Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, this public trade journal contains

useful trading tips a few times per week to encourage readers to return for more information and to help ensure I myself don't forget the importance of basic concepts within my own trading plan. Further, there are

market summaries from Youtube Bloomberg, CNNMoney and Yahoo Finance as a quick archive of what happened in the markets on a particular day of trading. Thus, if you're looking for trading tips and market summaries that can improve your trading and/or understanding of what happen on a particular day that involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader.

Today's

#FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=77&t=608 click on the below images to view normal sizeAttachment:

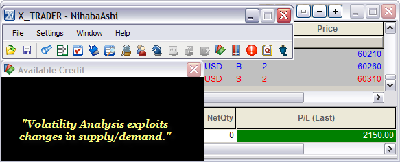

083110_wrbtrader_PnL_Blotter_Profit.png [ 32.62 KiB | Viewed 423 times ]

083110_wrbtrader_PnL_Blotter_Profit.png [ 32.62 KiB | Viewed 423 times ]

Trade Performance for Today: +21.50 points or $2150 dollars in the ICE Russell 2000 Emini TF ($TF_F) Futures.

1 tick or 0.10 = $10 dollars and to find out more contract information about the Russell 2000 Emini TF...

click here.

Quote:

Today's results are 5 wins : 3 losses (see above #FuturesTrades log). I concentrated on trade management after entry because it has been my weakness via not following the trading plan this entire month. However, to be fair, it's usually like that during August for me as I try to take it easy to re-energize going into the fall (October and November) trading session. Anyways, 3 of my 5 winners had excellent trade management especially the first trade.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about any thing related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=119. However, you must join the TSL Support Forum to access the free study guide. To register...

click here.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm Daily Trade Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=120&t=731------------------------------

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.  U.S. Stocks Rise on Consumer Confidence, Home Price Data: Video

U.S. Stocks Rise on Consumer Confidence, Home Price Data: Video Aug. 31 (Bloomberg) -- Bloomberg's Elizabeth Faublas reports on the performance of the U.S. equity market today. Stocks rose, trimming the biggest August slump since 2001, as regulators approved a Chinese investment in Morgan Stanley and gains in home prices and consumer confidence tempered concern the economy is faltering.

Stocks End August With A Whimper Attachment:

![chart_ws_index_dow.top[2].png](./download/file.php?id=710&t=1&sid=54d905ba46d87da9c7df8d0ca8b58827) chart_ws_index_dow.top[2].png [ 13.38 KiB | Viewed 456 times ]

chart_ws_index_dow.top[2].png [ 13.38 KiB | Viewed 456 times ]

By Ben Rooney, staff reporter

August 31, 2010: 5:41 PM ET

NEW YORK (CNNMoney.com) -- Stocks were little changed at the end of a choppy session Tuesday, closing out a lackluster August for the market as investors weighed meeting minutes from the Federal Reserve against upbeat economic reports.

The Dow Jones industrial average (INDU) gained 4 points, or less than 0.1%. The S&P 500 (SPX) edged up less than 1 point. The Nasdaq (COMP) composite lost 6 points, or 0.3%.

All three indexes posted monthly declines. The Dow lost about 4.3% in August, while the S&P 500 fell 4.7%, and the Nasdaq slumped 6.2% in the month.

The lackluster performance in August came after stocks rallied 7% in July on strong profit growth from major U.S. corporations. But the market is still down for the year. The Dow has lost nearly 4% so far in 2010.

On Tuesday, stocks were supported earlier in the session by a larger-than-expected rise in consumer confidence and a jump in U.S. home prices. But the tone turned bearish late in the day after the Fed released minutes from its Aug. 10 meeting.

The minutes raised concerns that the central bank may not take steps to support the faltering economic recovery unless conditions deteriorate significantly, said Dan Cook, senior market analyst at IG Markets.

"The market was anticipating that they would get in with a bit of a slowdown," he said. "But the minutes suggest that things will have to get a lot worse."

Cook said trading will probably remain volatile as investors await key economic reports due later this week, including the government's closely watched monthly jobs numbers on Friday.

"It's hard to be long or short ahead of the non-farms payroll report," he said.

Investors have been focused on the outlook for the U.S. economy recently as the nation's growth has slowed. In particular, they are worried that the weak job market will continue to weigh on consumer spending -- which drives the bulk of economic activity.

Economic reports due Wednesday morning include an index of nationwide manufacturing activity and a report on private sector job cuts in August. In addition, major automakers report August sales figures throughout the day.

The uncertainty surrounding the economic outlook and historically low trading volumes led to increased turbulence on Wall Street during August. The CBOE Market Volatility Index, or VIX (VIX), rose more than 18% in August to 26.05.

Trading volumes continued to be light Tuesday with many market participants on vacation this week. Stocks dropped more than 1% in thin trading Monday.

Economy: Investors welcomed a slight improvement in the economic news Tuesday with better-than-expected readings on consumer confidence and home prices.

The Conference Board's index of consumer confidence rose to a reading of 53.5 in August from an adjusted 51 in July. Economists were expecting the index to come in at 50, according to consensus estimates from Briefing.com.

The rebound in confidence numbers was attributed mostly to an improvement in how consumers view the short-term economic outlook, the Conference Board said. Meanwhile, the weak job market continues to darken their long-term view.

"The comfort in this release is that confidence did not fall further," said Paul Dales, an economist at Capital Economics. "But there are few signs that households will ramp up their spending."

Separately, the Chicago PMI, a regional reading on manufacturing activity, fell to 56.7 in August. That's down from 62.3 in July and slightly weaker than expected. Economists were looking for 57 in August.

Before the market opened, a report showed that national home prices jumped a substantial 3.6% in the past year, versus a forecasted 3.1% gain. The S&P/Case-Shiller Home Price Index also showed that prices climbed 4.4% in the second quarter, compared with a 2.8% plunge in the first quarter.

Investors are especially wary ahead of Friday's big employment report, which is expected to show that the economy lost jobs for a third month in a row in August.

Economists expect employers to have shed 120,000 jobs in August, after cutting payrolls by 131,000 in July. The unemployment rate is forecast to creep up to 9.6% from 9.5%.

Companies: Technology shares came under pressure after research firm Gartner lowered its forecast for PC sales in the second half of 2010, citing an uncertain economic outlook in the United States and Europe.

The Philadelphia Semiconductor Index, or SOX (SOX), fell nearly 2%.

Monsanto (MON, Fortune 500) fell almost 6% after the company warned that its fiscal year earnings per share will be at the lower end of its forecasted range. The agribusiness giant said it expects to earn between $2.40 and $2.45 a share this fiscal year. Analysts surveyed by Thomson Financial expect $2.48 per share.

Shares of Saks Inc. (SKS) spiked 20% after a report from the Daily Mail said a group of U.S. and U.K. private equity companies may soon bid $1.7 billion, or $11 per share, for the high-end retailer.

Data-storage company 3PAR (PAR) rose nearly 1% as a Reuters survey revealed that most analysts and investors expect Dell (DELL, Fortune 500) to bow out of the bidding war with Hewlett-Packard Co. (HPQ, Fortune 500) Dell has until Wednesday to match HP's $2 billion bid for 3PAR.

World markets: European shares closed higher. The CAC 40 in France edged up 0.1%, the DAX in Germany rose 0.2%, Britain's FTSE 100 gained 0.4%.

Asian markets ended lower. Japan's benchmark Nikkei index sank 3.6% to a 16-month closing low. The Shanghai Composite decreased 0.5% and the Hang Seng in Hong Kong lost 1%.

Meanwhile, India's economy grew by 8.8% during the three months ended June 30. That compares with 8.6% during the previous quarter and 6% growth during the same quarter a year ago.

Currencies and commodities: The dollar edged lower against the euro and the Japanese yen but was higher versus the British pound.

Oil futures for October delivery fell $3 to $71.70 a barrel. Gold for December delivery gained $11.10 to $1,250.30 an ounce.

Bonds: The yield on the 10-year Treasury note fell to 2.48% from 2.54% late Monday.

Yahoo! Finance

Yahoo! Finance 4:35 pm : August finished on a flat note after a bit of end-of-month buying fizzled into the close. The lackluster finish left stocks to lock in another marked monthly loss.

Technical support at the 1040 line helped the S&P 500 bounce back from an opening slide. The rebound initially paused near the neutral line, but stocks then pushed into positive territory with the release of the Conference Board's Consumer Confidence Index for August. The Index climbed to 53.5 from 51.0. It was widely expected to slip to 50.0.

The broader market gave more weight to the consumer confidence reading than the generally anecdotal and entirely regional Chicago PMI, which came in at 56.7 for August. Not only did that figure fall short of the consensus of 57.0, but it was also the lowest since November 2009.

There was little reaction among market participants to the minutes from the August 10 FOMC meeting. As expressed in Fed Chairman Bernanke's speech last week, the minutes indicated that the pace of the economic recovery slowed in recent months. However, many policymakers judged that downside risks to the U.S. recovery had become somewhat larger.

Interest among buyers has been unsustainable in recent weeks, but there was some modest end-of-month buying, which helped drive some midsession gains and took trading volume above recent averages. However, many participants remain unwilling to jump back into stocks ahead of the monthly payrolls report. A glimpse into the official figures (due Friday) will come with the ADP Employment Change tomorrow morning. Caution ahead of the report left stocks to crawl to a flat finish.

Weakness of the past couple of weeks culminated with a 4.7% loss for the S&P 500 during August. That poor performance marks the stock market's third monthly loss in four months.

Amid such weakness the yield on the 10-year Note fell more than 40 basis points to close out August near 2.47%. It registered its 19-month low of 2.42% just last week.

Though stocks have been weak in recent weeks and there is a growing concern about the tenuous footing of the economy, merger and acquisition activity continues on. Most recently, Exelon (EXC 40.72, +0.20) announced it will acquire the renewable energy unit of Deere & Co. (DE 63.27, +0.29) in a deal valued at some $900 million.

Dow component 3M (MMM 78.55, -1.10) will pay an investor group $230 million to acquire Attenti Holdings S.A. That announcement came after 3M agreed to acquire Cogent (COGT 11.00, -0.09) just yesterday.

In other corporate news, Monsanto (MON 52.65, -3.25) issued a tepid revenue forecast, which caused it to fall sharply out of favor. Shares of MON were among this session's worst performing issues.

Advancing Sectors: Telecom (+1.1%), Financials (+0.9%), Utilities (+0.4%), Materials (+0.3%), Consumer Staples (+0.2%), Consumer Discretionary (+0.1%)

Declining Sectors: Tech (-0.6%), Health Care (-0.4%), Industrials (-0.3%), Energy (-0.2%)DJ30 +4.99 NASDAQ -5.94 NQ100 -0.3% R2K +0.1% SP400 +0.00% SP500 +0.41 NASDAQ Adv/Vol/Dec 1264/2.12 bln/1320 NYSE Adv/Vol/Dec 1654/1.40 bln/1332

3:30 pm : The CRB Commodity Index ended lower by 1.3% today, led by the substantial 2.4% sell off in the energy sector. That sell off was anchored by Oct crude oil, which shed 3.7% to settle at $71.92 per barrel. The flight from risk assets, to safety, weighed on crude oil today. Sept natural gas closed higher by 0.1% to $3.82 per MMBtu.

Precious metals were the largest advancing sector today, adding 1.2%. Dec gold finished higher up 0.8% to $1250.30 per ounce, while Dec silver settled up 1.5% to $19.43 per ounce. Concerns about the state of the economy lead to a flight to safety today. Gold put in session highs at $1251.80 -its best level in two months. DJ30 -29.86 NASDAQ -15.75 SP500 -3.84 NASDAQ Adv/Vol/Dec 1087/1.5 bln/1489 NYSE Adv/Vol/Dec 1391/704.6 mln/1572

3:00 pm : Stocks recently rolled over so that they now trade with a modest loss. Should the pressure persist into the close it will mark the stock market's seventh slide in nine sessions. Stocks are already on pace for a monthly loss of more than 4%, which actually makes for the stock market's worst August since 2001.DJ30 -9.62 NASDAQ -10.47 SP500 -1.79 NASDAQ Adv/Vol/Dec 1142/1.37 bln/1395 NYSE Adv/Vol/Dec 1451/640 mln/1497

2:30 pm : Stocks have slipped back to the neutral line amid mixed action in the broader market.

There wasn't much of a reaction among market participants to the minutes from the August 10 FOMC meeting. The minutes, which were released at 2:00 PM ET, indicated that the pace of the economic recovery slowed in recent months and that inflation remained subdued. However, many policymakers judged that downside risks to the U.S. recovery had become somewhat larger. DJ30 +7.72 NASDAQ -3.65 SP500 +0.08 NASDAQ Adv/Vol/Dec 1379/1.19 bln/1136 NYSE Adv/Vol/Dec 1695/560 mln/1232

2:00 pm : Stocks are stuck in a relatively narrow range, but the action has kept them in positive ground.

Telecom has managed to make its way to a fresh session high. The sector is now up 1.4%. Should the gain hold, it would market the telecom's best single-session performance in about four weeks. That would help solidify the telecom sector's monthly gain, which currently stands at about 2.5%. In contrast, the broad-based S&P 500 is on track for a monthly loss of about 4.5%.

Minutes from the latest FOMC meeting are hitting newswires. A summary will be posted when available. DJ30 38.22 NASDAQ +1.98 SP500 +3.58 NASDAQ Adv/Vol/Dec 1511/1.08 bln/996 NYSE Adv/Vol/Dec 1933/498 mln/986

1:30 pm : Stocks recently drifted back toward the neutral line, but they have since bounced back to a modest gain. Since making their way into higher ground, stocks have found support at the flat line -- they have tested it three times since turning positive.

Though stocks continue to trade with modest gains, Treasuries remain in favor. Specifically, the benchmark 10-year Note is up 14 ticks, which has been enough to take its yield back below 2.5%. DJ30 +44.19 NASDAQ +4.10 SP500 +3.91 NASDAQ Adv/Vol/Dec 1569/1.00 bln/926 NYSE Adv/Vol/Dec 1964/465 mln/955

1:05 pm : An opening slide sent the stock market toward its monthly low, but technical support and an upbeat consumer confidence reading invited some end-of-month buying that took stocks to higher ground. However, waning support has taken the stock market back near the neutral line.

The prior session's slide extended into early trade as market participants further pared their positions. Sellers took the S&P 500 back down to the 1040 line, but technical support there provided a floor for stocks once again.

Stocks extended their bounce off of the morning low amid news that the Conference Board's Consumer Confidence Index increased more than expected to 53.5 from 51.0. That overshadowed a disappointing Chicago PMI, which came in at 56.7 for August.

Though stocks were able to push into positive territory this morning, broader market support has started to fade.

Financials are still up nicely. The sector's 0.8% gain makes it one of today's best performers. Bank stocks have been a boon to the sector. Their bounce comes after the KBW Bank Index tested 2010 lows in the prior session.

Telecom stocks, typically considered defensive issues, have also been strong performers. They are up 1.1%, collectively.

Conversely, tech stocks have lagged for the entire session. The sector's 0.3% loss comes as large-cap tech issues lose luster. Their weakness has also hampered the Nasdaq, which has trailed the Dow and S&P 500 for a modest margin all session.

Corporate headlines have been relatively limited. Among the more notable announcements, Monsanto (MON 52.57, -3.33) issued a tepid revenue forecast, while Exelon (EXC 40.43, -0.09) announced it will acquire the renewable energy unit of Deere & Co. (DE 63.55, +0.57) in a deal valued at some $900 million.

Coming up at 2:00 PM ET, minutes from the latest FOMC meeting will be released. The minutes come after Fed Chairman Bernanke's comments last week about the economy and its outlook. DJ30 +27.47 NASDAQ +0.04 SP500 +2.52 NASDAQ Adv/Vol/Dec 1460/945 mln/1011 NYSE Adv/Vol/Dec 1859/435 mln/1062

12:30 pm : Stocks are drifting off of their session highs. Both tech stocks (-0.2%) and energy stocks (-0.1%) are causing a drag -- together the two sectors represent almost 30% of the S&P 500's market weight. While the tech sector continues to be bogged down by large-cap tech issues, the energy sector has been undercut by a 2.7% drop in oil prices to $72.70 per barrel.

Meanwhile, Treasury yields have made their way back toward session highs. Specifically, the yield on the benchmark 10-year Note is now down to 2.48%. Its 19-month low stands near 2.42%.DJ30 +36.85 NASDAQ +2.44 SP500 +2.86 NASDAQ Adv/Vol/Dec 1501/830 mln/938 NYSE Adv/Vol/Dec 1929/391 mln/973

12:00 pm : The S&P 500 has made a modest move higher. It now trades at its best level of the day.

Financials have sprinted out to a 1.1% gain. The sector had been performing in-line with the broader market, but is now one of this session's best. The financial sector's bounce comes as bank stocks, represented by the KBW Bank Index, climb 1.4% after they tested 2010 lows during the prior session. DJ30 +49.98 NASDAQ +3.84 SP500 +4.57 NASDAQ Adv/Vol/Dec 1486/762 mln/935 NYSE Adv/Vol/Dec 2019/362 mln/869

11:30 am : The neutral line has been a steady floor for the S&P 500 for the past couple of hours. In turn, stocks continue to chop along with modest gains.

Monsanto (MON 53.00, -2.90) has been a notable laggard this session. Shares of the company have been shunned in the wake of the company's tepid revenue forecast.

Elsewhere in the basic materials space, gold and silver plays are faring well. For instance, Newmont Mining (NEM 61.45, +1.53) is up by more than 2%. Meanwhile, the SPDR Gold ETF (GLD 121.84, +0.93) is up almost 1%. DJ30 +33.60 NASDAQ -0.65 SP500 +2.99 NASDAQ Adv/Vol/Dec 1366/670 mln/1036 NYSE Adv/Vol/Dec 1868/320 mln/978

11:00 am : The Dow and S&P 500 are still in positive territory with modest gains after being backed down to the neutral line. The Nasdaq is flat at the moment.

Telecom stocks, typically considered defensive in nature, are sporting the best gains of this session. The sector is up 1.0% as Verizon (VZ 29.81, +0.37) and AT&T (T 26.88, +0.25) provide leadership.

Tech stocks are lagging. The sector is down 0.2% as large-cap tech plays like Intel (INTC 17.90, -0.06) and Research In Motion (RIMM 43.62, -1.97) come under pressure. Their weakness has also weighed on the tech-rich Nasdaq. DJ30 +35.42 NASDAQ +0.56 SP500 +2.93 NASDAQ Adv/Vol/Dec 1362/549 mln/973 NYSE Adv/Vol/Dec 1870/268 mln/932

10:30 am : Recent weakness in the dollar index gave select commodities a boost.

October crude oil rallied over a dollar back to the unchanged line in recent activity. However, crude is now back in negative territory at $74.37 per barrel, down 0.4%.

The October crude contract hit new lows of $71.63 per barrel last Tuesday. Last week, crude closed 1.9% higher, but is down for a second day in a row so far in this week's trade.

October natural gas is not benefitting from weakness in the dollar index as the energy component fell in the red two hours ago, hitting new session lows of $3.73 per MMBtu less than an hour ago. Currently, the energy component is trading 1.1% lower at $3.77 per MMBtu.

Precious metals rallied just after the open of pit trading this morning with December gold pushing to morning highs of $1249.40 per ounce and December silver rising to its own fresh morning highs of $19.34 per ounce. Gold is currently 0.6% higher at $1246.40 per ounce. Silver is up 1.1% at $19.28 per ounce.DJ30 +31.03 NASDAQ +3.04 SP500 +2.73 NASDAQ Adv/Vol/Dec 1403/409.8 mln/878 NYSE Adv/Vol/Dec 1841/201.0 mln/912

10:05 am : The stock market recently extended its bounce off of the 1040 line, but paused as it came close to the neutral line. It has since moved another leg higher with the release of the August Consumer Confidence Index, which came in at 53.5. DJ30 +16.57 NASDAQ +1.71 SP500 +1.29 NASDAQ Adv/Vol/Dec 1215/283 mln/966 NYSE Adv/Vol/Dec 1586/150 mln/1104

09:45 am : The S&P 500 started the session with a sharp slide lower, but the 1040 line provided support. Stocks remain in the red, but the 1040 line continues to act as a floor for trade.

The Chicago PMI for August hit 56.7, which is below the 57.0 that had been expected, on average, by a sample of economists polled by Briefing.com. What's more, the August reading is the lowest since November 2009. DJ30 -46.02 NASDAQ -15.94 SP500 -6.36

09:15 am : S&P futures vs fair value: -3.70. Nasdaq futures vs fair value: -6.50. The stock market fell for the sixth time in eight sessions yesterday. It now heads into the final session of August facing a monthly loss of almost 5%. The tone to premarket trade has improved a bit in the past few minutes, though. Earlier it looked like stocks would open with a marked loss near monthly lows. Initial weakness this morning came amid broad selling efforts overseas and a sense of uncertainty ahead of the always-pivotal jobs report on Friday. Market participants get a glimpse into the report with the release of the ADP Employment Change tomorrow morning. Today has already brought the latest S&P/CaseShiller Home Price Index, which improved modestly from the prior month. Still on the way are Chicago PMI (9:45 AM ET), Consumer Confidence (10:00 AM ET), and minutes from the latest FOMC meeting (2:00 PM ET). As an aside, the dollar has slipped to a new morning low, such that it now trails a basket of major foreign currencies by 0.3%. Most of its loss stems from strength in the euro and yen. The euro is currently up 0.6% to trade at $1.27 while the yen is currently up 0.3% to 84.4 yen per dollar, which puts it close to its 15-year high.

09:00 am : S&P futures vs fair value: -6.80. Nasdaq futures vs fair value: -11.50. Stock futures have made a fractional improvement with the release of the S&P/CaseShiller Home Price Index for June. It came in at about 148.0, which is an improvement from the 146.5 that was recorded in the prior month. The 20-City Composite for June increased at a seasonally adjusted 0.3% month-over-month after it had made a 0.5% monthly increase in May. Up next on the economic calendar is the Chicago PMI, which is due for release at 9:45 AM ET. It will be followed by the Consumer Confidence Index for August at 10:00 AM ET, then the minutes from the latest FOMC meeting at 2:00 PM ET.

08:30 am : S&P futures vs fair value: -8.50. Nasdaq futures vs fair value: -11.80. Futures for the S&P 500 continue to point to a lower start that could test monthly lows. Meanwhile, Germany's DAX has dropped to a 0.8% loss. It is currently on pace for a monthly loss of almost 5%. Of its 30 components only Bayer AG, Man SE, and Henkel AG have managed to make gains this session. Infineon Tech is and Commerzbank are among the worst performers. The couple also trades with some of the heaviest share volume of the session. As for Germany's unemployment rate, it stayed steady at 7.6% in August. In France, the CAC has fallen to a 1.1% loss. That puts it on pace for a monthly loss of little more than 5%. Vivendi, Pernod-Ricard, and Vallourec have managed to stage modest gains, but the other 37 issues in the Index are in the red. Sanofi-Aventis (SNY) is under some of the stiffest pressure. In Britain, the FTSE has fallen 0.9%, which has added to its month-to-date loss of about 3%. About 90% of the FTSE's components are in the red. BP Plc (BP) and Barclays (BCS) are under some of the most pressure, while Reckitt Benckiser and HSBC (HBC) show strength. In economic data, Consumer Confidence in the United Kingdom improved to -18 for August from -22 for July. In the broader eurozone, CPI for August showed a 1.6% increase, up from 1.7% in the prior month. The eurozone's unemployment rate for August was reported at 10%, unchanged month-over-month.

In Asia, Japan's Nikkei plummeted 3.6%. There wasn't a single stock in the 225-member index that managed to muster a gain. Such weakness left the Nikkei to end August with its lowest close more than 15 months and finish August with a 7.5% monthly loss. The selloff in Japan was partly owed to weakness in the U.S. on Monday, but also to continued concern about the implications of a stronger yen. The yen has extended its rally from the prior session so that it now trades near 84.3 yen per dollar - its 15-year high stands near 83.6 yen per dollar. Japan's economic news included the August Nomura Manufacturing PMI, which came in at 50.1, down from 52.8 in July. Industrial Production for July increased 0.3%, which is an improvement from the 1.1% drop in the prior month. Mainland China's Shanghai Composite closed 0.5% lower for the session, but made it out of the month essentially unchanged. PetroChina (PTR), China Petroleum (SNP), Bank of China, and Industrial & Commercial Bank were primary culprits in the final session of August. Hong Kong's Hang Seng shed 1.0% in the final session of August. It fell more than 2% for the month. Financial plays HSBC, China Construction Bank, and Industrial & Commercial Bank proved heavy drags on trade. China Mobile was also a laggard.

08:00 am : S&P futures vs fair value: -6.30. Nasdaq futures vs fair value: -8.50. Stocks dropped sharply in thin volume during the prior session, but the weakness of this morning's premarket trade suggests that sellers are not yet ready to stop their efforts. Sellers have also had their way with overseas markets, most of which moved markedly lower overnight and in early morning trade. There haven't been any earnings announcements of interest, but merger and acquisition activity continues to chug along. Most recently, Exelon (EXC) announced it will acquire the renewable energy unit of Deere & Co. (DE) for some $900 million. The S&P/CaseShiller Home Price Index for June is due at 9:00 AM ET. That is followed by the release of the Chicago Purchasing Manager Index for August at 9:45 AM ET. The Conference Board's Consumer Confidence for August is due at 10:00 AM ET. Minutes from the latest FOMC meeting are due at 2:00 PM ET.

06:39 am : S&P futures vs fair value: -5.60. Nasdaq futures vs fair value: -7.50.

06:39 am : Nikkei...8824.06...-325.20...-3.60%. Hang Seng...20536.49...-200.70...-1.00%.

06:39 am : FTSE...5151.81...-49.80...-1.00%. DAX...5867.00...-45.30...-0.80%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries. Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage