Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

121712-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+600.00.png [ 76.01 KiB | Viewed 275 times ]

121712-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+600.00.png [ 76.01 KiB | Viewed 275 times ]

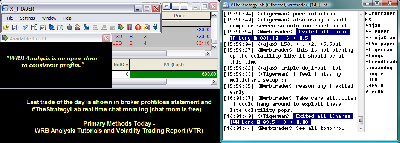

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$600.00 dollars or +6.00 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $600.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with

price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=111&t=1393 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=197&t=1686 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

Attachment:

121712-Key-Price-Action-Markets.png [ 527.17 KiB | Viewed 310 times ]

121712-Key-Price-Action-Markets.png [ 527.17 KiB | Viewed 310 times ]

Market Update

Market Update 4:20 pm : The major averages registered broad gains during today's session. The S&P 500 followed a modestly higher open with a steady climb to its highs. Shortly before midday, reports out of Washington indicated President Obama and House Speaker Boehner held a 45-minute conversation in an attempt to further the ongoing budget debate. The developments had little effect on the markets as the key indices continued their upward drift. As a result, the S&P 500 finished higher by 1.2%.

The financial sector paced the advance, and the SPDR Financial Select Sector ETF (XLF 16.33, +0.33) gained 2.1%. Weekend reports indicated Speaker Boehner offered to accept a tax hike for top earners if the new revenue is met with spending cuts. However, the White House has rejected the offer. While a deal remains elusive, the presence of discussion between the lawmakers is being received as a positive sign by the market. Among the majors, Goldman Sachs (GS 123.49, +4.13) and Morgan Stanley (MS 18.53, +0.48) both advanced near 3.0%.

Discretionary stocks also outperformed, and homebuilders contributed to the strength. DR Horton (DHI 19.69, +0.95), PulteGroup (PHM 18.04, +0.90), and Toll Brothers (TOL 32.22, +1.37) all gained between 4.4% and 5.3%.

Automakers and manufacturers of auto parts also showed relative strength. Ford Motor (F 11.39, +0.29) and Cooper Tire & Rubber (CTB 25.04, +0.97) finished higher by 2.6% and 4.0%, respectively.

In M&A news, Caribou Coffee (CBOU 16.10, +3.78) will be acquired by Joh. A. Benckiser for $16.00 per share. The transaction carries a total value of approximately $340 million, and the purchase price represents a 29.9% premium to Caribou's Friday closing price.

Among tech shares, Apple (AAPL 518.83, +9.04) was down as much as 1.5% intraday, but after a brief dip near $500, bargain hunters lifted the largest tech component to a gain of 1.8%. Earlier, Citigroup downgraded the stock to ‘Neutral' from ‘Buy.' The move came weeks after the company's November 26 initiation with a ‘Buy.' In addition, three investment banks lowered their price targets for Apple. Canaccord Genuity dropped its target to $750 from $800, Pacific Crest cut its estimate to $565 from $645, and Mizuho slashed its target to $600 from $750. Apple suppliers saw notable losses on Friday, but the group outperformed today. Skyworks Solution (SWKS 20.75, +0.95) advanced 4.8% and Qualcomm (QCOM 62.04, +2.20) rose by 3.7%.

The Dow Jones Transportation Average finished in-line with the remaining industrials. Of the twenty stocks which constitute the transportation complex, seventeen registered gains. Airlines saw broad strength after Dahlman Rose upgraded its outlook on the industry from neutral to bullish. JetBlue Airways (JBLU 5.71, +0.18) and Alaska Air (ALK 43.98, +0.82) outperformed their peers and gained 3.3% and 1.9%, respectively.

On the downside, Con-Way (CNW 27.47, -0.60) lost 2.1% after BB&T Capital Markets downgraded the stock to ‘Underweight' from ‘Hold.' The downgrade comes as BB&T believes Con-Way's consensus estimates are materially too high.

Also of note, Ryder System (R 48.82, -0.78) slipped 1.6% after the company announced Chief Executive Officer Gregory Swienton will retire at the time of the company's annual meeting of shareholders on May 3, 2013.

European markets ended the day on a mixed note. France's CAC and UK's FTSE saw respective losses of 0.1% and 0.2% while Germany's DAX added 0.1%.

In the United Kingdom, Aggreko lost 21.7% and was the weakest performer. The plunge followed cautious comments from the company regarding its 2013 profit expectations. On the upside, International Consolidated Airlines Group led the way with a 3.3% gain. In addition, miners outperformed. Anglo American, Kazakhmys, and Rio Tinto all gained between 1.6% and 3.2%.

In France, financials weighed on the index. BNP Paribas shed 0.7% and Credit Agricole lost 0.9%. On the upside, Alcatel-Lucent (ALU 1.32, +0.08) surged 5.8% to extend its recent strength.

In Germany, carmakers outperformed. Daimler advanced 1.9% after merging its two Mercedes units in China. Also of note, Infineon Technologies rose by 1.6% after the company's Chief Executive Officer said Infineon may make a handful of small-to-medium acquisitions. Drug makers and suppliers of medical products underperformed. Fresenius Medical, Fresenius SE, and Merck (MRK 43.63, +0.09) all lost near 1.0%.

Reviewing today's economic data, the December Empire State Manufacturing Survey registered a reading of -8.1, which was down from the prior month's reading of -5.2, and worse than the reading of 2.0 expected by the Briefing.com consensus.

Meanwhile, the October net long-term TIC flows report indicated a $1.3 billion inflow of foreign capital into U.S. denominated assets. This follows the prior month's $3.3 billion inflow.

Tomorrow, the third quarter current account balance will be reported at 8:30 ET and the December NAHB Housing Market Index will be released at 9:00 ET.

The U.S. Treasury will auction off $35 billion in 5-yr notes.DJ30 +100.38 NASDAQ +39.27 SP500 +16.78 NASDAQ Adv/Vol/Dec 1720/1.85 bln/772 NYSE Adv/Vol/Dec 2042/702.1 mln/1007

3:30 pm : Crude oil extended Friday's gains as the dollar index retreated to new session lows. The energy component came off its pit session low of $86.70 per barrel and traded up to a session high of $87.71 per barrel. However, prices pulled-back heading into the close, and crude settled with a 0.4% loss at $87.13 per barrel.

Natural gas advanced for the first time in eight sessions as it lifted off its session low of $3.32 per MMBtu. Despite retreating from its session high of $3.39 per MMBtu, it booked a 1.2% gain as it closed at $3.36 per MMBtu.

Gold erased overnight losses as it lifted off its pit session low of $1691.30 per ounce following manufacturing data that came in well below estimates. The yellow metal then chopped around the unchanged level for the remainder of the session and settled with a 0.1% gain at $1697.90 per ounce.

Silver traded up to a session high of $32.45 per ounce in morning floor action but lost momentum and slid to a session low of $32.08 per ounce. It managed to erase most of the loss and settled just 0.1% lower at $3.67 per ounce.DJ30 +75.73 NASDAQ +26.31 SP500 +12.23 NASDAQ Adv/Vol/Dec 1539/2661.9 mln/944 NYSE Adv/Vol/Dec 1871/427 mln/1175

3:00 pm : The major averages are holding their recent levels as trade enters the final hour.

Less than fifty companies covered by Briefing.com are scheduled to report their earnings this week. Most notably, economic bellwether FedEx (FDX 90.74, +0.65) will reveal its quarterly results ahead of Wednesday's opening bell.

Tomorrow morning, Jefferies Group (JEF 18.27, +0.17) and Sanderson Farms (SAFM 49.90, +0.16) are scheduled to report. The Capital IQ consensus expects Jefferies to announce earnings of $0.34 on $739.85 million in revenue. Elsewhere, Sanderson Farms is expected to report $0.28 in earnings on revenue of $625.67.DJ30 +61.08 NASDAQ +23.88 SP500 +11.04 NASDAQ Adv/Vol/Dec 1533/1.39 bln/957 NYSE Adv/Vol/Dec 1865/380.3 mln/1168

2:30 pm : Equities are holding their levels and the S&P 500 is higher by 0.7%.

The consumer staples sector has been pressured in afternoon trade and the SPDR Consumer Staples Select Sector ETF (XLP 35.94, -0.02) is currently off by 0.1%.

The afternoon weakness among staple stocks has been due to underperformance from major sector components. Names like Coca-Cola (KO 37.40, -0.26), Procter & Gamble (PG 69.68, -0.25), and Philip Morris (PM 87.25, -0.49) have been sliding steadily during the last 90 minutes.DJ30 +51.15 NASDAQ +19.90 SP500 +9.78 NASDAQ Adv/Vol/Dec 1488/1.3 bln/984 NYSE Adv/Vol/Dec 1836/354.2 mln/1186

2:00 pm : The S&P 500 has retreated off its highs, but the index remains firmly in the black, up 0.7%.

The materials sector is underperforming the broader market as mining stocks weigh. The Market Vectors Gold Miners ETF (GDX 46.36, -0.11) is off by 0.3% and Freeport-McMoRan (FCX 33.63, -0.15) is shedding 0.4%.

On Friday, steelmakers advanced broadly after China's HSBC PMI pointed to a second consecutive month of expansionary activity. Today, most producers are extending their gains. Reliance Steel (RS 59.58, +0.33) and Steel Dynamics (STLD 13.66, +0.08) are both higher by 0.6%.DJ30 +59.09 NASDAQ +21.00 SP500 +10.20 NASDAQ Adv/Vol/Dec 1546/1.2 bln/922 NYSE Adv/Vol/Dec 1878/323.5 mln/1125

1:30 pm : The Dow Jones Transportation Average is higher by 0.4%, but the bellwether complex is underperforming the remaining industrials.

Of the twenty stocks which constitute the transportation average, seventeen are registering gains. Airlines are seeing broad strength after Dahlman Rose upgraded its outlook on the industry from neutral to bullish. JetBlue Airways (JBLU 5.73, +0.20) and Alaska Air (ALK 44.03, +0.87) are seeing respective gains of 3.5% and 2.0% as they outperform their peers.

On the downside, Con-Way (CNW 27.16, -0.91) was downgraded to ‘Underweight' from ‘Hold' at BB&T Capital Markets. The downgrade comes as BB&T believes Con-Way's consensus estimates are materially too high.

Also of note, Ryder System (R 48.76, -0.84) is slipping 1.7% after the company announced Chief Executive Officer Gregory Swienton will retire at the time of the company's annual meeting of shareholders on May 3, 2013.DJ30 +76.22 NASDAQ +26.40 SP500 +12.52 NASDAQ Adv/Vol/Dec 1552/1.1 bln/907 NYSE Adv/Vol/Dec 1923/295.9 mln/1068

1:00 pm : Today's session began on an upbeat note and the major averages followed the strong open with a climb to their respective highs. In addition, the S&P 500 received a mid-morning boost when reports out of Washington indicated President Obama and House Speaker Boehner held a 45-minute conversation in an attempt to further the ongoing budget debate. At midday, the benchmark average is higher by 1.0%.

The financial sector is pacing the advance and the SPDR Financial Select Sector ETF (XLF 16.28, +0.28) is firmer by 1.7%. Weekend reports indicated House Speaker Boehner has offered to accept a tax hike for top earners if the new revenue is met with spending cuts. However, the White House has rejected the offer. While a deal remains elusive, the presence of discussion between the lawmakers is being received as a positive sign by the market. Among the majors, Goldman Sachs (GS 122.13, +2.77) and Morgan Stanley (MS 18.48, +0.43) are both up near 2.3%.

Discretionary stocks are also seeing relative strength and homebuilders are contributing to the outperformance. DR Horton (DHI 19.58, +0.84), PulteGroup (PHM 17.95, +0.81), and Toll Brothers (TOL 32.21, +1.36) are all up between 4.4% and 5.0%.

In M&A news, Caribou Coffee (CBOU 16.00, +3.68) will be acquired by Joh. A. Benckiser for $16.00 per share. The transaction carries a total value of approximately $340 million, and the purchase price represents a 29.9% premium to Caribou's Friday closing price.

Automakers and manufacturers of auto parts are also seeing strength among discretionary stocks. Ford Motor (F 11.30, +0.20) and Cooper Tire & Rubber (CTB 24.78, +0.71) are up 1.8% and 3.0%, respectively.

In notable analyst action, Finish Line (FINL 17.70, -0.26) is lower by 1.5% after Canaccord Genuity downgraded the stock to ‘Hold' from ‘Buy' with a $20 price target.

European markets have closed for the day, and the major indices ended on a mixed note. France's CAC and UK's FTSE saw respective losses of 0.1% and 0.2% while Germany's DAX added 0.1%.

In the United Kingdom, Aggreko lost 21.7% and was the weakest performer. The plunge followed cautious comments from the company regarding its 2013 profit expectations. On the upside, International Consolidated Airlines Group led the way with a 3.3% gain. In addition, miners outperformed. Anglo American, Kazakhmys, and Rio Tinto all gained between 1.6% and 3.2%.

In France, financials weighed on the index. BNP Paribas shed 0.7% and Credit Agricole lost 0.9%. On the upside, Alcatel-Lucent (ALU 1.33, +0.09) surged 5.8% to extend its recent strength.

In Germany, carmakers outperformed. Daimler advanced 1.9% after merging its two Mercedes units in China. Also of note, Infineon Technologies rose by 1.6% after the company's Chief Executive Officer said Infineon may make a handful of small-to-medium acquisitions. Drug makers and suppliers of medical products underperformed. Fresenius Medical, Fresenius SE, and Merck (MRK 43.78, +0.23) all lost near 1.0%.

Reviewing today's economic data, the December Empire State Manufacturing Survey registered a reading of -8.1, which was down from the prior month's reading of -5.2, and worse than the reading of 2.0 expected by the Briefing.com consensus.

The October net long-term TIC flows report indicated a $1.3 billion inflow of foreign capital into U.S. denominated assets. This follows the prior month's $3.3 billion inflow.DJ30 +78.20 NASDAQ +29.60 SP500 +13.13 NASDAQ Adv/Vol/Dec 1582/1.02 bln/865 NYSE Adv/Vol/Dec 1948/272.1 mln/1020

12:30 pm : The major averages have marked fresh highs and the S&P 500 is firmer by 1.0%.

European markets have closed for the day, and the major indices ended on a mixed note. France's CAC and UK's FTSE saw respective losses of 0.1% and 0.2% while Germany's DAX added 0.1%.

In the United Kingdom, Aggreko lost 21.7% and was the weakest performer. The plunge followed cautious comments from the company regarding its 2013 profit expectations. On the upside, International Consolidated Airlines Group led the way with a 3.3% gain. In addition, miners outperformed. Anglo American, Kazakhmys, and Rio Tinto all gained between 1.6% and 3.2%.

In France, financials weighed on the index. BNP Paribas shed 0.7% and Credit Agricole lost 0.9%. On the upside, Alcatel-Lucent (ALU 1.33, +0.09) surged 5.8% to extend its recent strength.

In Germany, carmakers outperformed. Daimler advanced 1.9% after merging its two Mercedes units in China. Also of note, Infineon Technologies rose by 1.6% after the company's Chief Executive Officer said Infineon may make a handful of small-to-medium acquisitions. Drug makers and suppliers of medical products underperformed. Fresenius Medical, Fresenius SE, and Merck (MRK 43.83, +0.28) all lost near 1.0%.DJ30 +90.51 NASDAQ +32.21 SP500 +14.32 NASDAQ Adv/Vol/Dec 1618/938.2 mln/817 NYSE Adv/Vol/Dec 2015/251.5 mln/977

12:00 pm : The S&P 500 has risen to a fresh session high after reports from Washington indicated President Obama and House Speaker Boehner have met to engage in a 45-minute conversation to continue the budget debate. Currently, the benchmark average is higher by 0.9%.

Discretionary stocks are outperforming the broader market and homebuilders are contributing to the relative strength. DR Horton (DHI 19.41, +0.67), PulteGroup (PHM 17.95, +0.81), and Toll Brothers (TOL 32.11, +1.26) are all up between 3.5% and 5.0%.

In M&A news, Caribou Coffee (CBOU 16.02, +3.70) will be acquired by Joh. A. Benckiser for $16.00 per share. The transaction carries a total value of approximately $340 million and the purchase price represents a 29.9% premium to Caribou's Friday closing price.

Automakers and manufacturers of auto parts are also seeing strength among discretionary stocks. Ford Motor (F 11.27, +0.17) and Cooper Tire & Rubber (CTB 24.89, +0.81) are up 1.6% and 3.4%, respectively.

In notable analyst action, Finish Line (FINL 17.69, -0.27) is lower by 1.5% after Canaccord Genuity downgraded the stock to ‘Hold' from ‘Buy' with a $20 price target.DJ30 +76.48 NASDAQ +26.79 SP500 +12.00 NASDAQ Adv/Vol/Dec 1563/848.2 mln/846 NYSE Adv/Vol/Dec 1975/227.2 mln/996

11:35 am : The major averages continue to trade near their highs as the S&P 500 adds 0.7%.

Telecom stocks are underperforming the broader market and the sector is the only S&P 500 group trading in the red. Sprint Nextel (S 5.54, -0.01) is modestly lower following the acquisition of Clearwire (CLWR 2.92, -0.44) for $2.97 per share. As a result of the transaction, Clearwire shareholders will receive $2.2 billion. MetroPCS (PCS 9.82, -0.23), which was discussed as a potential takeover target for Sprint earlier this year, is sliding 2.3% on the news.

Among major sector components, Verizon Communications (VZ 43.88, -0.32) is off by 0.7%.DJ30 +72.81 NASDAQ +20.21 SP500 +10.72 NASDAQ Adv/Vol/Dec 1534/931.8 mln/826 NYSE Adv/Vol/Dec 1927/197.8 mln/999

11:00 am : The major averages are holding their levels and the S&P 500 is higher by 0.6%.

The technology sector is underperforming the broader market and the SPDR Technology Select Sector ETF (XLK 28.77, +0.08) is adding 0.3%. The biggest sector component, Apple (AAPL 506.25, -3.54) remains in focus as the shares trade lower by 0.6%. Earlier Citigroup downgraded the stock to ‘Neutral' from ‘Buy.' The move comes weeks after the November 26 initiation with a ‘Buy.' In addition, three investment banks have lowered their price targets for Apple. Canaccord Genuity lowered its target to $750 from $800, Pacific Crest cut its estimate to $565 from $645, and Mizuho slashed its target to $600 from $750.

Apple suppliers saw notable losses on Friday, but the group is seeing relative strength today. Skyworks Solution (SWKS 20.01, +0.40) is advancing 2.0% and Qualcomm (QCOM 60.92, +1.09) is higher by 1.8%.

Also of note, Google (GOOG 713.68, +11.71) is higher by 1.7% following New York Times reports which indicated Google is nearing a settlement agreement in an ongoing antitrust investigation.

Elsewhere in technology, Compuware (CPWR 11.03, +1.50) is surging 15.9% after Elliott Management Corporation agreed to acquire the company for $11.00 per share. The transaction carries a total value of $2.3 billion and the purchase price represents a 15.4% premium to CPWR's Friday close.DJ30 +50.57 NASDAQ +12.20 SP500 +7.71 NASDAQ Adv/Vol/Dec 1381/591.8 mln/925 NYSE Adv/Vol/Dec 1719/161.5 mln/1161

10:30 am : The dollar index sold off about 50 minutes ago, but didn't do much for commodities, except for oil, which soared to a new session high. Jan crude oil rallied as high as $87.62/barrel and is now +0.9% at $87.49/barrel.

Natural gas has been trading inversely to crude oil, at least is recent activity this morning. Nat gas sold off from its morning high range back near the flat line. The Jan contract is now +0.7% at $3.34/MMBtu.

Precious metals rose sharply following the Empire Manufacturing data, pushing to new session highs. Gold has since gained slightly further and hit a new session minutes ago. Silver, on the other hand, has sold off back near the unchanged mark after that rally. In current action, Feb gold is +0.2% at $1700/oz and Mar silver is +0.0.3% at $32.31/oz.

DJ30 +57.70 NASDAQ +9.29 SP500 +7.64 NASDAQ Adv/Vol/Dec 1395/478.5 mln/865 NYSE Adv/Vol/Dec 1766/133 mln/1071

10:00 am : Equities continue to trade near their respective highs and the S&P 500 is adding 0.6%.

The financial sector is pacing the advance and the SPDR Financial Select Sector ETF (XLF 16.23, +0.23) is firmer by 1.4%. Weekend reports indicated House Speaker Boehner has offered to accept a tax hike for top earners if the new revenue is met with spending cuts. However, the White House has rejected the offer. While a deal remains elusive, the presence of discussion between the lawmakers is being seen as a positive sign by the market. Among the majors, Goldman Sachs (GS 122.05, +2.69) and Morgan Stanley (MS 18.37, +0.32) are both up near 2.0%.DJ30 +64.65 NASDAQ +13.54 SP500 +8.92 NASDAQ Adv/Vol/Dec 1487/309.8 mln/700 NYSE Adv/Vol/Dec 1879/93.3 mln/905

09:45 am : Equities are holding their early gains as the major averages trade near their respective highs. The S&P 500 is adding 0.5%.

Looking at the early sector alignment, financials, utilities, and technology stocks are all outperforming. Meanwhile, consumer staples and telecoms are showing relative weakness.

Apple (AAPL 512.96, +3.17) is adding 0.5% after displaying notable pre-market weakness. Similarly, Apple supplier, Cirrus Logic (CRUS 26.65, +1.06) is rising by 4.3% after losing over 6.0% on Friday.DJ30 +59.44 NASDAQ +17.85 SP500 +8.17 NASDAQ Adv/Vol/Dec 1441/200.5 mln/656 NYSE Adv/Vol/Dec 1830/69.2 mln/899

09:15 am : S&P futures vs fair value: +6.10. Nasdaq futures vs fair value: +4.00. Heading into the open, equity futures are pointing to a higher start. The S&P 500 futures are higher by 0.3%.

In M&A news, Caribou Coffee (CBOU 12.32, 0.00) will be acquired by Joh. A. Benckiser for $16.00 per share. The transaction carries a total value of approximately $340 million and the purchase price represents a 29.9% premium to Caribou's Friday closing price.

In notable downgrades, Con-Way (CNW 27.60, -0.47) is slipping 1.7% after BB&T downgraded the stock to ‘Underweight' from ‘Hold.' Elsewhere, Texas Instruments (TXN 30.33, -0.47) is lower by 1.5% after Sterne Agee downgraded the technology stock to ‘Underperform' from ‘Neutral' with a $27 price target.

Reviewing today's economic data, the December Empire State Manufacturing Survey registered a reading of -8.1, which was down from the prior month's reading of -5.2, and worse than the reading of 2.0 expected by the Briefing.com consensus.

Meanwhile, the October net long-term TIC flows report indicated a $1.3 billion inflow of foreign capital into U.S. denominated assets. This follows the prior month's $3.3 billion inflow.

09:04 am : [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +6.30. U.S. equity futures are near the middle of their pre-market range, and the S&P 500 futures are adding 0.4%.

The major Asian bourses ended mixed with outperformance coming from Japan's Nikkei (+0.9%) and China's Shanghai Composite (+0.5%). The Nikkei led the regional bourses after Shinzo Abe unseated current Prime Minister Yoshihiko Noda in the Lower House election. Mr. Abe will now serve his second term as Japanese Prime Minister, a position he last held in 2007. The pair strengthened to a 20-month high of 84.36 following Mr. Abe's victory, but has since slipped back below the key 84.00 level. Next week's two-day Bank of Japan meeting is now in focus as Mr. Abe has already called for more aggressive measures from the central bank. Elsewhere, China's Shanghai Composite gained 0.5% despite headlines suggesting China's new leadership may be tolerant of slower growth. The leaders are looking for a higher "quality and efficiency" of growth going forward as the country looks to be on track for its slowest pace of growth since 1999. There was no data from the region.

In Japan, the Nikkei advanced 0.9% to end at its best level in more than nine months. Robotics maker Fanuc added 1.4% and Nissan Motor jumped 1.8% as exporters continued to gain on the weaker yen. Utilities were also strong as Mr. Abe's platform was against a nuclear-free country. Tokyo Electric Power surged 32.9% and Kansai Electric jumped 17.7%.

Hong Kong's Hang Seng finished lower by 0.4% as traders booked profits following the recent gains. Property developers were under pressure as China Overseas Land and China Resources Land both shed close to 1.0%. Elsewhere, shares of AIA were halted after AIG announced it was selling the remainder of its 13.7% stake in the company.

In China, the Shanghai Composite gained 0.5% as commodity-related names paced the advance. Yanzhou Coal Mining added 2.9% and Sinopec Shanghai Petrochemical tacked on 2.8% to lead their respective sectors.

European markets are generally lower amid limited economic data. The Eurozone labor cost index rose by 2.0% year-over-year. Meanwhile, the region's trade balance came in at EUR7.9 billion, while expectations called for a reading of EUR10.8 billion. In news, German Chancellor Angela Merkel said Europe will need to "work very hard" in order to preserve its social welfare system. Elsewhere, Germany's Bundesbank expects the country's economy to have suffered a notable contraction during the fourth quarter. In addition, the central bank expects the German economy to grow at a rate of 0.4% in 2013.

In the United Kingdom, the FTSE is lower by 0.5% and consumer stocks are underperforming. Aggreko is sliding 17.4% after the company made cautious comments about its 2013 profit expectations. On the upside, miners are outperforming. Kazakhmys, Rio Tinto, and Vedanta Resources are all up between 0.8% and 1.9%.

France's CAC is shedding 0.4% and consumer names are relatively weaker as well. Food processor Danone is lower by 1.4% and drug maker Sanofi is dipping 1.2%. Meanwhile, industrials are outperforming. Bouygues and Renault are seeing respective gains of 2.3% and 2.6%.

In Germany, the DAX is flat. Infineon Technologies is rising by 1.2% after the company's Chief Executive Officer said Infineon may make a handful of small-to-medium acquisitions. On the downside, supplier of medical products, Fresenius SE, is slipping 1.4%.

In economic news, the October net long-term TIC flows report indicated a $1.3 billion inflow of foreign capital into U.S. denominated assets. This follows the prior month's $3.3 billion inflow.

08:31 am : [BRIEFING.COM] S&P futures vs fair value: +8.10. Nasdaq futures vs fair value: +8.50. U.S. equity futures are near their pre-market highs and the S&P 500 futures are adding 0.4%.

The Empire Manufacturing Survey for December registered a reading of -8.1, which is down from the prior month's reading of -5.2. Economists polled by Briefing.com had expected that the Survey would rise to 2.0.

08:00 am : S&P futures vs fair value: +5.40. Nasdaq futures vs fair value: -1.00. U.S. equity futures are mixed amid cautious European trade. The S&P 500 futures are adding 0.2% while Nasdaq futures are off by 0.1% due to weakness in shares of Apple (AAPL 503.15, -6.64). The largest tech component is shedding 1.3% in pre-market trade.

Overnight, the global equity markets were mixed and regional developments have driven their corresponding markets. As expected, Japan's LDP party won the country's election by a landslide. This means former Prime Minister Shinzo Abe will once again return to the seat. Upon his election, Mr. Abe wasted no time calling on the Bank of Japan to take more aggressive measures. This comes before a 2-day policy meeting scheduled to start on Wednesday. The Nikkei responded to the developments with a gain of 0.9%. In China, the Shanghai Composite advanced 0.5% following China's Central Economic Work Conference. Much of the conference was broad commentary, reiterating talk of urbanization and stressing importance of domestic demand over exports. The next meeting will be held in March. Elsewhere, Hong Kong's Hang Seng slipped 0.4%.

European markets are generally lower amid limited economic data. The Eurozone labor cost index rose by 2.0% year-over-year. Meanwhile, the region's trade balance came in at EUR7.9 billion, while expectations called for a reading of EUR10.8 billion. In news, German Chancellor Angela Merkel said that Europe will need to "work very hard" in order to preserve its social welfare system. Looking at regional indices, UK's FTSE is down 0.5%, France's CAC is off by 0.4%, and Germany's DAX is shedding 0.1%.

In U.S. corporate news, Apple is lower by 1.3% after Citigroup downgraded the stock to ‘Neutral' from ‘Buy.' The move comes weeks after Citigroup initiated Apple with a ‘Buy' on November 26.

Sprint Nextel (S 5.63, +0.08) is adding 1.4% after committing to acquire 100% ownership of Clearwire (CLWR 3.08, -0.29) for $2.97 per share. As a result, Clearwire shareholders will receive $2.2 billion.

Today's economic data is limited to the December Empire Manufacturing Index and October net long-term TIC flows. The two data points will be reported at 8:30 ET and 9:00 ET, respectively.

06:36 am : [BRIEFING.COM] S&P futures vs fair value: +4.50. Nasdaq futures vs fair value: -10.00.

06:36 am : Nikkei...9828.88...+91.30...+0.90%. Hang Seng...22513.61...-92.40...-0.40%.

06:36 am : FTSE...5885.47...-36.10...-0.60%. DAX...7583.06...-13.40...-0.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage