Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

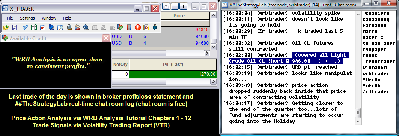

032813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1270.00.png [ 82.65 KiB | Viewed 494 times ]

032813-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1270.00.png [ 82.65 KiB | Viewed 494 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1900.00 dollars or +19.00 points, Light Crude Oil CL ($CL_F) futures @

($630.00) dollars or -0.63 points, EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $1270.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

##TheStrategyLab chat room. You can read

today's ##TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with

price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=115&t=1470 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=205&t=1773 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

What A Quarter! Dow and S&P At Record Highs Attachment:

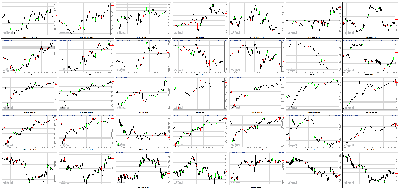

032813-Key-Price-Action-Markets.png [ 539.53 KiB | Viewed 499 times ]

032813-Key-Price-Action-Markets.png [ 539.53 KiB | Viewed 499 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Finally. Stocks wrapped up a stellar first quarter Thursday with the S&P 500 finishing at a new high, after flirting with the milestone for weeks.

The benchmark index gained 6 points, or 0.4%, to end at a record close of 1569.19, inching above its previous record of 1565.15 from October 2007.

Despite the new milestone, trading was relatively calm and light as investors monitored the ongoing crisis in Cyprus and mulled over new economic data in the United States. The Dow Jones industrial average and the Nasdaq rose just a little over 0.3%. The markets will be closed tomorrow in the United States and most of Europe for Good Friday.

But the first quarter of 2013 has been far from quiet. The Dow, which has been trading at record highs since early March, rallied more than 11% and booked its best first quarter since 1998. The S&P 500 soared 10% and the Nasdaq was up 8%.

* Check out CNNMoney's new Portfolio toolThe biggest gains were logged in January, but March has been a solid month for stocks as well, with all three indexes rising more than 3%. Stocks continued to rally in the holiday-shortened week despite Cyprus concerns. The Dow rose 0.5% for the week, while the S&P 500 added 0.8% and Nasdaq rose 0.7%.

Despite the big run-up this year, experts argue that valuations remain attractive for U.S. stocks. The S&P 500 is trading at just 16 times 2012 earnings. At its all-time high in October 2007, the S&P 500's valuation was just above 17 times profits for the past 12 months.

And looking at earnings projections, stocks still appear reasonably valued. The S&P 500 is trading at just 14 times 2013 estimates.

* What's next for the markets?Winners and losers: The best-performing stock in the S&P 500 during the quarter was Netflix (NFLX). Shares have more than doubled in the last few months as investors have become optimistic about the company's growth prospects, despite a series of missteps over the last couple of years. Best Buy (BBY, Fortune 500) and Hewlett-Packard (HPQ, Fortune 500), struggling companies that are in the middle of turnaround efforts, were the next strongest performers, with shares up 87% and 68% respectively.

Some of the weaker links were JC Penney (JCP, Fortune 500), which is having more trouble than success with its makeover plan, as well as coal company Peabody Energy (BTU, Fortune 500) and mining firm Cliffs Natural Resources (CLF, Fortune 500).

Cyprus banks back to business: Banks in Cyprus reopened Thursday morning after being closed since March 16. The island nation plans to limit the amount of money that depositors can withdraw in an attempt to prevent bank runs.

Cyprus agreed early Monday to raise billions of euros from big depositors at the Bank of Cyprus and Popular Bank of Cyprus, and to shrink its banking sector in return for a €10 billion European Union bailout.

* Bitcoin prices surge post-Cyprus bailoutU.S. economy humming along: Back in the United States, the government released its weekly data on initial jobless claims and its final reading on fourth-quarter GDP.

Jobless claims totaled 357,000 in the week ended March 23, an increase of 16,000 from the prior week and much worse than expected. The forecast called for a total of 335,000, according to a consensus of economists complied by Briefing.com.

The final government report for fourth-quarter GDP showed an annual increase of 0.4%, slightly higher than the expected increase of 0.3%. The prior reading showed the economy grew at a 0.1% pace.

What's moving: Blackberry (BBRY) slipped after the smartphone maker reported a surprise profit, but sales that fell short of expectations.

Shares of eBay (EBAY, Fortune 500) climbed 4% after the company's marketplaces chief Devin Wenig revealed plans to nearly double eBay's user base by 2015 and expectations of $110 billion in marketplace sales.

Pinnacle Foods (PF), owner of brands including Duncan Hines and Birds Eye, rose 11% in its stock market debut. Pinnacle raised $580 million in its initial public offering after pricing shares at the high end of its range. The company is backed by private equity firm Blackstone (BX).

Shares of Deckers Outdoor (DECK), which owns the Ugg boots brand, jumped after an analyst at Jefferies upgraded the stock and gave it a price target of $100 a share, nearly double its current price.

Dollar pulls back: European markets finished with solid gains, while Asian markets ended lower.

The dollar fell against the euro, British pound and the Japanese yen.

Oil prices gained slightly, while gold prices edged lower.

The price on the 10-year Treasury rose slightly, and the yield held steady at 1.85%.

What's buzzing: Wall Street strategists are betting the rally will continue. Wells Fargo Advisors increased its year-end 2013 target range for the S&P 500 to 1575-1625 from an earlier forecast of 1525-1575.

"Investors now appear to be more focused upon the potential for continuing global economic growth, said Scott Wren, senior equity strategist at Wells Fargo Advisors. "We anticipate investor confidence will continue to lift, slowly catching up with consumer confidence."

4:15 pm : The major averages ended the last session of the holiday-shortened week with slim gains. The S&P 500 added 0.4%, and notched its highest close of all-time, eclipsing the previous record close set on October 9, 2007.

The day began on a rather uneventful note, but the flat open was followed by a brief stumble which sent the S&P 500 into negative territory after the latest reading of the Chicago PMI missed expectations.

For March, the Purchasing Managers' Index fell to 52.4 from the 56.8 reported in the February report. Meanwhile, the Briefing.com consensus had expected a smaller decline, to 56.5.

The subsequent weakness was quickly bought up, which enabled the benchmark average to spend the rest of the day in a steady upward climb.

Although equities settled with gains, today's advance was paced primarily by defensively-minded groups. Health care and utilities led the broader market for the duration of the session, and ended as the top performing sectors on the day.

Notably, the health care sector ended the month as the top performing group. Further, having gained 15.2% year-to-date, the sector is also the best performer so far in 2013.

Today's other outperformers included industrials and materials. However, their gains were largely the result of rebound trade after the growth-oriented groups saw some weakness over the past two weeks.

The SPDR Materials Select Sector ETF (XLB 39.18, +0.15) settled higher by 0.4%, but even with today's gain, the sector ETF ended the month as the second weakest performer, trailing only behind telecom services.

The weakness of the materials sector is indicative of the persisting growth concerns. These same worries are being reflected by the price of copper futures, which fell 1.1% to $3.405 per pound, to end the quarter at their lowest level since November of last year.

While materials found themselves near the lead, cyclical financials and technology ended as the weakest performers.

Major bank stocks remained under pressure since the first Cypriot bailout proposal was unveiled two weeks ago. Morgan Stanley (MS 21.98, -0.31) was the weakest performer among the majors and the SPDR Financial Select Sector ETF (XLF 18.21, +0.05) registered a slim gain of 0.3% in today's action. However, even with today's gain, the bank sector ETF is down 1.6% since last Monday.

Elsewhere, the technology sector was unable to climb too far above yesterday's close as Apple (AAPL 442.66, -9.42) weighed. The largest tech stock sold off steadily throughout the day before ending lower by 2.1% Also of note, BlackBerry (BBRY 14.44, -0.12) slipped 0.8% after beating on earnings on below-consensus revenue.

Reviewing the final sector performance, utilities (+1.3%), health care (+1.0%), industrials (+0.6%), and materials (+0.5%) led the way. On the downside, energy (-0.3%), financials (+0.2%), and technology (+0.3%) lagged.

Looking back at the day's economic data, the latest weekly initial jobless claims count totaled 357,000. This was higher than the 338,000 that had been expected by the Briefing.com consensus. Today's tally was also above the revised prior week count of 341,000. As for continuing claims, they fell to 3.050 million from 3.077 million.

The third estimate of third quarter GDP showed growth of 0.4%, which was better than the 0.3% that had been expected by the Briefing.com consensus. Meanwhile, the third quarter GDP Deflator was revised up to 1.0%.

Note that equity and bond markets will be closed tomorrow in observance of Good Friday. However, a handful of economic data points will be reported on Friday. February personal income, personal spending and core PCE prices will all be reported at 8:30 ET. Lastly, the final March Michigan Consumer Sentiment Survey will be released at 9:55 ET.

Week in Review: Cyprus Remains in Focus

On Monday, the major averages ended the headline-filled session with modest losses, and the S&P 500 settled lower by 0.3%. Equities began the day amid broad strength with the early gains coming after Cyprus and the Eurogroup agreed on the terms of a rescue package for the island nation. The early gains did not hold past the opening hour after Dutch Finance Minister and Eurogroup head Jeroen Dijsselbloem gave an interview to Reuters in which he explained how the Cypriot bank restructuring may be used as a template for future bailout talks. Growth-oriented sectors were responsible for the bulk of Monday's losses. The industrial space ended as the biggest laggard amid broad weakness. Machinery producers lagged throughout the day, and Caterpillar (CAT 86.97, +0.07) lost 0.9%.

Tuesday ended with firm gains and the S&P 500 settled higher by 0.8%. After starting the day on a positive note, the benchmark average spent the balance of the session in a six-point range. Energy was the only economically-sensitive group which settled among the leaders. Crude oil contributed to the sector strength as the energy component climbed 1.5% to $96.26. Meanwhile, the SPDR Energy Select Sector (XLE 79.31, -0.23) ended higher by 1.1%.

Wednesday's session saw the S&P 500 overcome early losses to close lower by 0.1%. The index began the session lower by 0.8% as European worries remained at the forefront. The future of the eurozone was questioned as market participants speculated whether or not the European Union will copy the Cypriot playbook next time a troubled nation is in need of emergency assistance. Bank stocks reflected the uncertainty surrounding the eurozone. While most sectors ended the session well off their lows, banks settled near the bottom of today's range. The SPDR Financial Select Sector ETF ended lower by 0.5% and JPMorgan Chase (JPM 47.46, -0.31) was the weakest performer among the majors. Shares of JPMorgan fell 1.8% to close below their 50-day moving average.DJ30 +52.38 NASDAQ +11.00 SP500 +6.34 NASDAQ Adv/Vol/Dec 1375/1.54 bln/1081 NYSE Adv/Vol/Dec 1869/887.8 mln/1135

3:30 pm :

May crude oil got a boost from a weaker dollar index in today's floor trade. The energy component came off its session low of $96.38 per barrel set at pit trade open and broke into positive territory. It picked up momentum in afternoon action and settled 0.6% higher at $97.22 per barrel, slightly below its session high of $97.35 per barrel. Crude oil gained ~ 4.4% over the quarter.

May natural gas popped into positive territory and to a session high of $4.11 per MMBtu on inventory data that showed a draw of 95 bcf when a draw of 89 bcf was expected. However, the move was short lived and prices fell back into the red. Natural gas dipped to a session low of $3.97 per MMBtu in early afternoon action and settled with a 1.2% loss at $4.02 per MMBtu. Still, natural gas gained ~ 16.5% over the quarter, getting support from recent lower-than-average temperatures.

June gold traded lower today as banks reopened in Cyprus. The yellow metal popped to a session high of $1604.30 per ounce following initial claims and GDP data but quickly reversed. It trended lower for the remainder of floor trade and settled 0.7% lower at $1596.00 per ounce, bringing losses for the quarter to 5%.

May silver also fell deeper into negative territory. It dipped to a session low of $28.17 per ounce in late afternoon action and settled with a 1.0% loss at $28.33 per ounce. For the quarter, silver fell ~ 6.4%.

DJ30 +50.69 NASDAQ +8.63 SP500 +5.76 NASDAQ Adv/Vol/Dec 1411/1150.3 mln/1052 NYSE Adv/Vol/Dec 1861/381 mln/1115

3:00 pm : Heading into the final hour of trade, the S&P 500 continues to hover near its best level of the day. A quiet final hour is expected with today's closing bell also signaling the end of the first quarter.

Defensively-oriented health care and utilities have been responsible for the bulk of today's advance. In addition, those two sectors have shown relative strength in recent sessions while growth-oriented groups trailed behind the broader market.

Financials and technology continue to lag with the sectors unable to climb off yesterday's closing levels. The technology sector is seeing considerable weakness from its largest component, Apple (AAPL 442.75, -9.33), while cautious trade in major bank shares has weighed on the financial sector.DJ30 +42.89 NASDAQ +7.19 SP500 +5.10 NASDAQ Adv/Vol/Dec 1373/1.03 bln/1061 NYSE Adv/Vol/Dec 1834/343.7 mln/1138

2:30 pm : Recent trade saw little change from the major averages and the S&P 500 continues to trade higher by 0.3%. With the market set to close out the first quarter, the S&P 500 is looking at a March gain of more than 3.0%, which brings the year-to-date return of the benchmark average to 9.9%.

Notably, the health care sector was the top performer of the month, and health care stocks also appear atop today's leaderboard.

On the downside, the second half of the month brought some weakness to financials. Although the financial sector is poised to end the month in the middle of the pack, the economically-sensitive group underperformed when European worries returned to the forefront. The SPDR Financial Select Sector ETF (XLF 18.16, 0.00) is down 1.5% since March 15.DJ30 +36.67 NASDAQ +6.18 SP500 +4.38 NASDAQ Adv/Vol/Dec 1368/951.1 mln/1067 NYSE Adv/Vol/Dec 1807/319.1 mln/1129

2:00 pm : Quiet afternoon trade continues with the S&P 500 higher by 0.2%. The major averages have spent today's session in a narrow range, which has been respected for the duration of the session.

In addition, sector leadership remains unchanged from early trade with health care and utilities seeing the biggest gains. Meanwhile, financials and technology remain little changed.

The technology sector is unchanged from yesterday's close. Although most tech stocks trade higher, the largest sector component, Apple (AAPL 444.04, -8.04), is contributing to the underperformance. Shares of the largest tech company trade lower by 1.8%.DJ30 +35.41 NASDAQ +4.63 SP500 +3.85 NASDAQ Adv/Vol/Dec 1325/876.5 mln/1096 NYSE Adv/Vol/Dec 1777/297.2 mln/1159

1:30 pm : Equities continue to hover near their recent levels with the S&P 500 higher by 0.2%. Little change has been observed in sector leadership as health care and utilities continue to hover atop today's leaderboard. In addition, the materials sector trades ahead of the broader market after showing notable underperformance in recent days.

The SPDR Materials Select Sector ETF (XLB 39.13, +0.10) is higher by 0.3% today, but the sector ETF is down near 2.0% since March 18. The weakness in producers of basic materials was also reflected by the price of copper futures, which are poised to end the month at their lowest level since November. Today, copper futures are down 1.2% to $3.403 per pound.DJ30 +33.45 NASDAQ +3.97 SP500 +3.45 NASDAQ Adv/Vol/Dec 1244/794.2 mln/1158 NYSE Adv/Vol/Dec 1701/269.8 mln/1214

1:00 pm : At midday, the major averages are little changed, and the S&P 500 is higher by 0.1%.

Stocks began the final session of the holiday-shortened week on a positive note. However, the slim opening gains were erased briefly when the March Chicago PMI fell short of expectations.

For March, the Purchasing Managers' Index fell to 52.4 from the 56.8 reported in the February report. Meanwhile, the Briefing.com consensus had expected a smaller decline, to 56.5.

Although the disappointing report caused a stumble in the S&P 500, bargain hunters were quick to buy the weakness and push the benchmark average above its record close of 1565.15 set in October 2007.

Today's modest gains have been paced by defensive sectors. Health care and utilities have shown strength from the start, and they remain atop the leaderboard. The SPDR Utilities Select Sector ETF (XLU 38.88, +0.25) is higher by 0.7%, and is the top performing sector ETF.

In addition to health care and utilities, materials and industrials have outperformed the broader market after the growth-oriented sectors lagged in recent sessions. Today, the industrial sector is receiving considerable support from transportation-related stocks.

The Dow Jones Transportation Average is higher by 0.8% with railroads outperforming notably. All four railroads that comprise the transportation complex sport gains near 1.0% with Kansas City Southern (KSU 110.93, +3.19) leading the way.

On the downside, the financial sector trades with slim losses. Bank stocks have remained under pressure since the first Cypriot bailout proposal was unveiled two weeks ago. The SPDR Financial Select Sector ETF (XLF 18.13, -0.03) is off by 0.2% in today's action, and down 1.5% since last Monday.

Reviewing today's economic data, the latest weekly initial jobless claims count totaled 357,000. This was higher than the 338,000 that had been expected by the Briefing.com consensus. Today's tally was also above the revised prior week count of 341,000. As for continuing claims, they fell to 3.050 million from 3.077 million.

Lastly, the third estimate of third quarter GDP showed growth of 0.4%, which was better than the 0.3% that had been expected by the Briefing.com consensus. Meanwhile, the third quarter GDP Deflator was revised up to 1.0%.DJ30 +32.87 NASDAQ +3.23 SP500 +3.32 NASDAQ Adv/Vol/Dec 1245/740.5 mln/1151 NYSE Adv/Vol/Dec 1705/253.1 mln/1198

12:30 pm : The major averages have slipped off their highs, but the S&P 500 remains firmer by 0.1%. Although the S&P 500 trades with just a slim gain, health care and utilities trade well ahead of the broader market with the two sectors up 0.6% each.

On the downside, financials and technology continue to underperform. Bank stocks have come under pressure after the first Cypriot bailout package was rejected two weeks ago. The SPDR Financial Select Sector ETF (XLF 18.12, -0.04) is off by 0.2% in today's action, and down 1.5% since last Monday.DJ30 +23.36 NASDAQ -0.45 SP500 +1.57 NASDAQ Adv/Vol/Dec 1197/675.4 mln/1173 NYSE Adv/Vol/Dec 1604/232.5 mln/1289

12:00 pm : Equities continue to trade near their best levels of the day with the S&P 500 higher by 0.3%. With quiet trade taking place, the broad market gains are being paced by health care and utilities. In addition, industrials and materials are among today's top performers after the two sectors saw considerable weakness over the past week.

The industrial space is being supported, in part, by transportation related stocks. The Dow Jones Transportation Average is higher by 0.9% with railroads outperforming notably. All four railroads which comprise the transportation complex trade with gains over 1.0% and Kansas City Southern (KSU 111.17, +3.43) is the best performer of the four.DJ30 +49.69 NASDAQ +5.08 SP500 +4.58 NASDAQ Adv/Vol/Dec 1311/595.1 mln/1051 NYSE Adv/Vol/Dec 1743/206.1 mln/1119

11:30 am : The major averages continue to hover near their highs with the S&P 500 firmer by 0.3%. Quiet late morning trade continues as the benchmark average benefits from the outperformance of defensive sectors. Consumer staples, health care, and utilities are among the day's leaders as the counter cyclical groups continue their recent outperformance.

Meanwhile, financials and technology are little changed. Major bank shares came under pressure when the Cypriot bailout package was proposed originally, and they have continued to underperform since. Morgan Stanley (MS 22.17, -0.12) is the weakest performer among the majors, down 0.5%.

Elsewhere, the technology space trades flat as Apple (AAPL 446.50, -5.58) weighs. The largest tech stock is down 1.2%.DJ30 +53.64 NASDAQ +5.25 SP500 +4.90 NASDAQ Adv/Vol/Dec 1286/519.5 mln/1053 NYSE Adv/Vol/Dec 1738/183.2 mln/1102

11:00 am : After an early-morning stumble pushed the S&P 500 to session lows, the benchmark index was able to recover swiftly and cross above its October 2007 all-time closing high of 1565.15.

Although the S&P 500 crossed above its highest close of all-time, the index remains below its intraday high of 1576.09 notched on October 11, 2007.

As the broader market trades with slim gains, nine of 10 S&P 500 sectors trade in positive territory. Defensive sectors are among the top advancers with health care, utilities, and consumer staples in the lead. Meanwhile, energy, financials, and technology trail behind the broader market. The SPDR Financial Select Sector ETF (XLF 18.14, -0.02) is off by 0.2%, and is the worst performing sector ETF.DJ30 +48.38 NASDAQ +5.85 SP500 +3.96 NASDAQ Adv/Vol/Dec 1285/418.8 mln/1024 NYSE Adv/Vol/Dec 1706/153.1 mln/1102

10:30 am : Commodities are mixed today despite this weakness in the dollar index. Gold and silver are lower, copper is flat, natural gas and crude oil are modestly higher.

May natural gas rose as high as $4.12/MMBtu overnight, but is now -0.2% at $4.06/MMBtu just ahead of the weekly inventory data. Following the inventory data, nat gas spiked to a new HoD and is now +0.7% at $4.10/MMBtu.

Following the GDP data this morning, gold and silver spiked higher, while crude oil sold off. On that move lower, May crude oil fell to a new LoD of $96.26/barrel. In current action, crude oil is +0.2% at $96.75/barrel.

Precious metals have been trending lower today and quickly pulled back following that earlier spike on the GDP numbers. In current trade, Jun gold is -0.6% at $1597.70/oz and May silver is -0.4% at $28.50/oz. May copper is +0.01% at $3.44/lb.DJ30 +31.03 NASDAQ +2.89 SP500 +2.12 NASDAQ Adv/Vol/Dec 1179/318.0 mln/1068 NYSE Adv/Vol/Dec 1542/121 mln/1207

10:00 am : The S&P 500 has climbed off its early lows and the benchmark index is currently flat.

Most S&P 500 sectors trade in positive territory with the defensively-minded utilities space pacing the early gains. On the downside, financials and technology trade with slim losses.

In corporate earnings of note, BlackBerry (BBRY 14.93, +0.36) is higher by 2.5% after reporting a fourth quarter earnings beat on below-consensus revenue.

Reviewing the day's economic data, the latest weekly initial jobless claims count totaled 357,000, which was higher than the 338,000 that had been expected by the Briefing.com consensus.

The third estimate of third quarter GDP showed growth of 0.4%, which was better than the 0.3% that had been expected by the Briefing.com consensus. Meanwhile, the third quarter GDP Deflator was revised up to 1.0%.

Lastly, March Chicago PMI posted a reading of 52.4, which was worse than the 56.5 expected by the Briefing.com consensus.DJ30 +21.77 NASDAQ +0.81 SP500 +0.52 NASDAQ Adv/Vol/Dec 1080/208.2 mln/1069 NYSE Adv/Vol/Dec 1452/87.2 mln/1245

09:50 am : The major averages began the session with slim gains but the S&P 500 slipped into the red after the March Chicago PMI was reported at 52.4, below the 56.5 expected by the Briefing.com consensus.

The S&P 500 trades lower by 0.1% after slipping in the wake of the disappointing economic report.

Consumer staples, financials, and technology are among the early laggards while health care and utilities trade with slim gains.DJ30 -1.65 NASDAQ -1.27 SP500 -1.10 NASDAQ Adv/Vol/Dec 1086/150.3 mln/1021 NYSE Adv/Vol/Dec 1297/69.3 mln/1341

09:15 am : [BRIEFING.COM] S&P futures vs fair value: -0.50. Nasdaq futures vs fair value: flat. Heading into the open, index futures indicate little change at the start of the session. The S&P 500 is set to begin today's action less than three points away from its October 9, 2007 record close of 1565.15.

Today's action will punctuate a month which saw the benchmark index rise more than 3.0% with consumer staples and health care ending as the top performing sectors. The defensively-oriented groups saw increased interest during the second half of March when European worries returned to the forefront and resulted in money moving out of cyclical sectors and into defensive ones.

While countercyclical sectors outperformed the broader market in the second half of the month, economically-sensitive financials, industrials, and materials each lost more than 1.0% in the final two weeks of March.

March Chicago PMI will be reported at 9:45 ET.

The U.S. Treasury will auction off $29 billion in 7-yr notes.

09:00 am : [BRIEFING.COM] S&P futures vs fair value: -1.50. Nasdaq futures vs fair value: -0.50.

U.S. equity futures trade in mixed fashion with the S&P 500 futures off by 0.1%.

The major Asian bourses ended mostly lower as European worries remained front and center. China's Shanghai Composite (-2.8%) saw heavy selling with financials pacing the decline after Beijing announced more regulation on wealth management products. Elsewhere, comments from Bank of Japan Governor Kuroda failed to inspire the Nikkei (-1.2%). Mr. Kuroda suggested the current bond buying plan will not be enough to target 2% inflation, and that the central bank intends to purchase foreign bonds as well as JGBs. Data from the region saw Japanese retail sales post a weak -2.3% year-over-year (0.9% expected), Australian private sector credit miss (0.2% month-over-month actual v. 0.3% expected), and Thai industrial production slump 1.2% year-over-year.

In Japan, the Nikkei closed lower by 1.3% as exporters remained under pressure. Sony shed 3.0% and Canon gave up 2.1%. Elsewhere, Dreamliner's battery maker, GS Yuasa, plunged 11.1% after Mitsubishi Motors reported problems with one of its batteries made by the company.

Hong Kong's Hang Seng finished lower by 0.7% as financials were under pressure. Bank of China slipped 0.6% and Bank of Communications shed 4.0%.

In China, the Shanghai Composite shed 2.8% as financials were hit hard. China Citic Bank tumbled 9.1% and China Merchants Bank gave up 5.0%.

European indices trade near their highs following the release of several German economic data points. The country's retail sales rose 0.4% month-over-month (-1.0% consensus) while the year-over-year reading posted a decline of 2.2% (+0.4% consensus). Germany also reported worse-than-expected unemployment change of 13,000 (-4,000 consensus) while its unemployment rate remained unchanged at 6.9%, as expected. Elsewhere, Italian business confidence ticked up to 88.9 from the 88.6 reported in the prior month's reading (88.0 expected). Also of note, Eurozone retail PMI slipped to 43.70 from the prior month's reading of 44.50.

In news, the Bank of Italy said the country's GDP may see a bigger contraction in 2013 than the previously expected decline of 1.3%. In Cyprus, banks reopened with strict capital controls in place and withdrawals limited to EUR300 per day.

Germany's DAX is higher by 0.4% with defensive consumer and healthcare names in the lead. Bayer and Henkel are both up near 2.0%. On the downside, exporters BMW and Daimler are both down near 1.2%.

In France, the CAC is rising 0.6% with financials in the lead. BNP Paribas and Credit Agricole trade with respective gains of 2.3% and 3.1%.

The United Kingdom's FTSE is up 0.7% as consumer names pace the advance. InterContinental Hotels Group and Tate & Lyle are higher by 3.5% and 2.4%, respectively. On the downside, miners trail behind the broader market. Antofagasta and Eurasian Natural Resources are both down 3.8%.

08:33 am : [BRIEFING.COM] S&P futures vs fair value: +0.80. Nasdaq futures vs fair value: +3.20. Equity futures saw little change in reaction to the latest GDP and initial claims data. The S&P 500 futures are higher by 0.1%.

The latest weekly initial jobless claims count totaled 357,000, which was higher than the 338,000 that had been expected by the Briefing.com consensus. Today's tally was above the revised prior week count of 341,000. As for continuing claims, they fell to 3.050 million from 3.077 million.

Lastly, the third estimate of third quarter GDP showed growth of 0.4%, which was better than the 0.3% that had been expected by the Briefing.com consensus. Meanwhile, the third quarter GDP Deflator was revised up to 1.0%.

07:59 am : [BRIEFING.COM] S&P futures vs fair value: +0.60. Nasdaq futures vs fair value: +2.70.

U.S. equity futures trade modestly higher with the S&P 500 futures up 0.1%.

Looking at overseas developments:

Asian markets ended lower. Hong Kong's Hang Seng shed 0.7%, Japan's Nikkei lost 1.3%, and China's Shanghai Composite fell 2.8%.

In regional economic data:

Japanese retail sales declined 2.3% year-over-year while the consensus expected a decline of 1.2%.

In New Zealand, building consents rose 1.9%, less than the increase of 3.0% that had been expected by the market.

Looking at news:

Chinese equities declined amid the expectation the country's government could begin implementing property curbs in some cities as early as April.

European indices trade with modest gains as the session nears midday. France's CAC is higher by 0.2%, Germany's DAX is adding 0.3%, and the United Kingdom's FTSE is rising 0.6%.

Looking at economic data:

German retail sales rose 0.4% month-over-month (-1.0% consensus) while the year-over-year reading posted a decline of 2.2% (+0.4% consensus). Germany also reported worse-than-expected unemployment change of 13,000 (-4,000 consensus) while its unemployment rate remained unchanged at 6.9%, as expected.

Italian business confidence ticked up to 88.9 from the 88.6 reported in the prior month's reading (88.0 expected).

Eurozone retail PMI slipped to 43.70 from the prior month's reading of 44.50.

In news:

The Bank of Italy said the country's GDP may see a bigger contraction in 2013 than the previously expected decline of 1.3%.

In Cyprus, banks reopened with strict capital controls in place and withdrawals limited to EUR300 per day.

In U.S. corporate news:

BlackBerry (BBRY 14.08, -0.49) is down 3.7% after its fourth quarter results fell short of revenue expectations.

Dollar General (DG 50.15, -0.80) is lower by 1.6% after announcing the pricing of a 30-million share secondary offering at $50.75 per share.

Weekly initial and continuing claims will be reported at 8:30 ET. In addition, the third estimate of fourth quarter GDP and GDP deflator will also be announced at 8:30 ET. Lastly, March Chicago PMI will be released at 9:45 ET.

The U.S. Treasury will auction off $29 billion in 7-yr notes.

06:21 am : [BRIEFING.COM] S&P futures vs fair value: -2.00. Nasdaq futures vs fair value: -3.00.

06:21 am : Nikkei...12335.96...-157.80...-1.30%. Hang Seng...22299.63...-165.20...-0.70%.

06:21 am : FTSE...6396.73...+9.10...+0.10%. DAX...7801.07...+11.70...+0.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com HomepageMarket Update