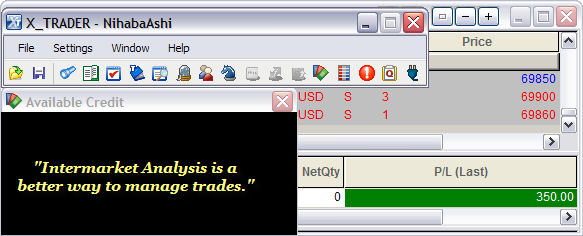

My Trading Performance:

+3.50 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

040910_wrbtrader_PnLBlotterProfit.png [ 32.29 KiB | Viewed 1473 times ]

040910_wrbtrader_PnLBlotterProfit.png [ 32.29 KiB | Viewed 1473 times ]

------------------------------

Stocks Finish Strong; Dow Touches 11,000 By Alexandra Twin, CNNMoney.com senior writer

April 9, 2010: 8:02 PM ET

NEW YORK (CNNMoney.com) -- Stocks gained Friday, with the Dow briefly topping 11,000 and the broad market ending higher for the seventh of eight weeks, as economic optimism trumped concerns about Greek debt.

The Dow Jones industrial average (INDU) added 70 points, or 0.6%, closing at 10,997. The Dow got as high as 11,000 in the final 10 minutes of trading but ended the session just short of that. Still, it was the highest close for the Dow since Sept. 26, 2008, when it finished at 11,143.13.

The S&P 500 index (SPX) gained 8 points, or 0.7%, closing at an 18-month high. The Nasdaq composite (COMP) gained 17 points, or 0.7%, ending at the highest point since June of 2008.

Stocks drifted higher through the session as investors weighed competing influences at the end of a choppy week on Wall Street.

Stocks gained Thursday as upbeat sales reports from the nation's retailers helped provide optimism about the economic outlook, taking the edge off worries about Greece and other euro-zone debt issues.

Greece's borrowing costs eased a bit after hitting a record high Thursday on worries about its ballooning deficit. Talk of a bailout as soon as this weekend circulated Friday. On the downside, ratings agency Fitch cut its outlook on Greece's debt.

Worries that Greece's default could usher in a bigger European debt crisis have popped up repeatedly this year. But the concerns have been tempered in recent weeks as investors have focused on signs that the economic recovery is picking up strength, despite ongoing weakness in the labor and housing markets.

The Dow, Nasdaq and S&P 500 have all risen in seven of eight weeks.

0:00 /3:21What Dow at 11,000 means

Among stock movers Friday, strength in energy shares gave a lift to the broad market, but it was tempered by weakness in financials. Chevron (CVX, Fortune 500), Exxon Mobil (XOM, Fortune 500), Coca-Cola (KO, Fortune 500) and Walt Disney (DIS, Fortune 500) drove Dow gains. Microsoft (MSFT, Fortune 500), Yahoo (YHOO, Fortune 500) and Intel (INTC, Fortune 500) were among the Nasdaq's big movers.

The next Greek tragedy: default or bail-out?

Economy: Wholesale inventories rose 0.6% in February after climbing 0.1% in January, the Census Bureau reported Friday. Inventories were expected to rise 0.4% ,according to economists surveyed by Briefing.com.

World markets: In overseas trading, European markets rallied in the afternoon, with London's FTSE up 1%, France's CAC-40 up 1.5% and Germany's DAX up 1.2%. Asian markets ended higher.

Bonds: Treasury prices rose, lowering the yield on the 10-year note to 3.89% from 3.90% late Thursday. The 10-year had risen as high as 4% Monday, an 18-month high. Treasury prices and yields move in opposite directions.

The dollar and commodities: The dollar fell versus the euro and the yen.

COMEX gold for June delivery rose $9 to settle at $1,161.90 per ounce.

U.S. light crude oil for May delivery settled down 47 cents to $84.92 a barrel on the New York Mercantile Exchange.

Market breadth was mixed. On the New York Stock Exchange, winners beat losers two to one on volume of 971 million shares. On the Nasdaq, advancers edged decliners by seven to six on volume of 2.12 billion shares.

Yahoo! Finance

Yahoo! Finance 4:30 pm : Most of this session was spent in choppy trade with modest gains, but a late flurry of buying boosted the stock market to its best intraday levels and highest close since September 2008.

Stocks spent the majority of the session broadly higher, but overall gains were held in check amid persistent wariness about the financial health of Greece. Those concerns became more real when analysts at Fitch downgraded Greece's debt rating to BBB-, but shortly thereafter Reuters reported that eurozone finance officials have reached a deal on how to provide loans to Greece if they are needed.

Though actual help to Greece could strain the coffers of other European Union members, the euro rallied. Its strength drove the Dollar Index down to a 0.7% loss.

Despite such pronounced weakness in the dollar, gains in the broader market remained contained until the close came within reach. However, a late surge in buying sent stocks to fresh 52-week highs in the face of suggestions that the stock market is near-term overbought. The Dow even kissed 11,000, but it settled just a few points below the widely-watched line.

Advancing issues outnumbered decliners in the Dow by 4-to-1. Chevron (CVX 79.50, +1.84) was a primary leader after it issued an upbeat interim update. That helped it fight off softer crude oil prices, which settled 0.6% lower at $84.85 per barrel and lead the broader energy sector to a 1.1% gain.

Alcoa (AA 14.39, -0.48) was a laggard among blue chips. The stock was downgraded by analysts at JPMorgan.

While stocks finished at session highs with broad-based gains, the move still wasn't as strong as what was booked overseas. Specifically, the Dow Jones World Index, excluding the US, finished Friday 1.2% higher. However, the S&P 500 finished the week with a 1.4% gain, which marked its sixth straight weekly advance. The Dow Jones World Index Ex US finished the week a more modest 0.8% higher, its second straight weekly gain.

Advancing Sectors: Energy (+1.1%), Telecom (+0.9%), Consumer Discretionary (+0.9%), Tech (+0.8%), Utilities (+0.6%), Consumer Staples (+0.6%), Financials (+0.5%), Industrials (+0.5%), Health Care (+0.4%), Materials (+0.3%)

Declining Sectors: (None) DJ30 +70.28 NASDAQ +17.24 NQ100 +0.7% R2K +0.5% SP400 +0.9% SP500 +7.93 NASDAQ Adv/Vol/Dec 1454/2.11 bln/1198 NYSE Adv/Vol/Dec 2053/968 mln/968

3:35 pm : Equities have trended upward in a narrow range this session. Energy is providing the most substantial leadership, currently up 1.0%.

Strength in energy commodities was led by natural gas. Natural gas futures reversed yesterday's steep losses (following another inventory report which added to bearish fundamentals yesterday morning) with a sharp gain. May natural gas closed 4.1% higher at $4.07 per MMBtu.

May crude oil, on the other hand, trended lower all morning. After hitting a session low at $84.12 per barrel, it closed 0.6% lower at $84.85 per barrel.

Gold and silver futures fared well as the dollar index was particularly weak this session. May silver opened the pit session higher and closed up 1.3% at $18.37 per ounce. June gold retreated to the flat line after opening with marginal gain. June gold then spiked to a session high at $1165.80 per ounce before closing at $1162.00 per ounce, up 0.8%. DJ30 +45.42 NASDAQ +13.37 SP500 +5.67 NASDAQ Adv/Vol/Dec 1349/1.75 bln/1270 NYSE Adv/Vol/Dec 1891/689 mln/1098

3:00 pm : Modest, but broad-based gains remain as stocks head into the final hour on light trading volume. Light volume has become a consistent theme in recent weeks. Over the previous four sessions volume on the NYSE has averaged just over 1 billion shares, which is below average of 1.2 billion shares per session during the past 200 days. DJ30 +38.39 NASDAQ +11.11 SP500 +4.76 NASDAQ Adv/Vol/Dec 1341/1.62 bln/1285 NYSE Adv/Vol/Dec 1841/643 mln/1147

2:30 pm : Though there hasn't been a clear path for stocks to follow this session, the tone of trade has been positive since the opening bell.

Gains have been relatively broad based, but modest. Gains have also lagged those registered abroad -- the S&P 500 is up less than 0.4%, while the Dow Jones World Index Excluding the US advanced 1.3% in the final session of the week. However, the World Index Ex US advanced 0.9% this week and the S&P 500 is currently up 1.1% week-to-date. DJ30 +34.69 NASDAQ +9.38 SP500 +4.19 NASDAQ Adv/Vol/Dec 1308/1.48 bln/1322 NYSE Adv/Vol/Dec 1819/595 mln/1138

2:00 pm : The materials sector continues to weaken. It is now down 0.4%. Steel has been a primary source of weakness this session. In particular, US Steel (X ) has fallen sharply. It has fallen 10% since it registered a 52-week high just three days ago.

Financials have also fallen into the red. The sector is down 0.1% as the likes of JPMorgan Chase (JPM 45.56, -0.20) and Bank of America (BAC 18.52, -0.13) come under increased pressure. DJ30 +24.18 NASDAQ +7.43 SP500 +2.84 NASDAQ Adv/Vol/Dec 1304/1.38 bln/1324 NYSE Adv/Vol/Dec 1744/555 mln/1211

1:30 pm : Stocks recently drifted off of session highs to trade with a more modest gain. The slide came withouth any major catalyst, but it has left the materials sector in the red -- materials stocks currently contend with a 0.2% loss while the other major sectors sport varied gains.

Oil prices have come under pressure in recent action, such that crude oil is now priced 1.2% lower at $84.40 per barrel. Despite softer oil prices, the energy sector continues to outperform the broader market with ease. Energy stocks are up 0.9%, collectively. DJ30 +36.50 NASDAQ +9.64 SP500 +4.11 NASDAQ Adv/Vol/Dec 1342/1.26 bln/1261 NYSE Adv/Vol/Dec 1827/515 mln/1122

1:05 pm : Stocks have spent the entire session stuck in choppy trade, but they still managed to push to a fractionally improved 52-week high. Though gains have faded in recent trade, strength has been largely underpinned by a weaker dollar.

The general mood among market participants this session has been positive since the opening bell, though stocks spent the first couple of hours without clear direction. Energy stocks, which are up 1.1% at the moment, provided an early source of support. The sector has been led by integrated oil and gas outfits after Chevron (CVX 79.17, +0.94) issued an upbeat interim update.

The stock market got a broader boost by a downturn in the dollar, which is currently down 0.6% against a basket of competing currencies. Its weakness primarily hinges upon the euro, which has rallied amid word from Reuters that eurozone finance officials have reached a deal on terms of possible loans to Greece. That report followed news that analysts at Fitch downgraded Greece's debt rating to BBB- and have a negative outlook.

Though a deal to help Greece has reportedly been put into place, there are lingering concerns regarding the implications of actually providing the country with aid since it would drain the coffers of fellow European Union members. Such consideration has held in check the enthusiasm of market participants this afternoon.

Stocks have also had difficulty extending their gains to more than incrementally improved 52-week highs. That sort of struggle has provided fodder for market analysts who believe stocks are overbought in the near term.

However, this session's gains have come without any real help from the financial sector, which has been one of the stock market's frequent leaders. Financials faltered in the early going, but managed to make a modest recovery. The sector is up just 0.1% at the moment.

Economic data was limited to a wholesale inventory report for February. Inventories increased 0.6% more than expected and the balance for January was revised higher to show a slight increase. The data was paid little attention by market participants, though. DJ30 +41.49 NASDAQ +8.67 SP500 +3.99 NASDAQ Adv/Vol/Dec 1319/1.18 bln/1266 NYSE Adv/Vol/Dec 1796/485 mln/1132

12:30 pm : The Dollar Index remains down 0.6%, near its session low. Its weakness comes primarily as a result of a rally in the euro, which is up 0.9% against the greenback even though analysts at Fitch downgraded Greece's debt rating to BBB- with a negative outlook. According to Dow Jones, the downgrade reflects the intensification of fiscal challenges in response to more adverse prospects for economic growth and increased interest costs. That headline was quickly followed by word from Reuters that eurozone finance officials have reached a deal on terms of possible loans to Greece. Though that is a positive for Greece, such support would add stress to the countries providing aid, should it be needed. DJ30 +51.77 NASDAQ +10.25 SP500 +5.52 NASDAQ Adv/Vol/Dec 1375/1.08 bln/1188 NYSE Adv/Vol/Dec 1876/446 mln/1040

12:00 pm : The dollar has extended its slide so that it now trades with a 0.6% loss against a basket of foreign currencies. That drop helped the stock market extend its gains to a fresh session high, which also marked a fractionally improved 52-week high. Stocks have since eased back a bit.

Meanwhile, commodities are mixed. Despite weakness in the buck, the CRB Commodity Index has only managed to muster a mere 0.2% gain. Natural gas prices are sharply higher, however; they were last quoted at $4.07 per MMBtu,up 4.3%. DJ30 +49.12 NASDAQ +8.71 SP500 +5.05 NASDAQ Adv/Vol/Dec 1334/980 mln/1203 NYSE Adv/Vol/Dec 1831/408 mln/1070

11:30 am : Stocks remain stuck in choppy trade, but a recent upward push has put the Dow and Nasdaq at fresh session highs. The S&P 500 has yet to push past the highs that it set this morning, though.

Financials recently fell to a modest loss, but they have since rebounded to a 0.3% gain. Insurers have been a primary source of strength to the sector, but investment banks like Goldman Sachs (GS 179.26, -0.24) have lagged.

Of the major sectors, utilities are the weakest. The sector is down just 0.1%, but it is the only sector that has so far failed to find positive territory. With a 3.6% year-to-date loss, relative weakness isn't anything new for the defensive-oriented sector -- only telecom's 5.2% year-to-date loss is worse. Electric utilities like Exelon (EXC 44.09, -0.34) and Dominion (D 41.14, -0.33) have weighed heavily on the sector this session and in recent weeks. DJ30 +51.24 NASDAQ +8.07 SP500 +5.05 NASDAQ Adv/Vol/Dec 1296/868 mln/1214 NYSE Adv/Vol/Dec 1750/368 mln/1107

11:00 am : Stocks have become caught up in some whipsaw-like trade. Specifically, the S&P 500 bounced up from an opening slip to challenge its 52-week high, but it then retreated back to earlier lows only to stage another recovery. The latest move has left stocks to trade with modest gains.

Though there have already been plenty of swings, the extent of the moves has been somewhat limited in that the S&P 500 has remained within a five-point range so far this session. Additionally, the Volatility Index is actually down 0.8%. DJ30 +25.54 NASDAQ +3.44 SP500 +2.12 NASDAQ Adv/Vol/Dec 1193/723 mln/1278 NYSE Adv/Vol/Dec 1592/313 mln/1246

10:30 am : The dollar index fell to new session lows in recent trade, which gave a boost to most commodities.

May crude oil has traded in positive territory all session, but has been on an overall downtrend since hitting highs of $86.37 per barrel overnight. Crude did receive a modest boost from the dollar index's decline, but it remains modestly higher at $85.51 per barrel, up 0.1%.

May natural gas trended higher for most of today's session. Natural gas dipped modestly around the open of pit trading, but that was short-lived. In recent trade, the energy component pushed to fresh session highs of $4.03 per MMBtu and is currently 3.2% higher at $4.03 per MMBtu.

Despite weakness in the dollar index, June gold was moving lower until recent activity. Just before the top of the hour, gold briefly fell into the red, but has since moved back into positive territory and is currently 0.2% higher at $1155.70 per ounce. May silver is showing more strength today than gold. Silver broke into positive territory overnight and has remained there since. Highs of $18.41 per ounce were hit in recent activity and currently silver is trading just under that level at $18.38 per ounce, up 1.4%. DJ30 +14.21 NASDAQ +3.06 SP500 +1.12 NASDAQ Adv/Vol/Dec 1111/531.4 mln/1289 NYSE Adv/Vol/Dec 1471/234.1 mln/1279

10:00 am : Stocks have bounced back from a recent slip that took the S&P 500 close to the unchanged line and the Nasdaq Composite to a slight loss. Though the move has been broad based, energy stocks continue to trade with the most strength -- the sector is now up 1.0%.

Wholesale inventories for February were just released. They increased 0.6%, which is slightly stronger than the expected increase of 0.4%. Inventories for the prior month were revised upward to reflect an increase of 0.1% from a decrease of 0.2%.

Advancing Sectors: Energy (+1.0%), Telecom (+0.8%), Financials (+0.6%), Industrials (+0.4%), Health Care (+0.4%), Consumer Staples (+0.3%), Materials (+0.3%), Tech (+0.2%), Consumer Discretionary (+0.1%)

Declining Sectors: Utilities (-0.4%) DJ30 +34.76 NASDAQ +2.82 SP500 +4.06 NASDAQ Adv/Vol/Dec 1058/334 mln/1258 NYSE Adv/Vol/Dec 1508/163 mln/1161

09:45 am : Stocks chopped around in the first few minutes of trade, but the major indices have started to push downward from moderate, broad-based gains. The downturn comes even though the dollar has retreated to a fresh morning low, where it trades with a loss of 0.4% against competing currencies.

Energy has displayed relative strength, however. The sector is up 0.8% at the moment. Its underlying strength spans from oil and gas equipment companies to refiners. Integrated outfit Chevron (CVX 78.60, +0.94) is up sharply after an upbeat interim update.

Retailers are on the retreat after a strong showing in the prior session. As a group, retailers are down 0.6%. DJ30 +17.83 NASDAQ -2.44 SP500 +1.44 NASDAQ Adv/Vol/Dec 868/248 mln/1389 NYSE Adv/Vol/Dec 1228/126 mln/1386

09:15 am : S&P futures vs fair value: +2.00. Nasdaq futures vs fair value: +3.80. Stock futures suggest a slightly higher start for this week's final session. That would add to, or at least help lock in place, the stock market's week-to-date gain, which currently stands at 0.7%. The S&P 500 has already booked six straight weekly gains. Though that stretch is certainly suggestive of a bullish trend, stocks have had an increasingly difficult time setting new highs. Such difficulty has given way to calls that the stock market is overbought in the near term. Of additional concern is the continued uncertainty related to the fiscal health of Greece. While European Central Bank President Trichet has helped quell some of that concern with statements that Greece is not in a position to default, many remain wary if not skeptical, especially as ministers of the European Union remain bent on producing a specific plan that could provide emergency aid to the country. Aside from the headlines from Greece, overall news flow has been slow and economic data has been absent. There is a wholesale inventory report due at 10:00 AM ET, though.

09:00 am : S&P futures vs fair value: +2.80. Nasdaq futures vs fair value: +4.80. Only a few morsels of corporate news are out this morning. Among them, Reuters reported that Boston Scientific (BSX) is looking to divest its Target Therapeutics and Advanced Bionics units. Constellation Brands (STZ) posted an upside earnings surprise for its latest quarter, but issued a downside forecast. Meanwhile, Chevron (CVX) issued an interim update that indicated the company expects earnings for its first fiscal quarter to exceed those generated in the fourth quarter.

08:35 am : S&P futures vs fair value: +3.50. Nasdaq futures vs fair value: +5.50. U.S. stock futures continue to trade with a narrow edge over fair value. The mood abroad appears to be stronger. As such, Germany's DAX is up 0.9%. Of its 30 members, only Allianz (AZ), Volkswagen, and Man SE are in negative territory. According to reports, German exports rebounded to a 5.1% increase in February. That beat the consensus call for a 4% increase. Michelin is the only component of France's 40-member CAC to trade in the red. Such broad-based strength has the CAC up 1.3%. Britain's FTSE is up 0.8% as HSBC (HBC) leads advancers on a 6-to-1 advantage over declining issues. Meanwhile, the continent's chief currency, the euro, has gained modestly against the greenback as headlines suggest that Greece is not in danger of defaulting, but that European Union ministers continue to pursue plans for a potential bailout. Greece has announced plans to auction later this month a series of 12-month Bills. The auction will likely measure the appetite for the country's short-term debt. In Asia, the MSCI Asia Pacific Index eked and Japan's Nikkei both closed 0.3% higher. The modest advance came despite efforts of profit taking in the wake of a recent rally to 18-month highs. However, exporters were hit hard. In Hong Kong, the Hang Seng climbed 1.6% as many considered the implications of appreciation in the yuan. Such consideration was particularly helpful to shares of Air China. In mainland China, the Shanghai Composite added 0.9%. New listings were in favor.

08:00 am : S&P futures vs fair value: +3.20. Nasdaq futures vs fair value: +5.80. The euro has added modestly to its upward move in the prior session as the latest lot of headlines about Greece suggests that the country is not in danger of defaulting and that it plans to auction a series of 12-month Bills later this month. Still, European Union ministers continue to pursue plans for a potential bailout. Europe's major bourses have also gained. That, along with a slightly weaker dollar, has helped give a modest lift to stock futures.

The only item on today's economic calendar is a wholesale inventory report for February at 10:00 AM ET. The report is unlikely to have any major influence over trade, however. There are no Fed speakers today.

06:45 am : S&P futures vs fair value: +3.10. Nasdaq futures vs fair value: +5.00.

06:45 am : Nikkei...11204.34...+36.10...+0.30%. Hang Seng...22208.50...+341.50...+1.60%.

06:45 am : FTSE...5754.14...+41.50...+0.70%. DAX...6223.16...+51.40...+0.80%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage