Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=73&t=506.

Quote:

Today's results are 9 wins : 6 losses. A great trading day and all the losses were minimized via keeping them at/below -0.6 ticks on each losing trade. In comparison, I had several profitable trades go for multiple points per contract. Simply, let your winners run and keep your losses small. As for today's volatility, awesome but only due to the growing fear concerning the global economic recovery could relapse after Greece's and Portugal had their credit rating lowered.

In fact, today is a good example of why some traders miss capturing a big trend day because most big trend days are news related and if you don't pay attention to eye popping news...you aren't going to let profits run (stay in profitable trades longer) and you'll be scratching your head about what happen today. It's the news that created the volatility.

Trading Tip: Global economies are more inter-connected. Therefore, the markets are often strongly influenced via what is occurring in foreign economies. Therefore, it pays to pay attention to the price action of markets in other countries...a type of intermarket analysis.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

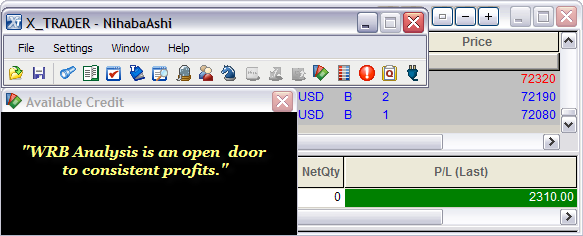

+23.10 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

042710_wrbtrader_PnLBlotterProfit.png [ 32.26 KiB | Viewed 1645 times ]

042710_wrbtrader_PnLBlotterProfit.png [ 32.26 KiB | Viewed 1645 times ]

------------------------------

Dow Plunges 213 points, Breaks Below 11,000 By Alexandra Twin, senior writer

April 27, 2010: 6:04 PM ET

NEW YORK (CNNMoney.com) -- Stocks fell Tuesday after Standard & Poors cut Greece's debt rating to junk and lowered Portugal's debt rating, raising fears that a euro zone debt crisis could slow the global economic recovery.

The Dow Jones industrial average (INDU) tumbled 213 points, or 1.9%, closing below 11,000, a key psychological level. The Dow ended the previous session at its highest point in 19 months.

The slide was the Dow's biggest one-day point drop since July 15, 2009, when it lost 257 points.

The S&P 500 index (SPX) fell 28 points, or 2.3%, closing below 1,200, a psychological level traders look at. The Nasdaq composite (COMP) slid 51 points, or 2%.

Stocks were flat to lower in the morning as Goldman Sachs sought to defend itself on Capitol Hill against allegations it profited from the housing market collapse. But news that ratings agency Standard & Poor's had cut Greece and Portugal's debt ratings overshadowed everything else, giving investors a reason to retreat on the back of an 8-week advance.

"We're seeing the fear factor kick in about Greece and Portugal," said Peter Cardillo, chief market economist at Avalon Partners. "That's rattling the market."

He said that fear was also reflected in the so-called flight to quality as investors poured money into bonds and the euro fell to a new low for the year.

That was reflected by a jump in the CBOE Volatility index, Wall Street's so-called "fear gauge." It spiked 24%, hitting the highest point since February. Typically a surge in the VIX corresponds with a selloff in stocks.

Greece: Standard & Poor's cut its ratings on Greece's long-term debt status to "BB+" with a negative outlook from "BBB+." The double-B plus rating is considered to be speculative or "junk," and reflects the ratings agency's concern about Greece's long-term ability to get out from underneath the its current fiscal crisis. S&P cut Greece's short-term debt even lower.

S&P also cut Portugal's long-term debt ratings by two notches and the short-term rating by one notch, but did not lower the debt to junk status.

The cost of insuring both Greece and Portugal's debt rose to record highs following the news.

Worries about the fiscal health of Greece and the other so-called PIIGS have weighed on the stock market on and off since the start of the year as investors worry the weakness will destabilize the euro and hurt global growth. The PIIGS are Portugal, Ireland, Italy, Greece and Spain.

Greece, Portugal debt gets slashed

However, Cardillo said that markets were also ripe for a pullback after moving higher for the last few months.

Rally loses steam: The Dow has ended higher for eight straight weeks, its best winning streak since January 2004. The Nasdaq has also been on the rise for 8 weeks, while the S&P 500 rose for 7 of the last 8 weeks.

Prior to Monday's selloff, the Dow and S&P 500 were just shy of 19-month highs, while the Nasdaq was at the highest point in nearly two years.

A better-than-expected reading on consumer confidence, a weaker-than-expected rise in a key measure of the housing market and anticipation at the start of the Federal Reserve's two-day policy setting meeting were all in play. Better-than-expected results from Texas Instruments, DuPont and 3M provided some support.

Stocks were barely higher Monday in a quiet session at the start of a busy week on Wall Street. In addition to the housing and consumer confidence reports, a revised reading on first-quarter GDP growth is due later in the week, as well as quarterly results from roughly one-third of the companies in the S&P 500.

Goldman execs fire back

Goldman: CEO Lloyd Blankfein and other executives from Goldman Sachs were answering lawmakers' questions as part of a Senate hearing on the role investment banks played in the financial market meltdown in 2008.

Blankfein, in prepared testimony, denied that the company sought to profit from the housing market collapse, an allegation lawmakers have made recently.

Fabrice Tourre, the trader charged in the Securities and Exchange Commission's fraud case against Goldman Sachs defended himself, saying he categorically denied the SEC's allegations.

On the move: Financials, energy and technology, the three biggest movers of the market in terms of sectors, all fell.

Goldman Sachs (GS, Fortune 500) gained 1%, but other bank shares plunged, with the KBW (BKX) Bank index losing over 3%. Sliding oil prices dragged on energy stocks, including Dow components Exxon Mobil (XOM, Fortune 500) and Chevron (CVX, Fortune 500).

Declines were broad based, with 28 of 30 Dow components falling. In addition to the Dow's financial and energy components, other losers included heavily weighted tech stocks Hewlett-Packard (HPQ, Fortune 500) and IBM (IBM, Fortune 500), aerospace and defense names Boeing (BA, Fortune 500) and United Technologies (UTX, Fortune 500) and heavy-machinery maker Caterpillar (CAT, Fortune 500).

Caterpillar shares rallied Monday after the company reported better-than-expected earnings and boosted its 2010 profit forecast.

Market breadth was negative. On the New York Stock Exchange, losers beat winners five to one on volume of 1.68 billion shares. On the Nasdaq, decliners topped advancers by over four to one on volume of 2.77 billion shares.

0:00 /2:38Goldman loyalty: Client or firm?

Economy: On the economic front, investors took in reports on home prices and consumer confidence.

The Case-Shiller 20 city home price index rose 0.6% in February versus a year earlier, the first rise on an annual basis in three years. However, economists surveyed by Briefing.com were expecting a bigger gain of 1.1%. Prices fell 0.7% in January.

Consumer confidence surged in April, according to the Conference Board, with its index rising to 57.9 from 52.3 in March. Economists thought it would rise to 53.5.

Debt commission: Policymakers need to put a plan in place to get spending in line with revenue so as to close the unsustainable fiscal gap threatening the recovery, Federal Reserve Chairman Ben Bernanke said Tuesday.

Bernanke spoke at the first meeting of President Obama's bipartisan debt commission.

Federal Reserve: The central bank policymakers were meeting Tuesday and Wednesday with an announcement on interest rates and the outlook due Wednesday afternoon.

The Ben Bernanke-led Fed is expected to hold interest rates steady at historic lows near zero. However, what the bankers say in the statement about the outlook for the economy and interest rates will be scrutinized.

Investors will also pay attention to whether the Fed provides more details about how it plans to continue unwinding programs put in place to prop up the economy during the financial crisis.

Company news: Ford Motor (F, Fortune 500) reported a better-than-expected first-quarter profit that rose from a year earlier. But shares slumped after the company's revenue growth was shy of expectations.

After the market closed Monday, Texas Instruments (TXN, Fortune 500) reported quarterly sales and earnings that topped estimates and rose from a year earlier. Shares were slightly lower.

3M (MMM, Fortune 500) reported higher quarterly sales and earnings that topped estimates thanks largely to strong international sales. The Dow component, considered to be a good barometer of the economy because of the breadth of its business, also boosted its 2010 profit forecast.

However, 3M said growth in Asia and Latin America are the drivers of that forecast and that the U.S. economic recovery will be patchy. Shares gained 0.6%.

Fellow Dow component DuPont (DD, Fortune 500) also reported higher quarterly sales and earnings that topped expectations, and lifted its 2010 profit forecast. But investors took a sell-the-news response and sent shares nearly 4% lower.

With 40% of the S&P 500 having reported, earnings are on track to have grown 50% from a year earlier and revenues 11%, according to the latest info from Thomson Reuters.

Roughly 82% of earnings have topped estimates. Should that figure hold up, it would be the highest percentage of companies topping earnings in Thomson's history.

The dollar and commodities: The dollar gained versus the euro and fell against the yen.

U.S. light crude oil for June delivery fell $1.76 to settle at $82.44 a barrel on the New York Mercantile Exchange.

COMEX gold for June delivery rose $8.20 to settle at $1,162.20 per ounce.

World markets: In overseas trading, European markets slumped, with London's FTSE down 2.6%, France's CAC 40 down 3.8% and Germany's DAX down 2.7%. Asian markets were mixed, with Hong Kong's Hang Seng index down 1.5% and Japan's Nikkei up 0.4%.

Bonds: Treasury prices rallied, lowering the yield on the 10-year note to 3.70% from 3.82% late Monday. Treasury prices and yields move in opposite directions.

Yahoo! Finance

Yahoo! Finance 4:15 pm : A high-volume selling effort in response to downgrades on the sovereign debt of Greece and Portugal sent stocks to their worst percentage loss in more than two months, but drove the dollar to its best gain in four months.

Early trade was rather lackluster as widespread weakness among overseas markets weighed on mood of morning participants, so much that better-than-expected earnings and guidance from Texas Instruments (TXI 38.20, -1.33), 3M (MMM 87.97, +0.53), and DuPont (DD 39.40, -1.55) were generally disregarded by the broader market.

Data didn't do anything to improve the mood either. The S&P/CaseShiller 20-City Composite made its first increase since 2006 with a 0.6% year-over-year increase, but that was still weaker than the 1.3% annual increase that had been expected.

Consumer confidence climbed in April as the Conference Board's Consumer Confidence Index came in at 57.9, which was not only higher than the 53.5 that had been expected, but was the best reading since August 2008.

Weakness quickly worsened when it was learned that credit analysts at Standard & Poor's downgraded Greece's debt to junk and cut Portugal's debt two notches to A-. Subsequent selling pressure sent the Dow down roughly 150 points in just 30 minutes. It even pushed through its 20-day moving average for the first time since February. It was never able to recover and, as a result, finished near its session low.

The wave of selling sent volatility sharply higher. In fact, the Volatility Index made its way up more than 30% to its highest level since February.

Many market participants fled to the dollar for safety. That gave the greenback a 1.3% gain against a basket of foreign currencies. The euro was especially weak as it fell to 1.3179 against the buck. That puts it on par with its one-year low against the dollar.

Though the dollar drove many commodities lower, such that the CRB Commodity Index dropped 1.9%, gold gained 0.7% to close pit trade at $1162.20 per ounce. Its status as a safe haven helped it extend the advance into electronic trade.

Treasuries also garnered support. The benchmark 10-year Note advanced nearly one full point in its strongest move in just over one month. That dropped its yield below 3.70% for the first time in one month.

Trade this session was backed by heavy participation. Trading volume on the NYSE surged to nearly 1.7 billion shares, which is the most for any non-options expiration session this year. It also made for the fifth straight session in which trading volume has exceeded the 200-day moving average.

The action sets the stage for the FOMC's latest policy statement, which will be released at 2:15 PM ET. No change in interest rate targets is expected, so traders will take their cues from the FOMC's actual directive.

Advancing Sectors: (None)

Declining Sectors: Financials (-3.4%), Materials (-3.2%), Consumer Discretionary (-2.9%), Energy (-2.8%), Industrial (-2.6%), Tech (-2.0%), Utilities (-1.8%), Consumer Staples (-1.7%), Telecom (-1.2%), Health Care (-1.1%) DJ30 -213.04 NASDAQ -51.48 R2K -2.4% SP400 -2.4% SP500 -28.34 NASDAQ Adv/Dec 535/2218 NYSE Adv/Vol/Dec 493/1.66/2604

3:35 pm : Commodities lost nearly 2% this session. Practically every asset class was lower this session. Still, the largest gain in the dollar index in nearly one month did not help commodity prices.

One of the lone exceptions came from gold futures. June gold closed 0.7% higher at $1162.20 per ounce. May silver was not able to salvage a gain this session. It closed 1.2% lower at $18.12 per ounce.

Energy closed down ~1.2 % this session. June crude oil futures sold off but found support at the $82 level. It closed down 2.1% at $82.44 per barrel. May natural gas closed 1.0% lower at $4.22 per MMBtu. DJ30 -155.23 NASDAQ -41.16 SP500 -22.03 NASDAQ Adv/Vol/Dec 629/2.24/2075 NYSE Adv/Vol/Dec 1429/1.22 bln/1616

3:00 pm : The stock market has drifted back down to its session low. The 1190 line provided support for the S&P 500 earlier this session, but it has come back into focus as participants enter the final hour of trade.

Participation has been strong this session. Even with another hour still left in the session trading volume has surpassed 1.0 billion shares on the NYSE. This will most likely be the first time this year that volume on the NYSE has both exceeded 1.2 billion shares for five straight sessions and topped the 200-day moving average of 1.18 billion. DJ30 -148.12 NASDAQ -41.77 SP500 -21.53 NASDAQ Adv/Vol/Dec 671/2.00 bln/2038 NYSE Adv/Vol/Dec 550/1.09 bln/2512

2:30 pm : Weakness remains widespread. Even defensive-oriented utilities stocks are down a sharp 0.9% as broader market pressure overshadows news that Williams Co's (WMB 23.84, -0.62) raised its quarterly dividend to $0.125 per share from $0.11 per share. Meanwhile, American Electric (AEP 33.62, -0.14) increased its quarterly dividend to $0.42 per share from $0.41 per share.

Tech giant IBM (IBM 130.08, -0.65) hiked its quarterly cash dividend by a dime to to $0.65 per share from $0.55 per share. Big Blue also authorized an $8.0 billion increase in the company's stock repurchase program. That plan now holds a total of $10 billion for buybacks. DJ30 -128.55 NASDAQ -33.98 SP500 -18.04 NASDAQ Adv/Vol/Dec 750/1.87 bln/1954 NYSE Adv/Vol/Dec 611/1.01 bln/2443

2:00 pm : Trading volume has been exceptionally high this session. The increased participation comes with a flurry of headlines and a spike in participation.

Losses have been widespread this afternoon. All three major equity averages are down in excess of 1%. Such losses have combined with those incurred overseas to take the Dow Jones World Index down 1.7%. DJ30 -109.20 NASDAQ -28.07 SP500 -15.53 NASDAQ Adv/Vol/Dec 757/176 bln/1936 NYSE Adv/Vol/Dec 619/943 mln/2433

1:30 pm : Results from the Treasury's $44 billion auction of 2-year Notes produced a yield of 1.02% in a bid-to-cover rate of 3-to-1 and indirect bidder participation of 31%. The previous 2-year Note offering saw a cover ratio of 3.0 and an indirect bidder take of 34.8%.

Treasuries have eased off of their highs in recent trade. The drift doesn't necessarily come from disappointment over the auction. Rather, it is mostly from the stock market's upward crawl from session lows. The benchmark 10-year Note now trades with a 25-tick gain and the 2-year Note is up four ticks.

Auction results from longer maturities, the 5-year and 7-year, are due over the next two days. DJ30 -99.68 NASDAQ -27.84 SP500 -14.75 NASDAQ Adv/Vol/Dec 629/1.63 bln/2035 NYSE Adv/Vol/Dec 529/871 mln/2524

1:00 pm : Stocks have sold off sharply following the downgrade of Greek and Portuguese debt by Standard & Poor's. The S&P 500 is down close to 1.8% on the session, which would be its biggest one-day loss since February.

Broader market weakness has been underpinned by the downgrade of Greek debt to junk, and the accompanying downgrade of Portuguese debt two notches to A-. That news has also put tremendous pressure on the euro, sending it to 1.3212, its lowest level in over a year.

As the euro moved lower, investors sought the safe-haven of the dollar, sending commodities prices tumbling. Crude oil dropped over $2.00 to below $82.00 per barrel before finding support. Gold prices were the exception, and strengthened to near 1160 as other commodities sold off.

Those events have overshadowed better-than-expected consumer confidence numbers, and positive earnings results from Texas Instruments (TXI 38.50, -1.03), 3M (MMM 88.67, +1.23), and DuPont (DD 39.96, -0.99). The trio had offered support to the broader market in early trade.

U.S. Steel (X 57.93, -2.14) also exceeded expectations, but still posted a loss for the quarter. Shares in the company are trading lower by nearly 4%. Weakness can be found across the materials sector as selling in the space in Asia and Europe has spilled over into the U.S. Materials are the worst performing sector down collectively 2.5%.

The yield on 10-yr notes has fallen over 12 basis points to 3.693% as investors search for yield following the selloff in equities. The selloff in equities and the rise in volatility has caused the VIX to spike to 21.11, up more than 20% to its highest levels since February. DJ30 -136.94 NASDAQ -39.36 SP500 -19.38 NASDAQ Adv/Vol/Dec 595/1.5 bln/2063 NYSE Adv/Vol/Dec 493/806 mln/2553

12:30 pm : A hearing held by the Senate Permanent Subcommittee on Investigations on the role of Goldman Sachs (GS 151.96, -0.07) in structuring and selling certain deals and investments during the financial crisis and housing market meltdown remains in progress. Despite the continuous questions of committee members, no real surprises have come out of the event. However, shares of GS have held steady near the neutral line, while the broader market retreats deeper into the red. DJ30 -166.49 NASDAQ -42.70 SP500 -22.00 NASDAQ Adv/Vol/Dec 580/1.38 bln/2065 NYSE Adv/Vol/Dec 498/733 mln/2534

12:00 pm : The stock market has steadied from its recent slide, but not after the S&P 500 pushed below its 20-day moving average for the first time since February. The level had held and provided price support on two occasions last week.

More than 90% of the names in the S&P 500 are now in the red. Due to broader market weakness and smaller-than-expected earnings Office Depot (ODP 7.40, -1.55) is one of the worst overall performers this session. The stock is actually on pace for its worst single-session slide by percent in nearly nine months.

In contrast, Tellabs (TLAB 8.76, +0.54) is a leader among those that have managed to stage a gain. The company posted this morning an upside earnings surprise and issued upside guidance. Shares of TLAB registered a fresh 52-week high earlier this session; only six other stocks in the Nasdaq accomplished the same feat today.

Volatility continues to spiral higher, such that the Volatility Index is now up more than 16%. DJ30 -151.07 NASDAQ -39.81 SP500 -19.90 NASDAQ Adv/Vol/Dec 691/1.17 bln/1921 NYSE Adv/Vol/Dec 582/618 mln/2399

11:30 am : The stock market is on the retreat and is now at a new session low. Selling pressure has been exacerbated by word that credit analysts at Standard & Poor's downgraded Greece's debt to junk.

The news has caused Europe's major bourses to close at session lows with losses of roughly 1.9% for Germany's DAX, 1.8% for Britain's FTSE, and 2.7% for France's CAC.

Meanwhile, the dollar is up to a new session high to trade with a 0.8% gain. Treasuries continue to garner additional support of their own, such that the benchmark 10-year Note is now up nearly one full point.

The Volatility Index has also spiked to a session high. It is now up 8.6%. DJ30 -146.39 NASDAQ -35.11 SP500 -19.43 NASDAQ Adv/Vol/Dec 1126/894 mln/1441 NYSE Adv/Vol/Dec 858/470 mln/2043

11:00 am : Selling pressure had eased in recent action, such that the Dow and Nasdaq pushed into positive terriotory and the S&P 500 came within a couple of points of the neutral line, but sellers have since redoubled their efforts with news that analysts at Standard & Poor's downgraded Portugal's ratings.

Despite the announcement, the dollar is off of its morning high. Still, it sports a 0.5% gain, most of which has come against the euro. Europe's chief currency is at 1.3310 against the dollar. That's just above its annual low.

Meanwhile, gold prices are now up 0.4% to $1158 per ounce in the face of the greenback's gain.

Treasuries also continue to tick higher. The benchmark 10-year Note is now up 15 ticks. DJ30 -10.43 NASDAQ -1.87 SP500 -2.27 NASDAQ Adv/Vol/Dec 1330/681 mln/1205 NYSE Adv/Vol/Dec 1220/358 mln/1615

10:30 am : The US Dollar Index is just under recently hit highs of 81.825 and its strength is modestly weighing on the energy markets.

June crude oil has traded in the red all session and hit session lows of $83.06 per barrel just after 5:30ET. Since then, the energy component has trended modestly higher and is at $83.44 per barrel, down 0.9%.

May natural gas has also been trading in negative territory all session, excluding a brief moment early in the overnight session. Natural gas hit morning lows of $4.19 per MMBtu about 30 minutes before pit trading began. Currently, it's trading just above that low at $4.23 per MMBtu, down 0.7%.

Precious metals hit session lows an hour and a half ago with June gold touching $1146.60 per ounce and May silver falling to $18.09 per ounce. Gold is currently just under the unchanged line at $1153.80 per ounce, while silver is down 0.4% at $18.26 per ounce.

DJ30 +5.44 NASDAQ -2.67 SP500 -2.76 NASDAQ Adv/Vol/Dec 1213/578.9 mln/1252 NYSE Adv/Vol/Dec 1429/1222 mln/1616

10:00 am : The Consumer Confidence Index for April came in at 57.9, which is well above the 53.5 that had been expected and an improvement from the 52.3 that was posted in the prior month. The April reading is the best since August 2008.

The better-than-expected reading has added to this morning's choppy trade. Losses remain broad based.

However, health care stocks have held strong in higher ground. The health care sector is now up 0.3%. Strength within the health care sector is broad as health care facilities (+2.1%), health care (+1.3%), managed care (+1.2%), and biotech (+0.7%) sport impressive gains. DJ30 -4.99 NASDAQ -6.71 SP500 -4.41 NASDAQ Adv/Vol/Dec 1111/262 mln/1247 NYSE Adv/Vol/Dec 826/155 mln/1836

09:45 am : Weakness is relatively widespread in the first few minutes of trade. More specificically, nine of the 10 major sectors in the S&P 500 are in negative territory.

Materials stocks are under the most pressure. The sector has already shed 1.2% as steel stocks sink to a 1.9% loss and shares of diversified metals and miners drop 3.1%. U.S. Steel (X 60.48, +0.41) has managed to swing to a gain, though; the company posted this morning a narrower-than-expected loss for its latest quarter.

Health care stocks make up the only sector presently in positive territory. The group is up 0.1% after it lagged in the prior session. DJ30 -6.35 NASDAQ -4.85 SP500 -4.32 NASDAQ Adv/Vol/Dec 1048/235 mln/1278 NYSE Adv/Vol/Dec 1429/1.20 bln/1616

09:15 am : S&P futures vs fair value: -7.10. Nasdaq futures vs fair value: -8.40. A firmly lower start looks to be in order for the broader market as stock futures drift to fresh morning lows as the opening bell draws closer. The relatively negative tone this morning comes amid stiff selling in both Asia and Europe, where the challenge of providing financial aid to Greece continues to keep the euro near its annual low against the U.S. dollar. The greenback is currently up 0.7% against a basket of competing currencies. Its strength has undermined another batch of better-than-expected earnings reports and outlooks from several widely-held companies, including Texas Instruments (TXI), 3M (MMM), and DuPont (DD). Paricipants have also been a bit distracted from the reports by an upcoming testimony from Goldman Sachs (GS). The testimony comes on the heels of the Senate's failure to pass last night a vote to put financial reform on track for a full vote.

09:05 am : S&P futures vs fair value: -6.40. Nasdaq futures vs fair value: -7.40. The S&P/CaseShiller Home Price Index for February hit 144.0, which is essentially in-line with the 144.8 that had been widely forecast. However, the reading is down a bit from the 145.3 that was posted in January. The 20-city composite increased 0.6% year-over-year after it had logged a 0.7% annual decline in the prior month. While the composite had been expected to show an annual increase of 1.3% in February, it was nonetheless the first rise since 2006. Stock futures have shown little reaction to the news and remain under pressure.

08:35 am : S&P futures vs fair value: -5.30. Nasdaq futures vs fair value: -5.90. U.S. equity futures remain under pressure. Overseas weakness has only weighed on sentiment. Germany's DAX is down 0.7%. Deutsche Bank (DB) is under considerable pressure, despite news that its earnings staged strong annual growth and strong sequential growth. Financial issues have also weakened France's CAC, which is off by 1.6%. BNP Paribas is under some of the stiffest pressure. In Britain, the FTSE has fallen 1.2%. Royal Dutch Shell (RDS.A) has offered some support, but BP PLC (BP) is down despite better-than-expected earnings. In Asia, mainland China's Shanghai Composite fell 2.1%. Energy plays PetroChina (PTR) and China Petroleum (SNP) were key sources of weakness. Industrial & Commercial Bank also caused a considerable drag. Hong Kong's Hang Seng fell 1.5%. Banking issues HSBC (HBC), China Construction Bank, and Industrial & Commercial Bank led losses. Of the 43 members in the Hang Seng, only China Unicom and China Resources Power finished in higher ground. Losses were more modest in the MSCI Asia Pacific Index, which closed just 0.2% lower, but Japan's Nikkei managed to gain 0.4%. Fanuc LTD was a leader as it surged 11% in its best single-session percentage advance this year.

08:05 am : S&P futures vs fair value: -4.70. Nasdaq futures vs fair value: -5.20. Stock futures are down even though quarterly earnings reports remain strong. In the latest round, both 3M (MMM) and DuPont (DD) reported a better-than-expected bottom line and raised guidance above the consensus forecast for fiscal 2010. Texas Instruments (TXI) also exceeded the consensus earnings estimate and issued an upside forecast for its second fiscal quarter. Ford (F) topped earnings expectations, while UPS (UPS) made official the earnings results that it had preannounced earlier this month. Continued strength in the dollar has acted as a bit of a headwind - the buck is up 0.7% against competing currencies this morning. Should the gain hold, the dollar will book its eighth advance in 9 sessions. Goldman Sachs (GS) is scheduled to face questioning from a U.S. Senate committee today. The S&P CaseShiller Home Price Index for February is due at 9:00 AM ET. The Consumer Confidence Index for April follows at 10:00 AM ET. Results from the Treasury's $44 billion auction of 2-year Notes are due at 1:00 PM ET.

06:55 am : S&P futures vs fair value: -6.00. Nasdaq futures vs fair value: -8.20.

06:50 am : Nikkei...11212.66...+46.90...+0.40%. Hang Seng...21261.79...-325.30...-1.50%.

06:50 am : FTSE...5687.38...-66.40...-1.20%. DAX...6278.56...-53.70...-0.90%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage