Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

113012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+970.00.png [ 75.32 KiB | Viewed 486 times ]

113012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+970.00.png [ 75.32 KiB | Viewed 486 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$770.00 dollars or +7.70 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$200.00 dollars or +0.20 points.

Total Profit @ $970.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

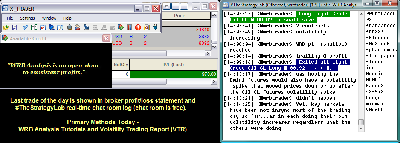

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with

price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1380 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

U.S. Market Wrap Nov. 30 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. U.S. stocks erased losses in the final 15 minutes, sending the Standard & Poor’s 500 Index to a second weekly gain, as investors bought shares before changes to MSCI Inc. indexes and weighed developments in budget talks.

Attachment:

113012-Key-Price-Action-Markets.png [ 544.13 KiB | Viewed 477 times ]

113012-Key-Price-Action-Markets.png [ 544.13 KiB | Viewed 477 times ]

Market Update

Market Update 4:15 pm : Equities were on uncertain footing during the first hour of the session. The S&P 500 followed the early indecision by sliding to its lows just above the 1410 level. A familiar theme played out intraday as President Obama and House Speaker Boehner held another round of press conferences. The President reiterated the importance of reaching compromise and expressed hope that enough Republicans can be convinced to break rank and vote in favor of his budget proposal. Meanwhile, House Speaker Boehner maintained his prior stance and said that Republicans are willing to compromise if Democratic lawmakers agree to spending cuts. Until then, the two sides remain at a stalemate. The benchmark average spent the majority of the session in the red, but a buying surge shortly before day's end lifted the index to flat close.

Financials saw relative weakness as the budget debate remains in focus. Citigroup (C 34.57, -0.64) lost 1.8% and was the weakest performer among the majors.

Though U.S. financials underperformed, their European counterparts advanced. Barclays (BCS 15.83, +0.17) and UBS (UBS 15.70, +0.11) added 1.1% and 0.7%, respectively. Earlier, Reuters reported Barclays may cut as many as 3500 investment bank positions and reduce the scope of its Asian operations.

Tech stocks lagged the broader market and large cap names saw weakness. Apple (AAPL 585.28, -4.08), International Business Machines (IBM 190.07, -1.46), and Microsoft (MSFT 26.61, -0.33) all lost between 0.7% and 1.2%.

Elsewhere, VeriSign (VRSN 34.15, -5.19) slid 13.2% after its updated agreement with the Department of Commerce limited the company's ability to increase domain registration prices.

Also of note, Groupon (GRPN 4.14, -0.40) fell 8.8% after company spokesman said Chief Executive Officer Andrew Mason will not be replaced in the near term.

Consumer discretionary stocks saw weakness and carmakers weighed on the sector. Earlier, Ford Motor (F 11.45, -0.08) said it plans to increase its electric car market share to 11.0%, from the current 5.2%. Despite the news, shares of Ford finished lower by 0.7%. Looking at other automakers, Honda Motor (HMC 33.29, -0.30), Toyota Motor (TM 86.08, -0.43), and Thor (THO 37.74, -0.21) all lost between 0.5% and 1.0%.

Restaurant operator Yum! Brands (YUM 67.08, -7.39) also weighed on the discretionary space. The restaurant operator slid 9.9% after issuing full-year 2013 guidance and reaffirming its full-year 2012 earnings growth forecast of at least 13%. The guidance proved to be a point of concern as sales in China are expected to continue tracking lower. Following the update, Raymond James, Susquehanna, and UBS all downgraded the stock.

On the upside, teen retailer Five Below (FIVE 37.15, +5.76) soared 18.4% after beating on earnings and revenue. In addition, the company issued downside fourth quarter earnings guidance while revenue is expected to come in above consensus estimates.

The utilities sector was the top performer and the SPDR Utilities Select Sector ETF (XLU 35.32, +0.37) settled higher by 1.1%. Within the space, electric utilities paced the advance. Duke Energy (DUK 63.82, +1.43) gained 2.3% after reaching settlement with the North Carolina Utilities Commission. The settlement aims to resolve issues following the merger of Duke Energy and Progress Energy. In addition, the company President, Chairman, and Chief Executive Officer Jim Rogers announced his intention to retire by the end of next year. Looking at other utility stocks, Northeast Utilities (NU 38.74, +0.58) and IDACORP (IDA 42.71, +0.47) both advanced near 1.3%.

In economic news, the November Chicago PMI reading of 50.4 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.7 to follow the prior month's 49.9.

Personal income was unchanged in October, which was below the 0.2% increase expected by the Briefing.com consensus. Personal spending decreased by 0.2%, which was below the expected 0.1% uptick. Core personal consumption expenditures were higher by 0.1%, which fell short of the broadly expected reading of 0.2%.

Monday's economic data will include the November ISM Index as well as October construction spending. The two reports will be released at 10:00 ET. In addition, automakers will report their sales throughout the day.

Week in Review: Equities Eke Out Gains amid Fiscal Cliff Debate

On Monday, equities began the week on a cautious note as uncertainty crept back into the markets. Overseas, the Eurogroup continued to discuss the next tranche of Greek aid. Reports from the talks indicated lawmakers remained split over whether or not haircuts should be applied to the outstanding Greek debt. Additionally, elections in the Spanish region of Catalonia resulted in two-thirds of the vote going to parties which support a referendum on independence. The European news combined with some profit-taking following Friday's rally translated into a downbeat session which saw the S&P 500 slip 0.2%. Retailers succumbed to the broad market pressure, and the SPDR S&P 500 Retail ETF (XRT 63.27, -0.09) slid 1.0%.

Tuesday's session began on a negative note, and the indices finished on their lows. Overnight reports from Europe indicated the International Monetary Fund and the Eurozone finance ministers agreed on the terms of the next installment of Greek aid. As part of the agreement, the country's debt-to-GDP ratio is expected to decline from 190% in 2014 to 124% in 2020. The news did little to inspire investor confidence as the markets doubted the sovereign's ability to reach the lofty goals. Instead, market participants remained focused on Washington where Senator Harry Reid said little progress has been made in budget negotiations. After the Senate majority leader's comments, the S&P 500 fell to session lows from its flat line. The index declined further when a final round of selling pressured it to a loss of 0.5%. Exelon (EXC 30.22, +0.26) gained 0.9% after ISI Group upgraded the stock to ‘buy' from ‘neutral.'

On Wednesday, equities opened lower, but staged a reversal when top lawmakers reiterated their desire to reach a budget agreement. After marking a session low near its 200-day moving average, the S&P 500 reversed 25 handles to session highs. The reversal was aided by comments from House Speaker Boehner who said he is optimistic a deal can be reached in order to avoid going over the fiscal cliff. In addition, the President held a press conference where he reiterated his belief in higher tax rates for top earners. He also stressed that if Congress fails to approve selective tax increases, going over the cliff will result in an across-the-board tax hike. The S&P 500 ended the session with a gain of 0.8%. Green Mountain Coffee Roasters (GMCR 36.67, +0.30) surged 27.3% after reporting strong earnings.

Thursday started on a positive note after Wednesday's comments from House Speaker Boehner were viewed as supportive. However, the Speaker held another press conference on Thursday at which he said no "substantive progress" has been made. The S&P 500 responded to Mr. Boehner's remarks by falling back to its flat line. The weakness did not last long, and the benchmark average was able to regain its losses to close higher by 0.4%. Kohl's (KSS 44.65, -0.37) sank 12.0% after its same store sales declined by 5.6% on expectations of a 2.1% increase.DJ30 +3.76 NASDAQ -1.79 SP500 +0.23 NASDAQ Adv/Vol/Dec 1219/1.98 bln/1230 NYSE Adv/Vol/Dec 1658/1.18 bln/1359

3:30 pm : Crude oil extended yesterday's gains as it lifted off its session low of $87.98 per barrel set right at pit trade open. The energy component touched a session high of $88.99 per barrel just before it settled at $88.94 per barrel. The advance was supported by a slightly weaker dollar index and brought crude's gain for the week to 0.7%.

Natural gas, on the other hand, fell for a third consecutive session. It tumbled from its session high of $3.68 per MMBtu and brushed a session low of $3.55 per MMBtu moments before it settled the week at $3.56 per MMBtu, or 11.7% below last Friday's closing price.

Precious metals fell deeper into negative territory in choppy fashion on weak November Chicago PMI data and more uncertainty over a "fiscal cliff" resolution. Gold fell off its session high of $1728.10 per ounce and brushed a session low of $1710.80 per ounce as it headed towards the pit close. Today's decline left gold to settle the week 2.3% lower at $1713.30 per ounce. Silver also slid off its session high of $34.31 per ounce and tumbled as low as $33.22 per ounce. It settled at $33.31 per ounce, bringing the weekly loss to 2.6%.DJ30 -13.27 NASDAQ -7.40 SP500 -1.90 NASDAQ Adv/Vol/Dec 1096/1386.8 mln/1336 NYSE Adv/Vol/Dec 1460/412 mln/1532

3:00 pm : The S&P 500 has returned to its session low as afternoon trade enters the final hour.

Major solar names have shown recent strength despite reporting mixed quarterly results. Earlier, ReneSola (SOL 1.27, +0.09) missed on earnings, but beat the Capital IQ revenue estimate. In addition, the company issued downside fourth quarter revenue guidance. Shares of SOL are higher by 7.6% in reaction to earnings.

Meanwhile, LDK Solar (LDK 1.16, -0.02) is slightly lower ahead of its earnings release scheduled for Monday morning.DJ30 -24.93 NASDAQ -7.91 SP500 -3.12 NASDAQ Adv/Vol/Dec 1060/1.23 bln/1356 NYSE Adv/Vol/Dec 1308/363.7 mln/1653

2:30 pm : The S&P 500 has erased the early weakness and the index now trades flat.

Coal stocks are attempting to halt their post-election slide and the Market Vectors Coal ETF (KOL 23.71, +0.11) is adding 0.5%. Among major coal producers, Walter Energy (WLT 30.68, +2.13) is surging 7.5% after the company was mentioned as a potential takeover target for BHP Billiton (BHP 72.22, 0.00).

Alpha Natural Resources (ANR 7.43, +0.25) and James River Coal (JRCC 3.81, +0.27) are seeing respective gains of 3.5% and 7.6% as they outperform their peers.DJ30 -1.54 NASDAQ -1.97 SP500 -0.33 NASDAQ Adv/Vol/Dec 1102/1.13 bln/1289 NYSE Adv/Vol/Dec 1445/332.9 mln/1507

2:00 pm : The S&P 500 is off by 0.1% as it continues to trade near its recent levels.

Two telecom stocks are headed in opposite directions in reaction to news. Tellabs (TLAB 3.43, +0.48) is surging 16.4% after the company declared a special dividend of $1.00. In addition, Tellabs' Board of Directors appointed Daniel P. Kelly as the new Chief Executive Officer and President.

Meanwhile, NTELOS Holdings (NTLS 12.24, -3.93) is tumbling 24.3% after FBR Capital downgraded the stock to ‘underperform' due to the adverse cash flow impact of the anticipated non-renewal of the SNA agreement.

Elsewhere in the space, Clearwire (CLWR 2.40, +0.19) is advancing 8.2% amid renewed takeover chatter.DJ30 -8.73 NASDAQ -4.84 SP500 -1.21 NASDAQ Adv/Vol/Dec 1026/1.03 bln/1379 NYSE Adv/Vol/Dec 1333/303.5 mln/1596

1:30 pm : The S&P 500 is off by 0.1% as it attempts to return into positive territory.

The Dow Jones Transportation Average is down 0.6% as it lags the broader market. The bellwether complex is showing broad weakness as only a handful of stocks buck the bearish sentiment. Airlines Alaska Air (ALK 42.62, +0.01), JetBlue Airways (JBLU 5.13, 0.00), and Southwest Airlines (LUV 9.50, 0.00) are showing little change as they outperform.

Meanwhile, trucking stocks are among the weakest transportation components. Con-way (CNW 28.20, -0.45) and JB Hunt (JBHT 59.17, -0.67) are down 1.6% and 1.1%, respectively.DJ30 -5.36 NASDAQ -5.42 SP500 -1.04 NASDAQ Adv/Vol/Dec 1008/948.9 mln/1360 NYSE Adv/Vol/Dec 1386/281.3 mln/1552

1:00 pm : Stocks showed indecision during the early part of the session. Familiar headlines continued to set the tone as Washington lawmakers held another round of press conferences. President Obama spoke from a factory is Pennsylvania, and expressed hope that enough Republicans can be convinced to break rank and vote in favor of his budget proposal. The President's speech was followed by the ongoing remarks from House Speaker Boehner. At midday, the S&P 500 is off by 0.2%.

Financials are seeing relative weakness as markets continue to react to updates from politicians regarding the budget debate. Citigroup (C 34.68, -0.53) is the weakest performer among the majors as it trades lower by 1.5%.

While U.S. financials underperform, their European counterparts are seeing gains. Deutsche Bank (DB 43.97, +0.10), Barclays (BCS 15.76, +0.10), and UBS (UBS 15.64, +0.05) are all up near 0.4%. Earlier, Reuters reported Barclays may cut as many as 3500 investment bank positions and reduce the scope of its Asian operations.

The consumer discretionary sector is the biggest laggard as carmakers weigh. Earlier, Ford Motor (F 11.38, -0.15) said it plans to increase its electric car market share to 11.0% from the current 5.2%. Despite the news, shares of Ford are lower by 1.3%. Looking at other automakers, Honda Motor (HMC 33.26, -0.33), Toyota Motor (TM 86.02, -0.49), and Thor (THO 37.42, -0.53) are all down between 0.6% and 1.5%.

Elsewhere in the space, high-end retailers are also underperforming. Coach (COH 57.39, -1.97) is down 3.3% and Ralph Lauren (RL 156.97, -3.43) is off by 2.1%.

Also of note, Yum! Brands (YUM 67.74, -6.74) is sliding 9.0% as it weighs on the discretionary space. Earlier, the company issued full-year 2013 guidance and reaffirmed its full-year 2012 earnings growth forecast of at least 13%. The guidance proved to be a point of concern as sales in China are expected to continue tracking lower. Following the update, Raymond James, Susquehanna, and UBS all downgraded the stock.

Utility stocks are among the top performers as the SPDR Utilities Select Sector ETF (XLU 35.07, +0.12) trades higher by 0.4%. Within the space, gas utilities are leading the advance. AGL Resources (GAS 38.93, +0.16) and WGL Holdings (WGL 38.89, +0.29) are both up near 0.6%.

Meanwhile, electric utilities are also seeing strength. Duke Energy (DUK 63.46, +1.07) is rising by 1.7% after reaching settlement with the North Carolina Utilities Commission. The settlement aims to resolve issues following the merger of Duke Energy and Progress Energy. In addition, the company President, Chairman, and Chief Executive Officer Jim Rogers announced his intention to retire by the end of next year.

In economic news, the November Chicago PMI reading of 50.4 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.7 to follow the prior month's 49.9. Personal income was unchanged in October, which is below the 0.2% increase expected by the Briefing.com consensus.

Personal spending decreased by 0.2%, which is below the expected 0.1% uptick. Core personal consumption expenditures were higher by 0.1%, which fell short of the broadly expected reading of 0.2%.DJ30 -21.81 NASDAQ -8.57 SP500 -2.89 NASDAQ Adv/Vol/Dec 974/861.5 mln/1373 NYSE Adv/Vol/Dec 1296/255.8 mln/1605

12:30 pm : The S&P 500 continues to trade near its session low following President Obama's remarks. In his statement from a Pennsylvania factory, the President reiterated the importance of reaching compromise and expressed hope that enough Republicans can be convinced to break rank and vote in favor of the President's budget proposal.

Financials are underperforming as the markets continue reacting to updates from politicians regarding the budget debate. Citigroup (C 34.61, -0.59) is the biggest laggard among the majors as it trades lower by 1.7%.

While U.S. financials trade lower, their European counterparts are seeing gains. Deutsche Bank (DB 44.05, +0.18), Banco Bilbao Vizcaya Argentaria (BBVA 8.47, +0.05), and Barclays (BCS 15.75, +0.09) are all up near 0.6%. Earlier, Reuters reported Barclays may cut as many as 3500 investment bank positions and reduce the scope of its Asian operations.DJ30 -12.98 NASDAQ -6.66 SP500 -2.11 NASDAQ Adv/Vol/Dec 966/777.7 mln/1364 NYSE Adv/Vol/Dec 1323/231.3 mln/1573

12:00 pm : Cautious action continues as the S&P 500 trades lower by 0.2%. Lawmakers will hold another press conference today as President Obama is scheduled to speak at 12:00 ET while House Speaker Boehner will address the media at 12:45 ET.

Tech stocks are underperforming the broader market and large cap names are seeing weakness. Apple (AAPL 584.55, -4.81), International Business Machines (IBM 190.02, -1.51), and Microsoft (MSFT 26.60, -0.35) are all down between 0.7% and 1.3%.

Also of note, VeriSign (VRSN 34.01, -5.33) is sliding 13.6% after its updated agreement with the Department of Commerce limited the company's ability to increase domain registration prices.

Lastly, Groupon (GRPN 4.14, -0.40) is shedding 8.8% after company spokesman said Chief Executive Officer Andrew Mason will not be replaced in the near term.DJ30 -16.21 NASDAQ -6.93 SP500 -2.64 NASDAQ Adv/Vol/Dec 976/711.5 mln/1336 NYSE Adv/Vol/Dec 1332/210.7 mln/1551

11:30 am : The S&P 500 is off by 0.2% as it continues to trade near its session low.

The consumer discretionary sector is the biggest laggard and automakers are weighing on the space. Earlier, Ford Motor (F 11.38, -0.15) said it plans to increase its electric car market share to 11.0% from the current 5.2%. Despite the news, shares of Ford are lower by 1.3%. Looking at other automakers, Honda Motor (HMC 33.22, -0.37), Toyota Motor (TM 85.99, -0.52), and Thor (THO 37.01, -0.94) are all down between 0.6% and 2.4%.

Elsewhere in the space, higher-end retailers are also underperforming. Coach (COH 57.74, -1.62) is down 2.7% and Ralph Lauren (RL 157.50, -2.90) is off by 1.8%.

Also of note, Yum! Brands (YUM 67.38, -7.09) is sliding 9.5% as it weighs on the discretionary space. Earlier, the company issued full-year 2013 guidance and reaffirmed its full-year 2012 earnings growth forecast of at least 13%. The guidance proved to be a point of concern as sales in China are expected to continue tracking lower. Following the update, Raymond James, Susquehanna, and UBS all downgraded the stock.DJ30 -15.74 NASDAQ -9.80 SP500 -2.65 NASDAQ Adv/Vol/Dec 930/607.8 mln/1344 NYSE Adv/Vol/Dec 1308/180.3 mln/1534

11:00 am : The major averages are near their respective lows and S&P 500 is off by 0.2%.

Three apparel retailers have reported their earnings after yesterday's close. Teen retailer Five Below (FIVE 34.26, +2.87) is soaring 9.1% after beating on earnings and revenue. In addition, the company issued downside fourth quarter earnings guidance while revenue is expected to come in above consensus estimates.

While Five Below is enjoying a strong session, two other names are under pressure after reporting their earnings. Pacific Sunwear (PSUN 1.71, -0.18) is sliding 9.5% and Zumiez (ZUMZ 18.91, -1.84) is down 9.0% after reporting earnings which disappointed the Street.DJ30 -6.91 NASDAQ -5.38 SP500 -1.88 NASDAQ Adv/Vol/Dec 1017/497.2 mln/1217 NYSE Adv/Vol/Dec 1391/150.5 mln/1444

10:30 am : Commodities are mixed today, while the dollar index is in negative territory. Jan crude oil just rallied almost $1/barrel and a new session high of $88.63/barrel. In current trade, crude oil is +0.3% at $88.37/barrel.

Jan natural gas futures found some buyers in recent activity and is now +0.4% at $3.66/MMBtu.

Precious metals are in the red, while copper is showing some gains. Dec gold sold off sharply earlier to a new LoD of $1721.60, while Dec silver dropped to its own new LoD of $38.03/oz. In current trade, gold is -0.2% at $1725.30 and silver is -0.9% at $34.14/oz. Dec copper +0.7% at $3.63/lb.DJ30 +14.76 NASDAQ -1.63 SP500 +0.21 NASDAQ Adv/Vol/Dec 1074/386.5 mln/1119 NYSE Adv/Vol/Dec 1507/123 mln/1249

10:00 am : The S&P 500 is adding 0.1% as it trades near its early high.

Utility stocks are among the top early performers as the SPDR Utilities Select Sector ETF (XLU 35.14, +0.19) trades higher by 0.5%. Within the space, gas utilities are outperforming. ONEOK (OKE 44.66, +0.29) and WGL Holdings (WGL 38.89, +0.29) are both up near 0.8%.

Meanwhile, electric utilities are also seeing strength. Duke Energy (DUK 63.25, +0.86) is rising by 1.4% after reaching settlement with the North Carolina Utilities Commission. The settlement aims to resolve issues following the merger of Duke Energy and Progress Energy. In addition, the company President, Chairman, and Chief Executive Officer Jim Rogers announced his intention to retire by the end of next year.DJ30 +29.38 NASDAQ -1.09 SP500 +1.35 NASDAQ Adv/Vol/Dec 1119/245.8 mln/997 NYSE Adv/Vol/Dec 1591/85.6 mln/1074

09:45 am : The S&P 500 has slid off its opening levels and the benchmark index trades lower by 0.1%.

Looking at the early sector alignment, utility stocks are outperforming the broader market. Meanwhile, the consumer discretionary sector is the biggest laggard. Yum! Brands (YUM 67.11, -7.36) is sliding 9.9% as it weighs on the discretionary space. Earlier, the company issued full-year 2013 guidance and reaffirmed its full-year 2012 earnings growth forecast of at least 13%. The guidance proved to be a point of concern as sales in China are expected to continue tracking lower. Following the guidance update, Raymond James, Susquehanna, and UBS all downgraded the stock.

In economic news, the November Chicago PMI reading of 50.4 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.7 to follow the prior month's 49.9.DJ30 +2.61 NASDAQ -2.23 SP500 -1.21 NASDAQ Adv/Vol/Dec 1051/152.1 mln/995 NYSE Adv/Vol/Dec 1421/62.5 mln/1188

09:15 am : [BRIEFING.COM] S&P futures vs fair value: +1.00. Nasdaq futures vs fair value: +1.00. As the open nears, equity futures are pointing to a flat start to the session.

Cautious early trade appears to be shaping up as high-beta names see relative weakness in pre-market action. Bank of America (BAC 9.80, -0.03) and Citigroup (C 35.07, -0.14) are both off by 0.4%.

Elsewhere, Tellabs (TLAB 3.35, +0.40) is surging 13.6% after the company named Daniel P. Kelly as the new Chief Executive Officer and President. In addition, the company declared a special dividend of $1.00.

Today's economic data will be topped off by the November Chicago PMI, which will be reported at 9:45 ET.

09:00 am : [BRIEFING.COM] S&P futures vs fair value: +1.40. Nasdaq futures vs fair value: +1.80. U.S. equity futures have slid off their pre-market highs and they are currently flat.

The major Asian averages ended mostly higher after the Japanese government launched its second stimulus package in just over a month. The latest stimulus more than doubles last month's plan to JPY880 billion, and comes as government leaders feel the pressure of next month's election. India's Sensex (+0.9%) advanced for the third consecutive session with today's gains running it to an 18-month high. The bid comes despite India's GDP slightly missing estimates with a 5.3% year-over-year print (5.4% expected, 5.5% previous). Elsewhere, Japanese data was mixed as household spending (-0.1% year-over-year actual versus -0.8% expected) and preliminary industrial production (1.8% year-over-year actual versus -1.8% expected) beat and Tokyo core CPI (-0.5% year-over-year actual versus -0.4% expected) missed. Australia's private sector credit fell short of estimates with a 0.1% month-over-month reading (0.3% expected); South Korea's industrial production posted a disappointing -0.8% year-over-year (0.9% expected); and Thailand's trade surplus swung to a $0.10 billion deficit.

In Japan, the Nikkei gained 0.5% to end at its best level in seven months. Exporters remained strong as Nissan Motor added 0.8% and Komatsu tacked on 1.2%. Elsewhere, Hitachi and Mitsubishi Heavy announced the combination of their thermal power businesses in an effort to better compete overseas. The stocks gained 4.2% and 3.0%, respectively on the news.

In Hong Kong, the Hang Seng finished higher by 0.5% as financials outperformed. Bank of Communications was firm, adding 1.1%. On the downside, Hong Kong Exchange slipped 1.4% following the announcement of a HKD7.75 billion private placement to help fund its acquisition of the London Metal Exchange.

China's Shanghai Composite advanced 0.9% to climb off a near four-year low. Construction related names led the way following comments from Vice Premier Li Keqiang who suggested the urbanization of the country is the number one priority. Jiangxi Wanniangqing Cement surged 6.1% and Poly Real Estate climbed 3.3% as a result of the comments.

The major European indices are seeing gains. European Central Bank President Draghi spoke in Paris and called out the Eurozone for living in a "fairy world." He also stated the ECB cannot solve the crisis alone. Elsewhere, Germany's finance minister commented that a Greek default would trigger a break-up of the single currency. This talk preceded the German vote on Greek aid, which was approved. Recent months have seen an uptick in disappointing economic data out of Germany. Earlier, the country reported a 2.8% month-over-month decrease in retail sales as the reading widely missed the broadly expected decline of 0.2%. In other economic data, Italy's monthly unemployment came in at 11.1%, ahead of the expected 10.9%.

In the United Kingdom, the FTSE is adding 0.2% as industrials outperform. IMI and Meggitt are seeing respective gains of 1.6% and 1.7%. Miners Eurasian Natural Resources and Evraz are the biggest laggards as the two trade lower by 1.8% and 1.3%, respectively.

France's CAC is higher by 0.2% and LVMH Moet Hennessy Louis Vuitton is leading the index. The producer of luxury goods is climbing 2.9% after Goldman Sachs upgraded the stock to ‘buy.' On the downside, telecom companies are underperforming. Alcatel-Lucent, France Telecom, and Vivendi are all down between 1.2% and 1.9%.

In Germany, the DAX is advancing 0.3% and producers of building materials are seeing relative strength. Lanxess is rising by 2.0% while HeidelbergCement is firmer by 1.7% after Morgan Stanley issued a buy recommendation. Meanwhile, steelmaker ThyssenKrupp is the biggest laggard, down 0.8%.

08:30 am : S&P futures vs fair value: +1.10. Nasdaq futures vs fair value: +2.30. Equity futures ticked lower in reaction to the latest income and spending data. The S&P 500 futures are registering marginal losses.

Personal income was unchanged in October, which is below the 0.2% increase expected by the Briefing.com consensus. Personal spending decreased by 0.2%, which is below the expected 0.1% uptick. Core personal consumption expenditures were higher by 0.1%, which fell short of the broadly expected reading of 0.2%.

08:00 am : S&P futures vs fair value: +2.50. Nasdaq futures vs fair value: +6.50. U.S. equity futures are modestly higher amid positive overseas trade.

Overnight, the world equity markets continued their climb higher. In Japan, economic data highlighted better-than-expected industrial production. In addition, the Japanese government approved another $10.7 billion in fiscal stimulus. As a result of the move, the yen weakened and exporters were bid. Meanwhile, Japan's CPI was in-line with expectations. Japan's Nikkei and Hong Kong's Hang Seng added 0.5% each, while China's Shanghai Composite gained 0.9%.

European Central Bank President Draghi spoke last night and called out the Eurozone for living in a "fairy world." He also stated the ECB cannot solve the crisis alone. Elsewhere, Germany's finance minister commented that a Greek default would trigger a break-up of the single currency. This talk preceded the German vote on Greek aid, which was approved. Recent months have seen an uptick in disappointing economic data out of Germany. Earlier, the country reported a 2.8% month-over-month decrease in retail sales and the reading widely missed the broadly expected decline of 0.2%. In other economic data, Italy's monthly unemployment came in at 11.1%, ahead of the expected 10.9%. Looking at regional indices, Germany's DAX and France's CAC are adding 0.4% each while UK's FTSE is firmer by 0.2%.

In U.S. corporate news, Yum! Brands (YUM 67.35, -7.12) is sliding 9.6% after issuing full-year 2013 guidance and reaffirming its full-year 2012 earnings growth forecast of at least 13%. The guidance proved to be a point of concern as sales in China are expected to continue tracking lower. Following the guidance update, Raymond James, Susquehanna, and UBS all downgraded the stock.

Groupon (GRPN 4.38, -0.16) is shedding 3.5% after company spokesman said Chief Executive Officer Andrew Mason will not be replaced in the near term.

Seagate Technology (STX 25.59, +0.33) is adding 1.3% after increasing its quarterly dividend by 19.0%, to $0.38 from $0.32.

Five Below (FIVE 34.21, +2.82) is rising by 9.0% after beating on earnings and revenue. In addition, the company issued downside fourth quarter earnings guidance while revenue is expected to come in above consensus estimates.

October personal income and personal spending as well as core PCE prices will all be released at 8:30 ET. Lastly, November Chicago PMI will be reported at 9:45 ET.

06:27 am : [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +6.00.

06:27 am : Nikkei...9446.01...+45.10...+0.50%. Hang Seng...22030.39...+107.50...+0.50%.

06:27 am : FTSE...5880.30...+10.00...+0.20%. DAX...7426.11...+25.10...+0.30%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage