Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

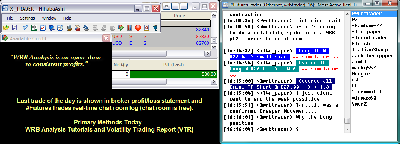

033012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-530.png [ 75.92 KiB | Viewed 502 times ]

033012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-530.png [ 75.92 KiB | Viewed 502 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +5.30 points or

$530 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. You can read

today's #FuturesTrades trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=102&t=1181.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=150&t=1403 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

Stocks End Spectacular Quarter Attachment:

033012-Key-Price-Action-Markets.png [ 531.47 KiB | Viewed 497 times ]

033012-Key-Price-Action-Markets.png [ 531.47 KiB | Viewed 497 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- U.S. stocks closed mixed Friday, with the Dow and S&P 500 ending their best first quarter in over a decade, as investors weighed a report on consumer spending and a boost in the eurozone bailout fund.

The Dow Jones industrial average (INDU) gained 66 points, or 0.5%, to end at 13,212. The S&P 500 (SPX) added 5 points, or 0.4%, to 1.408. The Nasdaq (COMP) edged down 4 points, or 0.1%, to 3,090.

Friday's gains capped a stellar three months for stocks, with the Dow and S&P posting the biggest first-quarter gain since 1998. Despite Friday's decline, the Nasdaq had its best first quarter since 1991, according to the Stock Trader's Almanac.

For the quarter, the Dow gained 8.1%, the S&P 500 advanced 12% and the Nasdaq rose a whopping 19% since New Year's Day.

The Dow and S&P 500 are at their highest levels since 2008, while the Nasdaq is at its highest point since 2000.

The gains were driven by improving economic data in the United States and easing concerns about the debt crisis in Europe. Stocks have also been supported by expectations the Federal Reserve will continue to support the economy.

"That's been enough to put the risk back on in the first part of this year versus last year," said Peter Tuz, a portfolio manager at Chase Investment Counsel in Charlottesville, Va.

On Friday, stocks opened higher as investors focused on personal spending data and news that eurozone finance officials agreed to raise their financial firewall to €700 billion.

* The highest earning hedge fund manager is...But the market wavered as the morning progressed, with shares of Apple weighing on the Nasdaq, said Ben Schwartz, chief market strategist at Lightspeed Financial.

Apple (AAPL, Fortune 500) has had an outsize impact on the market this quarter. The stock has driven roughly 15% of the S&P 500's performance so far this year, according to Barclays Capital.

Other top performers this quarter include Sears Holdings (SHLD, Fortune 500), Bank of America (BAC, Fortune 500) and Netflix (NFLX). The main laggards were Apollo Group, (APOL, Fortune 500) Supervalue (SVU, Fortune 500) and FirstSolar (FSLR).

Schwartz said the market is becoming more volatile as investors gear up for corporate reports due out later next month. But he suggested that stocks could find some support as the recent rally draws so-called retail investors off the sidelines.

"You're starting to see the market move a bit," he said. "But we're waiting for more volume to come in to support the rally we had over last three months."

Meanwhile, traders said institutional investors have been making big moves recently as they rebalance portfolios ahead of quarterly statements to clients.

"Hedge fund and mutual fund managers have used the last two weeks to get their portfolios competitive," said Quincy Krosby, market strategist with Prudential Financial in Newark, N.J. "This is a quarter in which you did not want to be lagging the market performance."

U.S. stocks bounced around Thursday and ended little changed. Both the S&P 500 and the Nasdaq closed in the red for the third straight day, while the Dow broke a two-day losing streak.

Economy: A report released before the opening bell showed that personal spending increased 0.8% in February, topping analyst predictions of a 0.6% jump.

Meanwhile, personal income grew by 0.2%, less than the 0.3% predicted rate.

The Chicago Purchasing Managers' Index for March fell to 62.2, down from 64 in February and below expectations of 63. Any reading above 50 indicates expansion.

The March edition of the University of Michigan Consumer Sentiment Index rose to 76.2, from 74.3 in February. Analysts were expecting the index to remain flat.

* Video - First quarter gains, thanks to the FedCompanies: Shares of Apple were slightly lower a day after a heavily anticipated report on working conditions at supplier Foxconn's China facilities was released. The report documents dozens of major labor-rights violations, including excessive overtime, unpaid wages and salaries that aren't enough to cover basic living expenses.

Shares of credit card payment processor Global Payments (GPN) fell 9% after the company disclosed a major data breach that could involve more than 10 million card numbers.

Representatives from MasterCard (MA, Fortune 500) and Visa (V, Fortune 500) confirmed that a breach has potentially compromised credit and debit card information from all of the major card brands.

On Friday, retailer Finish Line (FINL) said it earned 81 cents per share last quarter -- a number in line with analyst estimates. The company reported better-than-expected revenue, but shares tumbled.

Research in Motion (RIMM) shares were higher even after the BlackBerry-maker missed expectations on revenues and earnings. The company said it's considering strategic alternatives, and one director left its board.

World markets: European stocks ended modestly higher. Britain's FTSE 100 (UKX) increased 0.4%, the DAX (DAX) in Germany rose 0.6% and France's CAC 40 (CAC40) gained 0.7%.

Eurozone finance ministers agreed to increase the size of the region's capacity for crisis lending to €700 billion.

* Like a bear in a China shopAsian markets ended mixed. The Shanghai Composite (SHCOMP) added 0.5%, while the Hang Seng (HSI) in Hong Kong and Japan's Nikkei (N225) dropped 0.3%.

Currencies and commodities: The dollar lost ground against the euro, the British pound and the Japanese yen.

Oil for May delivery added 24 cents to settle at $103.02 per a barrel.

Gold futures for April delivery rose $17.10 to end the day at $1,669.30 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury dropped, pushing the yield up to 2.17% from 2.16% late Thursday.

Market Update

Market Update 4:30 pm : Broad support on Friday helped the S&P 500 come back after booking three straight declines. The effort helped feed a weekly gain of 0.8%, which stands as the eleventh weekly advance in 13 tries for the S&P 500. That hot streak drove the broad market measure to a 3.1% gain for March -- its fourth straight monthly gain -- and a 12.0% gain for the first quarter. That marks the best quarterly performance for the stock market since 2009 and the best first quarter performance since 1998.

Tech stocks were integral in the stock market's streak of gains, but they were relatively weak today. That hampered the Nasdaq. In fact, Tech fell 0.4% and was the only sector to settle in the red. Despite that, Tech still scored a 1.0% weekly gain, a 5.0% monthly gain, and a 21.1% quarterly gain.

For the second straight day Energy emerged as a leader after a listless start to the session. Energy stocks advanced 0.8% on Friday, but fell 0.5% for the week and 3.4% for the month. The Energy sector was up 3.4% in the first quarter, but that paled in comparison to the 17.6% that it had rallied in the fourth quarter.

Energy's action this week came in close connection to movement in oil prices. Earlier this week oil prices fell to a new monthly low narrowly above $102 per barrel, but it bounced back to $103 per barrel today. As a proxy for oil's action this week, the US Oil Fund (USO 39.23, -0.06) fell 3.6% this week and 4.0% for the month. It advanced 2.9% for the quarter.

Corporate news today was limited in scope and generally without consequence. For the most part economic data was also shrugged off.

Personal income reportedly increased in February by 0.2%, but that is slightly less than the 0.3% increase that had been generally expected. However, personal spending grew by 0.8%, which is faster than the 0.6% increase that had been broadly expected.

The Chicago PMI slipped to 62.2 in March from 64.0 in February. A tick down to 63.0 had been broadly expected.

The final reading on consumer sentiment in March from the University of Michigan improved to 76.2 from the preliminary reading of 74.3, which is where economists polled by Briefing.com had generally expected the reading to remain.

Earlier in the week it was announced that the Conference Board's latest Consumer Confidence Index declined to 70.2 from an upwardly revised 71.6 for the prior month. The decline was on the order of what had been widely anticipated, though.

The latest initial jobless claims count climbed 9,000 week-over-week to 359,000, which is greater than the tally of 350,000 that had been expected, on average, among economists polled by Briefing.com.

Durable goods orders increased by 2.2% during February, but that is actually a slower pace than the 2.8% increase that had been broadly expected. Prior month orders data were revised slightly higher to reflect a 3.6% decline. Excluding transportation items, durable goods orders were up 1.6% in February. That is a stronger clip than the 1.0% increase that had been widely expected, but still relatively underwhelming when compared to loftier estimates that were widely issued. Nonetheless, the latest figure marks an improvement from the prior month decline of 3.0%.

The final reading on fourth quarter GDP continued to show that the economy expanded at a rate of 3.0%, just as had been widely anticipated, but in a separate event Fed Chairman Bernanke seemed to give tacit indication that the Fed recognizes the need for accommodative policies, given that job market conditions remain far from normal. DJ30 +66.22 NASDAQ -3.79 NQ100 -0.1% R2K -0.2% SP400 +0.0% SP500 +5.19 NASDAQ Adv/Vol/Dec 1180/1.79 bln/1365 NYSE Adv/Vol/Dec 1727/966 mln/1254

3:30 pm : The CRB Index booked a 0.8% gain today, but it still finished the week nearly 2% below where it began. For the month the CRB fell more than 4%, but it managed to score a 1.0% gain for the first quarter.

Crude oil trended higher in pit trade, but pulled back about shortly before the close to settle at $103.04 per barrel, which stands as a 3.6% loss from the prior week. The decline is largely due to concerns about softer demand. Highlighting that theme the weekly inventory data released mid-week showed a build of 7.1 million barrels when a build of 2.7 million barrels had been anticipated. With regard to supply issues, headlines earlier today stated that President Obama cleared Iranian sanctions aimed at squeezing oil exports.

Natural gas logged losses every day this week. That left the energy component to settle at $2.13 per MMBtu, which makes for a weekly loss of 6.2%. Earlier this week inventory numbers showed a build of 57 bcf, which exceeded the expected build of 50 bcf.

Precious metals experienced some dramatic swings this week, but both gold and silver ended the week on a positive note with respective weekly gains of 0.4% and 0.6% at $1669.10 per ounce and $32.44 per ounce.

Grains came into focus following the USDA’s grain stocks report, which stated that corn stocks in all positions at the start of March totaled 6.01 billion bushels, down 8% year over year, but that corn planted in 2012 will be 4% higher than in 2011. Corn finished pit trade 6.8% higher at $6.44 per bushel. DJ30 +68.72 NASDAQ +1.20 SP500 +5.92 NASDAQ Adv/Vol/Dec 1340/1.28 bln/1170 NYSE Adv/Vol/Dec 1900/460 mln/1050

3:00 pm : Stocks head into the final hour with a modest gain that has the stock market up nearly 1% for the week -- its eleventh weekly gain in 13 tries. That hot streak has the broad market measure up 12% in the first quarter. While stocks haven't had such a strong quarterly performance since 2009, they haven't had such an impressive first quarter performance since 1998.DJ30 +66.07 NASDAQ +0.77 SP500 +5.84 NASDAQ Adv/Vol/Dec 1385/1.15 bln/1100 NYSE Adv/Vol/Dec 1965/405 mln/990

2:30 pm : Although their collective decline is only fractional, Tech stocks continue to make up the only major sector still stuck in negative territory. Up more than 1% for the week, they've outperformed the broad market in the last five sessions. In fact, the Tech sector hasn't suffered a weekly decline this year. That hot streak has the Tech sector up more than 5% month to date and up more than 20% in the first quarter. That follows a fourth quarter gain of more than 8%.DJ30 +66.4 NASDAQ +3.35 SP500 +6.31 NASDAQ Adv/Vol/Dec 1370/1.05 bln/1095 NYSE Adv/Vol/Dec 1955/370 mln/980

2:00 pm : The S&P 500 has made a modest move higher to set an incrementally improved session high. The Dow is back near its best levels of the day, but the Nasdaq has yet to return to its opening highs.

The greenback gradually improved its position, but it still isn't in positive territory for the day. Its 0.2% loss leaves it positioned for a weekly decline of 0.4%, which would mark its third straight weekly loss. Despite that streak of weakness, the Dollar Index is still up 0.3%. For the quarter, though, it is down 1.5%.

Treasuries continue to trade lower, such that the yield on the 10-year Note is now back at 2.20%. DJ30 +66.03 NASDAQ +5.42 SP500 +6.85 NASDAQ Adv/Vol/Dec 1335/995 mln/1125 NYSE Adv/Vol/Dec 1920/350 mln/1020

1:30 pm : The 10-year Note has slipped into negative territory to trade with a narrow loss. Its yield remains a few basis points below 2.20%, though.

For quick comparison, the yield on Germany's 10-year Bund stands at 1.79%, while the yield on Britain's 10-year Gilt is at 2.20%. Meanwhile, Japan's 10-year government issued Note is yielding 0.99%. DJ30 +58.20 NASDAQ +3.86 SP500 +5.96 NASDAQ Adv/Vol/Dec 1285/910 mln/1160 NYSE Adv/Vol/Dec 1845/320 mln/1080

1:00 pm : Energy stocks recently staged a strong run that has the sector sporting a 0.6% gain. Although that isn't quite as strong as the 0.7% gains currently displayed by Consumer Staples stocks and Health Care stocks, the Energy sector carries much more influence because of its market weight.

Still, overall gains remain only modest as stocks chop along in the final session of March. As things currently stand, the S&P 500 will book a first quarter gain of 12%, which is owed to an impressive run that has taken the broad market to 11 weekly gains in 13 tries.

Financials and Tech have been integral in the stock market's first quarter performance, but both sectors have been relatively quiet today. While Financials have at least worked their way up to a 0.3% gain, the Tech sector remains mired in negative territory with a narrow loss of 0.1%.

Corporate news has been without any real consequence and economic data has hardly been influential in today's trade.

Personal income increased in February by slightly slower-than-expected 0.2%, but personal spending proved better than expected by climbing 0.8%. Separately, the Chicago PMI slipped more than expected to 62.2 in March, while the final reading on consumer sentiment in March from the University of Michigan improved unexpectedly to 76.2. DJ30 +52.48 NASDAQ +1.70 SP500 +4.97 NASDAQ Adv/Vol/Dec 1305/835 mln/1125 NYSE Adv/Vol/Dec 1895/295 mln/990

12:30 pm : Stocks have entered into a sideways drift. The action makes for some rather unexciting mid-session trade.

Outside of equities, commodities continue to trade with solid gains, which have lifted the CRB Index to a 1.1% gain. However, the CRB still has a ways to go before it can fully offset the 1.8% slump that it suffered yesterday and the 1.3% drop that it endured the day before. Those declines have left the CRB on pace for a weekly loss of about 1.6%. For the month the CRB is down 4.0%, but up 1.4% for the first quarter. DJ30 +54.07 NASDAQ +.02 SP500 +4.67 NASDAQ Adv/Vol/Dec 1290/745 mln/1130 NYSE Adv/Vol/Dec 1840/270 mln/1030

12:00 pm : Stocks have been unable to extend their recent move higher. The effort remains hampered by a lack of leadership.

Tech, which is the largest sector by market weight, has been unable to fully break free from sellers, who have kept the sector mired in negative territory with a narrow loss. Heavyweight Apple (AAPL 602.19, -7.67) has been a considerable drag on the space -- the stock's down in excess of 1% for the second straight session. Although that sounds like pronounced weakness, it is only a modest setback in the context of AAPL's first quarter performance. As things currently stand, AAPL is poised for a first quarter gain of nearly 50%. That rapid run higher has made the stock the largest by market cap. DJ30 +55.81 NASDAQ +3.32 SP500 +5.00 NASDAQ Adv/Vol/Dec 1315/665 mln/1075 NYSE Adv/Vol/Dec 1860/245 mln/995

11:30 am : Stocks have bounced higher in recent trade. The move has swung the Dow from its session low back to its opening highs. As for the S&P 500, it isn't quite back to the levels that it set in the early going. The Nasdaq is only narrowly positive now. There isn't any clear catalyst for the recent climb, but the move was rather broad.DJ30 +49.64 NASDAQ +2.13 SP500 +4.46 NASDAQ Adv/Vol/Dec 1165/560 mln/1175 NYSE Adv/Vol/Dec 1755/205 mln/1065

11:00 am : The Nasdaq has fallen into negative territory, while the S&P 500 chops along near the neutral line. The Dow also came in contact with the flat line in recent trade, but support there has enabled it to remain in positive territory with a modest gain.

The recent retreat by stocks comes amid a lack of leadership -- Health Care stocks and Consumer Staples stocks, both up 0.5%, are today's top performing sectors, but neither possesses the market weight to make them influential in broad market trade. Typical leaders like Tech are trading lower today; the sector was last quoted with a 0.3% loss and has lagged since the open. As for Financials, they're down, too, but with a 0.1% loss. Energy stocks are up with only a tepid gain of 0.2%. DJ30 +25.89 NASDAQ -5.92 SP500 +0.54 NASDAQ Adv/Vol/Dec 925/470 mln/1390 NYSE Adv/Vol/Dec 1440/180 mln/1365

10:30 am : Crude oil prices climbed shortly before the open of pit trade, but they have been unable to extend the move. In fact, prices recently came under pressure, dropping to nearly $102.80 per barrel before rebounding to $103.25 per barrel for a 0.5% gain.

Natural gas prices have oscillated since overnight trade, when they slipped fractionally below $2.12 per MMBtu to set new multi-year lows. Prices are now up 0.4% to $2.16 per MMBtu.

Precious metals have had some of their gains pared, but gold still sports a 0.6% gain at $1664.50 per ounce, while silver sits at $32.34 per ounce with a 1.1% gain.

Corn futures trading just opened. Prices have spiked 5.1% to $6.35 per bushel. Earlier this morning the latest USDA planting report indicated that March corn stocks are down 8% year over year, but corn growers intend to increase their 2012 all-purpose corn planting by 4% from last year the highest corn acreage in the U.S. since 1937. DJ30 +28.33 NASDAQ -7.55 SP500 +1.41 NASDAQ Adv/Vol/Dec 1215/285 mln/1015 NYSE Adv/Vol/Dec 1765/115 mln/990

10:00 am : Stocks benefited from a mild bit of buying following the final reading on consumer sentiment in March from the University of Michigan. It improved to 76.2 from the preliminary reading of 74.3, which is where economists polled by Briefing.com had generally expected the reading to remain.

Although leadership remains limited, Tech stocks are lagging noticeably. The sector has slipped into the red to trade with a 0.1% loss. Although that isn't much, it makes Tech this morning's poorest performing sector. DJ30 +28.38 NASDAQ +0.96 SP500 +2.98 NASDAQ Adv/Vol/Dec 1500/120 mln/595 NYSE Adv/Vol/Dec 2140/60 mln/505

09:45 am : Stocks have drifted down from their opening levels, but the three major equity averages remain in positive territory with modest gains.

There isn't a single sector in negative territory, but leadership is limited. However, Health Care is starting to separate itself from the rest of the pack. The sector has already worked its way up to an early gain of 0.5%. Health Care stocks also outperformed in the prior session.

Just released, the Chicago PMI slipped to 62.2 in March from 64.0 in February. A tick down to 63.0 had been broadly expected. DJ30 +32.46 NASDAQ +5.72 SP500 +3.74

09:15 am : S&P futures vs fair value: +6.70. Nasdaq futures vs fair value: +12.80. A positive posture to premarket trade suggests that the cash market will open with a modest gain. That would help secure another weekly gain for the S&P 500, which is sitting on a first quarter gain in excess of 11%.

The relatively upbeat mood has extended into the commodity complex after it had experienced a couple of generally weak sessions. Indicative of an increased tolerance for risk, the dollar is down markedly this morning in favor of the euro. Eurozone members recently made it known that they have expanded the region's firewall fund to 800 billion euros.

Data haven't been all that riveting thus far -- personal income increased by slightly slower-than-expected 0.2% during February, but personal spending grew by a better-than-expected rate of 0.8%. Still on the docket, the latest Chicago PMI report will be posted at 9:45 AM ET. It will be followed almost immediately by the final monthly reading on consumer sentiment from the University of Michigan at 9:55 AM ET.

09:05 am : S&P futures vs fair value: +6.70. Nasdaq futures vs fair value: +12.50. A bout of buying interest in late electronic trade lifted crude oil prices, but they have since eased back so that they trade with a 0.6% gain at $103.40 per barrel in early pit trade. The bounce comes after oil prices fell sharply to set new monthly lows in the prior session. Natural gas prices have swung higher in recent trade. The move has prices up 0.4% to $2.16 per MMBtu. In the early hours of electronic trade its price slipped fractionally below $2.12 per MMBtu to set new multi-year lows.

As for precious metals, gold prices are currently up a strong 0.8% at $1668.70 per ounce, while silver sits at $32.52 per ounce with a 1.7% gain.

Worth noting, the latest USDA planting report indicates that March corn stocks are down 8% year over year, but corn growers intend to increase their 2012 all-purpose corn planting by 4% from last year -- the corresponding 95.9 million acres of planted corn would mark the highest corn acreage in the U.S. since 1937. Open outrcry trade for corn does not begin until 10:30 AM ET.

08:35 am : S&P futures vs fair value: +5.60. Nasdaq futures vs fair value: +10.80. Stock futures are off of their morning highs, but they continue to lead fair value following a recent dose of data that indicate personal income increased by 0.2% during February. That comes in slight contrast to the Briefing.com consensus call for a 0.3% increase. As for personal spending, it grew by 0.8%, which is faster than the 0.6% increase that had been expected, on average, among economists polled by Briefing.com. Core personal consumption expenditures (PCE) prices for February were up 0.1%, just as had been broadly anticipated.

08:05 am : S&P futures vs fair value: +7.40. Nasdaq futures vs fair value: +15.00. In the prior session the S&P 500 staged a late rally that slashed losses, but the broad market measure still settled in the red for the third straight day. With help from renewed strength in Europe the improved mood has carried over into premarket trade this morning, such that a positive open is anticipated. That would add to another weekly gain -- a heady move on Monday is owed credit for the stock market's week-to-date gain of 0.4%. Although that is only a modest move, it marks the eleventh weekly advance for the S&P 500 in 13 tries.

That run has the stock market heading into its final session of March sporting a month-to-date gain of almost 3% and a quarterly gain greater than 11%. Perhaps more impressive is that such a performance has come in the face of concerns and uncertainty related to sovereign debt, the pace of global economic growth, and plans for domestic monetary policy.

While those themes certainly remain on the radar for many market participants, attention this morning will be given to monthly personal income and spending numbers at 8:30 AM ET; the latest Chicago PMI report at 9:45 AM ET, and; the final monthly reading on consumer sentiment from the University of Michigan at 9:55 AM ET.

Corporate news has offered few catalysts to traders.

06:18 am : [BRIEFING.COM] S&P futures vs fair value: +7.00. Nasdaq futures vs fair value: +14.80.

06:18 am : Nikkei...10083.56...-31.20...-0.30%. Hang Seng...20555.58...-53.80...-0.30%.

06:18 am : FTSE...5778.95...+36.90...+0.60%. DAX...6946.83...+71.70...+1.00%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader,

http://stocktwits.com/wrbtrader and

http://chart.ly/users/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage