Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

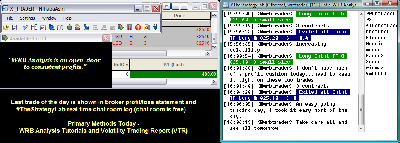

110112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+480.00.png [ 76.75 KiB | Viewed 327 times ]

110112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+480.00.png [ 76.75 KiB | Viewed 327 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$480.00 dollars or +4.80 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $480.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1359 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading (day trading, swing trading, position trading) and reactions to the markets...something I can

not get from my broker statements alone.

U.S. Market Wrap Nov. 1 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market. U.S. stocks rose, giving benchmark indexes their biggest advance in seven weeks, as reports on employment and manufacturing topped estimates while consumer confidence climbed in October to a more than four-year high.

Stocks Rally Into November Attachment:

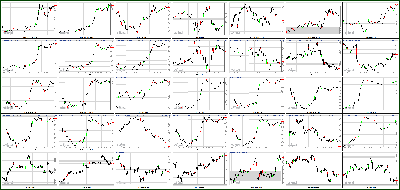

110112-Key-Price-Action-Markets.png [ 530.51 KiB | Viewed 306 times ]

110112-Key-Price-Action-Markets.png [ 530.51 KiB | Viewed 306 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- U.S. stocks started November with a strong rally Thursday, following mostly upbeat jobs reports. All three major indexes jumped more than 1%, as Wall Street continues to recover from a two-day trading suspension due to Superstorm Sandy.

The Dow Jones industrial average rose 135 points, or 1%, the Nasdaq increased 1.4% and the S&P 500 jumped 1.1%.

The gains came as investors parsed through a bevy of corporate and economic news, including planned job cuts, private sector job gains and initial unemployment claims. Those numbers are all a prelude to the government's monthly jobs report , which will be released before markets open Friday.

While outplacement firm Challenger, Gray & Christmas reported the number of planned job cuts surged to a five-month high in October, two other reports were positive. Payroll processor ADP said U.S. private-sector employers added 158,000 jobs in October, which was above expectations, and weekly initial jobless claims fell by 9,000 to 363.000 last week, coming in lower than forecasts.

"The employment numbers look a little stronger than we were anticipating," said Kim Forrest, senior equity analyst at Fort Pitt Capital. But Forrest warned that doesn't necessarily mean the October jobs report will be stronger than expected.

Related: What to expect from the jobs report

"From all the chatter that we've been listening to during company earnings calls, it doesn't seem like American companies have been doing much hiring," she said. "There may be some job growth at small businesses, but even with that, I'd be surprised to see a strong employment number."

Economists surveyed by CNNMoney are expecting the economy to have added 125,000 jobs in October, up from 114,000 the prior month. They're also expecting the unemployment rate to tick up to 7.9%, from 7.8% in September.

Related: Knight Capital back in business

Meanwhile, U.S. manufacturing activity continued to rebound in October, and the Conference Board's consumer confidence index rose to the highest level since February 2008. Construction spending increased in September by the most in three months, though the jump was slightly less than analysts were looking for.

Fear & Greed Index

Companies: The corporate world was also busy Thursday. Better-than-expected earnings sent shares of Exxon Mobil (XOM, Fortune 500) slightly higher.

Netflix (NFLX) shares retreated after a massive 14% runup Wednesday. The previous day's gains came after famed corporate raider Carl Icahn disclosed he bought a 10% stake in Netflix, and strongly hinted he'd like a larger company to buy the streaming video and DVD service.

Japan-based Panasonic (PC) released an earnings report Thursday that was full of bad news. The electronics company posted a loss, dramatically lowered its forecast for the year, and announced it will suspend its dividend. Business conditions are expected to become "much more severe." Shares of the company declined.

Also in Japan, Sony (SNE) reported a narrower loss for its fiscal second quarter and reaffirmed its full-year forecast for a swing to profit. Its U.S.-traded gained ground.

Shares of Ford (F, Fortune 500) rose after the company announced that Alan Mulally would remain president and CEO through at least 2014, and named Mark Fields as chief operating officer.

Shares of Visa (V, Fortune 500) gained after its Wednesday earnings report topped analysts' estimates. Sirius (SIRI) also gained after the satellite radio company reported its new subscriber sign-ups were strong last quarter.

Pfizer (PFE, Fortune 500) slipped after it reported quarterly revenue that fell far below analysts' estimates.

GM (GM, Fortune 500) said its U.S. sales jumped 5% in October to the highest levels since 2007.

After the closing bell, AIG (AIG, Fortune 500), Starbucks (SBUX, Fortune 500) and LinkedIn (LNKD) reported results.

Shares of Starbucks spiked in after-hours trading after the coffee chain hiked its dividend as it beat its profit and revenue forecast.

AIG also topped expectations, but shares of the insurance giant slipped in after-hours trading.

LinkedIn's stock bounced in after-hours trading after the company topped Wall Street's expectations.

World Markets: European stocks closed sharply higher. Britain's FTSE 100 rose 1.3%, the DAX in Germany increased 1% and France's CAC 40 added 1.4%.

Asian markets closed higher. The Shanghai Composite had the strongest gains, up 1.7%, while the Hang Seng in Hong Kong jumped 0.8%, and Japan's Nikkei rose 0.2%.

China's government reported earlier in the day that its official purchasing manager's index jumped to 50.2 in October, from 49.8 the previous month. Any reading above 50 indicates that factory conditions are improving in the manufacturing sector.

Currencies and commodities: The dollar rose versus the euro, the British pound and the Japanese yen.

Oil for December delivery added 85 cents to settle at $87.09 a barrel.

Gold futures for December delivery fell $3.60 to settle at $1,715.50 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury edged lower, pushing the yield up to 1.72% from 1.69% late Wednesday.

Market Update

Market Update 4:15 pm : Stocks began the day with a bullish sentiment as the three major averages spent the first 90 minutes on a steady upward climb. After reaching session highs, the S&P 500 leveled off and held its gains into the afternoon before ending with a gain of 1.1%.

The technology sector was one of the top performers, and the SPDR Technology Select Sector ETF (XLK 29.34, +0.46) settled higher by 1.6%. However, the biggest tech component, Apple (AAPL 596.53, +1.21), underperformed with a gain of just 0.2%.

In notable tech earnings, Visa (V 143.88, +5.12) advanced 3.7% after beating on the top and bottom lines. The payment processor earned $1.54, which was $0.04 better than the Capital IQ consensus estimate. Visa's revenue of $2.73 billion represents a 14.6% year-over-year increase, and was reported ahead of expectations. In addition, the company announced a new $1.5 billion repurchase program.

Elsewhere, JDA Software (JDAS 44.76, +6.61) surged 17.3% after announcing plans to merge with RedPrairie. Per the agreement, JDA stockholders will receive $45 per share, which represents a 33.0% premium to JDA's closing price on October 26. This was the day before speculation regarding a sale started circulating. In addition, JDA reported third quarter earnings of $0.53 on $164.5 million in revenue. The earnings may not be comparable to the Capital IQ analyst estimate of $0.54, while the company's revenue fell short of expectations.

In other M&A news, auto parts manufacturer, Williams Controls (WMCO 15.36, +4.45), soared 40.8% after agreeing to be acquired by Curtis-Wright (CW 31.50, +0.63). Per the agreement, Williams Controls stockholders will receive $15.42 per share, which represents a 41.3% premium to WMCO's Wednesday closing price.

Also of note, Advance Auto Parts (AAP 81.00, +10.06) spiked 14.2% after CNBC reported the company has hired Blackstone to explore a sale. The total price tag may be over $6 billion, which would equate to about $82 per share. Peers Autozone (AZO 380.34, +5.34), O'Reilly Automotive (ORLY 88.05, +2.20), and Pep Boys (PBY 10.47, +0.48) all moved higher on the news.

As the new month begins, retailers are reporting their October same store sales. Out of the eighteen companies which already reported, twelve beat consensus estimates while six missed. However, half of the names which missed reported upside third quarter guidance.

Among the names which exceeded expectations, Bon-Ton Stores (BONT 13.49, +1.23) led the group higher with a gain of 10.0%. Meanwhile, Costco (COST 97.13, -1.30) and Stein Mart (SMRT 7.52, -0.34) saw respective losses of 1.3% and 4.3% despite reporting sales ahead of expectations.

On the downside, Zumies (ZUMZ 21.13, -4.19) slid 16.6% after reporting a 0.6% increase in same store sales. The reading was a disappointment as the Retail Metrics consensus expected the company to post a 4.4% increase. The company pointed to Europe as the reason for anemic growth, and issued downside guidance. Following the news, Piper Jaffray downgraded the stock to ‘underweight' from ‘neutral.'

Looking at automakers which reported their sales, Ford Motor (F 11.25, +0.09) gained 0.8% after reporting October sales of 168,456 vehicles. The figure represents a 0.4% year-over-year growth.

Toyota Motor (TM 78.05, +0.58) added 0.8% after reporting monthly sales of 155,242, which is a 15.8% increase on a daily selling rate basis and on an unadjusted raw volume basis. Also of note, a story out of Reuters indicated the company's October sales in China fell by 44.0%.

Honda Motor (HMC 30.35, +0.19) advanced 0.6% after its October sales increased by 8.8% year-over-year, to 106,973 units.

A number of economic data points came through today and most figures were largely in-line with expectations. The October Challenger Job Cuts report showed a 12.0% year-over-year increase. This follows the prior reading which indicated a 70.8% decline.

According to today's ADP National Employment Report, employment in the nonfarm private business sector rose by 158K in October. This was above the 143K increase expected by Briefing.com consensus.

The latest weekly initial jobless claims count totaled 363,000, which was lower than the 375,000 that had been expected by the Briefing.com consensus. The tally was below the revised prior week count of 372,000. As for continuing claims, they rose to 3.263 million from 3.254 million.

The consumer confidence reading for October came in at 72.2 while economists polled by Briefing.com expected a reading of 72.0. This follows prior month's 70.3 print.

The October ISM Index came in better-than-expected at 51.7 versus the 51.0 Briefing.com consensus, and up from September's reading of 51.5. Meanwhile, September construction spending rose by 0.6% month-over-month, against the expected increase of 0.8%.

Lastly, third quarter unit labor costs decreased by 0.1% which was lower than the 1.4% rise that had been widely anticipated. During the same period, productivity increased by 1.9%, according to the preliminary reading. An increase of 1.6% had been broadly forecast.

Tomorrow's economic data will focus on jobs as October nonfarm payrolls, nonfarm private payrolls, the unemployment rate, hourly earnings, and average workweek will all be announced at 8:30 ET. In addition, September factory orders will be reported at 10:00 ET.DJ30 +136.16 NASDAQ +42.83 SP500 +15.43 NASDAQ Adv/Vol/Dec 1611/1.81 bln/855 NYSE Adv/Vol/Dec 2343/797.5 mln/705

3:30 pm : A rebound by the dollar index following encouraging ADP and Initial Claims numbers put pressure on precious metals during today's pit trade. Both gold and silver retreated from their respective session highs of $1726.00 per ounce and $32.63 per ounce set in early morning action and trended lower for most of their sessions.

Gold eventually slipped into negative territory and settled 0.2% lower at $1715.50 per ounce. Silver also broke below the breakeven level and closed with a 0.2% loss at $32.26 per ounce.

Crude oil popped to its pit session high of $87.42 per barrel following bullish inventory data that showed a draw of 2.05 mln barrels when a build of 1.8 mln barrels was anticipated. The energy component then traded in a consolidative pattern just below that level despite a rebound by the dollar index. Crude eventually closed with a 1.0% gain at $87.06 per barrel.

Natural gas dipped to a floor session low of $3.65 per MMBtu moments after inventory data showed a build of 65 bcf when a build of 67 bcf was widely expected. It chopped around between positive and negative territory for the remainder of pit trade and settled at $3.70 per MMBtu, or 0.3% higher.DJ30 +117.46 NASDAQ +40.79 SP500 +14.03 NASDAQ Adv/Vol/Dec 1530/1462.5 mln/899 NYSE Adv/Vol/Dec 2293/498 mln/736

3:05 pm : The S&P 500 has returned near its session high as it trades up 1.1%.

Advance Auto Parts (AAP 81.00, +10.06) is surging 14.2% after CNBC reported that the company has hired Blackstone to explore a sale. The total price tag may be over $6 billion, which would equate to about $82 per share. Peers Autozone (AZO 381.33, +6.33), O'Reilly Automotive (ORLY 89.06, +3.21), and Pep Boys (PBY 10.50, +0.51) all moved higher on the news.DJ30 +133.41 NASDAQ +42.18 SP500 +14.98 NASDAQ Adv/Vol/Dec 1518/1.34 bln/918 NYSE Adv/Vol/Dec 2288/458.9 mln/732

2:30 pm : The major averages are maintaining their afternoon levels and the S&P 500 is higher by 1.0%.

Looking at automakers which reported their sales, Ford Motor (F 11.10, -0.06) is slipping 0.5% after reporting October sales of 168,456 vehicles. The figure represents a 0.4% year-over-year growth.

Toyota Motor (TM 77.96, +0.49) is adding 0.6% after reporting monthly sales of 155,242, which is a 15.8% increase on a daily selling rate basis and on an unadjusted raw volume basis. Also of note, a story out of Reuters indicated the company's October sales in China fell by 44.0%.

Honda Motor (HMC 30.36, +0.20) is advancing 0.7% after its October sales increased by 8.8% year-over-year, to 106,973 units.DJ30 +12.92 NASDAQ +38.47 SP500 +13.10 NASDAQ Adv/Vol/Dec 1421/1.23 bln/993 NYSE Adv/Vol/Dec 2221/415.4 mln/782

2:00 pm : The major averages are holding their recent levels and the S&P 500 is higher by 0.9%.

Treasuries have seen some afternoon buying as the major averages slip off their best levels. The complex has trimmed its losses with shorter dated maturities ticking back up to their respective flat lines. However, longer dated paper remains firmly entrenched in negative territory with the 30-yr bond off 28/32 at 97 00/32. A more modest decline of 8/32 has the 10-yr yield up more than 3 basis points from yesterday's cash close, and has the yield back above its 50-day moving average. More importantly, the trend line off the July lows remains intact, an indication Treasury bulls remain in control for the time being. Some flattening has taken hold along the yield curve as the 2-10-yr spread trades at 142 basis points.

Elsewhere, precious metals have slumped into negative territory with gold down $3 at $1716 and silver off $0.05 near $32.25.DJ30 +117.54 NASDAQ +36.54 SP500 +12.38 NASDAQ Adv/Vol/Dec 1383/1.14 bln/1024 NYSE Adv/Vol/Dec 2188/377.9 mln/804

1:30 pm : The Dow has retreated off its session highs, but it remains firmly in the black. The industrial average is currently adding 0.9%.

The Dow Jones Transportation Average is higher by 1.2% as it outperforms the remaining industrials. Railroads are seeing strength as Kansas City Southern (KSU 82.51, +2.05) and Norfolk Southern (NSC 62.31, +0.96) are rising by 2.6% and 1.6%, respectively.

On the downside, Con-way (CNW 27.40, -1.71) is sliding 5.9% after the company missed on the top and bottom lines. In addition, the management said it expects the fourth quarter to be challenging as well.DJ30 +111.08 NASDAQ +34.81 SP500 +12.39 NASDAQ Adv/Vol/Dec 1361/1.05 bln/1025 NYSE Adv/Vol/Dec 2200/348.3 mln/783

1:00 pm : The major averages began the session on a positive note, and continued building on their gains through the morning. After reaching session highs 90 minutes into the day, the key indices are holding their gains. At midday, the S&P 500 is up 0.9%.

The technology sector is the top performer, and the SPDR Technology Select Sector ETF (XLK 29.32, +0.44) is higher by 1.6%. However, the biggest tech component, Apple (AAPL 598.28, +2.96), is underperforming with a gain of just 0.5%.

Looking at technology earnings, Visa (V 143.71, +4.95) is higher by 3.6% after beating on the top and bottom lines. The payment processor earned $1.54, which was $0.04 better than the Capital IQ consensus estimate. Visa's revenue of $2.73 billion represents a 14.6% year-over-year increase, and was reported ahead of expectations. In addition, the company announced a new $1.5 billion repurchase program. Rival Mastercard (MA 472.72, +11.79) is rising by 2.6% after the company's earnings of $6.17 exceeded the Capital IQ consensus estimate by $0.24. Meanwhile, Mastercard's revenue of $1.92 billion was in-line with expectations.

Elsewhere, JDA Software (JDAS 44.78, +6.63) is surging 17.4% after announcing plans to merge with RedPrairie. Per the agreement, JDA stockholders will receive $45 per share, which represents a 33.0% premium to JDA's closing price on October 26. This was the day before speculation regarding a sale started circulating. In addition, JDA reported third quarter earnings of $0.53 on $164.5 million in revenue. The earnings may not be comparable to the Capital IQ analyst estimate of $0.54, while the company's revenue fell short of expectations.

In other M&A news, auto parts manufacturer, Williams Controls (WMCO 15.39, +4.48), is soaring 41.1% after agreeing to be acquired by Curtis-Wright (CW 31.45, +0.58). Per the agreement, Williams Controls stockholders will receive $15.42 per share, which represents a 41.3% premium to WMCO's Wednesday closing price.

As the new month begins, retailers are reporting their October same store sales. Out of the eighteen companies which already reported, twelve beat consensus estimates while six missed. However, half of the names which missed reported upside third quarter guidance.

Among the names which exceeded expectations, Bon-Ton Stores (BONT 12.91, +0.65) leads the group higher with a gain of 5.3%. Meanwhile, Costco (COST 98.05, -0.38) and Stein Mart (SMRT 7.70, -0.16) are seeing respective losses of 0.4% and 2.0% despite reporting sales ahead of expectations.

On the downside, Zumies (ZUMZ 21.14, -4.18) is sliding 16.5% after reporting a 0.6% increase in same store sales. The reading was a disappointment as the Retail Metrics consensus expected the company to post a 4.4% increase. The company pointed to Europe as the reason for anemic growth and issued downside guidance. Following the news, Piper Jaffray downgraded the stock to ‘underweight' from ‘neutral.'

The October Challenger Job Cuts report showed a 12.0% year-over-year increase. This follows the prior reading which indicated a 70.8% decline.

According to today's ADP National Employment Report, employment in the nonfarm private business sector rose by 158K in October. This was above the 143K increase expected by Briefing.com consensus.

Elsewhere, the latest weekly initial jobless claims count totaled 363,000, which was lower than the 375,000 that had been expected by the Briefing.com consensus. The tally was below the revised prior week count of 372,000. As for continuing claims, they rose to 3.263 million from 3.254 million.

Lastly, third quarter unit labor costs decreased by 0.1% which was lower than the 1.4% rise that had been widely anticipated. During the same period, productivity increased by 1.9%, according to the preliminary reading. An increase of 1.6% had been broadly forecast.

The latest consumer confidence reading for October came in at 72.2 while economists polled by Briefing.com expected a reading of 72.0. This follows prior month's 70.3 print.

The October ISM Index came in better-than-expected at 51.7 versus the 51.0 Briefing.com consensus, and up from September's reading of 51.5. Meanwhile, September construction spending rose by 0.6% month-over-month, against the expected increase of 0.8%.DJ30 +116.88 NASDAQ +36.03 SP500 +12.48 NASDAQ Adv/Vol/Dec 1404/982.2 mln/977 NYSE Adv/Vol/Dec 2196/322.5 mln/770

12:30 pm : The major averages continue to hover near their respective highs and the S&P 500 is up 1.1%.

A handful of footwear manufacturers are seeing strength following upbeat earnings. K-Swiss (KSWS 3.01, +0.73) is surging 32.0% after beating on earnings and revenues. During the third quarter, the company recorded a loss of $0.05, which was $0.08 better than the Capital IQ consensus estimate. Meanwhile, the company's revenue of $67.6 million was ahead of the $63.03 million expected by the consensus. In addition, the company issued upside guidance as it expects its full-year revenue to come in ahead of expectations.

Meanwhile, Steve Madden (SHOO 45.50, +2.58) is rising by 6.0% after the company beat on the bottom line and reported revenues in-line with analyst expectations. The company also raised its full-year earnings guidance ahead of analyst estimates. Note that today's buying has lifted the stock to its all-time best.

Other footwear stocks are also garnering interest. Deckers Outdoor (DECK 29.94, +1.31) and Crocs (CROX 12.79, +0.19) are seeing respective gains of 4.5% and 1.5%.DJ30 +147.59 NASDAQ +42.24 SP500 +15.16 NASDAQ Adv/Vol/Dec 1493/892.6 mln/858 NYSE Adv/Vol/Dec 2259/291.8 mln/687

12:00 pm : The key indices are holding their recent levels and the Nasdaq is higher by 1.5%.

The technology sector is the top performer of the day and the SPDR Technology Select Sector ETF (XLK 29.34, +0.46) is higher by 1.6%.

The biggest tech component, Apple (AAPL 600.00, +4.68) is advancing 0.8% as it underperforms the sector.

Looking at technology earnings, Visa (V 143.71, +4.95) is higher by 3.6% after beating on the top and the bottom line. The payment processor earned $1.54, which was $0.04 better than the Capital IQ consensus estimate. Visa's revenue of $2.73 billion represents a 14.6% year-over-year increase, and was reported ahead of expectations. In addition, the company announced a new $1.5 billion repurchase program.

Mastercard (MA 473.85, +12.92) is rising by 2.8% after the company's earnings of $6.17 exceeded the Capital IQ consensus estimate by $0.24. Meanwhile, Mastercard's revenue of $1.92 billion was in-line with expectations.

Elsewhere, JDA Software (JDAS 44.78, +6.63) is surging 17.4% after announcing plans to merge with RedPrairie. Per the agreement, JDA stockholders will receive $45 per share, which represents a 33.0% premium to JDA's closing price on October 26. This was the day before speculation regarding a sale started circulating. In addition, JDA reported third quarter earnings of $0.53 on $164.5 million in revenue. The earnings may not be comparable to the Capital IQ analyst estimate of $0.54, while the company's revenue fell short of expectations.DJ30 +143.76 NASDAQ +43.92 SP500 +15.33 NASDAQ Adv/Vol/Dec 1555/803.8 mln/789 NYSE Adv/Vol/Dec 2278/261.8 mln/659

11:30 am : The major averages continue to trade near their respective highs and the S&P 500 is rising by 1.0%.

As the new month begins, retailers are reporting their October same store sales. Out of the eighteen companies which already reported, twelve beat consensus estimates while six missed. However, half of the names which missed reported upside third quarter guidance.

Among the names which exceeded expectations, Bon-Ton Stores (BONT 12.90, +0.64) is higher by 5.2%. Meanwhile, Costco (COST 98.08, -0.35) and Stein Mart (SMRT 7.70, -0.16) are seeing respective losses of 0.4% and 2.0% despite reporting sales ahead of expectations.

On the downside, Zumies (ZUMZ 21.95, -3.36) is sliding 13.3% after reporting a 0.6% increase in same store sales. The reading was a disappointment as the Retail Metrics consensus expected the company to post a 4.4% increase. The company pointed to Europe as the reason for anemic growth and issued downside guidance. Following the news, Piper Jaffray downgraded the stock to ‘underweight' from ‘neutral.'DJ30 +142.14 NASDAQ +37.93 SP500 +13.48 NASDAQ Adv/Vol/Dec 1541/685.1 mln/774 NYSE Adv/Vol/Dec 2269/227.2 mln/647

11:05 am : The major averages are rising steadily and the S&P 500 is higher by 1.0%. Meanwhile, Nasdaq is rising by 1.4% as it outperforms the other indices.

The industrial sector is one of the top performers, and providers of building products are leading the space despite reporting mixed earnings. The strength is likely resulting from expectations of an increase in demand for building supplies as the East coast recovers from Hurricane Sandy.

Masco (MAS 16.01, +0.92) is spiking 6.2% after reporting earnings of $0.13, which may not be comparable with the Capital IQ consensus estimate of $0.12. Meanwhile, the company's revenue of $1.98 billion was below the $2.02 billion expected by analysts.

Lennox International (LII 51.67, +1.62) is advancing 3.0% after reporting mixed results. However, the company raised its full-year 2012 earnings and revenue guidance above consensus.

Industrial conglomerates are also garnering interest. Standex International (SXI 50.74, +4.50) is spiking 9.7% after the company's earnings of $0.92 fell short of the $0.97 expected by the Capital IQ consensus. Standex' top line was a positive as its revenue of $183.4 exceeded estimates. In addition, SXI raised its quarterly cash dividend by 14.3%, to $0.08 from $0.07.DJ30 +147.30 NASDAQ +40.30 SP500 +13.44 NASDAQ Adv/Vol/Dec 1541/572.5 mln/746 NYSE Adv/Vol/Dec 2280/193.2 mln/614

10:35 am : Commodities are volatile this morning with energy and metals mixed. The dollar index has been trending lower since the overnight session, which has helped crude oil and copper futures. Meanwhile, gold and silver have been on a downtrend as well despite the weakness in the dollar index.

Natural gas futures has been on a downtrend since hitting its current session high of $3.74/MMBtu. Ahead of inventory data, Dec nat gas was down 0.7% at $3.67/MMBtu. Following the data, which showed a small-than-expected- build (65 bcf vs 67 bcf expected), nat gas spiked into positive territory and is now +0.3% at $3.70/MMBtu.

Dec crude oil just rallied from just above the $86 area, pushing back to its current HoD. In current action, crude is +0.2% at $86.40/barrel.

Dec gold and Dec silver have both erased all of their losses and are now near the unchanged mark. More specifically, Dec gold is +0.01% at $1719.20/oz and Dec silver is +0.2% at $32.40/oz. Dec copper is +1.2% at $3.56/lb.DJ30 +137.48 NASDAQ +34.60 SP500 +12.44 NASDAQ Adv/Vol/Dec 1553/415.6 mln/677 NYSE Adv/Vol/Dec 2265/146 mln/573

10:05 am : The major averages have pushed to fresh highs and the S&P 500 is advancing 0.8%.

The latest consumer confidence reading for October came in at 72.2 while economists polled by Briefing.com expected a reading of 72.0. This follows prior month's 70.3 print.

October ISM Index came in better-than-expected at 51.7 versus the 51.0 Briefing.com consensus, and up from September's reading of 51.5. Meanwhile, September construction spending rose by 0.6% month-over-month, against the expected increase of 0.8%.DJ30 +144.62 NASDAQ +28.57 SP500 +11.84 NASDAQ Adv/Vol/Dec 1467/253.4 mln/669 NYSE Adv/Vol/Dec 2168/99.9 mln/608

09:45 am : Equities have extended their bullish pre-market sentiment as all three indices are near their respective highs. The S&P 500 is rising by 0.3%.

Auto parts manufacturer Williams Controls (WMCO 15.38, +4.47) is soaring 41.0% after agreeing to be acquired by Curtis-Wright (CW 31.04, +0.17). Per the agreement, Williams Controls stockholders will receive $15.42 per share, which represents a 41.3% premium to WMCO's Wednesday closing price.

October ISM Index, September construction spending, and October consumer confidence will all be reported at 10:00 ET.DJ30 +72.24 NASDAQ +13.90 SP500 +4.98 NASDAQ Adv/Vol/Dec 1283/146.5 mln/768 NYSE Adv/Vol/Dec 1932/66.2 mln/782

09:01 am : [BRIEFING.COM] S&P futures vs fair value: +1.40. Nasdaq futures vs fair value: +9.00. U.S. equity futures are near their pre-market highs and the S&P 500 futures are adding 0.1%.

The major Asian bourses ended the day mixed as some saw a boost from China's PMI data. China's Manufacturing PMI ticked up to 50.2 (50.3 expected, 49.8 previous), to post its first expansionary number in three months while the HSBC Final Manufacturing PMI rose to 49.5 (49.1 previous, 49.1 expected), but remained in contraction. The data has many believing this is a sign the Chinese economy has bottomed; however, it is still much too early to make that claim. Hong Kong's Monetary Authority intervened for a second straight day to maintain its HK$7.75 peg per dollar. Data across the region was heavy with Australia's import prices posting a 2.4% quarter-over-quarter decline (-1.2% expected), South Korea's trade surplus expanding to $3.8 billion ($3.42 billion expected, $3.1 billion previous) and its CPI ticking up to 2.1% year-over-year (2.2% expected, 2.0% previous).

In Japan, the Nikkei added 0.2%, and was buoyed by the Chinese data and weaker yen. Construction names advanced on the Chinese data as Komatsu and Hitachi Construction jumped 3.1% and 4.4% respectively. Meanwhile, shares of Panasonic tumbled 19.5% after announcing it expects to post a full year loss of JPY765 billion. This comes following a July projection of a JPY50 billion profit.

Hong Kong's Hang Seng finished higher by 0.8% as real estate and shipping stocks led the way. New World Holdings climbed 0.8% and China Shipping Container Lines surged 8.2% to provide some leadership in their respective sectors.

China's Shanghai Composite advanced 1.7% as financials and real estate names provided leadership. China Construction Bank rallied 1.5% as financials saw gains. Elsewhere, real estate firms were firm on reports Beijing may ease restrictions on real estate transactions. Poly Real Estate led the space with a 4.4% gain.

European indices are also seeing gains. Notable economic data in the region was light as UK's Manufacturing PMI was reported at 47.5, which fell short of the expected reading of 48.1. In addition, the country's nationwide housing price index showed a better-than-expected increase of 0.6%. According to reports, a buyback program is the most likely outcome of the Greek debt conundrum. However, haircuts for private bondholders are currently being ruled out.

In the United Kingdom, the FTSE is higher by 0.6% and a handful of stocks are seeing notable gains. Lloyds Banking Group is surging 6.3% after the financial reported a smaller loss than what analysts expected. Elsewhere, British Sky Broadcasting Group gained 5.4% after reporting better-than-expected earnings.

France's CAC is rising by 0.7% and consumer stocks are outperforming. Carrefour and Sanofi are seeing respective gains of 1.7% and 1.9%. On the downside, industrials are seeing weakness. Safran is slipping 0.3% and Vallourec is off by 1.3%.

Germany's DAX is advancing 0.8% and carmakers are leading the way. BMW, Daimler, and Volkswagen are all up between 1.0% and 2.5%. Consumer stocks are among the decliners as Fresenius SE and Fresenius Medical are down 1.8% and 2.2%, respectively.

08:35 am : [BRIEFING.COM] S&P futures vs fair value: +0.40. Nasdaq futures vs fair value: +8.00. Equity futures have shown little reaction to the release of a number of economic data points. The S&P 500 futures are currently flat.

According to today's ADP National Employment Report, employment in the nonfarm private business sector rose by 158K in October. This was above the 143K increase expected by Briefing.com consensus.

Elsewhere, the latest weekly initial jobless claims count totaled 363,000, which is lower than the 375,000 that had been expected by the Briefing.com consensus. The tally is below the revised prior week count of 372,000. As for continuing claims, they rose to 3.263 million from 3.254 million.

Lastly, third quarter unit labor costs decreased by 0.1% which is lower than the 1.4% rise that had been widely anticipated. During the same period, productivity increased by 1.9%, according to the preliminary reading. An increase of 1.6% had been broadly forecast.

08:00 am : S&P futures vs fair value: -0.20. Nasdaq futures vs fair value: +5.80. U.S. equity futures are modestly higher amid upbeat overseas trade.

Overnight, the global equity markets continued climbing, and China's Shanghai Composite outperformed with a 1.7% gain. The advance followed the country's Manufacturing PMI reading which improved to 50.20 from the previous level of 49.80. Meanwhile, Chinese press reported People's Bank of China injected a record CNY379 billion into its money markets during the past week. Elsewhere, Hong Kong's Hang Seng advanced 0.8% while Japan's Nikkei managed to add 0.2% despite being pressured by disappointing quarterly reports.

European bourses are also seeing gains. Economic data in the region was light as UK's Manufacturing PMI was reported at 47.5, which fell short of the expected reading of 48.1. In addition, the country's nationwide housing price index showed a better-than-expected increase of 0.6%. According to reports, a buyback program is the most likely outcome of the Greek debt conundrum. However, haircuts for private bondholders are currently being ruled out. Otherwise, earnings out of Europe are painting a mixed picture as Shell posted better than expected results, while Lloyd's Banking Group reported an unexpected loss. Looking at the region's key indices, France's CAC, Germany's DAX, and UK's FTSE are all higher by 0.6%.

In U.S. corporate news, Visa (V 143.33, +4.57) is higher by 3.0% after beating on the top and the bottom line. The payment processor earned $1.54, which was $0.04 better than the Capital IQ consensus estimate. Visa's revenue of $2.73 billion represents a 14.6% year-over-year increase, and was reported ahead of expectations. In addition, the company announced a new $1.5 billion repurchase program.

Pfizer (PFE 24.50, -0.37) is shedding 1.5% after reporting disappointing earnings. The drug maker's earnings of $0.53 were $0.01 ahead of the Capital IQ consensus estimate. However, the company's revenue declined 15.9% year-over-year to $13.98 billion, and the figure was below analyst expectations. In addition, Pfizer narrowed its full-year 2012 earnings and revenue guidance below consensus.

Cirrus Logic (CRUS 42.50, +1.72) is adding 4.2% after Needham upgraded the stock to ‘strong buy' from ‘buy' with a $57 price target.

Zumies (ZUMZ 21.95, -3.37) is sliding 13.3% after reporting a 0.6% increase in same store sales. The reading was a disappointment as the Retail Metrics consensus expected the company to post a 4.4% increase. The company pointed to Europe as the reason for anemic growth and issued downside guidance. Following the news, Piper Jaffray downgraded the stock to ‘underweight' from ‘neutral.'

The October Challenger Job Cuts report showed a 12.0% year-over-year increase. This follows the prior reading which indicated a 70.8% decline.

Market participants will receive a full slate of economic data as October ADP Employment Change Survey will be released at 8:15 ET. Weekly initial and continuing claims, third quarter unit labor costs and preliminary productivity will all be released at 8:30 ET. In addition, the ISM Index, construction spending, and consumer confidence will all hit the wires at 10:00 ET. Lastly, automakers will be reporting their sales throughout the day while retailers will report their same store sales.

06:29 am : [BRIEFING.COM] S&P futures vs fair value: -2.50. Nasdaq futures vs fair value: +2.00.

06:29 am : Nikkei...8946.87...+18.60...+0.20%. Hang Seng...21821.87...+180.10...+0.80%.

06:29 am : FTSE...5791.93...+9.20...+0.20%. DAX...7271.16...+10.50...+0.20%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage