Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

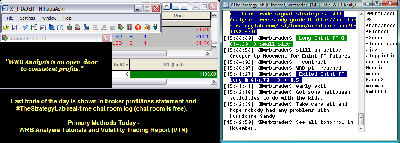

Attachment:

103112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1100.00.png [ 77.34 KiB | Viewed 472 times ]

103112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1100.00.png [ 77.34 KiB | Viewed 472 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1100.00 dollars or +11.00 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$0.00 dollars or +0.00 points.

Total Profit @ $1100.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=109&t=1356 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=192&t=1618 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading (day trading, swing trading, position trading) and reactions to the markets...something I can

not get from my broker statements alone.

U.S. Market Wrap Oct. 31 (Bloomberg) -- Bloomberg's Dina Gusovsky reports on the performance of the U.S. equity market today. Most U.S. stocks rose, with the Standard & Poor’s 500 Index reversing an earlier loss, as equity markets in the world’s largest economy reopened after Atlantic superstorm Sandy caused the longest weather-related shutdown since 1888.

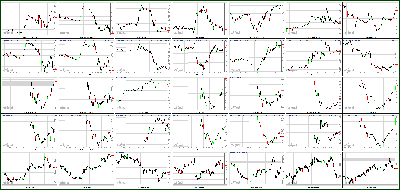

Attachment:

103112-Key-Price-Action-Markets.png [ 520.76 KiB | Viewed 431 times ]

103112-Key-Price-Action-Markets.png [ 520.76 KiB | Viewed 431 times ]

Market Update

Market Update 4:20 pm : Equities began the session on a strong note. However, the bullish sentiment failed to hold as major averages began sliding off their highs shortly after the open. The key indices then marked their respective lows in the early afternoon before rallying in the final hour to finish mixed. The S&P 500 finished flat, while Nasdaq lost 0.4%.

Looking at tech companies, the SPDR Technology Select Sector ETF (XLK 28.87, -0.11) slid 0.4%. The biggest sector component, Apple (AAPL 595.32, -8.68), lost 1.4% after announcing the departure of Scott Forstall, who was the company's head of mobile software products.

Seagate Technology (STX 27.33, -0.58) shed 2.1% after reporting disappointing earnings. During the first quarter, the hard drive manufacturer earned $1.45, which was $0.25 worse than the Capital IQ consensus estimate. In addition, the company's revenue of $3.73 billion also fell short of analyst expectations.

Western Union (WU 12.72, -5.20) plunged 29.0% after reporting in-line earnings. However, the company's revenue of $1.42 billion fell short of the $1.47 billion expected by the Capital IQ consensus. In addition, the company announced a 25.0% increase in quarterly dividend to $0.125. Following the earnings release, Western Union received six analyst downgrades.

Facebook (FB 21.11, -0.83) lost 3.5% after another lockup expiry took place.

A handful of names within the software industry made notable moves. Commvault Systems (CVLT 62.37, +8.90) soared 16.6% after beating on the top and the bottom line. During the second quarter, the software company earned $0.38 on $118.2 million in revenue. Both figures were ahead of the Capital IQ consensus estimates. In addition, the Board of Directors authorized a $50 million increase to the existing stock repurchase program.

Elsewhere, JDA Software (JDAS 38.15, +4.23) spiked 12.5% after reports from Reuters indicated JDA is exploring a sale, and has hired JPMorgan as an advisor.

OPNET Technologies (OPNT 42.05, +9.95) surged 31.0% after entering into a definitive agreement to be acquired by Riverbed Technology (RVBD 18.47, -4.15). Per the agreement, Riverbed will pay $43 per share, representing a 34.0% premium to OPNET's Friday closing price.

In other M&A news, Warnaco Group (WRC 70.58, +19.70) will be acquired by PVH (PVH 109.96, +18.46) in a transaction valued at $2.9 billion. Warnaco stockholders will receive $68.43 per share, which represents a 34.0% premium to Warnaco's last closing price. Following the acquisition, PVH issued upside guidance as the company now expects third quarter and full-year earnings near the top range of its prior guidance of $2.28-2.30. Meanwhile, the Capital IQ consensus expects the company to earn $2.29 per share.

The Dow Jones Transportation Average settled higher by 0.7% with trucking stocks leading the complex. Landstar System (LSTR 50.60, +2.47) was the top performer, and settled higher by 5.1% after Goldman initiated coverage of the stock with a ‘neutral' rating. Con-way (CNW 29.11, +1.12) rose by 4.0% after Goldman resumed coverage with a ‘buy' rating. Meanwhile, other freight carriers also saw strength. JB Hunt Transport (JBHT 58.70, +1.54) and CH Robinson (CHRW 60.31, +0.90) advanced 2.7% and 1.5%, respectively.

On the downside, railroads saw general weakness. Norfolk Southern (NSC 61.35, -0.92) and Union Pacific (UNP 123.03, -0.58) shed 1.5% and 0.5%, respectively.

Two automakers moved higher after reporting strong earnings. General Motors (GM 25.50, +2.22) surged 9.5% after reporting earnings of $0.90, which was $0.30 ahead of the Capital IQ consensus estimate. The automaker's revenue of $37.6 billion represented a 4.6% year-over-year decrease, but the figure was ahead of analyst estimates.

Meanwhile, Ford Motor (F 11.16, +0.85) jumped 8.2% after reporting mixed earnings. During the third quarter, the company earned $0.40, which was $0.10 better than the Capital IQ consensus estimate. However, the company's revenue of $30.20 billion fell short of analyst expectations. Regarding the fourth quarter outlook, management said it expects production volume to increase in all regions except Europe. Today's buying has lifted the shares to levels not seen since early May.

The weekly MBA Mortgage Index registered a 4.8% decrease in new mortgage applications over the past week. This follows last week's 12.0% decrease.

Third quarter Employment Cost Index increased by 0.4%, which was slightly worse than the 0.5% increase that was widely forecast. Today's reading follows prior quarter's increase of 0.5%.

October Chicago PMI of 49.9 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.9 to follow the prior month's 49.7.

Looking at tomorrow's economic data, automakers will be reporting their sales throughout the day and October Challenger Job Cuts will be announced at 7:30 ET. October ADP Employment Change Survey will be released at 8:15 ET. In addition, weekly initial and continuing claims, third quarter unit labor costs and preliminary productivity will all be released at 8:30 ET. Lastly, the ISM Index, construction spending, and consumer confidence will all hit the wires at 10:00 ET.DJ30 -10.75 NASDAQ -10.75 SP500 +0.22 NASDAQ Adv/Vol/Dec 1354/1.76 bln/1131 NYSE Adv/Vol/Dec 1776/852.9 mln/1289

3:30 pm : Crude oil popped to a pit session high of $87.14 per barrel in late morning action. However, the energy component slowly gave up the gain as the dollar index recovered near the unchanged level. It settled at $86.22 per barrel.

Natural gas brushed a floor session high of $3.78 in early morning action but inched lower as the session progressed. It eventually closed at $3.69.

Precious metals advanced higher as pit trade went on. Gold came off its session low of $1716.60 per ounce and popped to a session high of $1726.60 per ounce in late morning action. It settled at $1719.40 per ounce. Silver traded as high as $32.44 per ounce and closed at $32.31 per ounce.DJ30 +9.53 NASDAQ -10.92 SP500 +1.86 NASDAQ Adv/Vol/Dec 1210/1421.2 mln/1251 NYSE Adv/Vol/Dec 1671/510 mln/1384

3:00 pm : The major averages are holding their recent levels and the S&P 500 is off by 0.2%.

More than eighty companies are scheduled to report their earnings after today's close. Allstate (ALL 39.77, -0.38) is one of the names which will announce its earnings this evening. The Capital IQ consensus expects the insurer to report earnings of $1.12 on $6.72 billion in revenue.

Visa (V 138.35, +0.04) is also scheduled to report after-hours. The Capital IQ consensus calls for earnings of $1.50 on revenue of $2.67 billion. Other notable names which will report after the bell include, Caesars Entertainment (CZR 5.85, 0.00), Con-way (CNW 28.80, +0.81), MetLife (MET 35.35, +0.13), and Sturm Ruger (RGR 45.85, -0.50).

Tomorrow morning, Avon Products (AVP 15.50, +0.02), Exxon Mobil (XOM 90.73, +0.11), Kellogg (K 52.52, -0.38), and Sony (SNE 11.75, -0.10) are among the names scheduled to report before the open.DJ30 -35.13 NASDAQ -15.78 SP500 -2.72 NASDAQ Adv/Vol/Dec 1130/1.31 bln/1321 NYSE Adv/Vol/Dec 1525/461.2 mln/1515

2:30 pm : The Dow and S&P 500 are shedding 0.1% as they hover just below their respective flat lines.

Two automakers are moving higher after reporting strong earnings. General Motors (GM 25.48, +2.20) is surging 9.4% after reporting earnings of $0.90, which was $0.30 ahead of the Capital IQ consensus estimate. The auto maker's revenue of $37.6 billion represented a 4.6% year-over-year decrease, but the figure was ahead of analyst estimates.

Ford Motor (F 11.00, +0.69) is advancing 6.7% after reporting mixed earnings. During the third quarter, the company earned $0.40, which was $0.10 better than the Capital IQ consensus estimate. However, the company's revenue of $30.20 billion fell short of analyst expectations. Regarding the fourth quarter outlook, management said it expects production volume to increase in all regions except Europe. Today's buying has lifted the shares to levels not seen since early May.DJ30 -15.36 NASDAQ -11.87 SP500 -0.93 NASDAQ Adv/Vol/Dec 1114/1.18 bln/1329 NYSE Adv/Vol/Dec 1527/421.9 mln/1499

2:00 pm : The major averages have shown little change during the past 30 minutes and the S&P 500 is off by 0.2%.

A handful of names within the software industry are making notable moves. OPNET Technologies (OPNT 41.47, +9.37) is surging 29.2% after entering into a definitive agreement to be acquired by Riverbed Technology (RVBD 18.27, -4.35). Per the agreement, Riverbed will pay $43 per share, representing a 34.0% premium to OPNET's Friday closing price.

Commvault Systems (CVLT 63.47, +10.00) is soaring 18.7% after beating on the top and the bottom line. During the second quarter, the software company earned $0.38 on $118.2 million in revenue. Both figures were ahead of the Capital IQ consensus estimates. In addition, the Board of Directors authorized a $50 million increase to the existing stock repurchase program.

Elsewhere, JDA Software (JDAS 37.92, +4.00) is spiking 11.8% after reports from Reuters indicated JDA is exploring a sale, and has hired JPMorgan as an advisor.DJ30 -36.22 NASDAQ -17.37 SP500 -3.06 NASDAQ Adv/Vol/Dec 1056/1.09 bln/1370 NYSE Adv/Vol/Dec 1433/389.8 mln/1591

1:30 pm : The Dow is shedding 0.2% as it trades just above its session low.

The Dow Jones Transportation Average trades higher by 0.4% and trucking stocks are leading. Landstar System (LSTR 50.51, +2.38) is the top performer as it trades higher by 4.9% after Goldman initiated coverage of the stock with a ‘neutral' rating. Con-way (CNW 28.66, +0.67) is rising by 2.4% after Goldman resumed coverage with a ‘buy' rating. Meanwhile, other freight carriers are also seeing strength. JB Hunt Transport (JBHT 58.41, +1.25) and CH Robinson (CHRW 60.62, +1.21) are advancing 2.2% and 2.1%, respectively.

On the downside, railroads are seeing general weakness. Norfolk Southern (NSC 61.60, -0.67) and Union Pacific (UNP 122.78, -0.83) are down 1.1% and 0.7%, respectively.DJ30 -30.06 NASDAQ -16.92 SP500 -2.80 NASDAQ Adv/Vol/Dec 1019/1.02 bln/1388 NYSE Adv/Vol/Dec 1414/363.2 mln/1602

1:00 pm : Equities started the session on a positive note, but the bullish sentiment was dispelled within the first two hours of trade. The major averages have been declining steadily into afternoon trade, and the S&P 500 is currently lower by 0.3%. The Nasdaq is down 0.6% as it underperforms the other indices.

Looking at tech companies, the SPDR Technology Select Sector ETF (XLK 28.84, -0.14) is off by 0.5%. The biggest sector component, Apple (AAPL 596.22, -7.78), is down 1.3% after announcing the departure of Scott Forstall, who was the company's head of mobile software products.

Seagate Technology (STX 27.07, -0.84) is shedding 3.0% after reporting disappointing earnings. During the first quarter, the hard drive manufacturer earned $1.45, which was $0.25 worse than the Capital IQ consensus estimate. In addition, the company's revenue of $3.73 billion also fell short of analyst expectations.

Western Union (WU 12.74, -5.19) is diving 29.0% after reporting in-line earnings. However, the company's revenue $1.42 billion fell short of the $1.47 billion expected by the Capital IQ consensus. In addition, the company announced a 25.0% increase in quarterly dividend to $0.125. Following the earnings release, WU received six analyst downgrades.

Facebook (FB 21.17, -0.77) is down 3.5% after another lockup expiry took place. Peer Zynga (ZNGA 2.22, -0.09) is sliding 3.9% after Electronic Arts (EA 12.19, +0.28) commented on weakness in mobile gaming in its earnings report.

Mastercard (MA 459.09, +6.11) is adding 1.4% after beating on the bottom line. The payment processor reported earnings of $6.17 per share, which was $0.24 better than the Capital IQ consensus estimate. Meanwhile, the company's revenue was in-line with expectations.

Steel stocks are trading lower as a group. ArcelorMittal (MT 14.79, -0.64) is down 4.2% after reporting a loss of $0.46, which may not be comparable with the Capital IQ consensus estimates. Meanwhile, the company's revenue of $19.72 billion was in-line with estimates. In addition, the company's Board of Directors proposed a reduction to the annual dividend from $0.75 to $0.20.

Elsewhere, United States Steel (X 20.44, -0.70) is sliding 3.4% after reporting earnings of $0.01, which was slightly better than the Capital IQ forecast of a breakeven quarter. The company's revenue of $4.65 billion was in-line with expectations. Also of note, rumors are suggesting that a noted short seller David Einhorn has taken a cautious stance on the stock. Other steelmakers are also seeing weakness. AK Steel (AKS 5.02, -0.16) and Reliance Steel & Aluminum (RS 53.99, -0.94) are down 3.1% and 1.7%, respectively.

In M&A news, Warnaco Group (WRC 69.92, +19.04) will be acquired by PVH (PVH 106.38, +14.88) in a transaction valued at $2.9 billion. Warnaco stockholders will receive $68.43 per share, which represents a 34.0% premium to Warnaco's last closing price. Following the acquisition, PVH issued upside guidance as the company now expects third quarter and full-year earnings near the top range of its prior guidance of $2.28-2.30. Meanwhile, the Capital IQ consensus expects the company to earn $2.29 per share.

In economic data, the October Chicago PMI of 49.9 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.9 to follow the prior month's 49.7.DJ30 -35.61 NASDAQ -17.37 SP500 -3.63 NASDAQ Adv/Vol/Dec 1005/943.5 mln/1404 NYSE Adv/Vol/Dec 1395/337.4 mln/1604

12:30 pm : The S&P 500 and Dow have slipped to fresh session lows and both indices are shedding 0.3%.

Steel stocks are trading lower as a group. ArcelorMittal (MT 14.81, -0.63) is down 4.1% after reporting a loss of $0.46, which may not be comparable with the Capital IQ consensus estimates. Meanwhile, the company's revenue of $19.72 billion was in-line with estimates. In addition, the company's Board of Directors proposed a reduction to the annual dividend from $0.75 to $0.20.

Elsewhere, United States Steel (X 20.32, -0.82) is sliding 3.9% after reporting earnings of $0.01, which was slightly better than the Capital IQ forecast of a breakeven quarter. The company's revenue of $4.65 billion was in-line with expectations. Also of note, rumors are suggesting that a noted short seller David Einhorn has taken a cautious stance on the stock.

Other steelmakers are also seeing weakness. AK Steel (AKS 5.06, -0.13) and Reliance Steel & Aluminum (RS 54.01, -0.92) are down 2.5% and 1.6%, respectively.DJ30 -48.86 NASDAQ -21.01 SP500 -5.67 NASDAQ Adv/Vol/Dec 1007/859.5 mln/1383 NYSE Adv/Vol/Dec 1382/306.8 mln/1603

12:00 pm : The S&P 500 is off by 0.2% as it continues to hover near its unchanged line.

The health care sector is the weakest performer of the day. Within the group, WellCare Health Plans (WCG 47.50, -7.73) is sliding 14.0% after the company's earnings of $1.05 missed the Capital IQ consensus estimate by $0.42. In addition, the company issued downside full-year 2012 earnings guidance.

Impax Laboratories (IPXL 21.26, -3.08) is falling 12.7% after reporting in-line earnings, and revenue below Capital IQ consensus estimates. The company's revenue fell short of analyst expectations and management issued downside fourth quarter guidance.

On the upside, Hansen Medical (HNSN 2.22, +0.41) is spiking 22.7% after announcing an expanded patent agreement with Intuitive Surgical (ISRG 541.54, +5.70).DJ30 -14.97 NASDAQ -16.85 SP500 -2.47 NASDAQ Adv/Vol/Dec 1088/767.5 mln/1294 NYSE Adv/Vol/Dec 1529/272.3 mln/1445

11:30 am : The major averages have bounced off their freshly-set lows, and the three indices are now mixed. The S&P 500 is currently flat.

The SPDR S&P Homebuilders ETF (XHB 25.90, +0.38) trades higher by 1.5%, but the strength is not related to homebuilder stocks. DR Horton (DHI 20.71, -0.05), PulteGroup (PHM 17.21, -0.06), and MDC Holdings (MDC 37.59, -0.24) are all down between 0.2% and 0.5%.

Meanwhile, home improvement stores and furniture producers are driving the homebuilders ETF higher. Home Depot (HD 61.49, +1.45) and Lowe's (LOW 32.15, +0.79) are both up near 2.5%. Furniture manufacturer Leggett & Platt (LEG 26.73, +1.33) is advancing 5.2% and appliance manufacturer Whirlpool (WHR 96.30, +1.01) is firmer by 1.1%.DJ30 +6.23 NASDAQ -11.33 SP500 -0.18 NASDAQ Adv/Vol/Dec 1105/681.5 mln/1268 NYSE Adv/Vol/Dec 1547/241.2 mln/1415

11:00 am : The major averages have slipped to their respective session lows. The Nasdaq is the worst performing index as it trades lower by 0.5%.

Looking at the tech companies, the SPDR Technology Select Sector ETF (XLK 28.83, -0.16) is off by 0.6%. The biggest sector component Apple (AAPL 590.00, -14.00) is down 2.3% after announcing the departure of Scott Forstall, who was the company's head of mobile software products.

Seagate Technology (STX 27.13, -0.77) is shedding 2.8% after reporting disappointing earnings. During the first quarter, the hard drive manufacturer earned $1.45, which was $0.25 worse than the Capital IQ consensus estimate. In addition, the company's revenue of $3.73 billion also fell short of analyst expectations.

Western Union (WU 13.22, -4.71) is diving 26.3% after reporting in-line earnings. However, the company's revenue $1.42 billion fell short of the $1.47 billion expected by the Capital IQ consensus. In addition, the company announced a 25.0% increase in quarterly dividend to $0.125. Following the earnings release, WU received six analyst downgrades.

Facebook (FB 21.36, -0.57) is down 2.6% after another lockup expiry took place. Peer Zynga (ZNGA 2.21, -0.10) is sliding 4.3%.

Lastly, Mastercard (MA 455.40, +2.42) is adding 0.5% after beating on earnings. The payment processor reported earnings of $6.17 per share, which was $0.24 better than the Capital IQ consensus estimate. Meanwhile, the company's revenue was in-line with expectations.DJ30 +10.82 NASDAQ -17.09 SP500 -1.09 NASDAQ Adv/Vol/Dec 1068/544.6 mln/1274 NYSE Adv/Vol/Dec 1484/201.8 mln/1435

10:35 am : The dollar index has been in the red all morning so far, falling in negative overnight. As a result, commodities have benefitted and are trading higher this morning. Dec crude oil rose as high as $86.59/barrel overnight and is currently back near its HoD, now at $86.41/barrel, up 0.9%.

Dec natural gas has been in positive territory all session, pushing to a HoD of $3.78/MMBtu. It is currently pulling back and is now +1.4% at $3.74/MMBtu.

Precious metals are higher as well with gold and silver trading near session highs. In current activity, Dec gold is +0.4% at $1719.20/oz, while Dec silver is +1.3% at $32.22/oz. Dec copper is +0.7% at $3.53/lb.DJ30 +40.51 NASDAQ -10.22 SP500 +2.38 NASDAQ Adv/Vol/Dec 1104/416.4 mln/1200 NYSE Adv/Vol/Dec 1658/166 mln/1217

10:05 am : The S&P 500 trades higher by 0.3% while Nasdaq continues its decline. The tech-heavy index is currently off by 0.2%.

The industrial sector is the top performer and providers of building materials are seeing strength in the early going. Beacon Roofing Supply (BECN 32.44, +1.45), Eagle Materials (EXP 52.24, +4.01), Fastenal Company (FAST 44.95, +1.71), and Owens Corning (OC 33.50, +2.06) are all up between 4.0% and 8.3%.

Elsewhere in industrials, provider of industrial equipment, Lawson Products (LAWS 6.92, +0.35) is higher by 5.4%.DJ30 +65.94 NASDAQ -4.63 SP500 +4.47 NASDAQ Adv/Vol/Dec 1130/266.1 mln/1096 NYSE Adv/Vol/Dec 1696/116.9 mln/1139

09:50 am : Equities have opened on a mixed note. The Dow is higher by 0.5% while Nasdaq is off by 0.2%.

Seagate Technology (STX 27.50, -0.41) is shedding 1.5% after reporting disappointing earnings. During the first quarter, the hard drive manufacturer earned $1.45, which was $0.25 worse than the Capital IQ consensus estimate. In addition, the company's revenue of $3.73 billion also fell short of analyst expectations.

In M&A news, Warnaco Group (WRC 71.08, +20.16) will be acquired by PVH (PVH 111.32, +19.82) in a transaction valued at $2.9 billion. Warnaco stockholders will receive $68.43 per share, which represents a 34.0% premium to Warnaco's last closing price. Following the acquisition, PVH issued upside guidance as the company now expects third quarter and full-year earnings near the top range of its prior guidance of $2.28-2.30. Meanwhile, the Capital IQ consensus expects the company to earn $2.29 per share.

The October Chicago PMI reading of 49.9 surprised to the downside as economists surveyed by Briefing.com had generally expected a reading of 50.9 to follow the prior month's 49.7.DJ30 +62.05 NASDAQ -4.04 SP500 +4.63 NASDAQ Adv/Vol/Dec 1151/171.5 mln/1045 NYSE Adv/Vol/Dec 1651/90.9 mln/1129

09:19 am : [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: -0.30. Heading into the open, the S&P 500 futures are higher by 0.4%. Volatile trade can be expected as stocks will be reacting to earnings which were reported on Monday, Tuesday, and earlier today.

Home improvement stores are seeing strength in the pre-market as they are expected to benefit from hurricane recovery. Home Depot (HD 62.50, +2.46) and Lowe's (LOW 32.75, +1.39) are seeing respective gains of 4.1% and 4.4%.

Elsewhere, Walt Disney (DIS 51.45, +1.37) is rising by 2.7% after agreeing to acquire Lucasfilm Ltd. for $4.05 billion. Hasbro (HAS 36.99, +1.00), who is holding the license to make Star Wars toys through 2020, is adding 2.8%.

October Chicago PMI will be reported at 9:45 ET.

09:01 am : [BRIEFING.COM] S&P futures vs fair value: +6.70. Nasdaq futures vs fair value: +1.00. U.S. equity futures are mixed. The S&P 500 futures are higher by 0.4% while Nasdaq futures are flat.

The major Asian indices ended mostly higher, receiving a boost from the earnings of some of China's state-owned enterprises. Data out overnight was heavy as Japan's average cash earnings were unchanged year-over-year (-0.3% expected) and both Australian building approvals (7.8% month-over-month actual v. 1.1% expected) and private sector credit (0.3% month-over-month actual v. 0.2% expected) beat. Elsewhere, South Korea's industrial production expanded at a weaker than expected 0.7% year-over-year (1.2% expected) while Singapore's unemployment rate eased to 1.9% (2.2% previous).

In Japan, the Nikkei closed higher by 1.0% thanks to some surprising earnings results. Komatsu and Hitachi both gained 3.2% after reaffirming their outlooks for next year, and Fuji Heavy surged 6.7% after a 22% jump in profit.

Hong Kong's Hang Seng advanced 1.0% as financials gained while energy lagged. Industrial & Commercial Bank of China rallied 1.2% following its better than expected reults, and that caused the other banking giants to climb between 1.0% and 1.6% as they piggybacked the move. Meanwhile, PetroChina shed 3.3% after third quarter profit fell a greater than expected 33.0%

China's Shanghai Composite added 0.3% as rail names outperformed. China Railway Group surged 5.7% and China Railway Construction gained 4.7% after both companies posted better than expected results.

European markets are generally higher after a slew of mixed macro data points crossed the wires. In the United Kingdom, consumer confidence came in at -30, which was the lowest level since April. German retail sales showed a 3.1% year-over-year decrease, while expectations called for a more palatable decline of 1.2%. The Eurozone unemployment rate ticked up to 11.6% while the region's Flash CPI was reported at 2.5%, in-line with expectations. Elsewhere, a European Central Bank member noted the Bank is not discussing conditions for its bond purchase program with any Eurozone government. Meanwhile, Eurozone finance ministers are holding a call to discuss Greece as the country is set to present the draft of its 2013 budget today.

In the United Kingdom, the FTSE is shedding 0.3%. Barclays is down 3.5% after revealing that the financial is the target of two regulatory probes. Elsewhere, energy producer BG Group is sliding 17.2% after issuing disappointing guidance. However, other energy stocks are outperforming. Petrofac and Tullow Oil are both up near 3.3%.

France's CAC is showing little change. Car maker Renault is the top performer as it trades higher by 1.3%. On the downside, steelmaker ArcelorMittal is down 4.9% after reporting a drop in quarterly profit and cutting the 2013 dividend due to slowing Asian demand. Financials are also seeing weakness. BNP Paribas, Credit Agricole, and Societe Generale are all down between 0.6% and 1.5%.

In Germany, the DAX is advancing 0.5% and Deutsche Lufthansa is leading the index. The airline operator is spiking 7.2% after reporting strong earnings. Health care stocks are underperforming. Fresenius Medical and Fresenius SE are seeing respective losses of 4.0% and 2.0%.

08:33 am : [BRIEFING.COM] S&P futures vs fair value: +7.00. Nasdaq futures vs fair value: +2.30. Equity futures have shown little change to the latest Employment Cost Index data. The S&P 500 futures are higher by 0.5%.

The third quarter Employment Cost Index increased by 0.4%, which is slightly worse than the 0.5% increase that was widely forecast. Today's reading follows prior quarter's increase of 0.5%.

08:00 am : S&P futures vs fair value: +8.20. Nasdaq futures vs fair value: +8.30. U.S. equity futures are modestly higher as trade on the New York Stock Exchange is set to resume at 9:30 ET.

Overnight, the global equity markets climbed higher, and appeared to be setting the stage for a rally in the U.S. following the 2-day closure. In Asia, Japan rebounded from yesterday's weakness which followed Bank of Japan's ninth easing operation. Economic data was light in the region, but Japan's average cash earnings were unchanged year-over-year. This was ahead of the expected 0.3% decline. Meanwhile, housing starts increased by 15.5% as compared to last year. The reading was behind the 16.1% expected rise. Key Asian indices finished broadly higher as Japan's Nikkei and Hong Kong's Hang Seng gained 1.0% each. China's Shanghai Composite underperformed, but rallied into the close to finish higher by 0.3%.

In Europe, a slew of mixed macro data points were reported. In the UK, consumer confidence came in at -30, which was its lowest level since April. German retail sales showed a 3.1% year-over-year decrease, while expectations called for a 1.2% decline. The Eurozone unemployment rate ticked up to 11.6% while the region's CPI was reported at 2.5%, in-line with expectations. Elsewhere, a European Central Bank member noted the Bank is not discussing conditions for its bond purchase program with any Eurozone government. Meanwhile, the Eurozone finance ministers are holding a call to discuss Greece as the country is set to present its 2013 draft budget today. Nearing midday, Germany's DAX is advancing 0.7%, France's CAC is higher by 0.4%, and UK's FTSE is off by 0.1%.

In U.S. corporate news, Warnaco Group (WRC 50.88, 0.00) will be acquired by PVH (PVH 97.23, +5.73) in a transaction valued at $2.9 billion. Warnaco stockholders will receive $68.43 per share, which represents a 34.0% premium to Warnaco's last closing price. Following the acquisition, PVH issued upside guidance as the company now expects third quarter and full-year earnings near the top range of its prior guidance of $2.28-2.30. Meanwhile, the Capital IQ consensus expects the company to earn $2.29 per share.

General Motors (GM 24.00, +0.72) is higher by 3.1% after reporting earnings of $0.90, which was $0.30 ahead of the Capital IQ consensus estimate. The auto maker's revenue of $37.6 billion represented a 4.6% year-over-year decrease, but the figure was ahead of analyst estimates.

Ford Motor (F 10.77, +0.46) is advancing 4.5% after reporting mixed earnings. During the third quarter, the company earned $0.40, which was $0.10 better than the Capital IQ consensus estimate. However, the car maker's revenue of $30.20 billion was below analyst expectations.

The weekly MBA Mortgage Index registered a 4.8% decrease in new mortgage applications over the past week. This follows last week's 12.0% decrease.

The third quarter employment cost index will be released at 8:30 ET while October Chicago PMI will hit the wires at 9:45 ET.

06:41 am : [BRIEFING.COM] S&P futures vs fair value: +9.50. Nasdaq futures vs fair value: +13.00.

06:40 am : Nikkei...8928.29...+86.30...+1.00%. Hang Seng...21641.82...+213.20...+1.00%.

06:40 am : FTSE...5845.51...-4.40...-0.10%. DAX...7329.60...+45.20...+0.60%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage