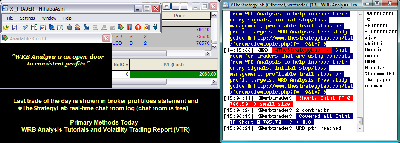

Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

073112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-2060.png [ 78.97 KiB | Viewed 497 times ]

073112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-2060.png [ 78.97 KiB | Viewed 497 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +20.60 points or

$2060 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=106&t=1284.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=163&t=1526 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

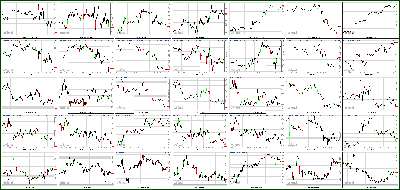

Stocks: Investors Hit Pause Ahead of Fed, ECB Attachment:

073112-Key-Price-Action-Markets.png [ 555.68 KiB | Viewed 479 times ]

073112-Key-Price-Action-Markets.png [ 555.68 KiB | Viewed 479 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- U.S. stocks closed down slightly Tuesday amid another day of cautious trading ahead of meetings by U.S. and European central bankers.

The Dow Jones Industrial Average slipped 64 points, or 0.5%, the S&P 500 lost 6 points, or 0.4%, and the Nasdaq fell 6 points, or 0.2%.

While investors sifted through a handful of encouraging economic reports, they were mostly sitting back and waiting for central bank meetings when they'll find out whether the U.S. Federal Reserve and the European Central Bank will announce new stimulus measures to boost the economy.

"It's hard to believe that someone is going to make any big bets with the possibility of something drastic coming out of either central bank," said Art Hogan, managing director at Lazard Capital Markets.

The Fed's two-day meeting kicked off Tuesday, with an announcement due Wednesday afternoon.

"The Fed has three credible options, and the hope is that one of them comes to fruition," said Hogan. "If we don't get anything, this is a market that will be disappointed. But at the same time, even if they do something, I'm not sure how much will be enough."

* Central banks take center stageThe most likely step the Fed will take is cutting the interest rate the Fed pays on bank reserves from its current 0.25% to zero, following the ECB's decision earlier this month to cut its deposit rate to zero, said Hogan.

The Fed could also extend its plan to keep interest rates near zero beyond its current 2014 forecast, he said.

Hogan said the least likely outcome is a third round of quantitative easing from the Fed.

"Expectations for QE3 at this meeting are very low, but the market will expect hints on future actions," he said. "The market has priced in some type of change in language."

The ECB will take center stage Thursday, when its Governing Council meets in Frankfurt.

* Fear & Greed Index slides into greedAll three indexes ended July with mild gains. The Dow saw a 1% uptick, the S&P 500 posted a 1.3% increase and the Nasdaq ended the month with a 0.15% rise.

World markets: European markets closed mixed. Britain's FTSE 100 slid 0.8% and CAC 40 dropped 0.5%, while the DAX in Germany rose 0.2%.

The unemployment rate for the 17-nation eurozone held steady from the previous month at a record 11.2% in June, according to Eurostat, the European Union's statistical office. In the broader 27 nations that make up the EU, the unemployment rate in June remained at 10.4% -- unchanged from May.

Eurostat also said that inflation was unchanged in July, at 2.4%.

Asian markets ended mixed. The Shanghai Composite lost 0.3%, while the Hang Seng in Hong Kong gained 1.1% and Japan's Nikkei rose 0.7%.

Economy: Personal income rose 0.5% in June, while spending remained unchanged, according to a government report. Economists surveyed by Briefing.com expected a 0.4% increase in income and a 0.1% rise in spending.

In a sign of a U.S. housing rebound, home prices in 20 major cities rose 2.2% in May, according to the S&P/Case-Shiller index. Economists were forecasting a 1.8% drop in prices in May, following a 1.9% decline in the previous month.

The Chicago PMI, a regional reading on manufacturing activity, rose to 53.7 in July from 52.9 the prior month. Economists were expecting the index to slip to 52.5 during the month.

Consumer confidence rose in July. The Conference Board's index rose to 65.9 from 62.7 in June. Economists were expecting the reading to decline slightly to 61.

Companies: Coach (COH) shares tumbled after the retailer reported revenue that fell short of forecasts. Of particular concern is the fact that Coach pointed to sluggishness in North America.

* UBS lost $356 million on Facebook, suing Nasdaq for itUBS (UBS) said its second-quarter profit tumbled 58% from a year earlier due to lower trading revenue and losses from the botched Facebook (FB) IPO.

Deutsche Bank (DB) said its second-quarter profit dropped 44% and revenue declined 6% as Europe's sovereign debt crisis weighs on investor confidence and client activity across the bank. The bank said it is cutting 1,900 jobs, mostly outside of Germany, in an effort to save €350 million, sending the stock higher.

Oil producer BP (BP) reported a loss of $1.4 billion for the second quarter, sending shares sharply lower. The company wrote down the value of $5 billion worth of assets, including U.S. refineries and shale gas assets, and had continued costs related to the Gulf of Mexico oil spill.

* Drought strains U.S. oil productionShares of Pfizer (PFE, Fortune 500) rose after the drug maker beat earnings and revenue expectations.

Humana (HUM, Fortune 500) shares sank after the health insurer reported a drop in second-quarter profit and lowered its full-year profit outlook.

United States Steel's (X, Fortune 500) stock jumped after the company's earnings and revenue topped expectations.

Shares of Apple (AAPL, Fortune 500) climbed after an analyst at Bernstein Research said the company is considering a stock split, a move that could prompt it to be added to the Dow Jones Industrial Average.

* Corn prices hit record as crops shrivelCurrencies and commodities: The dollar fell against the euro and the Japanese yen, but gained ground versus the British pound.

Oil for September delivery fell $2.18 to $87.60 a barrel.

Gold futures for August delivery lost $9.20 to $1,610.50 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury edged lower, pushing the yield up to 1.49% from 1.50% late Monday.

Market Update

Market Update 4:15 pm : Stocks remained in a tight range throughout the day before settling on their session lows. Market action was similar to that observed yesterday as the major indices hovered around their respective unchanged levels for most of the session. Low volume and in-line economic data contributed to an uneventful session as investors await tomorrow's comments from the Federal Reserve and Thursday's European Central Bank rate decision.

Personal income increased by 0.5% in June, which was slightly greater than the 0.4% expected increase. Personal spending was unchanged, instead of increasing by 0.1% as had been broadly anticipated. Core personal consumption expenditures ticked up 0.2% month over month, in-line with expectations. Additionally, consumer confidence came in at 65.9 on expectations of a 61.0 reading.

Summer vacations and the on-going Olympics are some of the possible reasons for today's lackluster market action. Weak volume headlined the day before late-day selling pushed the total number of traded shares closer to the 50-day average.

As equities traded without direction, the dollar index ended down 0.2%. At 1.2305, the euro maintained its 0.4% advance versus the dollar after choppy morning trade.

Fueled by a positive earnings surprise and better-than-expected revenue growth, United States Steel (X 20.65, +1.73) was one of the day's best performers, finishing up 9%.

Energy was the worst performing sector today. Down 5%, Nabors Industries (NBR 13.84, -0.74) was the main laggard. Today's sell-off coincided with the stock testing $14.60 resistance which has held for the past six months.

With more than 100 companies set to report earnings after hours, competitors Electronic Arts (EA 11.02, -0.21) and Take-Two Interactive (TTWO 8.78, -0.35) bear watching. EA has been stuck in a downtrend throughout the year. At $11, the stock is testing lows not seen since 1999. Take-Two has also been slumping, albeit not as severely as EA. The current $9 level has provided strong support for the stock during the past three years.

Frontier Communications (FTR 3.92, +0.21) will also report earnings after the bell. The company's shares started the day flat but managed to build up a 5.7% advance over the course of the session. The consensus estimate calls for earnings of $0.06 per share on revenue of $1.24 billion.

In addition to tomorrow's results of the FOMC meeting scheduled for 2:15 PM ET, ADP Employment Change will be reported at 8:15 AM ET and will be followed by the ISM Index and construction spending at 10 AM ET.DJ30 -64.33 NASDAQ -6.32 SP500 -5.98 NASDAQ Adv/Vol/Dec 1022/1.73 bln/1466 NYSE Adv/Vol/Dec 1234/887.9 mln/1779

3:35 pm : Crude oil extended yesterday's losses following numerous European headlines and U.S. economic data. Weakness also came ahead of tomorrow's policy directive from The Federal Reserve. It came off its pit session high of $90.11 per barrel and plummeted into negative territory moments after floor trade opened. It touched a session low of $87.52 per barrel before it consolidated and closed with a 1.9% loss at $88.07 per barrel.

Natural gas traded up to a floor session high of $3.28 per MMBtu in morning action but lost momentum. It fell into negative territory to a session low of $3.16 per MMBtu. However, buyers stepped in during afternoon action and helped push prices higher. Natural gas erased the entire loss and managed to book a 0.3% gain as it closed at $3.22 per MMBtu.

Precious metals followed in crude's footsteps and fell into negative territory despite a weaker dollar. Gold slid off its pit session high of $1631.60 per ounce and brushed a session low of $1614.20 per ounce moments before pit close. It settled at $1615.40 per ounce, or 0.5% lower, after volatile and choppy trading. Silver was also unable to stay above the break-even level and moved into the red in afternoon action. It settled with a 0.4% loss at $27.90 per ounce, just above its session low of $27.86 per ounce.DJ30 -35.88 NASDAQ -1.96 SP500 -3.74 NASDAQ Adv/Vol/Dec 1132/1423.7 mln/1329 NYSE Adv/Vol/Dec 1309/507 mln/1672

3:00 pm : Heading into the final hour of trading, equities continue to bounce around their respective unchanged levels. The Nasdaq has managed to stay positive for the majority of the session, but its gains have been limited to just 0.2%.

Frontier Communications (FTR 3.95, +0.24) will report earnings after the bell. The company's stock started the day flat, but has managed to build up a 6.5% advance over the course of the session. The consensus estimate calls for earnings of $0.06 per share on revenue of $1.24 billion.DJ30 -31.79 NASDAQ +0.17 SP500 -3.15 NASDAQ Adv/Vol/Dec 1132/1.23 bln/1315 NYSE Adv/Vol/Dec 1337/440.2 mln/1630

2:30 pm : Mired in low volume, stocks make yet another push to come off their session lows. The S&P 500 has trimmed half of its losses, and is currently down 0.1%.

With more than 100 companies set to report earnings after hours, competitors Electronic Arts (EA 11.14, -0.09) and Take-Two Interactive (TTWO 8.98, -0.15) bear watching. EA has been stuck in a downtrend throughout the year. At $11, the stock is testing lows not seen since 1999. Take-Two has also been slumping, albeit not as severely as EA. The current $9 level has provided strong support for the stock during the past three years.DJ30 -9.99 NASDAQ +5.14 SP500 -0.97 NASDAQ Adv/Vol/Dec 1171/1.14 bln/1281 NYSE Adv/Vol/Dec 1348/404.1 mln/1605

2:00 pm : Equities are making further attempts to push off session lows. The S&P 500 and Dow are maintaining their slim 0.3% losses.

Weak volume continues to be the story of the day. With 370 million shares traded so far, total volume is on pace for one of the slowest days of the year.

After yesterday's total fell nearly 20% short of the 50-day moving average, today's session is poised for similar results.

Summer vacations and the on-going Olympics are some of the possible reasons for lackluster market action. Additionally, investors are anticipating Wednesday's FOMC statement along with a European Central Bank rate decision on Thursday.DJ30 -40.87 NASDAQ -0.67 SP500 -4.27 NASDAQ Adv/Vol/Dec 1084/1.04 bln/1355 NYSE Adv/Vol/Dec 1212/370.1 mln/1711

1:30 pm : The main indices hold just above session lows. The S&P 500 and the Dow are posting declines of 0.3% each while the Nasdaq remains flat.

As equities continue trading without direction, the dollar index is 0.2% lower. At 1.2310, the euro is maintaining its 0.4% advance versus the greenback after a choppy morning trade.DJ30 -28.69 NASDAQ +2.20 SP500 -2.75 NASDAQ Adv/Vol/Dec 1129/969.1 mln/1290 NYSE Adv/Vol/Dec 1247/345.3 mln/1675

1:05 pm : At midday, equities hold near their respective session lows. The three indices were essentially unchanged for the majority of the day until selling pressure pushed the S&P 500 down to the 1,381 area.

Despite a slew of earnings and a full slate of economic data, markets have been unable to make a considerable push in either direction.

Personal income increased in June by 0.5%, which is slightly greater than the 0.4% increase that had been widely expected while personal spending was unchanged, instead of increasing by 0.1% as had been broadly anticipated. Core personal consumption expenditures were up 0.2% month over month, in-line with expectations. Additionally, consumer confidence came in at 65.9 on expectations of a 61.0 reading.

A few bright spots are present in the materials and heavy machinery sectors.

United States Steel (X 20.41, +1.49) is one of the day's best performers, currently up 8%. The company reported a positive earnings surprise along with better-than-expected revenue growth.

Engine maker Cummins (CMI 96.69, +6.21) is 7% higher following an earnings beat combined with a revenue miss. Three weeks ago, the company reduced their second quarter earnings expectations thus priming the market for a less optimistic report.

The consumer discretionary sector is notably lower today. Shares of Coach (COH 50.00, -10.58) are down 17% in light of lower guidance issued by the company.

The poor outlook from the company is spilling over to other sector components, sending Tiffany & Co. (TIF 54.75, -2.46) 4.3% lower.

Energy remains one of the worst performing sectors today. Down 4.7%, Nabors Industries (NBR 13.89, -0.69) is the main laggard. Today's sell-off comes as the stock was testing $14.60 resistance which has held for the past six months.DJ30 -46.43 NASDAQ -5.55 SP500 -5.14 NASDAQ Adv/Vol/Dec 1020/903.1 mln/1395 NYSE Adv/Vol/Dec 1140/321.5 mln/1760

12:30 pm : After staying range bound throughout morning trade, markets have turned down and marked fresh session lows. The biggest drop can be seen in the S&P 500 which is down 0.3% while the Nasdaq is now 0.1% in the red.

Energy remains as one of the worst performing sectors today. Down 4%, Nabors Industries (NBR 13.98, -0.60) is the main laggard of the sector. Today's sell-off comes as the stock was testing resistance around $14.60 which has held for the past six months.DJ30 -39.92 NASDAQ -1.50 SP500 -4.10 NASDAQ Adv/Vol/Dec 1129/819.6 mln/1265 NYSE Adv/Vol/Dec 1216/288.2 mln/1650

12:00 pm : Following the European close, markets have been unable to break out of their range. The Nasdaq is the only index which has managed to stay positive, although its gains are limited to 0.3%.

United States Steel (X 21.10, +2.18) is one of the day's best performers, currently up 12%. The company reported a positive earnings surprise along with a better-than-expected revenue growth. In addition, the company declared a dividend of five cents per share.

Engine maker Cummins (CMI 97.61, +7.13) is 7.9% higher following an earnings beat combined with a revenue miss. Three weeks ago, the company reduced their second quarter earnings expectations thus priming the market for a less optimistic report.DJ30 -7.08 NASDAQ +7.52 SP500 -0.13 NASDAQ Adv/Vol/Dec 1313/710.1 mln/1056 NYSE Adv/Vol/Dec 1457/254.3 mln/1413

11:30 am : As European markets close, U.S. indices are attempting to break the tight range which they have been constrained to since yesterday. The Nasdaq has been the most resilient, up 0.4%.

The euro has seen volatile trading through the early part of the session. The single currency spiked to 1.2310 following supportive comments from French President Francois Hollande. However, a subsequent CNBC report indicated that a Bundesbank source said monetary policy should focus strictly on the mandate of price stability, and that problems facing some states are fiscal, which should be addressed with fiscal tools such as the EFSF. Following the headlines, the euro dropped back to 1.2275.

Heading into the European close, the euro pulled up to a session high near the 1.2330 level.DJ30 +4.62 NASDAQ +11.64 SP500 +1.40 NASDAQ Adv/Vol/Dec 1326/616.7 mln/1001 NYSE Adv/Vol/Dec 1538/222.1 mln/1285

11:00 am : Flat trading continues across the major indices. The S&P 500 is hovering within a narrow five point range around the unchanged level.

The consumer discretionary sector is the worst performing S&P 500 component so far today. Shares of Coach (COH 50.77, -9.81) are down 16% in light of lower guidance issued by the company.

The poor outlook from the company is spilling over to other sector components, sending Tiffany & Co. (TIF 55.31, -1.89) 3.3% lower.DJ30 -10.75 NASDAQ +6.21 SP500 -0.62 NASDAQ Adv/Vol/Dec 1215/503.1 mln/1056 NYSE Adv/Vol/Dec 1433/187.2 mln/1358

10:35 am : Recent Europe headlines send the euro lower and most commodities lower as well.

In energy today, Sept crude oil sold off sharply this morning and fell as low as $88.35. This came just ahead of the beginning of floor trading, and is down almost $2/barrel off its session high now, hit earlier this morning. Crude is now -1.3% at $88.63/barrel.

Sept natural gas is back near the unchanged line after recovering from its sell off earlier this morning, which sent the energy component as low as $3.17. Nat gas is now +0.4% at $3.23/MMBtu.

Metals: August gold and Sept silver also sold off in recent activity, hitting new session lows (Gold $1620.20, Silver $27.97) July copper is trading higher this morning, now up 0.3% at $3.43/lb.

In ag, in overnight trading, December (and continuous contract) corn futures rose to a new all-time high of $8.20/bushel as drought conditions continue to be an issue. Also, this follows the USDA weekly crop progress report, which came out at 4pm ET yesterday, which showed further deterioration (Corn is good to excellent condition fell to 24% from 26%). Since June 15, corn is trading 62% higher.

10:00 am : Choppy trading continues during the first half-hour of the session. The Nasdaq is staying slightly positive, up 0.1% while the Dow and the S&P 500 are both down nearly 0.2%.

The July Chicago PMI of 53.7 surprised to the upside as economists had generally expected a reading of 52.5 to follow the prior month's 52.9.

Additionally, consumer confidence came in at 65.9 while economists expected a reading of 61.0. Today's reading is the best since April of this year.DJ30 -13.09 NASDAQ +6.93 SP500 -0.02 NASDAQ Adv/Vol/Dec 1207/226.3 mln/945 NYSE Adv/Vol/Dec 1488/97.9 mln/1212

09:45 am : The first minutes of the session are seeing mixed trading. The Nasdaq is staying slightly positive, up 0.4% while the Dow and the S&P 500 are hovering near unchanged territory.

The erratic moves in pre-market futures have been dictated by headlines out of Europe, with several German officials putting a damper on recent hopes for further monetary easing.

Cirrus Logic (CRUS 36.25, +6.41) is up 22% after mixed quarterly results and increasing guidance above consensus.DJ30 -14.15 NASDAQ +13.04 SP500 +0.50 NASDAQ Adv/Vol/Dec 1206/133.1 mln/882 NYSE Adv/Vol/Dec 1557/69.4 mln/1095

09:15 am : S&P futures vs fair value: -0.90. Nasdaq futures vs fair value: +5.50. U.S. futures are currently pointing to a flattish open, near the lows of the morning.

The euro initially spiked to highs near 1.2300 on comments from French President Hollande in support of defending the euro. However, a subsequent CNBC report indicated that a Bundesbank source said monetary policy should focus strictly on the mandate of price stability, and that problems facing some states are fiscal, which should be addressed with fiscal tools such as the EFSF, if necessary. Following the headlines, the euro dropped back to 1.2275.

09:04 am : [BRIEFING.COM] S&P futures vs fair value: +1.40. Nasdaq futures vs fair value: +6.80. Futures continue to point to a higher open. The euro has just risen to highs on the heels of comments from French President Hollande in support of defending the currency.

While the Fed is the biggest item of interest over the next two days, there is a heavy flow of earnings reports to digest in the interim. There have been a number of notable reports since yesterday's close.

British Petroleum (BP 39.99 -1.83) missed on earnings but saw revenues above expectations. As a result, the stock is down more than 4% in pre-market trading.

Pfizer (PFE 23.95 +0.24) is advancing nearly 1% in pre-market action following a positive earnings report. The pharmaceutical producer beat on revenues and earnings per share.

Seagate Technology (STX 28.00, -2.43) is over 8% down after reporting lower-than-expected earnings and revenues.

Coach (COH 51.10, -9.48) shares are down 14% after the company beat by a penny in Q4 (Jun) on in-line rev of $1.16 billion.

Archer-Daniels Midland (ADM 26.00, -1.49) is down 5% after it missed the EPS consensus by $0.23, despite stronger-than-expected rev of $22.7 billion.

The Case-Shiller 20-city Home Price Index slid 0.7% when a 1.8% decline had been generally expected.

The Chicago PMI is set for release at 9:45 AM ET, followed by consumer confidence at 10 AM ET.

08:30 am : S&P futures vs fair value: +2.30. Nasdaq futures vs fair value: +8.30. U.S. futures are pointing slightly higher with Nasdaq futures indicating an advance of 0.3% at the open.

Asian markets ended Tuesday mixed. Following the close, reports came out indicating further easing being considered by Chinese authorities. With the inflation rate likely below 2%, the PBOC sees more room for action.

European markets continue trading mixed as the euro is up 0.25% versus the dollar. It currently trades near 1.2290.

Personal income increased in June by 0.5%, which is slightly greater than the 0.4% increase that had been widely expected. Personal spending was unchanged, instead of increasing by 0.1% as had been broadly anticipated. Core personal consumption expenditures were up 0.2% month over month, in-line with expectations.

As for the first quarter Employment Cost Index, it increased by 0.5%, which matches the 0.5% increase that was widely forecasted.

The Case-Shiller 20-city Home Price Index will be reported at 9 AM ET, the Chicago PMI will be released at 9:45 AM ET, and consumer confidence report is scheduled for 10 AM ET.

08:00 am : [BRIEFING.COM] S&P futures vs fair value: +3.20. Nasdaq futures vs fair value: +9.00. European markets are mixed this morning as the recent rally appears to be slowing down. Britain's FTSE is down 0.4% while Germany's DAX is up nearly 0.5%. Italy's MIB and Spain's IBEX are managing to stay positive, both up roughly 0.7%. Even though Italy's MIB is staying positive, the mid cap component of the index is firmly in the red, down over 6%.

Spanish and Italian 10-yr yields decreased slightly to levels near 6.5% and 6% respectively.

Today's European economic data was mixed with no major surprises. German retail sales posted a 2.9% advance over last year when a 0.4% rise was expected. However, Spanish retail sales contracted by 5.2% when a more severe 7.7% contraction was anticipated.

The German unemployment rate maintained its 6.8% level while Italian unemployment rose to 10.8% from a previous 10.6%.

The unemployment for the Eurozone remained at 11.2%. At 2.4%, Consumer Price Index was also stable.

Deutsche Bank (DB) delivered a disappointing earnings report. The financial giant saw its profits decline by 63% during the second quarter. The firm attributed losses to the ongoing debt crisis as well as euro weakness compared to the dollar and the British pound.

In addition to corporate earnings, U.S. investors will be looking to a full slate of economic data set for release.

Personal income and spending will be released at 8:30 AM ET. In addition, the Case-Shiller 20-city Index will be reported at 9 AM ET. Finally, the Chicago PMI and consumer confidence will hit the wires at 9:45 AM ET and 10 AM ET respectively.

Tuesday is also the first day of the FOMC meeting. The Committee will release its statement on Wednesday at 2:15 PM.

Futures are currently pointing to a moderately higher open with Nasdaq futures leading the way, up 0.3%.

06:45 am : S&P futures vs fair value: +3.0... Nasdaq futures vs fair value: +7.50.

06:43 am : Nikkei...8695.06...+59.60...+0.70%. Hang Seng...19796.81...+211.40...+1.10%.

06:43 am : FTSE...5685.42...-8.20...-0.20%. DAX...6809.35...+35.30...+0.50%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage