Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

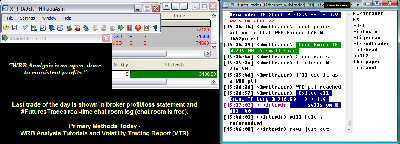

110111-wrbtrader-PnL-Blotter-Profit-3130.png [ 74.43 KiB | Viewed 311 times ]

110111-wrbtrader-PnL-Blotter-Profit-3130.png [ 74.43 KiB | Viewed 311 times ]

click on the above image to view today's trading summary Trade Performance for Today: +31.30 points or

$3130.00 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. Today's

#FuturesTrades trading chat room logs provides details (e.g. time, price, contract size) about each one of my trades from entry to exit along with price action commentary as the trade traversed...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=96&t=1042.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=5&t=180.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=145&t=1269 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

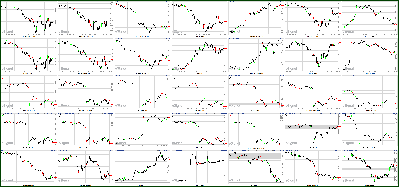

Stocks Fall Hard On Greece Fears Attachment:

110111-Key-Price-Action-Markets.png [ 514.88 KiB | Viewed 309 times ]

110111-Key-Price-Action-Markets.png [ 514.88 KiB | Viewed 309 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- New fears about the fate of the European rescue plan reverberated through stock markets in the United States and around the world Tuesday.

Following European markets, U.S. stocks ended sharply lower across the board. Bank stocks were hit especially hard.

The bad news was propelled by Greek Prime Minister George Papandreou's surprise announcement that he would put his country's participation in last week's European debt plan to a voter

referendum.

The announcement spooked investors, who feared a public vote would jeopardize the carefully-crafted deal.

Tuesday afternoon, stocks clawed back from the lowest levels of the day following a Dow Jones report that said the referendum is "basically dead." But just minutes before the market close, other news reports said the referendum will go ahead.

In the end, the Dow Jones industrial average (INDU) finished 297 points lower, falling 2.5%, the S&P 500 (SPX) sank 35 points, or 2.8%, and the Nasdaq (COMP) lost 77 points, or 2.9%. Earlier, all three indexes were off around 3%.

"Beggars can't be choosers and the fact that Greece even thinks they have a choice in accepting the EU debt deal is beyond logic," said Kathy Lien, director of currency research at Global Forex Trading, in a note to clients.

* Video - Greece is still the wordPapandreou may be demonstrating "political brinkmanship in order to solidify his position in the view of the public," despite the highly unpopular austerity measures, said Mark Luschini, chief investment strategist at Janney Montgomery Scott.

The referendum could also be Greece's way of warning European officials that they need better terms that the public will support, or else the deal will fall apart, added Luschini. Or it could be a "complete policy blunder."

"Investors don't know what the referendum is going to mean, but they're selling first and will ask questions later," said Luschini. "If Greece ends up demanding different terms to the deal, European officials will be less willing to help. And that could put the prospect of a disorderly Greek default back on the table."

The market's fear gauge, the VIX (VIX), spiked 19% to 35.60. Any reading above 30 signals investor worry. Earlier, the index has surged 25%.

Stocks are coming off sharp losses Monday, as questions and doubts arose regarding the rescue package agreed upon by European leaders last week.

The recent selling puts the S&P 500 and Nasdaq back in negative territory for the year, while the Dow is up just 0.7% in 2011.

* MF Global may have millions missingCompanies: Bank stocks were hit especially hard in Tuesday's sell-off, with shares of Morgan Stanley (MS, Fortune 500) and Citigroup (C, Fortune 500) shares off nearly 8%. Bank of America (BAC, Fortune 500), JP Morgan Chase (JPM, Fortune 500) and Goldman Sachs (GS, Fortune 500) were down more than 5%.

Pfizer (PFE, Fortune 500) shares rose after the company reported quarterly earnings that beat Wall Street's estimates. The drugmaker was the only gainer on the Dow, and among a handful of S&P 500 stocks in positive territory.

Shares of Baker Hughes (BHI, Fortune 500) plunged, making it the big decliner on the S&P 500. The oilfield contractor missed earnings estimates.

MetroPCS (PCS) shares also fell after the wireless service provider reported lackluster earnings results.

Meanwhile, Bank of America said it will drop its planned $5 debit card usage fee after widespread customer complaints.

World markets: World markets tumbled Tuesday, with banks leading the decline globally. Germany's DAX (DAX) lost 5%, Britain's FTSE 100 (UKX) dropped 2.2%, and France's CAC 40 (CAC40) tumbled 5.4%

Societe Generale, BNP Paribas, and Credit Agricole shed between 12% and 17% in Paris. In Germany, shares of Deutsche Bank (DB) dropped 8%.

Asian markets ended mostly in the red, after a report showed China's manufacturing activity slowed in September. The Shanghai Composite (SHCOMP) was flat, while the Hang Seng (HSI) in Hong Kong fell 2.5% and Japan's Nikkei (N225) shed 1.7%.

Economy: The ISM index show manufacturing activity barely expanded in October, coming in at 50.8. Any level above 50 indicates growth in the sector. But the reading fell from September and came in below expectations.

Construction spending edged up 0.2% in September, down from a 1.6% pickup in August. Economists were expecting spending to rise 0.3%.

Auto sales figures will be coming out throughout the day.

* Video - Trichet defends his handling of crisisCurrencies and commodities: The dollar rose against the euro and British pound, and versus the Japanese yen.

Oil for December delivery slipped $1.00, or 1.1%, to settle at $92.19 barrel.

Gold futures for December delivery fell $13.40, or 0.8%, to settle at $1,711.80 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury rose, pushing the yield down to 2.00% from 2.18% late Monday.

Market Update

Market Update 4:30 pm : Revived concerns related to Europe's ability to efficiently and effectively restore financial conditions resulted in another round of aggressive selling.

Stocks extended the prior session's sell-off by suffering another steep slide. Selling pressure was essentially underpinned by the belief that Greece could disrupt the implementation of the eurozone bailout plan by issuing a referendum, although some afternoon headlines suggested that the referendum was unlikely to win support. Selling pressure was exacerbated by dwindling confidence in Italy's financial health, as indicated by a spike in the yields of the country's debt.

Those themes took a heavy toll on Europe's bourses. In turn, the EuroStoxx 50 fell nearly 3%. The euro was also implicated; it tumbled to a 1% loss against the greenback, as of the close of trade.

Diversified bank stocks were some of the hardest hit issues in both Europe and at home. Their weight and their weakness left the overall financial sector to fall almost 5%.

Pfizer (PFE 19.33, +0.07) was the only Dow component that managed to post a gain. Its strength was owed to a better-than-expected quarterly report. That didn't do anything to inspire buying in the rest of the health care space, though. Health care stocks still suffered a collective loss of 2.0%.

As more participants turned to selling the Volatility Index surged. At session's end it was up 20%, which comes on top of the 10% jump that it made during the prior session.

Treasuries attracted a bevy of buyers amid the market's second straight tumble. That drove the yield on the benchmark 10-year Note below 2.0% after it had been near 2.4% less than one week ago.

Data did nothing to improve the mood of participants. The ISM Manufacturing Index declined to 50.8 in October from 51.6 in the prior month. It had been expected to improve to 52.1.

Construction spending increased by 0.2% in September, but it had been expected to increase by 0.3% after a 1.4% jump the month before.

Data from abroad featured the the United Kingdom third quarter GDP report, which showed a 0.5% increase, and an October PMI reading of 47.4 that followed a reading of 51.1 in the prior month. China posted a PMI of 50.4 for October, but that is down from 51.2 in the prior month.

Advancing Sectors: (None)

Declining Sectors: Telecom -1.6%, Consumer Staples -1.7%, Health Care -2.0%, Utilities -2.0%, Consumer Discretionary -2.2%, Materials -2.6%, Tech -2.8%, Industrials -3.1%, Energy -3.1%, Financials -4.7%DJ30 -297.05 NASDAQ -77.45 NQ100 -2.6% R2K -3.7% SP400 -3.3% SP500 -35.02 NASDAQ Adv/Vol/Dec 409/2.29 bln/2158 NYSE Adv/Vol/Dec 445/1.32 bln/2603

3:30 pm : Trade in commodities was focused around what will happen next in Greece. Late in the session headlines crossed the wires which indicated that a referendum vote was unlikely in Greece. This caused the dollar to give back some of its gains and helped commodities recoup some of their losses. Gold futures ended lower by 0.7% at $1711 per ounce, silver shed 4% to close at $32.97 per ounce.

Crude oil, which settled lower by 1.1% at $92.19 per barrel, rallied heading into the close, recouping around 1.5 points in afternoon trade. Futures finished just shy of overnight highs around $92.50. Natural gas shed 3.7% to close at $3.79 per MMBtu. Forecasts for mild weather across the Midwest and Northeast pressured prices throughout the session.DJ30 -258.11 NASDAQ -68.36 SP500 -31.91 NASDAQ Adv/Vol/Dec 430/1.8 bln/2122 NYSE Adv/Vol/Dec 470 /941.9 mln/2587

3:00 pm : Stocks have started to roll over after working their way to afternoon highs, which were almost in line with the session highs that were set this morning. Selling interest has been broad, but financials, down nearly 4%, continue to lead the effort.

With only an hour remaining in today's trade, the stock market is on pace for its second straight loss of about 2.5%. The back-to-back drops currently make for the market's worst two-session performance since the stock market fell 2.5% in the final session of September and then 2.9% in the first session of October. DJ30 -230.87 NASDAQ -62.51 SP500 -27.56 NASDAQ Adv/Vol/Dec 475/1.62 bln/2050 NYSE Adv/Vol/Dec 495/820 mln/2525

2:30 pm : Monthly motor vehicle sales numbers have been released intermittently today. Their share prices have varied amid today's volatility.

Ford (F 11.23, -0.45) reported that its U.S. sales for October climbed by 6% from the previous year. General Motors (GM 23.55, -2.30) posted a 2% annual increase in U.S. sales for October. As for foreign auto makers, Honda Motor (HMC 30.35, +0.45) had a 3% annual increase in American sales. Toyota Motors (TM 65.72, -0.99) experienced a 4% increase in U.S. sales. DJ30 -173.99 NASDAQ -49.63 SP500 -21.32 NASDAQ Adv/Vol/Dec 455/1.49 bln/2060 NYSE Adv/Vol/Dec 465/750 mln/2555

2:05 pm : Stocks have managed to sustain their recent move higher, but havn'e quite reached the session highs that were set this morning. Nonetheless, losses are still significantly less than what they were only an hour ago.

Improved trade has put some pressure on the dollar, which is now well off of its session high, but still sporting a 0.8% gain against a collection of competing currencies. Treasuries have also pulled back. DJ30 -211.45 NASDAQ -60.57 SP500 -26.04 NASDAQ Adv/Vol/Dec 455/1.38 bln/2060 NYSE Adv/Vol/Dec 465/695 mln/2560

1:30 pm : Stocks are spiking higher. The move has been so fast and dramatic that the Dow has slashed its loss by about 100 points in only a matter of minutes. The move has coincided with a headline that Greece's referendum is unlikely.DJ30 -208.92 NASDAQ -68.32 SP500 -29.02 NASDAQ Adv/Vol/Dec 325/1.20 bln/2170 NYSE Adv/Vol/Dec 360/595 mln/2645

1:00 pm : Stocks are at risk of suffering their second straight rout. Selling pressure comes as market participants respond to revived concerns related to Europe's ability to efficiently and effectively restore financial conditions.

The S&P 500 dropped 2.5% yesterday as euphoria from Europe's bailout plan evaporated and participants reacted to reports that officials in Greece are seeking a referendum for the plan. A slump by Europe's bourses in response to the threat that Greece could disrupt the implementation of the bailout and rekindled concerns about Italy's ability to meet its debt obligations has perpetuated selling pressure. In turn, domestic stocks are on pace for another precipitous drop.

Macro concerns have almost completely overshadowed earnings, although a better-than-expected report from Pfizer (PFE 19.43, +0.17) has helped the stock bounce in the face of broad market weakness. It pharmaceutical giant is the only name in the Dow currently sporting a gain.

Financials are generally in the worst shape today. Although many major bank stocks have worked their way up from session lows, concern about their exposure to Europe continues to hamper them. Collectively, financials are down more than 4%.

A loss of confidence among so many participants has stoked volatility, such that the Volatility Index has spiked more than 20% today. That comes after it climbed more than 10% yesterday.

Amid all of the action the dollar has been a source of safety for traders. It has extended its prior session rally by advancing another 1.1% against a collection of competing currencies. DJ30 -313.39 NASDAQ -85.08 SP500 -37.16 NASDAQ Adv/Vol/Dec 345/1.11 bln/2150 NYSE Adv/Vol/Dec 365/550 mln/2640

12:30 pm : Stocks appear to have stabilized, for now, but weakness remains widespread as the major equity averages wrestle with sizable losses. As things currently stand, the stock market is on pace to lose more than 5% of its value in only two days.

With stocks looking so shaky, the Volatility Index, which is often euphemistically referred to as the Fear Gauge, is up more than 20% today. That surge comes on top of a spike of more than 10% during the prior session. The VIX is now back near its 10-day high after setting a two-month low late last week. DJ30 -283.21 NASDAQ -77.13 SP500 -34.17 NASDAQ Adv/Vol/Dec 360/980 mln/2120 NYSE Adv/Vol/Dec 365/490 mln/2630

12:00 pm : Stocks have descended to new session lows. The decline has left the Dow to trade with a loss of about 300 points. Of the Dow's 30 components, only Pfizer (PFE 19.67, +0.41) is in positive territory. The stock's strength comes in the wake of a better-than-expected quarterly report, which was posted this morning.DJ30 -304.55 NASDAQ -79.13 SP500 -35.87 NASDAQ Adv/Vol/Dec 390/840 mln/2070 NYSE Adv/Vol/Dec 400/430 mln/2575

11:30 am : Stocks recently slipped from their mid-morning highs, but they are starting to recover. Overall losses remain sizable, though.

As was the case in the prior session, utilities make up the only major sector that has limited its loss to less than 1%. The sector's relative strength is largely owed its appeal as a safe haven, given the general stability of utilities businesses, especially those with regulated entities, and their hefty dividend payments. That said, Public Service Group (PEG 33.30, -0.69) is down 2%, even though the company posted this morning an upside earnings surprise. DJ30 -207.41 NASDAQ -54.46 SP500 -25.14 NASDAQ Adv/Vol/Dec 350/690 mln/2050 NYSE Adv/Vol/Dec 400/360 mln/2540

11:00 am : Financials had been staging a steady climb up from session lows, but were recently caught up in a flurry of selling pressure. The sector was down more than 4% at its low, but had cut that in half as it worked its way to a session high. After retracing part of that move the sector now trades with a 3.4% loss.

Given that contagion concerns in Europe have been rekindled, participants are applying particularly sharp pressure on diversified banks and financial services stocks that are believed to have exposure to Europe. As such, Bank of America (BAC 6.48, -0.87), JPMorgan Chase (JPM 32.80, -3.89), and Citigroup (C 29.50, -4.66) are all down in excess of 10%. European financial outfits are in even worse shape as names like Deutsche Bank (DB 38.56, -8.24) and Royal Bank of Scotland (RBS 7.18, -1.31) drop precipitously. DJ30 -221.22 NASDAQ -54.92 SP500 26.38 NASDAQ Adv/Vol/Dec 385/595 mln/1995 NYSE Adv/Vol/Dec 410/310 mln/2510

10:30 am : Stocks are trying to trim some of their losses, but selling pressure remains strong. Many commodities have also improved their position, but continue to wrestle with aggressive selling, too.

Oil prices were down about 4% at their session lows, but the energy component has cut its loss to about 2.7% as it trades for $90.65 per barrel. In contrast, natural gas prices have extended their descent by sliding to $3.93 per MMbtu for a 3.2% loss.

Precious metals have moved higher in the past 90 minutes, but their prices remain in the red. Gold prices are currently down 0.9% at $1710 per ounce after they had been down more than 2% earlier today. Silver prices had slumped more than 6%, but the metal is now down 3.0% at $33.31 per ounce. DJ30 -200.78 NASDAQ -54.55 SP500 -23.77 NASDAQ Adv/Vol/Dec 270/408 mln/2075 NYSE Adv/Vol/Dec 305/225 mln/2575

10:05 am : Stocks have slipped after attempting to work their way up from opening lows. The move comes amid news that the ISM Manufacturing Index for October eased down to 50.8 from 51.6 in the prior month. It had been broadly expected to improve to 52.1.

Construction spending during September increased by 0.2%, which is less than the 1.4% increase experienced in the prior month. It is also less than the 0.3% increase that had been generally expected. DJ30 -254.47 NASDAQ -63.52 SP500 -29.31 NASDAQ Adv/Vol/Dec 160/170 mln/2125 NYSE Adv/Vol/Dec 210/110 mln/2570

09:45 am : Selling has been so aggressive in the first few minutes of trade that all three of the major equity averages are down well in excess of 2%. That has helped bolster buying interest in Treasuries, such that the yield on the benchmark 10-year Note is now down to 2.00% after it had been near 2.40% less than a week ago.DJ30 -254.97 NASDAQ -64.96 SP500 -31.33 NASDAQ Adv/Vol/Dec NA/NA/NA NYSE Adv/Vol/Dec NA/NA/NA

09:15 am : S&P futures vs fair value: -37.00. Nasdaq futures vs fair value: -53.30. Stocks are expected to slump at the open as participants respond to aggressive selling pressure in Europe, where contagion concerns have been revived amid reports that Greece may seek a referendum for the recently proposed bailout package and rising yields in Italy point to the country's precarious conditions. The dollar has been a home for safety seekers. On top of its prior session surge, the greenback is up well in excess of 1% against a basket of major foreign currencies. These themes have completely overshadowed the latest round of earnings results, which continue to generally exceed consensus estimates. Still on tap, though, are the monthly ISM Manufacturing Index and construction spending numbers, both of which are due at 10:00 AM ET. The FOMC also begins its two-day meeting today.

09:05 am : S&P futures vs fair value: -39.30. Nasdaq futures vs fair value: -57.50. Equities continue to come under sharp pressure ahead of the open. Commodities are also getting clipped aggressively. Specifically, crude oil prices are down 3.8% to $89.55 per barrel in the opening minutes of pit trade. Meanwhile, natural gas prices are down 2.8% to $3.94 per MMbtu. Precious metals haven't offered any safety to participants. Gold prices were last quoted with a 2.1% loss at $1689 per ounce. Worse still is the 6.0% drop that has taken silver to $32.29 per ounce. Exacerbating weakness in the commodity complex is the rally by the dollar, which is up 1.5% against a collection of competing currencies.

08:35 am : S&P futures vs fair value: -33.70. Nasdaq futures vs fair value: -52.80. The EuroStoxx 50 is down 3.4% as Europe's bourses are pummeled in response to the possibility that bailout plans will be interrupted by a referendum from Greece. Meanwhile, the thought that Italy is teetering on the brink of default has not only spiked yields on the country's debt, but revived contagion concerns in the region. Italy's primary market is currently down 5.9%. Greece's Athex 20 is presently down 6.4%. Germany's DAX has dropped to a 5.3% loss, France's CAC is currently off by 4.5%. Britain's FTSE has fallen to a 3.0% loss. Data from the United Kingdom showed a 0.5% increase in third quarter GDP. That follows a 0.1% increase in the second quarter. The United Kingdom's PMI for October fell to 47.4 from 51.1 in the prior month.

Data from China proved disappointing. The country's PMI for October fell to 50.4 from 51.2 in the prior month. The Shanghai Composite managed to muster a 0.1% gain. Some pundits proposed that the data could serve as proof to China's policymakers that measures are needed to energize the country's economy. Hong Kong's Hang Seng sank 2.5%. CNOOC (CEO) weighed heavily on action. Property plays were also pressured. Japan's Nikkei fell 1.7%. Pressure was broad, but Fanuc Ltd. was one of the heaviest drags on overall trade.

08:05 am : S&P futures vs fair value: -27.70. Nasdaq futures vs fair value: -45.30. Coming off of four straight weekly gains, stocks descended yesterday to their worst single-session loss in almost one month. Pressure persists this morning as participants consider the possibility that plans to bailout Europe will be undermined by Greece's proposal for a referandum on the plan's measures. The news has been especially problematic for Europe's bourses, many of which are down in excess of 3% and 4%. Adding to selling interest there is a signal of dwindling confidence in Italy, which has seen its bond yields surge. Amid these themes the dollar has staged a strong advance of about 1.1% against a basket of major foreign currencies. That comes on top of a similar run during the prior session. On tap for today is the latest ISM Manufacturing Index, which will be issued at 10:00 AM ET. Monthly construction spending numbers will also be released then. The FOMC begins its two-day meeting today, culminating in a policy statement and press conference tomorrow.

06:53 am : [BRIEFING.COM] S&P futures vs fair value: -24.40. Nasdaq futures vs fair value: -42.50.

06:52 am : Nikkei...8835.52...-152.90...-1.70%. Hang Seng...19369.96...-494.90...-2.50%.

06:52 am : FTSE...5391.80...-152.40...-2.80%. DAX...5876.96...-264.40...-4.30%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage