus). Germany's manufacturing PMI came in at 49.0 (48.9 consensus). The United Kingdom's manufacturing PMI of 48.3 fell short of the 48.5 expected by the consensus. Italian manufacturing PMI was reported at 44.5 (45.4 consensus). In addition, the country's monthly unemployment rate of 11.6% was better than the expected rate of 11.8%. Spain's manufacturing PMI of 44.2 was short of the 46.0 expected by the market.

According to eurozone officials, Cyprus will receive an extension until 2018 to meet its fiscal targets. In addition, Cyprus will pay 2.5% interest on its bailout loans with the repayment set to start in 10 years. Also of note, Finance Minister Michalis Sarris has resigned.

In Germany, the DAX is higher by 1.3% with utilities outperforming. E.ON is firmer by 2.4% and RWE is adding 1.5%.

In the United Kingdom, the FTSE is rising 1.2% with consumer names leading the way. EasyJet and InterContinental Hotels Group are higher by 4.1% and 2.2%, respectively.

France's CAC is adding 1.1% as industrials show relative strength. Bouygues is firmer by 3.4% and Safran trades higher by 3.0%.

08:02 am : [BRIEFING.COM] S&P futures vs fair value: +7.20. Nasdaq futures vs fair value: +15.70.

U.S. equity futures trade modestly higher amid upbeat overseas trade. The S&P 500 futures are higher by 0.4%.

Looking at overnight developments:

Asian markets ended mixed. Hong Kong's Hang Seng gained 0.3% while China's Shanghai Composite shed 0.3% and Japan's Nikkei lost 1.1%.

In economic data:

Japan's monetary base expanded 19.8% year-over-year against the expected increase of 16.3%. Meanwhile, average cash earnings fell 0.7% year-over-year, worse than the decline of 0.1% expected by the consensus.

The Reserve Bank of Australia left its key interest rate unchanged at 3.00%.

Looking at news:

Japan's Prime Minister Shinzo Abe said the country's economy is subject to unforeseen circumstances and it is possible the Bank of Japan will be unsuccessful in reaching its inflation target of 2.0%.

The Chinese Academy of Social Sciences believes the country's CPI rose 2.5% during March to follow February's increase of 3.2%.

European indices are broadly higher with Germany's DAX leading the way, up 1.3%. Elsewhere, the United Kingdom's FTSE and France's CAC are higher by 1.1%, respectively.

Regional economic data was plentiful:

The eurozone manufacturing PMI was reported at 46.8, while the consensus expected a reading of 46.6. Meanwhile, the eurozone unemployment rate was reported at an all-time high of 12.0%, in-line with expectations.

French manufacturing PMI was reported at 44.0 (43.9 consensus).

Germany's manufacturing PMI came in at 49.0 (48.9 consensus).

The United Kingdom's manufacturing PMI of 48.3 fell short of the 48.5 expected by the consensus.

Italian manufacturing PMI was reported at 44.5 (45.4 consensus). In addition, the country's monthly unemployment rate of 11.6% was better than the expected rate of 11.8%.

Spain's manufacturing PMI of 44.2 was short of the 46.0 expected by the market.

In news:

European markets trade higher after regional manufacturing PMI readings were reported mostly ahead of expectations. However, it should be noted all of the readings were reported below 50, which delineates the difference between expansion and contraction.

According to eurozone officials, Cyprus will receive an extension until 2018 to meet its fiscal targets.

In U.S. corporate news:

Several health care names trade higher after the Centers for Medicare & Medicaid Services announced a 2014 rate increase for Medicaid Advantage and prescription drug benefits. Humana (HUM 81.85, +6.85) and UnitedHealth Group (UNH 61.24, +2.27) are higher by 9.1% and 3.9%, respectively.

Hewlett-Packard (HPQ 22.58, -0.73) is down 3.1% after Goldman Sachs downgraded the stock to 'Sell' from 'Neutral.'

February factory orders will be reported at 10:00 ET. In addition, auto and truck manufacturers will be reporting their March sales throughout the day.

06:49 am : [BRIEFING.COM] S&P futures vs fair value: +7.00. Nasdaq futures vs fair value: +15.00.

06:49 am : Nikkei...12003.43...-131.60...-1.10%. Hang Seng...22367.82...+68.20...+0.30%.

06:49 am : FTSE...6477.53...+65.80...+1.00%. DAX...7889.19...+94.20...+1.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com HomepageMarket Update