Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

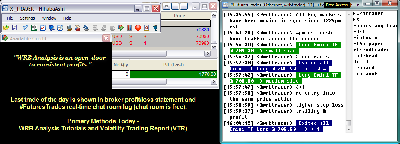

101411-wrbtrader-PnL-Blotter-Profit-1770.png [ 74.94 KiB | Viewed 305 times ]

101411-wrbtrader-PnL-Blotter-Profit-1770.png [ 74.94 KiB | Viewed 305 times ]

click on the above image to view today's trading summary Trade Performance for Today: +17.70 points or

$1770.00 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. Today's

#FuturesTrades trading chat room logs provides details (e.g. time, price, contract size) about each one of my trades from entry to exit along with price action commentary as the trade traversed...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=95&t=1028.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=5&t=180.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=144&t=1237 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

S&P 500 Caps Best Weekly Gain Since July 2009 on Retail Oct. 14 (Bloomberg) -- Bloomberg's Cali Carlin reports on the performance of the U.S. equity market today. U.S. stocks advanced, giving the Standard & Poor's 500 Index its biggest weekly gain since July 2009, as retail sales beat economists' estimates and the Group of 20 nations began discussions on Europe's debt crisis.

Dow and Nasdaq Back In Positive Territory Attachment:

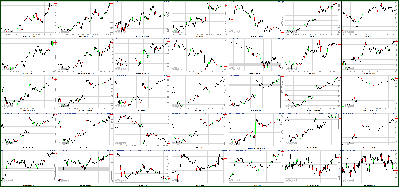

101411-Key-Price-Action-Markets.png [ 536.87 KiB | Viewed 341 times ]

101411-Key-Price-Action-Markets.png [ 536.87 KiB | Viewed 341 times ]

click on the above image to view today's price action of key markets By Maureen Farrell October 14, 2011: 4:33 PM ET

NEW YORK (CNNMoney) -- Stock market investors finally broke even for 2011, after a choppy trading week.

The Dow Jones industrial average and Nasdaq rallied Friday, moving both indexes into positive territory for the year. The S&P 500 came close.

The Dow Jones industrial average (INDU) closed up 166 points, or 4.9% for the week, and the S&P 500 (SPX) moved up 21 points Friday, or 6% for the week. The tech-heavy Nasdaq composite (COMP) was up 38 points, or 7.6% for the week.

The S&P offered up its best weekly gain since July 2009, and for the Nasdaq, since March 2009. The Dow had its best weekly gain since the last week of June.

"Recent economic data reinforces our belief that the U.S. economy is not in a recession," said Joseph Tanious, market strategist at JPMorgan Chase Asset Management. "The consumer is in fact coming back and starting to spend."

Investors clung onto positive data, and by Friday appeared to have at least temporarily shrugged off fears over the fate of Europe and a drop in profit at JPMorgan Chase, the first major bank to report quarterly earnings.

"I would call this a 'pray trade' today," said Sam Ginzburg, head of capital markets at First New York Securities. "People are hoping there's some good news out of Europe this weekend or some other good news that will reward people for buying."

With looming uncertainty over Europe and several large U.S. banks poised to report paltry earnings, some investors and traders questioned whether this week's rally would be sustainable.

Google (GOOG, Fortune 500) was among the biggest gainers Friday, a day after the search giant issued a stellar earnings report. The buying spilled over to other big tech names, with shares of Dow component Hewlett-Packard (HPQ, Fortune 500) moving up.

The Commerce Department released September retail sales figures before the opening bell that signaled a more positive reading on the buying patterns of the American consumer.

Meanwhile, thousands of consumers lined up outside Apple stores waiting to become among the first iPhone 4s buyers in another sign that spending is picking up. Apple's (AAPL, Fortune 500) shares jumped Friday too.

Expectations of more robust consumer demand caused a run-up in stocks in the oil and industrials sectors. Among the biggest Dow gainers were Chevron (CVX, Fortune 500), Exxon (XOM, Fortune 500) and General Electric (GE, Fortune 500). Oil prices hovered around a recent high of $87 a barrel.

* Video - Google's domination paying offBut investors are still wrestling with whether European leaders will take the appropriate steps to prevent massive fallout from Europe's debt crisis.

As finance ministers from the Group of 20 economies start a two-day meeting in Paris to discuss Europe's debt crisis, Treasury Secretary Timothy Geithner reiterated U.S. support to help Europe address its sovereign debt crisis.

Stocks ended mixed on Thursday, as investors turned cautious following lackluster earnings from JPMorgan Chase (JPM, Fortune 500).

In Friday morning trading, financial sector stocks hovered around break-even but occassionally moved into positive territory. Shares of JPMorgan Chase (JPM, Fortune 500), Goldman Sachs (GS, Fortune 500), Morgan Stanley (MS, Fortune 500), Credit Suisse (CS), and Bank of America (BAC, Fortune 500) had traded down yesterday and in early morning trading following JPMorgan Chase earnings.

Companies: Before the opening bell, Mattel (MAT, Fortune 500) reported strong sales of Barbie dolls, which helped drive its revenue higher than expected in the third quarter.

Economy: Early Friday, the Commerce Department reported retail sales rose 1.1% in September, an improvement after sales rose only 0.3% the month before. The data beat economists' expectations of a 0.6% increase.

The Bureau of Labor Statistics reported export prices rose 0.4%, and import prices rose 0.3% in September.

Because consumer spending makes up more than two thirds of the U.S. economy, these numbers are closely watched as a gauge of the recovery.

* Slovakia gives OK to Europe bailout planWorld markets: On Thursday, Slovakia became the last of the 17 countries in the eurozone to approve a plan to expand the powers of a bailout fund for troubled European banks and governments.

This development pushed European stocks higher Friday morning, but investors are expected to soon shift their focus to other problems -- such as the size of losses Greek bondholders may be forced to take.

European all finished the week higher. On Friday, Britain's FTSE 100 (UKX) added 1.2%, the DAX (DAX) in Germany gained 0.9%, and France's CAC 40 (CAC40) ticked up 1%.

Investors appear to largely ignore the overnight Standard & Poor's downgrade of Spain's credit rating once again on weak growth and banking sector risks.

Asian markets closed lower following a report on Chinese inflation. The Shanghai Composite (SHCOMP) shaved 0.3%, the Hang Seng (HSI) in Hong Kong dropped 1.4% and Japan's Nikkei (N225) lost 0.9%.

Currencies and commodities: The dollar fell against the euro and British pound, but gained against the Japanese yen.

Oil for November delivery added $3.08 to $87.31 a barrel.

Gold futures for December delivery gained $13.50 to $1,682.00 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury fell slightly, pushing the yield up to to 2.3%.

Market Update

Market Update 4:35 pm : The S&P 500 overcame resistance on Friday to score another strong gain, contributing to the broad market's best weekly performance since July 2009.

A positive tone among market participants was perpetuated by more buying in Europe, where the continent's major bourses extended their recent rally. On Friday, Britain's FTSE advanced 1.2%, but gained more than 3% for the week. France's CAC clmbed 1.0% in the week's final session, but 4% over the past five trading days. A 0.9% advance by the Germany's DAX on Friday helped fuel a 5% weekly gain. Such strength reflected improved sentiment in the eurozone, where concerns about fiscal and financial conditions in both the peripheral and core constituents have threatened confidence for months. Those concerns manifested in a downgrade of Spain by analysts at Fitch on Friday.

A commitment early this week by leading eurozone officials to develop a comprehensive plan intended to stabilize precarious conditions and shore up capital at European banks sent a strong signal to global investors. It also got the week started on a strong note -- the stock market rallied more than 3% on Monday for its best single-session percentage gain in almost seven weeks.

Following that heady move, trade became more subdued on Tuesday. Participants kept their focus on Europe as Slovakia moved to vote on the European Financial Stability Facility (EFSF). Country officials actually voted down the plan Tuesday night in conjunction with a no confidence vote for Slovakia's prime minister, but there remained a belief that the EFSF will eventually win approval.

Tuesday also ushered in the unofficial start of earnings season when Dow component Alcoa (AA 10.26, +0.16) announced its latest quarterly results after the close. Some regarded the fact that the company came short of the consensus earnings estimate as an ominous sign.

Minutes from the most recent FOMC meeting were released Wednesday, but the release was essentially a non-event since it offered no new insight into the mindset of the monetary policy setting committee.

JPMorgan Chase (JPM 31.89, +0.29) was bid up aggressively ahead of its quarterly announcement on Thursday morning. The diversified financial services giant posted earnings that exceeded what Wall Street had widely expected, but the dubious quality of that beat was a focus of analysts. Concerted selling caused the stock to drop sharply. Given that JPMorgan Chase is widely regarded as the best in its class, many other banks were implicated. The result was a near 5% drop for the KBW Bank Index, which only made a half-hearted attempt to rebound on Friday, when it advanced a relatively tame 0.7%.

Another weekly initial jobless claims count narrowly above 400,000 -- 404,000 to be specific -- had little impact on action during Thursday's trade, but that's mostly because the tally was right in stride with the 406,000 claims that had been widely expected.

A superior report from Google (GOOG 591.68, +32.69) helped close out the week on a strong note. Both the top and bottom line bested what had been expected. That sent the stock to its highest level in more than one month and inspired buying in other large-cap tech issues. Collectively, tech stocks climbed 2.1% on Friday.

Since tech is the largest sector by market weight, its strength helped the S&P 500 stage a late climb that took it past the 1220 line, which had been a point of formidable resistance at the start of the session and earlier in the week.

Energy stocks were the best performers on Friday. Their 3.6% climb was helped along by a 3.2% spike in oil prices to almost $87 per barrel. Oil prices ended the week about 5% above where they began it.

In the backdrop of Friday's action were some encouraging retail sales numbers. Overall retail sales for September increased by 1.1%, while sales less autos increased by 0.6%. Economists surveyed by Briefing.com had expected respective increases of 0.6% and 0.3%. Not only did the September numbers exceed expectations, but they also marked the strongest increases since the first quarter.

Friday's advance marked the fourth gain in five sessions, helping the S&P 500 score a 6% weekly gain. Perhaps more impressive is that the stock market has now advanced in seven of the past nine sessions for a cumulative gain of more than 11%. DJ30 +166.36 NASDAQ +47.61 NQ100 +1.9% R2K +2.0% SP400 +1.9% SP500 +20.92 NASDAQ Adv/Vol/Dec 1898/1.66 bln/632 NYSE Adv/Vol/Dec 2530/847 mln/493

3:30 pm : Commodities closed out the week on a strong note. Specifically, crude oil prices climbed 3.2% to $86.89 per barrel. More impressive is that oil prices settled with a weekly gain of 5.0%. Elsewhere in the energy complex, natural gas prices spiked 4.8% today and 6.0% for the week.

Among precious metals, gold prices settled pit trade at 1683.20 per ounce, which makes for a 0.9% gain this session. It advanced 2.9% for the week, though. Silver prices scored a 1.6% gain by advancing to $32.17 per ounce. The ended the week 3.6% higher than where they started. DJ30 +133.81 NASDAQ +40.07 SP500 +17.35 NASDAQ Adv/Vol/Dec 2415/1.22 bln/590 NYSE Adv/Vol/Dec 2430/500 mln/560

3:00 pm : A steady afternoon ascent has taken the S&P 500 back to the 1220 line in the final hour of trade. Participants have paused, though. They are waiting to see if stocks can muster enough momentum late in the final session of the week to push through the point of resistance, which actually proved too much for stocks in the early going.DJ30 126.55 NASDAQ 37.84 SP500 16.27

2:30 pm : Amazon.com (AMZN 243.74, +7.59) doesn't report earnings until October 25, but the stock is benefiting from lots of buying interest today. In turn, shares of AMZN have set a new record high. Meanwhile, Google (GOOG 591.79, +32.80) is also up nicely today, but still about 125 points below its record high. Strength in GOOG comes on the back of a strong quarterly report. Robust gains by such large-cap issues have helped drive the Nasdaq higher in eight of the past nine sessions for a cumulative gain of more than 13%.DJ30 +91.54 NASDAQ +29.98 SP500 +12.33 NASDAQ Adv/Vol/Dec 1590/1.06 bln/880 NYSE Adv/Vol/Dec 2325/425 mln/650

2:00 pm : Stocks have stretched ahead to new afternoon highs. The major averages aren't yet back to their best levels of the day, however.

Energy stocks have added to their gains so that the sector is now up almost 3%. That makes for a new session high. More impressive still, the sector is at its best level in almost one month.

Consumer staples stocks and telecom stocks are today's weakest perfomers. Both defensive in nature, they are up just 0.3% and 0.4%, respectively. DJ30 +113.34 NASDAQ +32.54 SP500 +14.55 NASDAQ Adv/Vol/Dec 1475/950/960 NYSE Adv/Vol/Dec 2220/380 mln/745

1:30 pm : Stocks have gradually worked their way up from session lows. Each of the three major equity averages are now up by about 1%.

Strength among stocks has kept pressure on Treasuries. In turn, the yield on the benchmark 10-year Note remains above 2.20%.

As for the greenback, it has struggled to fight back against the euro, which is up 0.9% to $1.386. DJ30 +93.13 NASDAQ +25.11 SP500 +11.80 NASDAQ Adv/Vol/Dec 1400/890 mln/1035 NYSE Adv/Vol/Dec 2160/355 mln/795

1:00 pm : Stocks may be off of session highs, but the broad market has resumed its uptrend. In turn, the stock market is on track for a 5% weekly gain.

Strength among Europe's bourses in the face of Fitch's decision to downgrade Spain brought buyers back into the fold after stocks logged a loss in the prior session. Buying interest was further bolstered by news that total retail sales for September increased by 1.1% and sales less autos were up 0.6%. Respective increases of 0.6% and 0.3% had been generally expected.

The S&P 500 quickly climbed to a gain in excess of 1%, but resistance at the 1220 line, which had already stymied an advance by stocks earlier this week, proved too much to overcome. Stocks trended lower from there, but have since entered into a relatively tight trading range.

For the second straight session tech has been a source of support. The sector, which is the largest by market weight, is up 1.3% today. That comes on top of its 1.0% gain in the prior session. Google (GOOG 589.28, +30.29) has been a driver in both efforts. Its latest leg of gains comes in response to a stronger-than-expected quarterly report. The stock is at its best level in more than a month.

Strength among other large-cap tech stocks has the Nasdaq headed for its eight gain in nine sessions. During that time the tech-rich Index has climbed about 13%.

Not to be ignored, energy stocks have rallied aggressively this session. The sector is currently up 2.3%. Oil and gas equipment and services stocks have been especially strong, thanks partly to a 3.0% jump in oil prices to $86.75 per barrel.

Financials started today's trade on a strong note, but have since fallen back to the flat line. They have remained there for the past few hours. DJ30 +87.95 NASDAQ +21.30 SP500 +10.90 NASDAQ Adv/Vol/Dec 1350/825 mln/1060 NYSE Adv/Vol/Dec 2090/325 mln/840

12:30 pm : The stock market has entered into a sideways drift of sorts. Although that has made for some rather unexciting action, it has allowed stocks to hold steady to their gains, keeping the stock market's uptrend in tact. Should today's gains hold, the stock market will score its seventh advance in nine sessions. The Nasdaq has done slightly better in that time; it is headed for its eighth game in nine trading days.DJ30 +74.44 NASDAQ +18.41 SP500 +9.48 NASDAQ Adv/Vol/Dec 1275/755 mln/1115 NYSE Adv/Vol/Dec 2010/300 mln/885

12:00 pm : Stocks continue to trade near their session lows. Tech, which represents the largest sector by market weight, and energy stocks have been steady sources of support. The two sectors are up 1.1% and 1.9%, respectively.

Among tech plays, Google (GOOG 591.41, +32.42) has been a primary leader. The stock's 5% spike comes on the back of a better-than-expected quarterly report. Baidu.com (BIDU 136.16, +3.19) has traded higher in conjunction with strength in GOOG. As for energy, oil and gas exploration and services stocks like Schlumberger (SLB 69.36, +2.16) and Halliburton (HAL 36.35, +1.33). DJ30 +67.97 NASDAQ +20.26 SP500 +9.31 NASDAQ Adv/Vol/Dec 1350/670 mln/1020 NYSE Adv/Vol/Dec 2120/265 mln/750

11:30 am : Stocks have slipped to new session lows after chopping along in a generally downward direction. Financials, still mired near the neutral line, continue to act as a drag on the broad market.

Despite underwhelming action in the financial sector, which has been a primary driver of action in recent weeks, and the pullback by the broad market, energy stocks are holding steady to strong gains. Their 1.8% advance makes them this session's best performers. Of course, it has helped the oil prices are up to $86.25 per barrel, sporting a gain well in excess of 2%. DJ30 +57.22 NASDAQ +18.87 SP500 +8.75 NASDAQ Adv/Vol/Dec 1470/560 mln/855 NYSE Adv/Vol/Dec 2240/225 mln/625

11:00 am : The major market averages are holding solid gains despite the disappointing Michigan Sentiment data. The S&P 500 and Nasdaq lead the advance with gains of 1.0% while the Dow is seeing slight underperformance as it trades higher by 0.8%.

Financials are stuck near the flat line and are currently trading up 0.2% collectively. Bank of America (BAC 6.16, -0.06) is the worst performer of the large financial institutions as it trades down 1.0%. Rivals Wells Fargo (WFC 26.05, -0.07) and Citigroup (C 27.56, -0.08) are also seeing losses as the space remains under pressure despite the recent run up in equities. DJ30 +86.06 NASDAQ +24.89 SP500 +10.84 NASDAQ Adv/Vol/Dec 1406/502.5 mln/876 NYSE Adv/Vol/Dec 2143/203.2 mln/735

10:35 am : The dollar index is back near its session low of 76.51, which has given a boost to commodities. Aluminum is the only commodity in the CRB Commodity Index that is in the red.

Crude oil futures have been in positive territory all session and rose as high as $87.28/barrel about an hour ago. It pulled back below the $87 level and is now up 2.5% at $86.30/barrel.

Natural gas showed a decent uptrend all morning and hit its own session high about an hour ago as well, reaching $3.62/MMBtu. The energy component is currently trading at $3.60, up 2%

Precious metals have shown gains all morning. Gold ran as high as $1685.5/oz, but has pulled back about $12/oz and is currently up 0.3% at $1673.10/oz. Silver is about 1% off its session high of $32.56/oz and is currently up 1.7% at $32.16/oz. Copper futures are currently up 3% at $3.41/lb.DJ30 +80.53 NASDAQ +24.83 SP500 +9.96 NASDAQ Adv/Vol/Dec 1379/423 mln/895 NYSE Adv/Vol/Dec 2128/169 mln/685

10:00 am : The S&P 500 continues to sport an impressive gain, but it has started to pull back from the 1220 line, which was a point of resistance this past Wednesday. The line essentially represents the stock market's two-month closing high.

The preliminary Consumer Sentiment Survey for September from the University of Michigan came in at 57.5, which is down from the 59.4 that was posted in the prior month, but also less than the 60.0 that had been expected, on average, among economists polled by Briefing.com.

Business inventory numbers for August were also just released. They increased by 0.5%, which is slightly better than the 0.4% increase that had been broadly expected to follow a 0.4% increase in the prior month. DJ30 +115.19 NASDAQ +33.56 SP500 +14.84 NASDAQ Adv/Vol/Dec 1680/112 mln/385 NYSE Adv/Vol/Dec 2465/60 mln/230

09:45 am : Stocks are sporting strong gains in the early going. The effort has been broad based in that all 10 major sectors are in positive territory. More than half of them are sporting gains in excess of 1%.

Strength among stocks has Treasuries under pressure. In turn, the yield on the benchmark 10-year Note is now up to 2.25%, which is about 50 basis points above the depths that it probed barely 10 days ago.

Meanwhile, the dollar continues to descend against the euro, which is up a sharp 1.0% to $1.387 this morning. That's right in line with the euro's one-month high and just shy of its 50-day moving average. DJ30 +121.25 NASDAQ +36.73 SP500 +16.60 NASDAQ Adv/Vol/Dec NA/NA/NA NYSE Adv/Vol/Dec NA/NA/NA

09:15 am : S&P futures vs fair value: +14.80. Nasdaq futures vs fair value: +31.20. The broad market ended the prior session with a modest loss, but it appears poised for a markedly positive open today. Stocks enter Friday more than 4% higher than where they began the week. Buying has been largely based on the actions of Europe, where improved sentiment has helped the continent's major bourses trend higher, even in the face of a recent downgrade of Spain's debt. Buying interest got a boost from a better-than-expected monthly retail sales report, which was released earlier. As for earnings, they don't really get going until next week, but for now, Google (GOOG) has impressed many by posting a significantly better-than-expected quarterly report. That said, many participants continue to keep an eye on financials, which weighed heavily on trade yesterday, after analysts at Fitch placed several investment banks and brokerages on the firm's Negative Watch list.

09:05 am : S&P futures vs fair value: +13.50. Nasdaq futures vs fair value: +28.50. Strength in the commodity complex has the CRB Commodity Index up a healthy 1.4% today. Among its more closely monitored components, oil prices are up a sharp 2.5% to $86.35 per barrel in the first few minutes of pit trade. The upward push comes after the energy component slid to a 1.6% loss. Natural gas prices are currently up 2.0% to $3.60 per MMBtu. They actually registered a 52-week low of $3.45 per MMBtu in the prior session, but rebounded to a 1.2% gain. Gold prices are up 0.8% to $1681 per ounce today. That recoups the 0.8% that the precious metal shed in the prior session. As for silver, it was last quoted with a 1.8% gain at $32.22 per ounce. It fell 3.0% yesterday.

08:35 am : S&P futures vs fair value: +13.60. Nasdaq futures vs fair value: +28.50. Stock futures have ticked higher in recent action. The bidding follows the latest dose of data, which featured news that retail sales increased by 1.1% during September. They had been broadly expected to increase by 0.6% after an upwardly revised 0.3% increase for the prior month. Excluding autos, retail sales were up by 0.6%. That also exceeded what had been widely anticipated, which was a 0.3% increase. Sales less autos for the prior month were revised higher, too. They now show an increase of 0.5%. Separately, import prices increased by 0.2% in September, as they did in the prior month. Export prices, excluding agricultural items, increased by 0.3%, just as they did in August.

08:05 am : S&P futures vs fair value: +10.30. Nasdaq futures vs fair value: +21.50. The broad market ended the prior session above its low, but was unable to garner enough support to post an actual gain. There is a more upbeat tone to trade this morning, though. In turn, stock futures point to a strong start to the final session of the week. Per usual, early participants are taking their cues from Europe, where the continent's major bourses have climbed to strong gains, dismissing news that analysts at Fitch downgraded Spain's debt and cut the rating of UBS (UBS). Analysts at Fitch have also placed Morgan Stanley (MS), Goldman Sachs (GS), Deutsche Bank (DB), Barclays (BCS), Credit Suisse (CS), and BNP Paribas on the firm's Negative Watch list.

Data from Europe featured a 3.0% increase in final CPI for September. Last night China reported a 6.1% increase in its September CPI. Most of Asia's averages logged losses in overnight action.

Google (GOOG) is among the few that have reported quarterly results since the prior session's close. Its better-than-expected results have driven shares some 7% higher ahead of the open.

There's a substantial dose of data on tap for today. The bottom of the hour brings monthly retail sales, along with import and export price data. The preliminary Consumer Sentiment Survey for October from the University of Michigan will be widely available at 9:55 AM ET. Monthly business inventory numbers follow immediately with a release at 10:00 AM ET. The latest Treasury Budget will be posted at 2:00 PM ET.

06:51 am : [BRIEFING.COM] S&P futures vs fair value: +8.90. Nasdaq futures vs fair value: +21.50.

06:51 am : Nikkei...8747.96...-75.30...-0.90%. Hang Seng...18501.79...-256.00...-1.40%.

06:51 am : FTSE...5459.67...+56.30...+1.00%. DAX...5961.50...+46.70...+0.80%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage