Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

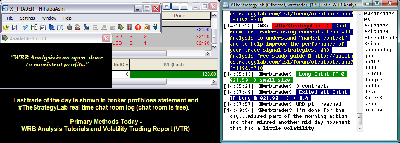

Attachment:

090512-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-120.png [ 78.12 KiB | Viewed 280 times ]

090512-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-120.png [ 78.12 KiB | Viewed 280 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +1.20 points or

$120 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=108&t=1314.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=171&t=1594 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading and reactions to the markets...something I can not get from my broker statements alone.

U.S. Market Wrap Sept. 5 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. Most U.S. stocks fell, sending the Standard & Poor’s 500 Index lower for a second day, amid a slump in FedEx Corp. and disappointing global economic data as investors awaited the European Central Bank’s plan to buy bonds.

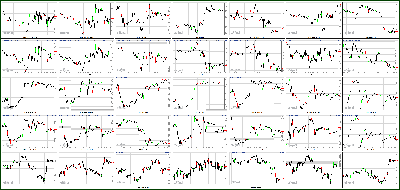

Attachment:

090512-Key-Price-Action-Markets.png [ 539.28 KiB | Viewed 275 times ]

090512-Key-Price-Action-Markets.png [ 539.28 KiB | Viewed 275 times ]

Market Update

Market Update 4:15 pm : Equities spent the majority of the session chopping around the unchanged line. The early morning volatility coincided with a Bloomberg TV report which indicated the European Central Bank bond purchase program is said to pledge unlimited, sterilized buying of bonds. However, the exuberance was short-lived as European Central Bank officials declined to comment, and reports out of Germany suggested Chancellor Angela Merkel would only support the program in the near-term. Afternoon trade was mostly quiet as the S&P 500 remained in a narrow range before closing lower by 0.1%.

The telecom sector got off to a strong start and maintained its gains throughout the day. Sprint (S 4.95, +0.15) advanced 3.1% as it outperformed other holdings within the iShares Dow Jones US Telecom ETF (IYZ 24.39, +0.13).

The Dow Jones Transportation Average continued its recent streak of underperformance; however, individual components within the group showed significant divergence. Shares of major airlines saw a relatively strong bid as United Continental Holdings (UAL 19.07, +0.97) led the major carriers with a 5.4% gain. Delta Air Lines (DAL 8.89, +0.33) added 3.9% after announcing August consolidated passenger unit revenue increased by 4.0% on a year-over-year basis. Meanwhile, companies specializing in logistics slipped after FedEx (FDX 85.80, -1.74) lowered its first quarter guidance, citing weaker global demand. FedEx shed 2.0% while UPS (UPS 71.94, -1.76) slid 2.4% and Con-way (CNW 29.97, -1.21) ended lower by 3.9%.

Financial stocks have traded mostly in-line with the broader market. However, several names diverged from the rest of the group. Goldman Sachs (GS 109.94, +3.53) was the best performer as it ended higher by 3.3%. On the downside, American Express (AXP 57.19, -1.42) dipped 2.2% as it trailed the other majors. Elsewhere, European financials were mostly higher with UBS (UBS 11.38, +0.29) and Credit Suisse (CS 19.24, +0.34) posting gains of 2.6% and 1.8%, respectively.

Restaurant operator Bloomin' Brands (BLMN 13.86, +0.41) advanced 3.1% after delivering its first earnings report as a publically traded company. The quarterly report showed second quarter earnings growth of 23.0% compared to the same period last year. Meanwhile, two names which began trading within the past twelve months also finished on a positive note. Facebook (FB 18.58, +0.85) closed higher by 4.8% after announcing Chief Executive Officer, Mark Zuckerberg, has no intention to sell any shares for at least twelve months. Meanwhile, Jefferies initiated coverage of the stock with a ‘buy' rating and a $30.00 price target. Zynga (ZNGA 2.92, +0.09) rose by 3.2% as it benefited from the strength in Facebook.

Nokia (NOK 2.38, -0.45) slumped 15.9% after the company unveiled its new Lumia 920 phone which features an improved camera and wireless charging capabilities. The phone is based on the Windows operating system, developed by Microsoft (MSFT 30.39, +0.01).

Productivity data for the second quarter showed an increase of 2.2%, which was an improvement over the 1.6% increase that had been reported in the preliminary reading. It is also better than the 1.8% increase that had been broadly expected. Unit labor costs for the first quarter were revised lower to reflect a 1.5% increase after they had reportedly increased by 1.7% in the preliminary reading. Economists polled by Briefing.com had expected that unit labor costs would tick down in the revised reading to reflect an increase of 1.4%.

A handful of economic data points will be released tomorrow. Challenger job cuts will be reported at 7:30 ET. ADP Employment Change is scheduled for an 8:15 ET release, while initial and continuing claims will hit the wires at 8:30 ET. The ISM Services report will top off the day's data at 10 ET.

Also of note, the European Central Bank will announce its interest rate decision at 7:45 ET which will be followed by Mario Draghi's press conference at 8:30 ET. In addition, the Bank of England will opine tomorrow morning at 7:00 ET. The central bank is expected to keep both its benchmark interest rate and its asset purchase program steady at 0.50% and GBP375 billion.DJ30 +11.54 NASDAQ -5.79 SP500 -1.50 NASDAQ Adv/Vol/Dec 1078/1.42 bln/1381 NYSE Adv/Vol/Dec 1407/675.6 mln/1553

3:30 pm : Crude oil touched a session high of $95.72 per barrel as pit trade opened but plunged into the red and to a session low of $94.26 per barrel moments after trading in the equity markets began. Despite the fall, the energy component erased the losses and climbed back into the black by afternoon action. Crude then chopped around near the unchanged line and settled four cents higher at $95.38 per barrel.

Natural gas trended lower into negative territory after it brushed a pit session high of $2.84 per MMBtu in morning action. It fell as low as $2.78 per MMBtu just before it settled with a 2.1% loss at $2.80 per MMBtu.

Gold see-sawed between positive and negative territory in choppy fashion during today's pit trade. Action came ahead of tomorrow's anticipated ECB meeting. It touched a session low of $1691.50 per ounce and peaked at $1697.60 per ounce. The yellow metal eventually settled slightly lower with a 0.1% loss at $1694.20 per ounce. Silver brushed a session high of $32.43 per ounce in morning action but was unable to stay in positive territory. It spent the remainder of its session trading just below the unchanged level and settled 0.2% lower at $32.33 per ounce.DJ30 +16.02 NASDAQ -4.67 SP500 -0.89 NASDAQ Adv/Vol/Dec 1124/1.13 bln/1325 NYSE Adv/Vol/Dec 1415/418.2 mln/1526

3:00 pm : Equities have pushed up to the unchanged line as slow afternoon trade continues.

Financial stocks have traded mostly in-line with the broader market. However, several names are diverging from the rest of the group. Goldman Sachs (109.83, +3.42) is the best performer as it trades higher by 3.2%. Meanwhile, American Express (AXP 57.26, -1.35) is down 2.3% as it trails the other majors.

Elsewhere, European financials are mostly higher with UBS (UBS 11.43, +0.34) and Credit Suisse (CS 19.29, +0.39) up 3.1% and 2.1%, respectively.DJ30 +15.10 NASDAQ -2.19 SP500 -0.63 NASDAQ Adv/Vol/Dec 1140/1.03 bln/1286 NYSE Adv/Vol/Dec 1423/381.4 mln/1500

2:30 pm : Stocks are lifting off their lows as they climb back towards the unchanged line. The S&P 500 is off by 0.1%.

Shares of gun makers are higher after the Federal Bureau of Investigation released its monthly summary of the National Instant Criminal Background Check System. The report showed a 34.0% increase in background checks conducted prior to handgun sales which translates into strong demand for Smith & Wesson (SWHC 8.68, +0.61) and Sturm, Ruger & Company (RGR 45.46, +1.96). The two stocks are higher by 7.6% and 4.5%, respectively. In addition, heavy call volume has been spotted in Smith & Wesson options ahead of its earnings release after the closing bell on Thursday. The gunsmith is expected to report earnings of $0.18 on $129.43 million revenues.DJ30 +6.64 NASDAQ -3.38 SP500 -1.39 NASDAQ Adv/Vol/Dec 1127/956.2 mln/1296 NYSE Adv/Vol/Dec 1364/351.7 mln/1551

2:00 pm : After maintaining a narrow range through the early afternoon, stocks have slipped to their session lows in a move which appeared to be broad-based. Nine out of ten S&P 500 sectors have followed the same pattern while telecoms were able to post slimmer losses than the rest. The S&P 500 is lower by 0.2%.DJ30 +0.57 NASDAQ -5.00 SP500 -1.94 NASDAQ Adv/Vol/Dec 1053/892.3 mln/1356 NYSE Adv/Vol/Dec 1284/328.5 mln/1627

1:30 pm : Stocks remain in a narrow afternoon range as the S&P 500 is unchanged.

Restaurant operator Bloomin' Brands (BLMN 14.28, +0.83) is higher by 5.9% after delivering its first earnings report as a publically traded company. The quarterly report showed a second quarter earnings growth of 23.0% compared to the same period last year.

Meanwhile, three names which began trading within the past twelve months are also advancing. Facebook (FB 18.56, +0.84) is up 4.6% after announcing Chief Executive Officer, Mark Zuckerberg, has no intention to sell any shares for at least twelve months. In addition, Jefferies initiated coverage of the stock with a ‘buy' rating and a $30.00 price target. Zynga (ZNGA 2.90, +0.07) is firmer by 2.5% as it benefits from Facebook's rise.

Elsewhere, Groupon (GRPN 4.27, +0.03) is up 1.0% after marking an all-time low at $4.00 yesterday.DJ30 +10.14 NASDAQ -1.99 SP500 -0.93 NASDAQ Adv/Vol/Dec 1073/817.4 mln/1315 NYSE Adv/Vol/Dec 1330/301.8 mln/1568

1:05 pm : After a choppy start to the session, equities have maintained a narrow range near the unchanged line. This morning's volatility coincided with a Bloomberg TV report which indicated the European Central Bank bond purchase program is said to pledge unlimited, sterilized buying of bonds. However, markets calmed after European Central Bank officials declined to comment, and reports out of Germany suggested Chancellor Angela Merkel would only support the program in the near-term. At midday, the S&P 500 is higher by 0.1%.

The telecom sector got off to a strong start and has maintained its gains into the afternoon. Sprint (S 4.94, +0.14) is higher by 3.0% as it outperforms other holdings within the iShares Dow Jones US Telecom ETF (IYZ 24.43, +0.17). Meanwhile, Verizon (VZ 43.94, +0.24) and Crown Castle International (CCI 63.58, +0.37) are both up near 0.5%.

Industrial stocks lag behind the broader market as Terex (TEX 20.82, -1.04) trades lower by 4.8%. The weakness could be related to a string of disappointing data out of the Asia-Pacific region. Elsewhere, M/I Homes (MHO 18.03, -1.52) is down 7.8% following the announcement of a proposed public offering of convertible senior subordinated notes due 2017 with a $50 million aggregate principal amount. The company also announced the proposed concurrent public offering of 2.2 million of its common shares as it tries to raise cash for land acquisition.

The Dow Jones Transportation Average is continuing its recent streak of underperformance; however, individual components within the group are showing significant divergence. Shares of major airlines are seeing a relatively strong bid as United Continental Holdings (UAL 19.02, +0.92) leads the major carriers, up 5.1%. Delta Air Lines (DAL 8.89, +0.33) is higher by 3.8% after announcing August consolidated passenger unit revenue increased by 4.0% on a year-over-year basis. Meanwhile, companies specializing in logistics are slipping after FedEx (FDX 86.48, -1.06) lowered its first quarter guidance, citing weaker global demand. FedEx is down 1.2% while UPS (UPS 72.30, -1.40) is sliding 1.9% and Con-way (30.32, -0.83) trades lower by 2.7%.

Producer of seismic monitoring equipment, OYO Geospace (OYOG 107.47, +13.68) is surging 14.5% after signing a letter of intent to provide 600 kilometers of seabed seismic monitoring system to Statoil (STO 25.22, -0.26). The system will be deployed on the Snorre and Grane fields on the Norwegian continental shelf. OYO's peer ION Geophysical (IO 6.94, +0.16) is higher by 2.4%.

Nokia (NOK 2.52, -0.31) is sliding 11.0% after the company unveiled its new Lumia 920 phone which features an improved camera and wireless charging capabilities. The phone is based on the Windows operating system, developed by Microsoft (MSFT 30.41, +0.03).

Productivity data for the second quarter showed an increase of 2.2%, which was an improvement over the 1.6% increase that had been reported in the preliminary reading. It is also better than the 1.8% increase that had been broadly expected. Unit labor costs for the first quarter were revised lower to reflect a 1.5% increase after they had reportedly increased by 1.7% in the preliminary reading. Economists polled by Briefing.com had expected that unit labor costs would tick down in the revised reading to reflect an increase of 1.4%.DJ30 +29.94 NASDAQ +3.58 SP500 +1.38 NASDAQ Adv/Vol/Dec 1158/757.8 mln/1217 NYSE Adv/Vol/Dec 1435/280.2 mln/1454

12:30 pm : Stocks remain range bound as the S&P 500 continues to hover within two points of its flat line.

Industrial stocks are underperforming the broader market as Terex (TEX 20.94, -0.94) trades lower by 4.3% with the weakness potentially related to a string of disappointing data out of the Asia-Pacific region. Elsewhere, M/I Homes (MHO 18.03, -1.52) is down 7.8% following the announcement of a proposed public offering of convertible senior subordinated notes due 2017 with a $50 million aggregate principal amount. The company also announced the proposed concurrent public offering of 2.2 million of its common shares as it tries to raise cash for land acquisition.DJ30 +34.07 NASDAQ +3.60 SP500 +1.91 NASDAQ Adv/Vol/Dec 1151/684.5 mln/1209 NYSE Adv/Vol/Dec 1471/256.1 mln/1405

12:00 pm : Stocks are trading near the middle of the day's range with the Dow up 0.3%.

The Dow Jones Transportation Average is continuing its recent streak of underperformance. However, individual components within the group are showing significant divergence. Shares of major airlines are seeing a relatively strong bid as United Continental Holdings (UAL 18.91, +0.81) leads the major carriers, up 4.5%. Delta Air Lines (DAL 8.84, +0.28) is higher by 3.3% after announcing August consolidated passenger unit revenue increased by 4.0% on a year-over-year basis.

Meanwhile, companies specializing in logistics are slipping after FedEx (FDX 86.48, -1.06) lowered its first quarter guidance citing weaker global demand. FedEx is down 1.2% while UPS (UPS 72.39, -1.31) is sliding 1.8% and Con-way (30.32, -0.83) trades lower by 2.7%.DJ30 +31.23 NASDAQ +0.64 SP500 +1.07 NASDAQ Adv/Vol/Dec 1092/612.3 mln/1241 NYSE Adv/Vol/Dec 1402/232.5 mln/1474

11:30 am : As European markets close, U.S. equities continue to trade near their respective flat lines.

Producer of seismic monitoring equipment, OYO Geospace (OYOG 107.40, +13.65) is surging 14.5% after signing a letter of intent to provide 600 kilometers of seabed seismic monitoring system to Statoil (STO 25.31, -0.18). The system will be deployed on the Snorre and Grane fields on the Norwegian continental shelf. OYO's peer ION Geophysical (IO 6.96, +0.18) is higher by 2.7%.DJ30 +36.23 NASDAQ +1.90 SP500 +1.39 NASDAQ Adv/Vol/Dec 1110/538.6 mln/1198 NYSE Adv/Vol/Dec 1391/208.8 mln/1457

11:00 am : The major averages continue to hover near their respective unchanged lines after enduring a choppy start to the session.

Nokia (NOK 2.52, -0.31) is sliding 11.0% as the company unveils its new "Lumia 920" phone which features an improved camera and wireless charging capabilities. The phone is based on the Windows operating system, developed by Microsoft (MSFT 30.35, -0.03).DJ30 +8.90 NASDAQ -7.24 SP500 -1.68 NASDAQ Adv/Vol/Dec 1000/447.3 mln/1273 NYSE Adv/Vol/Dec 1226/178.5 mln/1595

10:35 am : The dollar index continued to sell off and fell into negative territory 8am EST, which gave select commodities a boost.

Oil, however, almost an hour ago tanked by well over $1/barrel, falling to a new session low of $94.26/barrel, despite the dollar index sitting in negative territory. Crude has since been inching higher and is now -0.7% at $94.60/barrel.

Natural gas has been in the red all morning, excluding a brief moment, and is now -0.8% at $2.83/MMBtu.

In the precious metals space, Dec gold has been chopping around just under the unchanged line, while silver has been underperforming. Silver declined as low as $32/oz, but didn't fall through that level and has since erased most of today's losses so far. Dec gold is now back at the flat line, now at $1695.60/oz, while Dec silver is -0.3% at $32.32/oz.DJ30 +43.85 NASDAQ +4.63 SP500 +2.36 NASDAQ Adv/Vol/Dec 1167/341.2 mln/1051 NYSE Adv/Vol/Dec 1482/146 mln/1286

10:05 am : After stumbling out of the gate, the major indices have returned to their respective flat lines. The Dow outperforms slightly, up 0.2%.

Shares within the telecom space are in the early lead with Sprint (S 4.93, +0.13) higher by 2.6%. The stock is outperforming other holdings within the iShares Dow Jones US Telecom ETF (IYZ 24.35, +0.09) which is firmer by 0.6%. Meanwhile, Verizon (VZ 43.92, +0.22) is up 0.5%.DJ30 +16.03 NASDAQ -0.12 SP500 +0.08 NASDAQ Adv/Vol/Dec 958/208.4 mln/1229 NYSE Adv/Vol/Dec 1272/97.9 mln/1430

09:45 am : Equities were unable to hold above the flat line as the three major indices slipped into the red. The S&P 500 is lower by 0.2%.

Looking at the early sector performance, telecom stocks are managing to stay positive while industrials and technology lag.

Pep Boys (PBY 9.43, +0.44) is up 4.9% after reporting in-line revenues and earnings of $0.61 per share. The company also announced the appointment of David Stern as Executive Vice President and Chief Financial Officer.DJ30 -16.57 NASDAQ -11.40 SP500 -3.41 NASDAQ Adv/Vol/Dec 774/125.3 mln/1356 NYSE Adv/Vol/Dec 977/70.9 mln/1630

09:17 am : [BRIEFING.COM] S&P futures vs fair value: +0.80. Nasdaq futures vs fair value: -2.50. Heading into the open, equity futures are pointing to a flattish start to the session.

Looking at pre-market movers, Facebook (FB 18.24, +0.51) is higher by 2.9% after announcing Chief Executive Officer, Mark Zuckerberg, has no intention to sell any shares for at least twelve months. Meanwhile, Jefferies initiated coverage of the stock with a ‘buy' rating and a $30.00 price target.

Safeway (SWY 17.20, +1.38) is up 8.7% after announcing plans to file a registration statement for an initial public offering of a minority ownership stake in Blackhawk Network Holdings.

09:02 am : [BRIEFING.COM] S&P futures vs fair value: +1.80. Nasdaq futures vs fair value: -0.50. U.S. futures have erased most of their pre-market losses as they now point to a flattish open.

European markets are mixed as Germany's Services PMI figure was in-line with expectations. Meanwhile, France reported a miss on its Services PMI (49.2 versus 50.2 expected), which helped drag down the Eurozone reading under expectations. Elsewhere, Germany's Christian Democratic Party Leader Michael Fuchs warned that excessive bond buying by the European Central Bank could be inflationary and that Greece can be assisted if ‘she does her homework.' In addition, news headlines from Bloomberg TV indicated the European Central Bank bond purchase program is said to pledge unlimited, sterilized buying of bonds. However, the Central Bank declined to comment on the report. Finally, the German Bund auction failed to attract the expected $5 billion euro in bids.

Germany's DAX is up 0.5% as consumer names lead the way with Merck and Henkel both higher by 1.9%. Industrial and material stocks are weighing on the index as Deutsche Post is down 1.8%, while steelmaker ThyssenKrupp is lower by 1.3%.

In France, the CAC is higher by 0.3% as technology and communications stocks show weakness. STMicroelectronics is sliding 4.0%, while Alcatel-Lucent is down 2.7%. Industrial names are pushing higher with Legrand and Safran up 2.7% and 1.1%, respectively.

In the UK, the FTSE is down 0.2% as mining stocks extend their slide. Kazakhmys and Eurasian Natural Resources are down between 1.5% and 3.0%. BP is off by 3.6% after court filings showed United States Department of Justice will pursue charges for BP's role in the Deepwater Horizon oil spill. Building material distributor, Wolseley, is the day's top performer, up 2.9%.

It was a sea of red across Asia as all of the major averages finished in negative territory. Negative data continued to flow out of the region as China's HSBC Services PMI slipped to a one-year low of 52.0, and Australia's GDP missed estimates (0.6% quarter-over-quarter actual v. 0.8% expected). Australia's disappointing GDP number points to a continued slowdown in the region as weaker Chinese demand for Australian commodities weighs. The Bank of Thailand held its benchmark interest rate steady at 3.00% in a split vote as a couple members called for a cut. Also out were India's HSBC Services PMI (55.0 actual versus 54.2 expected) and Australia's AIG Services Index (42.4 actual versus 46.5 previous).

In Japan, the Nikkei slipped 1.1% to finish near its worst level in five weeks. Names with exposure to China were under pressure as construction machinery makers Komatsu and Hitachi Construction Machinery both lost close to 3.5%. Auto stocks slipped despite the strong U.S. sales as Toyota Motor and Honda Motor both shed roughly 1.0%.

In Hong Kong, the Hang Seng finished lower by 1.5% amid a broad-based decline. Exporter Li & Fung fell 2.2% while Citic Pacific declined 2.8%. Elsewhere, PC maker Lenovo plunged 5.6% following word that Japan-based NEC Corp. was selling its stake in the company.

China's Shanghai Composite slipped 0.3% with trade sliding to its lowest level since February 2009. Construction-related names were in the crosshairs as machinery maker Sany Heavy lost 3.7% and steelmaker Angang Steel shed 2.0%.

08:34 am : [BRIEFING.COM] S&P futures vs fair value: -0.20. Nasdaq futures vs fair value: -4.50. During the last 30 minutes, S&P futures spiked five points before promptly giving back their gains. The surge coincided with news headlines from Bloomberg TV that indicated the ECB bond purchase program is said to pledge unlimited, sterilized buying of bonds.

Productivity data for the second quarter showed an increase of 2.2%, which is a better than the 1.6% increase that had been reported in the preliminary reading. It is also better than the 1.8% increase that had been broadly expected. Unit labor costs for the first quarter were revised lower to reflect a 1.5% increase after they had reportedly increased by 1.7% in the preliminary reading. Economists polled by Briefing.com had expected that unit labor costs would tick down in the revised reading to reflect an increase of 1.4%.

08:00 am : S&P futures vs fair value: -3.10. Nasdaq futures vs fair value: -8.80. U.S. equity futures are pointing to a modestly lower start to the session, following lowered guidance from FedEx (FDX 85.05, -2.49) and mixed trading overseas. S&P futures are currently down 0.4%.

Overnight, Asian markets finished in the red, while European indices are mixed. The Asian markets were faced with disappointing data which showed modest misses on some key regional points. Australia's second quarter GDP growth was reported at 0.6%, ten basis points shy of expectations. China's HSBC Services PMI fell to a one-year low of 52.0, which was also below expectations. Meanwhile, China's Finance Minister indicated he is not optimistic on the current export situation. Another report suggested China's Industrial Production for 2012 could be running behind last year's 13.9% increase.

In Europe, although Germany's Services PMI figure was in-line with expectations, France's big miss on its Services PMI (49.2 versus 50.2 expected), helped drag down the Eurozone reading under expectations. Additionally, markets may have been initially disappointed that the European Central Bank remained mum on its bond buying intentions, after speculation crept into markets late yesterday that the Central Bank could lay out details. Elsewhere, Germany's Christian Democratic Party Leader Michael Fuchs warned that excessive bond buying by the European Central Bank could be inflationary and that Greece can be assisted if ‘she does her homework.' Finally, the German Bund auction failed to attract the expected $5 billion euro in bids. Nearing midday, Germany's DAX is up 0.4%, France's CAC is higher by 0.2%, and UK's FTSE is down 0.4%.

In U.S. corporate news, FedEx (FDX 85.05, -2.49) is down 2.8% after cutting its first quarter outlook. The lower guidance is noteworthy as the shipper serves as a bellwether for overall economic health. Peer UPS (UPS 71.90, -1.80) is down 2.4% in the wake of the guidance cut.

Pluristem (PSTI 4.67, +0.48) is up 11.5% after announcing that the company's stem cell treatment saved the life of a third bone marrow disease patient.

Dollar General (DG 53.00, +2.34) is higher by 4.6% after beating on earnings and reporting in-line revenues.

The MBA Mortgage Index showed a 2.5% decrease in new mortgage applications over the past week. A decrease of 4.3% was expected. The refinance index pointed to a 3.0% decrease which is the lowest level since May.

Nonfarm productivity and unit labor costs will be reported at 8:30 ET.

06:24 am : [BRIEFING.COM] S&P futures vs fair value: -1.00. Nasdaq futures vs fair value: -4.50.

06:23 am : Nikkei...8679.82...-95.70...-1.10%. Hang Seng...19145.07...-284.80...-1.50%.

06:23 am : FTSE...5671.23...-0.80...0.00. DAX...6983.52...+50.70...+0.70%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage